Search News Results

Boosting trade links for Commonwealth Countries

International trade experts will meet this week to advance a ground-breaking Aid for Trade initiative aimed at boosting economic growth and reducing poverty in African, Caribbean and Pacific (ACP) countries.

The Global Network meeting in Mauritius will strengthen the implementation of the innovative Hub and Spokes II Programme, which was launched in 2012 and has been recognised for its effectiveness in enhancing the trade capacity of ACP states.

The project, which is sponsored by the Commonwealth Secretariat, the European Union (EU), the Organisation Internationale de la Fracophonie (OIF) and the ACP Group Secretariat, provides support and technical assistance through the deployment of experienced Regional Trade Advisors (Hub) and National Trade Advisors (Spokes) to organisations and government ministries.

Andie Fong Toy, Deputy Secretary General of the Pacific Islands Forum Secretariat, described how the project had been “instrumental in supporting the Pacific ACP region’s engagement in Economic Partnership Agreement (EPA) negotiations”.

The technical support provided by the programme has also contributed to a Micronesian Trade Treaty in the Pacific.

Representatives from businesses, academia, civil society and key international bodies, including the World Trade Organisation, will attend the conference on 19-23 January to assess its impact and decide on the 2015 agenda.

Deodat Maharaj, Deputy Secretary-General of the Commonwealth, has stressed the importance of helping ACP countries improve their international trading links, through the forging of strategic partnerships and the strengthening of regional networks.

He said: “In addition to €12 million from the European Union, the Commonwealth and OIF have contributed €2.5 million and €1.2 million respectively to the new Hub and Spokes programme.

“This investment is evidence of our commitment to ensure that ACP countries are able to manoeuvre through persisting global financial challenges, by creating sound and effective trade policies and reaping the full benefits of regional and international trade opportunities.”

He noted that the support to ACP countries was further boosted by the Secretariat’s vibrant in-house trade work programme.

Mr Maharaj added: “We thank the Government of Mauritius for hosting this important meeting, which will ensure our strategy for 2015 is strong, effective and tailored to regional priorities.”

The Hub and Spokes II programme builds on the successes of the previous €29 million Hub and Spokes project, which ran from 2004 to 2012 and supported ACP countries through international trade negotiations and with the implementation of trade agreements.

During the programme, more than 15,000 individuals and groups from the public and non-government sectors were trained on trade policy issues.

An independent evaluation of the project by Dr Stephen Woolcock of the London School of Economics and Political Science, concluded it “had made a real contribution to the negotiating capacity of the regions and countries where Hub & Spokes have been located.”

Mr Maharaj said the Hub and Spokes II Programme will help the Commonwealth realise its ambition of fostering economic development, given the absolute importance of trade in stimulating and generating sustained development.

He added that trade on equal terms is “good for growth, good for jobs and good for the Commonwealth.”

Related News

Traders save Shs1.2 billion with Electronic Cargo Tracking System

A total of $434,107 (about Shs1.2 billion) has been saved by traders since Uganda Revenue Authority (URA) adopted the Electronic Cargo Tracking System (ECTS) in May last year.

Figures from the authority show that transporters used to pay between $200 and 250 per day due to roadblocks by police and customs authorities across the region before the tax body partnered with Trade Mark East Africa to have ECTS at a cost of $2million (about Shs5.5 billion)

In the past, cargo trucks would arrive at border points where a declaration is made but before being cleared by customs officers, goods would disappear. These would go on the market having evaded taxes and cause undue competition because they are often low priced.

And according to URA officials, the ECTS was in response to the above and Uganda’s strategic geographical location as it is a link to regional markets of South Sudan, DR Congo, Rwanda, and Burundi, among others.

Before May, every truck bringing in goods from Mombasa to Uganda was accorded an escort by URA with the owner paying $50 (about Shs138,500) every day for tracking the consignments to avoid tax avoidance.

