Search News Results

Report pushes for levy on imports in regional blocs

Regional blocs including the East African Community (EAC) should introduce a levy on imports to help self-finance its organs, a new report suggests.

The regional entities have depended solely on contributions from members yet a number of countries have not been meeting their obligations.

A report by the African Capacity Building Foundation (ACBF), a financier of research institutions in Africa for over a decade, said a country facing an economic crisis or catastrophe finds it difficult to pay dues.

ACBF said integration schemes such as EAC and the Common Market for Eastern and South African have copied the Eurozone model of regional groupings that depend on member contributions.

“A funding mechanism that combines national contributions with independent revenues, such as import levies, would go a long way to helping African regional economic communities become financially independent,” said the report.

However, analysts said clarity would be needed on how such a tax is to be implemented because some of the countries may fail to co-operate since the blocs do not have tax collection machinery.

“It is very good to have an alternative method of financing regional initiatives such as those we are party to. But the tax also has to be collected by someone. Who is it that would collect it?” asked Joseph Kieyah, principal policy analyst at the Kenya Institute of Public policy Research and Analysis.

Prof Kieyah said the levy alone would not achieve much unless there are willing participants in regional integration schemes. He said the citizenry and the private sector would need to be closely involved for buy-in.

“What we need is to drive integration from the bottom rather than from the top as has been the case all along. Citizens need to be sensitised about the importance of the regional integrations schemes so that they can get leaders to act,” he said.

In the EAC there have been divisions over pace of integration. The ACBF reports that obstacles to stronger blocs include the lack of enforcement mechanism for its decision, lack of citizen awareness as well as low human resource capacity in the groupings.

In the areas of human resource, the report notes shortfalls in contrast to the EU that has employed about 30,000 staff, two-fifths of whom are involved in policy design, implementation, and monitoring and evaluation.

Related News

Lawmakers push for transparency in mining

Participants at the just concluded global seminar on the role of parliaments in the development of extractive industries have committed to ensure that the mining sector in Africa help the continent become self-reliant through their oversight role.

This was one of the resolutions at the conclusion of the three-day meeting at the Parliament Building in Kigali, on Thursday.

“We believe that legislators can play an important role in creating viable oversight mechanism to monitor the collection and use of revenues from extractive industries, and in ensuring that the interests of citizens are taken into account during the allocation and disbursement of revenues collected by governments,” Speaker of Parliament Donatile Mukabalisa said in her closing remarks.

Held under the theme, “Transparency and Accountability in Extractive Industries: The Role of the Legislature,” the meeting was organised by the Commonwealth Parliamentary Association, the International Monetary Fund (IMF), the World Bank Institute (WBI), among other partners.

The seminar aimed to discuss ways in which legislators can be part of the transformation of the mining sector while ensuring that the revenue generated in the industry is put to good use for sustainable development.

The meeting brought together about 50 participants from Australia, Cameroon, DR Congo, Cameroon, Seychelles, Uganda, Niger, Nigeria, Tanzania, Zambia and host country Rwanda.

It was observed during discussions that economies that are overly dependent on oil and other mineral wealth have often encouraged dictatorial rather than democratic form of governance.

Mitchell O’Brien, World Bank’s governance specialist, on Tuesday noted that even though many developing countries are endowed with natural resources, they remain marred with challenges that have made it difficult for them to utilise these resources to reduce poverty.

“It is unfortunate that instead of contributing to poverty reduction and economic growth, these natural resources are a source of corruption and other related consequences, like conflict and wars. As legislators, let’s work together to influence good governance characterised by accountability, transparency in the utilisation of these resources for the social welfare of the citizens,” Mukabalisa added.

It was recommended that revenues from oil, gas, and mining should rather be used to spur economic growth and social development, rather than being the centre of conflict and civil wars, especially on the continent of Africa.

Peter Tinley, member of the Western Australia Legislative Assembly, said issues related to natural resources have at times been interpreted as a “curse”.

And to put end to the curse, Tinley suggested that proper, transparent, fiscal and production linkages along with consumption linkages are the four pillars that would determine how the revenues generated from the resources would flow to the communities to serve the benefits of all.

In their resolutions, the delegates committed to ensuring financial transparency in the extractive industries through budget ratification process to ensure that dividends benefit the community, as well as use of effective parliamentary oversight tools to enhance accountability of the extractive sector, and improve natural resource governance through enhanced political consensus.

Related News

AfDB partnership with CSOs to spur development in Africa

A committee comprising the African Development Bank and Civil Society Organizations (CSOs) has been relaunched with the aim of fostering partnership between the two players in order to enhance development on the continent.

The committee, reintroduced at a two-day meeting between the Bank and CSOs will discuss a work plan, modalities of its implementation as well as an accountability structure. “CSOs are our integral partners especially in the promotion of accountability, transparency and good governance. Accountability is key in terms of achieving our objective, and we could certainly do with an external reporting tool especially from CSOs,” Rakesh Nangia, Chair of the committee, said as he opened the meeting on January 14 at the Bank’s headquarters in Abidjan, Côte d’Ivoire.

Addressing the participants, who included regional civil society heads and representatives of key sectors within the Bank, he reiterated the importance of strengthening engagement with CSOs. “The Bank recognizes and values the expertise and contributions of CSOs, which are essential in achieving sustainable development in Africa,” said Nangia, who is also the Evaluator General of the Bank’s Independent Development Evaluation department (IDEV).

His remarks were echoed by Mamadou Goita, Chair of the Civil Society Coalition, who described the role of civil society as crucial in helping the Bank to frame projects that would be more relevant to communities. “We need to be involved from the first stage of designing a project because we know the context of our various communities. We can then help follow through to the implementation, monitoring and evaluation stages,” Goita said.

He cited the recent Ebola response saying civil society organizations would have been approached to help in framing the nature of the Bank’s assistance. “We are the ones on the ground and we know the specific needs on the ground; if it is support in getting skilled care, drugs, or even building new hospitals, among others.” In August last year, the Bank approved a US $60-million grant to help strengthen West Africa’s public health systems in a bid to address the Ebola crisis.

The issue of engaging with CSOs from fragile states came into focus with recommendations of sustainable funding and long-term institutional development of the organizations, including capacity building.

However there were calls for a range of CSOs (international and local) in fragile states to work together in order to strengthen delivery of services. “International NGOs may not be able to intervene on the ground without involvement of grassroots NGOs. Both need to collaborate and ensure results,” noted Baboucarr Sarr, the Lead Regional Fragility Coordinator in the Bank’s Transition Support Department. This, he said, was a key lesson learnt while working in the Horn of Africa.

The AfDB-CSOs partnership is guided by the Framework for Enhanced Engagement with Civil Society Organisations, which is in line with the Bank’s Ten Year Strategy (2013-2022).

Related News

Financing transit-oriented development with land values

Cities in developing countries are growing at a rapid pace. However, the associated positives of strong economic growth and rising real incomes have come with the negatives of low-density sprawl, traffic congestion, air pollution and greenhouse gas emissions, and lack of mobility for already marginalized populations.

Studies have shown that transit-oriented developments – typically higher density, mixed-use developments located around a transit station – are one of the most effective means of addressing these negative externalities of rapid urbanization. However, transit infrastructure is extremely costly and thus difficult to prioritize in cities where there are many other competing demands for funds.

Financing Transit-Oriented Development with Land Values proposes the use of “development-based land value capture” mechanisms to help overcome this financial hurdle. Coupled with supportive land use regulations, development-based land value capture (LVC) helps “capture” property value increases due to transit investments.

This revenue can in turn be used to help cover the cost of transit infrastructure and maintenance, and agreements for development rights transfers can include provisions such as services and facilities for low-income groups.