While meeting regional Dutch ambassadors who visited URA offices last week, the Commissioner Customs, Mr Richard Kamajugo, said ECTS depends on a control centre and automatic devices attached onto a cargo truck which repetitively give feedback to the team at the URA control centre on location of a vehicle, speed and status of the container.

Saying East African Integration has been eased with such technology, Mr Kamajugo said: “Without ECTS, East African integration would be very difficult.”

In his speech, Mr Alphons Hennekens, the Dutch Ambassador to Uganda, applauded the initiative and said his country supports the East African integration efforts.

Related News

Media Statement: Ordinary Joint Meeting of SADC Ministers of Health and Ministers Responsible for HIV and AIDS

SADC ministers of health and ministers responsible for HIV and AIDS met recently to review progress on the implementation of regional policies and programmes for addressing public health issues in the region.

This they did within the context of SADC Protocol on Health and the Maseru Declaration on HIV and AIDS.

A news release from SADC stated that ministers also agreed on common positions to be adopted at international fora namely the African Union (AU) and World Health Organisation (WHO).

The release said the ministers were also to participate in the commemoration of SADC Malaria Day, held over the weekend at Victoria Falls, under the theme Strong Partnerships Sustain Gains in Malaria Control and slogan: Combining Efforts - Key to Success.

The chairperson of the SADC ministers of health and ministers responsible for HIV and AIDS, and Minister of Health and Child Care of Zimbabwe, Dr David Parirenyatwa officially opened the meeting.

He outlined achievements and challenges recorded by the region in the fight against major communicable, emerging and re-emerging diseases, especially Ebola Virus Disease.

Ministers received status reports from SADC member states on the implementation of the SADC Protocol on Health with special focus on the agreed priorities in the areas of disease control, maternal, newborn, and reproductive health, health education and communication as well as health systems strengthening.

Ministers noted that the SADC region continues to experience a huge burden of communicable diseases. The big three, namely HIV and AIDS, TB and malaria remain the largest contributors to morbidity and mortality across SADC.

The meeting noted that declines in new HIV infections of 26 per cent and above were recorded in eight member states between 2001 and 2011. Botswana, Malawi, Namibia, Zambia and Zimbabwe recorded declines in new HIV infections among adults of between 26 per cent and 49 per cent, thus, surpassing the global target.

Mozambique, South Africa and Swaziland recorded declines in new HIV infections above 50 per cent during the same period. The meeting noted that eight member states are likely to reach the 50 per cent target reduction in new HIV infections by end of 2015.

The TB burden remains high in the member states, but significant achievements have been made in diagnostic and provision of TB treatment. The Ministers also took note of the rising burden of non-communicable diseases and the need to address them.

Ministers commended the region for the use of ICT in health communication such as print and electronic media, which influences behavioral change, thereby contributing to the realisation of positive health outcomes.

Ministers commended member states for measures taken to prevent the spread of Ebola in the region, including the containment and control of Ebola in the DRC, which was declared Ebola free.

In this regard, ministers reaffirmed their commitment to the implementation of internationally advocated state of preparedness and response guidelines for Ebola and have continued to adhere to International Health Regulations.

Ministers also reiterated their continued logistical, technical and financial support to Ebola affected countries in West Africa.

Ministers further reviewed and approved key strategic documents that will guide SADC public health priorities and for regional co-operation and integration.

In this regard, Ministers approved key documents including the SADC Code and Action Plan of Conduct on TB in the Mining Sector, minimum standards for the Integration of Sexual and Reproductive Health and HIV in SADC, framework of Action for Sustainable Financing of Health and HIV in the SADC Region and the establishment of Public Private Regional Partnership in complimentary health financing.

Ministers also endorsed WHO AFRO decision of strengthening health care systems in the continent through universal health coverage and further regard universal health coverage as a flagship of health care reform.

Ministers ended their meeting by expressing their gratitude to the government and the people of Zimbabwe for their hospitality during the course of the meeting.

Related News

Azevêdo invited to participate in informal meeting of African ministers

At the invitation of Egypt’s Minister of Industry, Trade and Small and Medium-sized Enterprises, Mounir Fakhry Abdel Nour, Director-General Roberto Azevêdo participated in an informal meeting of African ministers on 18 January in Cairo to discuss the WTO’s work in 2015. At the end of the meeting, the ministers issued the following press statement.

Press Statement

Ministers from Egypt, Nigeria, Kenya, South Africa and Senegal met in Cairo to discuss the multilateral trading system and the path forward in 2015 to the 10th Ministerial Meeting of the World Trade Organisation that will be held in December 2015 in Nairobi, Kenya. Ministers welcomed the presence of the WTO Director General, Ambassador Roberto Azevedo, invited to participate at the meeting.

Ministers agreed that current conditions in the global economy underscore the vital importance of the multilateral trading system as an engine for economic growth and development. Africa is a key beneficiary of a strong and functioning multilateral trading system.

Ministers agreed that to strengthen the system the Doha Development Agenda remained a critical element in the work of the WTO. They committed to work towards the development of a work program by mid-year that would consolidate the outstanding issues in the Bali agenda and establish a Road Map to ensure the conclusion of the Doha Round. Agriculture and development issues, including for LDCs and cotton, would be critical in defining a path forward – but all issues in the DDA need to be part of the discussion.

Ministers called for all members to be open-minded and show the necessary political commitment to ensure positive and substantive results, including on issues of interest to Africa. Development, after all, remains the key driving force behind the Doha negotiations.

To advance work, Ministers agreed it would be necessary for all WTO members to show the necessary flexibility to move work forward.

Ministers welcomed the dialogue with the WTO Director-General and agreed that this should continue as work progresses. The Director-General briefed Ministers on developments in Geneva, including the work to advance all Doha issues as well as to implement the WTO Trade Facilitation Agreement and to advance work on the WTO decision on public stockholding and all other Bali decisions.

The Ministers agreed to also reach out to other African countries to brief them on this meeting and to encourage all of Africa’s engagement on these important issues.

Ministers reiterated their strong support to the Government of Kenya as Chair of the 10th Ministerial Conference. They were determined to work with Kenya to ensure that the Ministerial Conference, the first to be held on the African continent, will be a “roaring” success that delivers strong outcomes for Africa and for development.

Ministers also thanked the Government of Egypt and in particular the Minister of Industry, Trade, and Small and Medium-sized Enterprises, Mounir Fakhry Abdel Nour for hosting the meeting.

Related News

Sustainable economic growth and peaceful elections should be Africa’s focus in 2015

African Development Bank President Donald Kaberuka on Friday, January 16 expressed optimism that 2015 holds an opportunity for the African continent to achieve progress in economic growth depending on the political will of African Governments. “It will depend on the policy stance of the countries, and the choices that they make or do not make,” he said.

The President was addressing diplomats accredited to the Bank’s host country, Côte d’Ivoire, the Bank’s senior management staff, and local and international media at an annual luncheon in Abidjan.

Kaberuka said although 2014 presented many challenges, including headwinds in the global economy, slowdown in the large emerging markets, and sharp declines in commodity prices, Africa remained resilient, maintaining its dynamism, at 5.5 percent growth.

“We know that given our demographics, 5 percent growth is strong but not stellar. It is 7 percent we must target,” he emphasised.

He said the outlook would even be better if faster progress was made in the areas of integration, especially removal of non-tariff barriers, and infrastructure development. “Those parts of the continent making faster progress on both areas are able to see higher growth, even when commodity prices are weakening,” he added, citing lack of jobs, inclusion, and effective safety nets as the giants holding back Africa’s full potential.

The challenge for 2015, he said, was not only in ensuring economic growth, but securing growth that is strong, sustainable, creates jobs, and one that benefits the broad categories of the population, not just few elites. Of the Bank’s importance is the ability of Africa to rebuild shock absorbers in the light of global uncertainties like commodity price volatility and altered conditions in the capital markets.