Development-based land value capture methods highlighted include:

-

Land development sale/lease: governments sell or lease development rights or land that is appreciating due to transit investments.

-

Partnerships between transit agencies and developers: developers contribute money or property to build station facilities that will attract people to do their businesses.

-

Air rights sale: governments sell additional development rights to developers interested in building more.

-

Land readjustment: landowners pool their land, which facilitates the sale of a portion for transit-oriented development-related investments.

-

Land consolidation and urban redevelopment: in more complex scenarios, landowners partner with private developers to consolidate their land and develop multi-purpose projects.

Benefits of using development-based land value capture:

-

Promotes and supports transiti-oriented development

-

Based on the concept of creating and sharing value

-

Helps cover the cost of transportation infrastructure

-

Businesses, products, and services are more closely located and accessible

-

Promotes inclusive development by improving mobility and access for all

-

Shows private entities that sustainability is profitable

-

Reduces pollution and unsustainable land development

Financing Transit-Oriented Development with Land Values uses a unique case study method to identify opportunities and pitfalls from experiences in Hong Kong SAR, Tokyo, New York City, Washington, D.C., London, Nanchang, Delhi, and Hyderabad.

Infographic (click to enlarge)

» Download the report: Financing transit-oriented development with land values: adapting land value capture in developing countries (8.06 MB).

Related News

Angola and China open Atlantic to African neighbours

The Benguela Railway was once Angola’s bloodline, carrying goods to and from the interior of the country, and onwards to Zambia and Zaire (now the Democratic Republic of Congo). Its profit posted in the last full year of business in 1973 was the equivalent of more than US$ 6 million dollars. The railway meant far more than just money, however, boasting a long and complex history.

Memories of the railway

The name of the Benguela Railway still resonates today, along with that of its promoter, Scotsman Robert Williams, friend of Cecil Rhodes, a pioneer in European exploration in Africa. “Benguela is the natural starting point for a railway to transport ore. I ask you to help me build the line and I will make Lobito a more important port than the one in Lourenço Marques” (now Maputo, in Mozambique), the entrepreneur told the Portuguese Ambassador in London in 1902.

This story still abounds with legends and images of long trains whose wagons are heaving with goods, ripping through the bright red earth of the Angolan highlands. It also brings up more dramatic memories, of the wreckage of once stately bridges shattered in the canyons during the war.

The railway line covered almost 1,350 kilometres, broken up by 67 stations. The line served as a bridge between the Angolan Atlantic and some of the richest mining areas in the world. It was impassable along its entire length for almost 40 years. Until now.

Today it is the most important of three railways that, with technical and financial support from China, promise to take trade and development into the heart of Angola … and of Africa.

Continued potential

About 85 years after the construction of the Benguela Railway, it’s potential is still intact. Nowadays it is even more valuable. The railway was initially intended to be the shortest route for export of ore from the region of Katanga (southern Congo) and the Copperbelt (Northwest Zambia) − through the port of Lobito. But the line also passes through agricultural areas with great potential.

Renowned Angolan academics Regina Santos, Ana Duarte and Fernando Pacheco have spearheaded research on the Lobito Corridor, producing several publications. They believe that the “unique” features of the Benguela Railway could be reproduced today. They told Macao magazine that the Lobito corridor crosses through 12 to 20 million hectares of arable land, with excellent potential for grazing and good access to water, plus about 150,000 hectares of eucalyptus plantations. Less than ten percent of this arable land is worked, and agro-industry is still rare.

All this points to the agricultural potential of Angola in general, but of the Benguela Railway in particular, to carry agricultural produce, for domestic demand and export through the Port of Lobito, they say. According to the academics, the explored area could be extended to around 250,000 hectares, including forestry. There is also indigenous forest in the provinces of Lunda Sul and Moxico offering potentially high income levels.

At the eastern end of the railway, in Moxico province, near the border with the Democratic Republic of Congo, is the famous bridge over the River Kasai. Just over the border is the province of Katanga. It is estimated that in Katanga alone deposits of copper and cobalt account for 40 percent and 50 percent of the world’s total reserves, respectively. Not coincidentally, the recovery of this railway line was considered in 2011, a key part of the Master Plan for Transportation in the Southern African Development Community (SADC).

Multiple benefits

“The awakening of the Benguela Railway is still very important as it is multimodal − offering transport between Angola, DRC and Zambia − and strategic, because it is the shortest and cheapest route from landlocked SADC countries to the markets of Europe and the US,” the Angolan researchers say.

Last year, the Angolan Ministry of Transport estimated that in 2015 the Benguela Railway would carry 20 million tons of goods. This would require the railway to attract the flow of Zambian and Congolese minerals for export. At the moment most of these goods are transported through South African ports, 8,000 miles away.

The refinery under construction in Lobito has the capacity to process 200,000 barrels of oil per day, creating the potential for another major stream: exports of Angolan fuels to neighbouring countries by land. This is a business worth millions of dollars and of strategic importance to the Angolan authorities.

The railway would facilitate transporting goods and attracting investment, as well as improving transport facilities for people in the region. It would also have an important role to play in economic growth in Angola and neighbouring countries. Following on from this, according to the researchers, “The integration of the transport and communication network would be facilitated at the regional level, allowing Zambia to import products directly from Angola, such as oil, and connect to the sea through the port of Lobito.” Once the Lobito Corridor is fully operational it “will enable further development of Zambia, re-launching sectors such as copper production, agriculture and the creation of joint ventures between businessmen of the two countries”. Angola, the researchers say, could become a “regional hub, given its privileged location, including its ports, particularly in terms of international trade”.

Luís Bernardino, Doctoral Researcher at the Centre for International Studies of the University Institute of Lisbon (CIS-IUL), says, “Angola has had a good strategic vision by focusing on creating communication routes, and will become an economic hub in the sub-Saharan region.” He continues: “The southern Atlantic Ocean is the future … one where the main commercial routes will be located in the future. And Angola is geo-strategically well positioned to be a regional power in central and south-south trade.” For neighbouring countries this is a golden opportunity.

Rebirth of ports

The focal point of this corridor will be the Port of Lobito, which has been modernised and expanded with a container terminal, an ore terminal and another one for fuel. Work was carried out by the China Harbour Engineering Company. The port’s current capacity of 3.7 million tons of cargo per year will be increased to 4.1 million tons when the Benguela Railway, rebuilt by China Railway Construction, is working at full capacity.

Lobito-born Eugenio Costa Almeida, an Angolan researcher at CEI-IUL (Centre for International Studies, ISCTE-IUL), notes that this port has the potential to be the most important in West Africa. “The economic reality is that there is excellent dovetailing between railways and ports,” he tells Macao magazine.

The Angolan government’s project has always involved the reconstruction of the railway. But now it is expanding to include a wider set of infrastructure initiatives designed to support growth and development of areas of high potential. The corridor project includes the international airport of Catumbela and others, plus A roads and highways to complement this. In Luau on the border with the DRC a new international airport is under construction. A container depot and warehouses will also be built soon.

“The development of the railways in general and the Benguela Railway in particular, will not only boost the development of Angola and its neighbouring countries through raw materials, fuel and food at lower and more affordable prices, but will also allow further development of areas around the railways. In the case of the Benguela Railway, it will increase the economic and territorial expansion of the port of Lobito with the return − due to being closer and cheaper − of minerals and raw materials produced in the DRC and Zambia,” says Costa Almeida.

Three great railways

Ports are also the essential end points of two other railways: the Luanda Railway (CFL), rebuilt by China Railway 20, and the Moçâmedes Railway (CFM) in the hands of China Hyway. The regions and populations served by these facilities are also expecting a boost to development.

The Luanda Railway focuses on transporting people, particularly between Luanda and Viana. Although in the case of the Benguela Railway economic activity is still in its infancy, further north there is already significant business activity. In Malanje province, for example, the municipality of Cacuso has received significant public and private investments. These include the Capanda Dam and the adjacent Agro-Industrial Perimeter, which currently houses four agro-industrial companies, one with Chinese technical assistance. There is also the Biocom project, which is already producing sugar and electricity. In this case the partnership is between Odebrecht (Brazil), Sonangol (Angolan state company) and private Angolan company, Damler. Other projects are planned for the region and it is believed that the train will be a huge boon.

In the region of the Mocâmedes Railway, there are plans for iron ore exploration in Cassinga, Huila Province, as well as potential areas for mining in Kwando Kubango Province. Costa Almeida notes that the railway line should stretch south to Namibia, “which along with passing through some of the best mining centres in the country and with the development of the port of Namibe, would strongly develop this railroad.”

The development plan of Angola’s Integrated Railway System provides for the connection of the three lines to the rail networks of neighbouring countries. The Benguela Railway would connect to Zambian Railways, through a special branch line starting at Luacano station, in Moxico province, and the new Lumwana line, under construction in Zambia. The Moçâmedes Railway should connect to the Namibia railway system, starting from Cuvango station, stretching over a distance of 343 kilometres, as far as Oshikango in Namibia close to the border with Angola’s Cunene province. A study is underway for construction of the Congo Railway, which will link Luanda to the provinces of Bengo, Uige, Zaire and Cabinda, over a distance of 950 kilometres, linking up later with the Chemin de Fer du Congo Ocean, in Congo Brazzaville.

Another idea that has been mooted, “perhaps in the very long term” is the “perpendicular connection of the three great” railroads. “That would be the icing on the cake,” the researcher says.

Public-private partnerships?

Angola’s government over the last 12 months has given out signs that private companies may have a role in the development and management of these facilities. The move has been welcomed by analysts. The Economist Intelligence Unit (EIU) in a recent report said, “These potentially valuable assets are not to be handed over too cheaply, or delivered to firms without the capacity to be successful.”

The government is considering the merger of three railway companies, into a new public company, Caminhos de Ferro de Angola (Railways of Angola), with operational and commercial activities handed over to private companies. According to Costa Almeida, privatisation raises doubts: “Sometimes, and not infrequently [privatisation] is the best solution for good and better management of public affairs.” He cautions, however, that you need to discuss what kind of privatisation you are looking at − complete privatisation or just management?

Loro Horta, an academic researcher and diplomat based in Beijing, notes that these are strategic assets, so any privatisation requires “great care”. However, he adds that “partnerships in which the Angolan government and foreign companies work together can be, in my humble opinion, the best option”.

Outlook for China-Angola relations

The project for reconstruction of the main railway lines in Angola, by the China Railway Engineering Corporation, started in 2005 at a time when Angola had difficulty accessing financing, at an estimated cost of US$ 3.5 billion. The triple project was the main recipient of funds that China made available to the Angolan government.

Nowadays, three parallel connections are fully restored: the more than 900 kilometres between the port of Namibe and Menongue near the Cassinga iron mine; 540 kilometres from Luanda to Malanje, a diamond area; and almost 1,400 kilometres of the Benguela Railway. The focus now is on ensuring a quality service to drive growth and development.

The completion of the work opens up new areas for cooperation between Luanda and Beijing, which is investing heavily in railways in Africa. Work is about to begin on a US$ 3.8 billion-euro project financed by China’s Exim Bank to rebuild the East Africa Railway, connecting the port of Mombassa, in Kenya, to South Sudan, via Uganda, Rwanda and Burundi. The electric railway between Addis Ababa and Djibouti, and railway networks in Chad and Nigeria are also under construction.

Luís Bernardino said that China has a policy for the entire continent, investing in strategic sectors which impact on their interests, such as access to raw materials. Credit lines “are quite attractive for the Angolan government” and are “in key strategic projects” in the country. “I think we will continue to witness the presence of Chinese investment in Angolan soil for many years,” he added.

Regina Santos, Ana Duarte and Fernando Pacheco note the importance of the strategy for the transport sector, which is “imperative to create growth in other sectors”. These include agriculture, construction and real estate, to which “Chinese companies, some of which are private and already deployed in Angola, also make their contribution”.

“The Government continues to believe that relations between the two countries should go forward, given the multiple cooperation agreements, memorandums of understanding in various fields such as energy, telecommunications, education, culture, agriculture, etc. That is, everything points to both Angola and China seeing each other as strategic allies,” the researchers say.

According to Costa Almeida, the two countries have already shown that their relationship goes far beyond railways. “Just recently President Eduardo dos Santos visited two large industrial areas built entirely by the Chinese − a cement factory and a beer company − which will keep the Chinese managers and trainers in these companies for a long period,” he says. “Alongside this there are highways that continue to receive Chinese funding and there will be other areas where the Chinese can remain in Angola.”

Loro Horta notes that ties between the two countries are still at their strongest in the oil and gas sector. Now infrastructure “can be considered the second most important economic area”.

“China is now probably the most advanced nation in terms of railways and has supported many countries in developing their connections; inter-regional trade remains relatively small, and the railway can change that,” he says. “If these railways are planned as part of a wider system of infrastructure and economic activity, they have the potential to integrate the economies of southern Africa in a way that has never been seen before.”

Related News

Kenya signs Sh25 billion deal with Japan for Mombasa port expansion

Japan will on Friday advance to Kenya a Sh25 billion loan to fund the second phase of Mombasa port expansion.

The money, to be given through the Japan Bank for International Corporation (JBIC), is earmarked for the construction of a new container terminal by reclamation of the West Kipevu to create an additional 3 berths.

“The proposed project includes construction of a new port access road connecting the new container terminal with the existing Port Reitz Road that leads to Nairobi and inland bound highways,” the project document reads.

The money is part of Sh50 billion commitment by the Government of Japan to fund development of the facility.

The project will also see expansion of Port Reitz and Airport roads and drenching of access channel connecting new terminal and open sea.

The capacity of the new access road is expected to be 750,000 twenty feet equivalent of containers per year. A new railway station with four rail lines mounted with gantry cranes will also be constructed.

The facility will have a waiting area for empty trucks, repair and washing zone and an area for lorries waiting to be loaded with cargo. There will also be weigh-in-motion bridges to ensure axle load controls.

LAND RECLAMATION

The first phase of the terminal is expected to be completed by March 2016. The second and third phases will be ready by 2017 and 2020 respectively.

By last year, work on the three-berth terminal that involves land reclamation had seen contractor – Japanese Port Consultants – drench a large part to get to the deep sea meant to create dry land along the Indian Ocean and create space for second container terminal.

Mombasa port is the second largest in Africa in terms of tonnage and the containers handled per year with an average of 1,700 ships docking at the facility annually.

The port is preparing for competition that is expected to heighten movement of cargo in the East African region once another huge port being constructed by Tanzania at Bagamoyo is completed.

Last month, Kenya Ports Authority, the agency in charge of managing the port, said construction of phase one of the second container terminal – that is expected to significantly boost the port’s vessels handling capacity – was 65 per cent complete.

The ceremony to be held at Kenya Ports Authority headquarters at Mombasa will be attended by Treasury Cabinet Secretary Henry Rotich, his Transport counterpart Michael Kamau and ambassador of Japan to Kenya Mr Tatsushi Terada.

Related News

Global Economic Prospects: Sub-Saharan Africa regional outlook

Sub-Saharan Africa’s growth improved, for the second consecutive year, to 4.5 percent in 2014. Despite headwinds, growth is projected to pick up to 5.1 percent by 2017, lifted by infrastructure investment, increased agriculture production, and buoyant services.