President Kaberuka reiterated the need for a global epidemic management system, pointing to the Ebola crisis, which had exposed the cracks in Africa’s primary health care systems. Even though disease or epidemic management is not a core business of the Bank, Kaberuka said the Ebola outbreak necessitated the institution to mobilise every resource to counter the problem.

Up to now, the Bank has committed close to US $220 million including budget support to the three affected countries of Sierra Leone, Liberia and Guinea. The outbreak interfered with businesses. “At the beginning of the outbreak, regional solidarity was put to test as neighbours closed borders and supply chains were disrupted. Yet it was clear that more needed to be done,” he observed, prompting African countries to strengthen their disaster preparedness.

2015 is significant as at least 15 African countries will hold legislative or presidential elections. Kaberuka’s concern is for these countries to retain or at least not undermine investor confidence “by ensuring elections are not times of shedding blood or generating instability.”

The AfDB President regretted the instability caused jihadists, presenting a new challenge on the continent. He cited recent attacks by Boko Haram in Northeastern Nigeria, where hundreds were killed, and Al-Shabaab attacks on a shopping mall in Kenya in which about 70 people died in 2013.

Kaberuka underlined that these were attacks on the whole of Africa, and they greatly undermined development.

“The risks posed by these outlaws and their backers are a major issue for Africa’s development prospects, perception, risk profile, investment climate and the Africa brand.” He noted: “Fighting these jihadists diverts our resources, which could be used otherwise to build infrastructure.” He called on the nations of the world to come together and battle against jihadists and their offshoots everywhere.

During the luncheon, Kaberuka lauded the Bank’s growth from US $3.6 billion 11 years ago to now about US $8 billion, a growth he describes as in line with the expectations of an emerging Africa. The Bank recently moved back to its headquarters in Abidjan, Côte d’Ivoire, after 11 years of relocation to Tunisia.

Albert Toikeusse Mabri, Côte d'Ivoire’s Minister for Planning and Development, expressed confidence in the Bank’s activities, welcoming its relocation back to Abidjan. “We are proud to have the Bank back. We are proud of the Bank’s services to the continent of Africa,” he said.

Related News

World Economic Situation and Prospects 2015: International Trade

Trade flows

World trade flows, measured in terms of import volumes, continued to grow at a slow pace in 2014, expanding at about 3.3 per cent, slightly faster than in 2013 but still well below the long-term trend of the decades before the global financial crisis. In the two decades prior to the crisis, for instance, the annual growth of world trade, measured by imports in volume, was on average twice the growth of world gross product (WGP), although trade flows were characterized by much higher volatility than WGP. The eruption of the global financial crisis in 2008 and the subsequent Great Recession in 2009 led to a collapse in world trade flows, with the volume of world imports plummeting over 11 per cent in 2009, 5 times the percentage decline in WGP. Except for a strong rebound in 2010, world trade has been expanding at a sluggish pace during the recovery, at only about the same rate as WGP. In the forecast period, trade growth is expected to expand moderately, at a pace of 4.7 per cent in 2015 and 5.0 per cent in 2016. While this will be an improvement, the ratio of the growth of world trade to that of WGP will still be only 1.5, not a full recovery to the pre-crisis trend.

At issue is whether the slowdown in trade growth relative to WGP in the years since the global financial crisis reflects a fundamental change in the structure of the global economy, or a transient and cyclical change in the relationship between trade and gross domestic product (GDP). The answer is probably that both cyclical and structural changes are at play.

Some of these key factors driving the growth of world trade before the global financial crisis may have run their course. The WTO Doha Round of multilateral trade negotiations, for example, has made little progress in the past fourteen years, failing to provide new impetus to trade growth. Some may argue that the Doha Round has been at an impasse since 2001, but world trade still registered high growth in the years before the financial crisis of 2008. This is because world trade in the run-up to the crisis continued to benefit from the lagged effects of the trade liberalization of the earlier years. For example, although China’s accession to the WTO occurred in 2001, China had a grace period of five years to gradually remove or lower a large number of trade barriers. By now, the lagged benefits from the earlier trade agreements before the Doha Round may have tapered off. The proliferation of various regional trade agreements (RTAs) may generate some new trade flows in some regions, but the overall effects of RTAs on world trade in the long run are not certain and cannot replace the role of the multilateral trading system (see the section on trade policy).

The integration process of the economies in transition and China into the global economy, after accelerating in the 1990s and 2000s, may also have reached a steady state. For instance, after two decades of rapid growth in its exports, at an annual rate of above 20 per cent, China’s share in total world trade has increased from a small fraction to about 12 per cent, in line with its share of GDP in WGP. With its wages increasing markedly, its process of transferring labour from the agricultural sector to the manufacturing sector diminishing, and its restructuring towards the services sector, as well as the rising environmental costs associated with industrialization, China’s growth in exports is not expected to return to a double-digit pace. On the positive side, the rise of the African economies can provide a renewed impetus to world trade in the next decades, but it will take some time to see the results on a large scale, as the region’s share in world trade is still small, at about 3 per cent.

In short, growth of world trade is projected to pick up some momentum from the subdued pace of the past few years in the aftermath of the financial crisis, but the dynamism of the two decades before the crisis may not return soon.

Regional trends

Growth of exports from developing countries is expected to increase from 3.9 per cent in 2014 to 4.6 per cent in 2015 and 5.5 per cent in 2016, while growth of imports will expand similarly from 3.8 per cent in 2014 to 5.3 and 6.0 per cent in 2015 and 2016, respectively. Africa’s exports continued to be relatively weak in 2014, growing only by 2.0 per cent. This weakness was driven by a variety of factors, including slow growth in North Africa and persistent fragility in Central Africa. Tourism and commodity exports have also been slowed by a number of factors, including the Ebola outbreak, terrorist attacks and domestic and political turmoil. This is expected to reverse somewhat in the forecast period with export growth rising to 4.6 per cent in 2015 and 5.0 per cent in 2016, driven by a reversal in North Africa to positive export growth, continued robust growth in East and Southern Africa and improvements in West Africa. Import growth is expected to continue strengthening after rising to 5.4 per cent in 2014, up to 7.0 per cent by 2016.

Trade decomposition

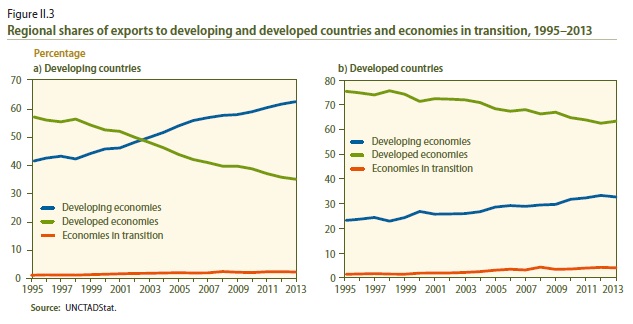

Many of the shifts in trade patterns that were observed over the past few decades continued in 2014, with developing countries exporting an increasing share of world trade by value, particularly manufactured goods. The destination of exports points to a more pronounced shift, as developing countries export a higher share to other developing countries than in the past, with a comparable fall in developed-country exports to developing countries. By contrast, the shift in exports to developed countries has been considerably lower, and developed countries still export most of their goods to other developed countries.