The outlook is subject to downside risks arising from a renewed spread of the Ebola epidemic, violent insurgencies, lower commodity prices, and volatile global financial conditions. Policy priorities include a need for budget restraint for some countries in the region and a shift of spending to increasingly productive ends, as infrastructure constraints are acute. Project selection and management could be improved with greater transparency and accountability in the use of public resources.

Recent developments

Growth picked up moderately in Sub-Saharan Africa in 2014, to 4.5 percent, compared with 4.2 percent in 2013. In South Africa, growth slowed markedly, constrained by strikes in the mining sector, electricity shortages, and low investor confidence. Angola was set back by a decline in oil production and the Ebola outbreak severely disrupted economic activity in Guinea, Liberia, and Sierra Leone. In contrast, in Nigeria, the region’s largest economy, activity expanded at a robust pace, supported by a buoyant non-oil sector. Growth was also strong in many of the region’s low-income countries. Excluding South Africa, the average growth for the rest of the region was 5.6 percent. However, extreme poverty remains high across the region.

Investment in public infrastructure, increased agriculture production, and buoyant services were key drivers of growth. FDI flows, an important source of financing of fixed capital formation in the region, declined in 2014, reflecting slower growth in emerging markets and soft commodity prices. However, several frontier market countries including Cote d’Ivoire, Kenya and Senegal, were able to tap international bond markets to finance infrastructure projects.

The fiscal deficit for the region narrowed as several countries took measures in 2014 to control expenditures. At the same time, however, the fiscal position deteriorated in many countries. In some, it was due to increases in the wage bill (e.g. Kenya and Mozambique). In other countries (e.g. Mali, Niger, and Uganda), it was due to higher spending associated with the frontloading and scaling up of public investment. Elsewhere, the higher deficits reflected declining revenues, notably among oil-exporting countries because of declining production and lower oil prices (e.g. Angola). The region’s debt ratio remained moderate thanks to robust growth and concessional interest rates. However, in a few countries, debt increased significantly in 2014, especially in Ghana, Niger, Mozambique and Senegal.

Falling prices for oil, metals, and agricultural commodities weighed on the region’s exports. In contrast, spurred by infrastructure projects, import demand remained strong. As a result, several frontier market countries as well as South Africa continued to have substantial twin fiscal and current account deficits. Inflation edged up in the first half of 2014, due in part to higher food prices, but remained low in most countries. Reflecting concerns about low oil prices, the sovereign spreads for oil exporters rose strongly. The Nigerian naira weakened sharply against the U.S. dollar, prompting the central bank to raise interest rates and devalue the naira. The South African rand continued to fall on concerns about the country’s large current account deficit.

Outlook

Regional GDP growth is projected to remain broadly unchanged at 4.6 percent in 2015, rising gradually to 5.1 percent in 2017, supported by sustained infrastructure investment, increased agricultural production, and expanding service sectors. Commodity prices and capital inflows are expected to provide less support, with demand and economic activity in emerging markets remaining subdued.

Growth will remain robust in most low-income countries, owing to infrastructure investment and agriculture expansion, although soft commodity prices will dampen activity in commodity exporters. South Africa is expected to experience slow but steady growth, helped in part by gradually increasing net exports, and reforms to alleviate bottlenecks in the energy sector. Growth is expected to pick up moderately in Angola, as oil production rebounds. In Nigeria, the devaluation of the naira will push up inflation and slow growth in 2015, but with continued expansion of non-oil sectors, particularly the services sector, growth is expected to pick up again in 2016 and beyond. Among frontier market countries, growth is expected to increase in Kenya, boosted by higher public investment and the recovery of tourism. High interest rates and inflation would weigh on consumer and investor sentiment in Ghana, slowing economic activity.

Risks

The risks to the region’s outlook are mostly on the downside, stemming from both domestic and external factors. On the domestic front, the Ebola outbreak could spread more widely than assumed in the baseline, dent confidence and cause severe disruptions to cross-border trade and supply chains in the region. In various countries, government budgets are at risk from demands for increased spending. Conflicts in South Sudan and Central Africa Republic, and security concerns in northern Nigeria could deteriorate further with harmful regional spillovers. On the external front, a sudden increase in volatility in international financial markets, and lower commodity prices are among the major risks to the region’s outlook. A sharper or sustained decline in the price of oil would adversely affect the region, even though net oil importers would gain.

Lower growth in emerging economies, to which Sub- Saharan Africa exports, is the main external risk to the regional outlook. A worse-than-expected slowdown in China especially would reduce demand for commodities, putting further downward pressure on prices, especially where supply is abundant. A further decline in the already depressed price of metals, in particular iron ore, gold, and copper, would severely affect a large number of countries in the region. In countries such as Mauritania, Mozambique, Niger, Tanzania, and Zambia, metals account for a large share of exports; and their exploitation involves large FDI flows. A protracted decline in metal prices would lead to a significant drop in export revenues. A scaling down of operations and new investments in these countries would reduce output in the short run, and reduce growth momentum over an extended period of years.

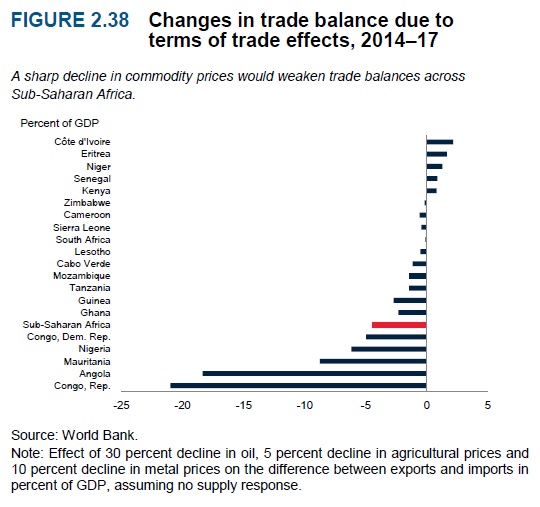

Simulation results suggest that the income effects of a sharp decline of commodity prices on Sub-Saharan African economies could be large. The scenario considered has a price decline from the baseline of 10 percent for metals (aluminum, copper, gold, iron ore, and silver), 5 percent for agricultural commodities (cocoa, coffee, tea, cotton, and tobacco), and 30 percent for crude oil. In the simulation, Sub-Saharan Africa is affected more than other parts of the developing world. Countries where metals, agricultural products, or oil represent a large share of total exports see their terms of trade deteriorate sharply. A sharper-than-expected and sustained decline in the price of oil from the baseline would, on the whole, adversely affect the Sub-Saharan Africa region, even though non-oil importers would gain. Oil exporters with a narrow economic base such as Angola and the Republic of Congo would be affected the most. The positive effect on oil importers is reflected in large trade balance improvements for Côte d’Ivoire, Eritrea, Kenya, Niger, and Senegal and moderate trade balance deterioration in South Africa.

Related News

Leveraging technology transfer for industrial development explored in new UNCTAD study

The study presents cases from Africa, Asia and Latin America, which provide contrasting experiences of the role of technology transfer and absorption in the development of different industries.

The report entitled Studies in Technology Transfer, Selected cases from Argentina, China, South Africa and Taiwan Province of China, builds on ongoing efforts by UNCTAD to investigate the role of the transfer of technology in economic development.

It was prepared under UNCTAD's mandate to undertake research and analysis in the area of science, technology and innovation (STI) with a focus on making STI capacity an instrument for supporting national development and helping local industry become more competitive.

The report examines the role of technology transfer in the development of integrated circuits production in Taiwan Province of China, button manufacturing in Qiaotou, China, automobile manufacturing in South Africa and biotechnology development in Argentina.

The cases therefore cover high-technology activities (integrated circuits and biotechnology), medium-technology activities (automobiles) and low-technology activities (buttons). This approach illustrates the potential for technology transfer to play a role in activities of widely differing knowledge, technology and skill intensities.