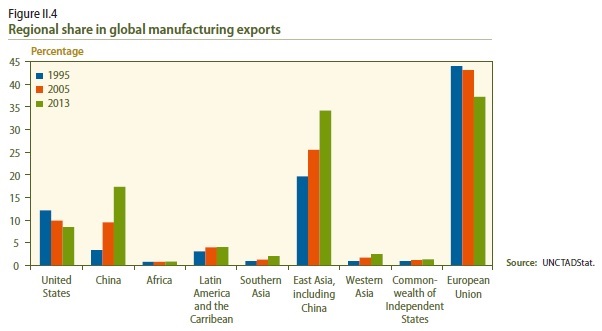

Much of the rise in developing countries’ share of world exports is due to East Asia’s rapidly increasing share of global manufacturing exports, which has risen from one fifth in 1995 to over one third in 2013. The expansion of China’s world trade profile has been a significant driving force in this rise, with a more than fivefold increase in the country’s share of global manufacturing exports, to about 17.3 per cent in 2013. A significant portion of the shift in manufactured goods trade shares has come at the expense of the United States, whose share fell by almost 4 percentage points. The EU is still the leading global manufacturing exporter, but its share also decreased, from 44.0 per cent in 1995 to 37.2 in 2013. If current trends persist, East Asia will take over as the largest exporter of manufactures by value in the forecast period.

Within the manufacturing sector there have been some significant changes, particularly as global value chains have expanded across the globe. Along with its overall increase in manufacturing exports, East Asia has seen its share of electronics exports rise from less than 20 per cent in 1995 to about 50 per cent in 2013. Mirroring this upward trend in East Asia, major developed-country electronics exporters, such as Japan, the United States and some European countries, have seen their shares diminish. There have been two parallel developments in this process. Some East Asian economies such as the Republic of Korea and Taiwan Province of China have seen their exports of intermediate goods to other countries (mainly in the region) rise, along with increases in the intermediate goods embedded in their own exports. China, on the other hand, continues to rely to a much greater degree on imported inputs for its exports with limited input into other country’s production processes. Meanwhile, the Philippines has seen its exports increasingly contribute to value chains in other countries, while absorbing a decreasing fraction of inputs from other countries in their own exports.

Trends for exports of primary products are somewhat different, influenced to some degree by changes in commodity prices over the past years. Overall, there has been a significant decline in the EU share in primary product exports, from 32 per cent in 1995 to about 22 per cent in 2013. This decline has been seen across almost all types of commodities, with only a few exceptions, such as tobacco, some types of crude materials, and animal oils and fats. In particular, there have been noticeable declines in the EU export shares in products such as meat, sugar, dairy products, beverages and crude fertilizers. However, the region continues to provide a significant portion of the world’s exports in many of those areas. At the same time, some regions have increased their market shares of primary commodities, with the biggest increase coming from Western Asia – although this was only by a little more than 8 per cent over the same period, particularly in fuels. For fuels in particular, the CIS has seen an increase from 1995 to 2013 by 4.5 percentage points to almost 15 per cent of world fuel exports. The United States has seen a relatively large increase in its share of fuel exports as well, by 55 per cent between 1995 and 2013. This increase still only puts United States’ fuel exports slightly above 4 per cent of the world total, but this is high enough to rank in the top five world fuel exporters.

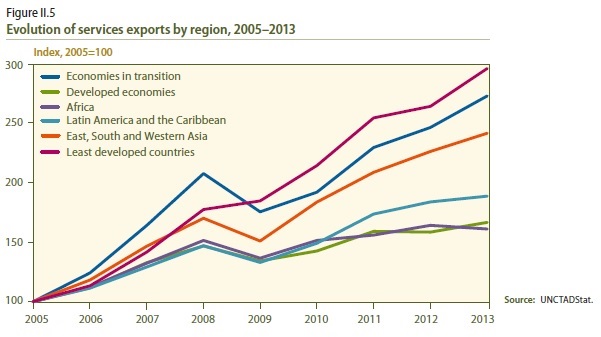

Trade in services

World services exports have continued to increase in recent years, providing some support to the sluggish performance of global trade. According to the most recent data, global exports of services increased by 5.5 per cent in 2013 and 7.0 per cent in the first quarter of 2014, at current prices. As a result, services exports reached $4.7 trillion in nominal value in 2013, about 20 per cent of total exports. The upward trend in services exports has been driven by developing countries, particularly in Asia and Latin America, as well as economies in transition. In addition, least developed countries (LDCs) have exhibited a remarkably fast expansion, although starting from a low initial level. As a result, between 2000 and 2013, the share of developing countries in world services exports rose from 23 per cent to 30 per cent, particularly in construction and computer and information services.