These cases represent varying degrees of success in the leveraging of technology transfer and local capability development for industrial development in developing economies.

The cases of integrated circuits in Taiwan Province of China and buttons in Qiaotou, China are both highly successful experiences of technological and industrial upgrading that laid the basis for globally competitive industries.

In the cases of biotechnology in Argentina and automobiles in South Africa, the results have been more mixed, with slower technological upgrading and a more nuanced picture in terms of the success of industrial upgrading and international competitiveness.

The four studies illustrate the varying approaches that firms and industries in different countries have taken in using international and domestic transfer of technology and combining these transfers with knowledge accumulated through internal effort in order to build stronger capabilities and improve their innovation performance.

They also illustrate the substantial variation in policy frameworks, institutional development, levels of policy intervention and underlying strategies implemented by national and local governments in developing economies in their quest to promote catch-up with more advanced economies by closing the gaps in scientific, engineering, technological and innovation capabilities and performance.

Related News

Kwacha fall leaves cross-border traders in quandary

The weakening of the kwacha against major currencies is pushing up prices of imported goods and may hurt some businesses, cross-border traders have warned.

The local unit has been weakening over the past few days but traded at K6.50 to a dollar by mid-morning yesterday after the Bank of Zambia’s intervention.

On Wednesday, the currency of Africa’s second copper producer hit K6.66 per dollar mark, its worst start to a year in more than six years.

The local currency’s poor performance has left several people counting the cost in lost business while a few are enjoying rich pickings.

Business owners who import goods from South Africa, retailers and cross-border traders are some of those that have been left hurt as the kwacha takes a beating.

Illegal currency dealers on the other hand have experienced a boom in their trade, as most people are exchanging the dollar for the kwacha.

In an interview on Thursday, cross-border traders who bring small orders, mostly clothing and alcoholic beverages, complained that since the kwacha came under pressure last year, businesses had drastically declined, forcing them to cut down on the number of trips out of the country.

COMESA/SADC Traders Trust chairperson Donald Kachingwe said at above K6.50 per dollar, the rate was still high and more government intervention to prop up the kwacha was needed.

“The kwacha should be propped up to the K4.80 to dollar level to make sense for our businesses,” Kachingwe said.

Individual traders explained that the weakening of the kwacha meant less buying power across the borders.

“My profit margins have seriously dropped. I used to make a K15 profit on each chitenge material I sold when the kwacha was trading below K6 to a dollar, but now I only make K5,” Nancy Zulu, who trades on Lusaka’s Chachacha Road, said.

Zulu, who has been trading for over four years, said a weak kwacha is a threat to the survival of her business.

“It is always a dilemma between increasing the prices and risking no one buying, but the only way out is to sacrifice a bit of profit,” said Zulu, who orders her goods from DR Congo, Tanzania and South Africa.

Beauty Mathonsi, another cross-border trader who operates from Lusaka’s COMESA market, a popular place for commodities from the COMESA region, said the fall in the kwacha has been “a curse” on her business.

“I buy clothes for resale from China, South Africa and Tanzania. The fall of the kwacha has not been a blessing as I have less money to order my stock outside Zambia using the dollar,” Mathonsi said, adding, “The choice I have here is to increase my goods.”

With the kwacha suffering a heavy battering most of last year, Zambia is still experiencing inflationary pressures as nearly 60 percent of goods in the shops are imported.

“The risk of this pressure on the kwacha is that it is likely to fuel illegal imports of goods,” said Joe Mbiya, a small-medium-enterprise business owner based in Lusaka.

“This is because we do not have serious manufacturing firms and in addition, the locally manufactured goods are too expensive to offset any price difference from imported goods.”

Related News

EAC rushes to draw pact on air routes after spat

An air routes spat, triggered by the suspension of Air Uganda last year, has seen the East African Community race to conclude an agreement on airlines covering routes between member states.

This follows Uganda’s move to give EAC routes to airlines from outside the bloc. The right for airlines to fly routes from one country to another is called the Fifth Right, but EAC members have been slow to embrace it, resulting in fewer flights between them and higher air travel and cargo costs.

A recent report by African Development Bank (AfDB) says the region’s aviation sector features extremely high fares caused by national airlines monopolising routes.

The report says that it is three times more expensive to fly from Nairobi to Entebbe than from Nairobi to Dubai, if one considers the distance.

According to the study, a flight between Nairobi and Entebbe costs between $295 (Sh26,550) and $390 (Sh35,100), whereas flying from Nairobi to Dubai (seven times as far) costs about $600 (Sh54,000).

The AfDB study found that taxes comprise 62 per cent of the total cost of air tickets within East Africa, while a Kenya Airways ticket from Nairobi to Dubai includes 41 per cent taxes.

Uganda has been increasing routes operated by foreign airlines following the withdrawal of Air Uganda’s licence by the Ugandan Civil Aviation Authority in June last year. As a result, RwandAir was granted the Fifth Right by Uganda to fly from Entebbe to Juba.

However, after being granted similar rights to fly from Entebbe to Nairobi, flights were stalled by lack of approvals from Kenya Civil Aviation Authority (KCAA).

Against this backdrop, and with Tanzania now threatening retaliation against KCAA’s refusal of approvals, the Northern Corridor Integration Project Summit held in Nairobi in December is now working on a memorandum of understanding between members states, which it plans to finalise by February.

The pact is set to do away with national airlines monopolising routes brought about by member states’ reluctance to allow other airlines to fly routes except to and from their own nations.

It will also help airlines such as FastJet to commence regional operations hence bringing more players into the market. This will lead to increased competition and eventually more affordable fares.

Demand for services

The MoU, signed by Uganda, Rwanda and South Sudan, is expected to be signed by Kenya. It also covers the harmonisation of procedures, infrastructure and operational activities such as air navigation services.

It is also expected to do away with regional airline rivalry which, for instance, led to the barring of Air Rwanda from picking passengers at Moi International Airport in Mombasa on its way to Juba.

This gave Kenya Airways a chance to dominate the local market and inflate fares due to high demand for its services. If the Fifth Right becomes operational, it will help cut regional airfares.

Transport ministers drawn from South Sudan, Uganda, Kenya and Rwanda who met in Kigali in September last year suggested that value added tax (VAT) and other taxes on airlines be scrapped because they add to the high cost of air travel.

VAT in the region ranges between 16 and 18 per cent.

Related News

More than half of Africa’s arable land ‘too damaged’ for food production

A report published last month by the Montpellier Panel – an eminent group of agriculture, ecology and trade experts from Africa and Europe – says about 65 percent of Africa’s arable land is too damaged to sustain viable food production.

The report, “No Ordinary Matter: conserving, restoring and enhancing Africa’s soil”, notes that Africa suffers from the triple threat of land degradation, poor yields and a growing population.

The Montpellier Panel has recommended, among others, that African governments and donors invest in land and soil management, and create incentives particularly on secure land rights to encourage the care and adequate management of farm land. In addition, the report recommends increasing financial support for investment on sustainable land management.

The publication of the report comes with the U.N. declaration of 2015 as the International Year of Soils, a declaration the Food and Agriculture Organisation (FAO) director general, Jose Graziano da Silva, said was important for “paving the road towards a real sustainable development for all and by all.”

According to the FAO, human pressure on the resource has left a third of all soils on which food production depends degraded worldwide.

Without new approaches to better managing soil health, the amount of arable and productive land available per person in 2050 will be a fourth of the level it was in 1960 as the FAO says it can take up to 1,000 years to form a centimetre of soil.

Soil expert and professor of agriculture at the Makerere University, Moses Tenywa tells IPS that African governments should do more to promote soil and water conservation, which is costly for farmers in terms of resources, labour, finances and inputs.

“Smallholder farmers usually lack the resources to effectively do soil and water conservation yet it is very important. Therefore, for small holder farmers to do it they must be motivated or incentivized and this can come through linkages to markets that bring in income or credit that enables them access inputs,” Tenywa says.

“Practicing climate smart agriculture in climate watersheds promotes soil health. This includes conservation agriculture, agro-forestry, diversification, mulching, and use of fertilizers in combination with rainwater harvesting.”

Before farmers received training on soil management methods, they applied fertilisers, for instance, without having their soils tested. Tenywa said now many smallholder farmers have been trained to diagnose their soils using a soil test kit and also to take their soils to laboratories for testing.

According to the Montpellier Panel report, an estimated 180 million people in Sub-Saharan Africa are affected by land degradation, which costs about 68 billion dollars in economic losses as a result of damaged soils that prevent crop yields.

“The burdens caused by Africa’s damaged soils are disproportionately carried by the continent’s resource-poor farmers,” says the chair of the Montpellier Panel, Professor Sir Gordon Conway.

“Problems such as fragile land security and limited access to financial resources prompt these farmers to forgo better land management practices that would lead to long-term gains for soil health on the continent, in favour of more affordable or less labour-intensive uses of resources which inevitably exacerbate the issue.”

Soil health is critical to enhancing the productivity of Africa’s agriculture, a major source of employment and a huge contributor to GDP, says development expert and acting divisional manager in charge of Visioning & Knowledge management at the Forum for Agricultural Research in Africa (FARA), Wole Fatunbi.

“The use of simple and appropriate tools that suits the smallholders system and pocket should be explored while there is need for policy interventions including strict regulation on land use for agricultural purposes to reduce the spate of land degradation,” Fatunbi told IPS

He explained that 15 years ago he developed a set of technologies using vegetative material as green manure to substitute for fertiliser use in the Savannah of West Africa. The technology did not last because of the laborious process of collecting the material and burying it to make compost.

“If technologies do not immediately lead to more income or more food, farmers do not want them because no one will eat good soil,” said Fatunbi. “Soil fertility measures need to be wrapped in a user friendly packet. Compost can be packed as pellets with fortified mineral fertilisers for easy application.”

Fatunbi cites the land terrace system to manage soil erosion in the highlands of Uganda and Rwanda as a success story that made an impact because the systems were backed legislation. Also, the use of organic manure in the Savannah region through an agriculture system integrating livestock and crops has become a model for farmers to protect and promote soil health.

Meanwhile, a new report by U.S. researchers cites global warming as another impact on soil with devastating consequences.

According to the report “Climate Change and Security in Africa”, the continent is expected to see a rise in average temperature that will be higher than the global average. Annual rainfall is projected to decrease throughout most of the region, with a possible exception of eastern Africa.

“Less rain will have serious implications for sub-Saharan agriculture, 75 percent of which is rain-fed… Average predicated production losses by 2050 for African crops are: maize 22 percent, sorghum 17 percent, millet 17 percent, groundnut 18 percent, and cassava 8 percent.

“Hence, in the absence of major interventions in capacity enhancements and adaption measures, warming by as little as 1.5C threatens food production in Africa significantly.”

A truly disturbing picture of the problems of soil was painted by the National Geographic magazine in a recent edition.

“By 1991, an area bigger than the United States and Canada combined was lost to soil erosion – and it shows no signs of stopping,” wrote agroecologist Jerry Glover in the article “Our Good Earth.” In fact, says Glover, “native forests and vegetation are being cleared and converted to agricultural land at a rate greater than any other period in history.

“We still continue to harvest more nutrients than we replace in soil,” he says. If a country is extracting oil, people worry about what will happen if the oil runs out. But they don’t seem to worry about what will happen if we run out of soil.

Adds Rattan Lal, soil scientist: “Political stability, environmental quality, hunger, and poverty all have the same root. In the long run, the solution to each is restoring the most basic of all resources, the soil.”

Related News

Taking stock of the proposed Continental Free Trade Area

Following the recent African Union (AU) Trade Ministers Conference held in Addis Ababa from December 4-5, 2014, we consider it opportune to discuss what 2015 may hold for progress towards establishing the Continental Free Trade Area.

The genesis of the accelerated intra-Africa trade agenda goes back to December 2010, when Africa trade ministers meeting in Kigali, Rwanda, agreed on a fast track agenda for a Continental Free Trade Area (CFTA) to address Africa’s low internal and external trade performances (at 13% and 2%, respectively). This in effect means that tariffs and quotas on the trade of most goods and services among African countries will be eliminated, bringing together 54 African countries with a combined population of more than one billion people and a combined gross domestic product of more than USD 1.2 trillion. The 18th African Union Summit of Heads of State, which convened on January 30, 2012, went a step further and approved an Action Plan for Boosting Intra-African Trade (BIAT). Both of these closely linked initiatives could easily lead to greater regional cooperation, trade and stability.

The projected numbers look impressive. A computable general equilibrium (CGE) analysis by Cheong, Jansen and Peters estimates that the CFTA could stimulate intra-African trade by up to USD 35 billion per year, or 52% (above the baseline) by 2022. It could also lead to a USD 10 billion decrease in imports from outside the continent, while boosting agriculture and industrial exports by up to USD 4 billion (7%) and USD 21 billion (5%) respectively. Gains in real income and employment could be even higher if the CFTA is complemented by trade facilitation reforms, reduction of non-tariff barriers, improved infrastructure and measures to counter-balance some of the negative effects associated with liberalization reforms such as loss of tariff revenue.

Key objectives of the CFTA

-

Create a single continental market for goods and services, with free movement of business persons and investments, and thus pave the way for accelerating the establishment of the Continental Customs Union by 2019 as provided for in the Abuja Treaty establishing the African Economic Community.

-

Expand intra-African trade through better harmonization and coordination of trade liberalization and facilitation regimes and instruments across Regional Economic Communities and across Africa in general.

-

Resolve the challenges of multiple and overlapping memberships and expedite the regional and continental integration processes.

-

Enhance competitiveness at the industry and enterprise level through exploiting opportunities for scale production, continental market access and better reallocation of resources.

The raw materials for achieving these levels of growth already exist. McKinsey estimates that the continent’s gross domestic product will rise from USD 1.7 trillion (2010) to USD 2.6 trillion (2020) pushing up consumer spending from USD 860 billion (2010) to USD 1.4 trillion (2020) and thus potentially lifting millions out of poverty. The consultancy also estimates that by 2030 nearly 50% of Africa’s population will be living in cities while there will be nearly 1.1 billion Africans of working age by 2040.

Implementing the CFTA

Even though the potential benefits of a CFTA are fairly clear, its implementation and the potential negative effects are the more contentious issues, which is why the various existing regional integration initiatives form its building blocks. At the heart of the process is the COMESA-EAC-SADC Tripartite Free Trade Area Initiative covering 26 countries, with a combined population of 530 million (57% of Africa’s population) and a total GDP of USD 630 billion (53% of Africa’s total GDP).

Linking the CFTA to the Tripartite FTA seeks to build on successful negotiations in the Tripartite as it would mean that more than half of the continent’s economy is already in a free trade area. What would remain is to extend that coverage to the rest of the continent. Moreover, important lessons can be learnt from that process in negotiating the creation of the CFTA in terms of scope, coverage, negotiating modalities and other approaches to the negotiations.

Trade Ministers meeting in Addis Ababa noted with concern that developments outside the continent have highlighted the importance of hastening Africa’s economic integration to mitigate the risk of preference erosion. Among those developments were, most notably, the emergence of mega-regional trade agreements like the Transatlantic Trade and Investment Partnership (TTIP) negotiations between the EU and the USA and the Trans-Pacific Partnership (involving 12 countries from Asia, the Pacific and the Americas) and the operationalization of the Africa-EU Economic Partnership Agreements (EPAs).

These developments raise a few questions. For instance, what would be the relationship between the CFTA and the existing regional FTAs? Countries have varied commercial and other interests that underpin their ongoing engagement in regional FTAs. This includes the pursuit of deeper trade liberalization and the elimination of duties, non-tariff barriers and other restrictive regulations of commerce, while similarly pursuing trade between and amongst regional partners.

A number of countries also have binding trade agreements with third parties like the economic partnership agreements (EPAs) with the EU and an assortment of bilateral investment treaties (BITs). It is important to establish a common understanding of how the systemic issues and multilateral system implication arising from these would be treated. Also, will the CFTA negotiations have sufficient depth to provide for flexible rules of origin, or for liberalization of trade in services and the free movement of persons? Will the negotiations provide for countries’ desire to purse an industrial policy? How will the CFTA ensure convergence on all or some of these issues which have proved contentious even within the Tripartite FTA?

There are no easy answers. Lessons from the Tripartite FTA process suggest that the AU Commission will need to strengthen its organizational and coordinating capabilities if it is to drive the CFTA negotiations. The Tripartite FTA process similarly faced resource challenges. Likewise the AU would have to mobilize sufficient funding, and the necessary technical expertise to manage negotiations of the size and scope of the CFTA. Apart from these basic issues, there is also the question of incentives and sanctions, especially if the deadline of 2017 will be met.

Whereas the resource discoveries, entrepreneurial revolution and abundant labour force are expected to drive growth in many African countries, the private sector in many jurisdictions are nascent, lack business support services and are besieged by high cost production environment. Trade policies in many African countries are characterized by protectionist trade regimes that are inimical to a CFTA. Judging from the resistance to the EPAs, it will not be a surprise in some countries if private sector lobbies are expected display resistance to the CFTA. Therefore, much more needs to be done to galvanize the private sector – both SMEs and large firms – to buy into the regional FTA and CFTA agenda.

Making it work

There are several FTAs in Africa which all aim to satisfy their members’ broad desire to increase market access opportunities and boost intra-regional trade volumes. For the most part, these FTAs have unfortunately been characterized by low levels of ambition, and have made limited progress in terms of: (i) full and timely implementation; (ii) eliminating non-tariff barriers; (iii) boosting a major increase in regional trade; and (iv) promoting regional industrialization. While there are certainly gains to be made in intra-African trade, the proposed CFTA may also compound some of the FTA implementation challenges experienced at a regional level.

The CFTA has to be carefully structured and synchronized in order to ensure broad based gains for member countries. This requires adoption of mechanisms to provide special and differential treatment for the least developed countries and to compensate them for certain negative effects associated with implementing the CFTA.

It is also important to understand that industry concentration and relocation may occur as the CFTA is implemented – meaning there will be winners and losers. Moreover, countries with better infrastructure and incentives may be more attractive to investors deciding where to locate. This has been the experience in other regions like the EU, East Asia and North America in the early transitions of their respective free trade arrangements.

A specialized body could be established to oversee the CFTA negotiations process. A comparable example is the Caribbean Community (CARICOM) Secretariat’s Office of Trade Negotiations, which is responsible for coordinating the 14-member CARICOM’s external trade negotiation resources and expertise. Technical issues such as non-tariff barriers, transit corridor issues, energy, transport, financial and logistics services can all be resolved by specialized institutions or agencies that do not have to be RECs. Such institutions could undertake inter-regional coordination and harmonization at a greater and more efficient pace than is achievable in individual RECs. Because nearly all the RECs have such institutions, it might be useful to spin them out of the RECs and create somewhat independent institutions that will take on the duties of these institutions.

In general, based on lessons from the Tripartite FTA process, we would recommend a sequential process, building on an incremental basis, i.e. sector by sector, covering Trade in Goods, Trade in Services, Investment, and other areas as applicable, as opposed rather than taking on a comprehensive agenda, given the challenges of capacity: skills, human, institutional, financial.

We also encourage the harmonization of regulatory frameworks (soft infrastructure), investments and cross-country infrastructure development projects that will facilitate freer movements of goods, services and persons across borders. However, such an approach should not lack ambition, in light of ambitious FTA developments taking place outside the continent.

Finally, it is important to recognize the role of the private sector as a major partner. Here, establishment of something like the African Business Council will provide the much-needed opportunity to effectively harness private sector inputs into continental trade policy making and the monitoring and evaluation on implementation processes.

The views expressed in this article are entirely those of the authors. They do not necessarily represent the views of the African Development Bank and its affiliated organizations, or those of the Executive Directors of the Bank or the governments they represent.

Related News

World Bank says Ebola puts future prosperity of Liberia, Sierra Leone ‘at high risk’

Job losses and food insecurity are among the far-reaching and persistent socio-economic impacts of Ebola in Liberia and Sierra Leone, according to the results of two new World Bank Group surveys released on 12 January 2015.

“[Ebola’s] socio-economic side effects put the current and future prosperity of households in Liberia and Sierra Leone at high risk,” said Ana Revenga, Senior Director for Poverty at the World Bank Group. “We must pay careful attention to those who are most vulnerable to both health and economic shocks, and ensure that they are supported throughout and after the crisis.”

The Liberian economy continues to shed jobs faster than they are replaced, with nearly half of household heads still out of work despite response-related jobs becoming available in construction and health fields. Most job losses are among private sector wage workers in urban areas, with women reported to be particularly vulnerable to the stagnant labour market, as they are disproportionately employed in non-farm self-employment.

In Sierra Leone, the first round of data collection found wage and non-farm self-employed workers seeing the largest declines in urban employment, with Ebola cited as the main cause. An estimated 179,000 people had stopped working outside of the agriculture sector. Most job losses were attributed to preventive efforts to limit the disease’s spread and to the general economic disruption caused by the outbreak, with quarantined and non-quarantined districts describing similar impacts.

The two reports found food insecurity persisting in both countries, with two-thirds of Liberian households reporting a lack of money to afford rice, regardless of price, three quarters indicating they worried about having enough to eat, and 80 per cent citing lack of money rather than availability or high prices.

No evidence was found on Ebola’s direct negative impacts on agriculture in Sierra Leone but harvest activities there were ongoing and future surveys are planned which will track any Ebola-related effects if and when they arise.

Over 80 per cent of those responding to the mobile phone survey in Liberia reported reduced harvests compared to last year, with the main concern the inability to organize work teams given Ebola fears. The same issue was cited as the main reason for incomplete harvests.

The survey showed some evidence of reduced use of health services for non-Ebola conditions in the Sierra Leonean capital, Freetown, with a much lower proportion of women reporting for post-natal clinic visits there compared to 2013. Elsewhere in the country there was little evidence of such a decline.

“From a poverty perspective, we are particularly concerned about households being forced into coping strategies that may harm their long term prospects to improve welfare, and now we can follow this in almost real time,” said Kristen Himelein, the World Bank Group’s poverty economist for Liberia and Sierra Leone.

“These high frequency surveys have been enormously helpful in bridging the gap between country-level growth analysis and the observations from those on the ground as part of the response,” she added.

The surveys are part of the World Bank’s $1 billion outbreak response and complement previous analysis that pointed to a possible $32.6 billion regional economic impact, which could catastrophic for these already fragile States. The surveys will continue in both countries, monitoring Ebola’s effects on economies and households and aiming to help Governments tackle the most pressing economic issues and plan the recovery.

Related News

The rise and fall of the world’s poorest nations

The world’s 48 Least Developed Countries (LDCs) – a special category of developing nations created by the General Assembly in 1971 but refused recognition by the World Bank – have long been described as “poorest of the poor” in need of special international assistance for their economic survival.

But only three – Botswana, Cape Verde and the Maldives – have so far “graduated” from being classified as an LDC to a developing nation, based primarily on their improved social and economic performance.

At a U.N.-sponsored ministerial meeting of Asian and Pacific nations in Nepal last month, four more LDCs, namely Bangladesh, Bhutan, Cambodia and Laos, were singled out as countries on the “threshold of graduation” based on their recent economic and social indicators.

And as economies improve, some predict that at least six more countries – Tuvalu, Vanuatu, Kiribati, Samoa, Angola and Equatorial Guinea (two African nations dependent on oil incomes) – are likely to be forced out of the ranks of LDCs, possibly by 2020 or beyond.

But this outlook may be premature due to several factors, including the impact of the global economic recession, the long-term effects of the decline in oil prices, reduced purchasing power due to falling national currencies, and in the case of Africa, the spread of Ebola.

Ambassador Anwarul Karim Chowdhury, the first U.N. Under-Secretary-General and High Representative for LDCs, Landlocked Developing Countries, and Small Island Developing States (2002-2007), told IPS the 2011 LDCs Conference in Istanbul, Turkey, set an objective of graduating 50 percent of LDCs out of the group by the year 2020.

“But this mechanical setting of a target for graduation is impractical and has the potential of undesirable tension for development cooperation at national and global levels,” he pointed out.

The foremost objective of graduation should be to bring LDCs out of poverty and their structural handicaps, he noted.

“But given the current distressing situation in most of the LDCs in both areas, it would be unwise for either the LDCs or their development partners to go towards realising this target,” Chowdhury added.

The people of these countries, particularly civil society, should be involved in the process to ensure that common people of LDCs do not become the greatest victims, he said.

“This is a reality in LDCs which we should not lose sight of,” he declared.

According to the United Nations, LDCs represent the poorest and weakest members of the international community, comprising more than 880 million people and accounting for less than 2.0 per cent of global Gross Domestic Product (GDP).

Fighting poverty in the LDCs is a key component towards reaching the U.N.’s landmark 2015 Millennium Development Goals (MDGs).

LDCs currently benefit from a range of special support measures from bilateral donors and multilateral organisations, and special treatment under regional and multilateral trade agreements.

The benefits that will be lost or reduced due to LDC graduation include trade preferences, official development assistance (ODA) including development financing and technical cooperation, and other forms of assistance, such as travel support for participation at U.N. conferences and other meetings of multilateral bodies.

As a result, special attention needs to be given to these special measures for graduating LDCs.

Arjun Karki, president of Rural Reconstruction of Nepal and international coordinator of LDC Watch, a network of LDC non-governmental organisations (NGOs), told IPS the aim of the 2011 Istanbul Programme of Action was to enable at least 24 LDCs (half of the existing 48) to graduate by 2020, so the current proposals for graduation have not reached this level.

The majority of LDCs (34 out of 48) are in Africa and to date only two African nations, Angola and Equatorial Guinea, are expected to graduate by 2020.

In both these cases, graduation is solely based on their income criterion (of Gross National Income per capita having exceeded at least twice the upper threshold of 1,190 dollars) while they fare low in the human assets and economic vulnerability criteria.

He said LDCs can only graduate when both LDC governments and development partners take action and it is vital they both have the political will to achieve this.

Gyan Chandra Acharya, the current Under-Secretary-General and High Representative for LDCs, Landlocked Developing Countries and Small Island Developing States, told delegates at the ministerial meeting in Nepal “the path towards graduation should not be an end in itself but should be viewed as a launching pad towards meaningful and transformative changes in the economic structures and the life conditions of people in graduated and graduating LDCs.”

He said sustainable graduation agenda needs to be tied up with that of productive capacity development, structural transformation resilience building and sustainable improvement in human and social capital.

Some of the practices being considered include enhancing investment in the productive sector, upgrading technologies and increasing protection from external shocks, such as climate related events, economic crises and natural disasters, according to a statement released by his office.

Chowdhury told IPS basically, graduation is a positive effort which requires the sincere and wholehearted engagement of both LDCs and their development partners.

“However, fixing an arbitrary target and using a technical approach for graduation could undermine realization of a good objective,” he stressed.

He also warned the ongoing economic crisis in the industrialised countries influenced the setting of the Istanbul target. “As the first High Representative of the new U.N. office established in 2002 to champion the cause of the worlds most vulnerable countries, I had worked diligently to make a space for the smooth transition in the graduation process,” Chowdhury explained.

That arrangement, he said, had made the LDCs less uncomfortable to engage in the process.

“I recall fully the agonising interactions for the graduation of Cape Verde and the Maldives during my tenure,” he said.

The consultative mechanism set up during the smooth transition needs to be closely monitored by the High Representative personally to ensure that the concerns of the graduating LDC have the true support of the U.N. system, he cautioned.

“This was part of my regular firsthand contacts with all of the Cape Verde graduation process,” he added.

Chowdhury also said overcoming of the constraints in two of the three determinants for LDC status to be eligible for graduation requires the full understanding by all sides of the real situation of LDCs.

“It is a pity that the biggest development assistance provider, the World Bank, has refused to accept LDCs in its work as a special category of countries as identified by the United Nations,” he said. “And my repeated visits to and efforts with the Bank headquarters did not get any response for the inclusion of LDCs.”

Related News

New test for economy as CET begins this month

Nigeria’s economy is set face more pressure amid falling oil prices and dwindling revenue, as the Economic Community of West African States (ECOWAS) implements the Common External Tariff (CET) regime this month.

The continued dependence on oil as the main foreign exchange earner, poor capacity in the manufacturing sector and ineffective anti-dumping measures, among others, are likely to undermine Nigeria at the take-off of the project, which is aimed at uplifting the economy of the region.

With uniform tariffs, revenue accruing to the Federal Government through the Nigeria Customs Service(NCS), which reached N3 trillion in 44 months preceding September 2014 and N977 billion between January and December 2014 , will likely plunge, according to analysts. This will put more pressure on the economy which depends on oil, whose price has already fallen to below $50 per barrel, about $15 less than Nigeria’s budget benchmark of $65.

Nigeria depends on oil for 75 percent of budget and 95 percent of foreign exchange earnings.

“There is a likelihood that revenue could fall, though I know a few measures are in place to ensure no country loses out,” said Tunde Oyelola, vice-chairman, PZ Cussons Nigeria plc.

The manufacturing sector and non-oil exports will be worst hit, as the twin sectors suffer from significant lack of competitiveness. While many sub-sectors in manufacturing have low capacity, non-oil export is mainly dominated by raw agricultural commodities, rather than finished manufactured goods, stakeholders say. For the CET regime, countries that do not have strong manufacturing base may lose out, as they will only become dumping grounds for other economies in the sub-region.

Stakeholders say this could affect output, employment and capacity utilisation in manufacturing.

Frank Jacobs, president, Manufacturers Association of Nigeria (MAN), said the implementation of cross-border policies such as the Common External Tariff (CET) and Economic Partnership Agreement (EPA) could throw up fresh challenges that might further complicate the current lacklustre performance of the country’s manufacturing sector.

According to Jacobs, who spoke during the 43rd annual general meeting of the MAN Apapa branch, held in Lagos, the CET and the EPA regimes would challenge the Nigerian economy, particularly the manufacturing sector, as local markets would be flooded with products made under favourable business environments at relatively lower prices.

The fear of real sector players is that CET will create an avenue for the adoption of the EPA, which is a trade liberalisation agreement between ECOWAS and the European Union.

Under the EPA agreement, 75 percent of the West African market will be gradually be liberalised in favour of the EU export products over the next 20 years.