Trade in services is highly correlated with foreign direct investment (FDI). Over 70 per cent of world FDI outflows between 2010 and 2012 were related to services activities. Developing countries’ share in global FDI outflows into services is still low at 17.0 per cent, but this represents a remarkable increase from the early 1990s when it was only 0.6 per cent. Services trade also requires cross-border movement of people supplying services in export markets, particularly the provision of professional and business services, and thus has a strong linkage to the growth in global remittance flows.

Between 2008 and 2013, the most dynamic services trade sectors in developing countries were computer and information services, posting an annual average growth in exports of these services by 13.0 per cent. Other fast-growing services trade sectors for developing countries were insurance services, followed by travel services and financial services. Communication services, however, have not yet recovered their pre-crisis level. Meanwhile, LDCs posted the highest increase in computer and information services, insurance services and, in particular, construction. However, these sectors together represented just 7.0 per cent of total services exports for LDCs in 2013.

WESP is produced at the beginning of each year by the UN Department of Economic and Social Affairs (UN/DESA), the UN Conference on Trade and Development (UNCTAD), the five UN regional commissions and the World Tourism Organisation (UNWTO).

Related News

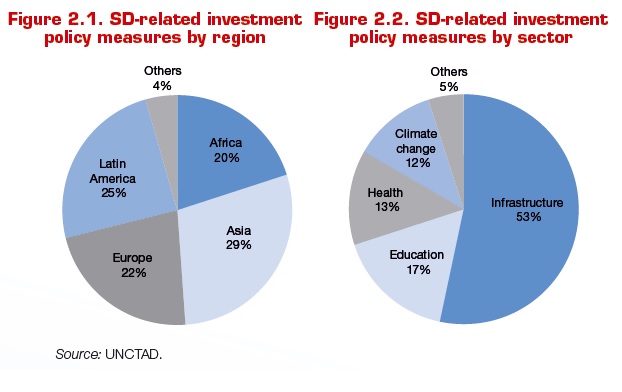

UNCTAD releases the 13th Investment Policy Monitor

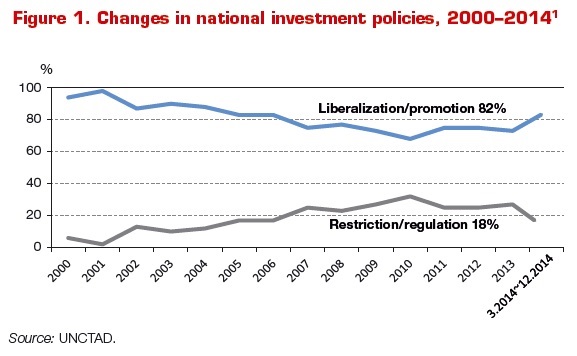

The Monitor finds that 33 countries or economies took 45 investment policy measures in the review period (March 2014-December 2014). The share of liberalization and promotion measures reached 82% – slightly above the average of recent years. These policies related to numerous sectors and industries. Despite these numerous measures aimed at improving investment conditions, there are also new concerns about the role of foreign investors in host countries.

A recent UNCTAD survey shows that countries increasingly pay attention to sustainable development in their national investment policies. However, the share of such measures among all investment-related policy changes is still low (approximately 8%). More can be done in investment policies to enhance the contribution of foreign investment to the sustainable development goals.

Regarding international investment policies, the Monitor finds that 51 economies concluded 26 new international investment agreements (IIAs). These include 14 bilateral investment treaties (BITs) and 12 “other IIAs.” Negotiations for one megaregional agreement (CETA) were concluded, and negotiations for 6 others continue.

An UNCTAD meeting will discuss the Transformation of the IIA Regime, 25-27 February 2015 in Geneva.

Featured infographics

National investment policies

As in previous review periods, the vast majority of new investment policy measures aimed at creating more favourable investment conditions.

Investment policy measures related to sustainable development (SD)

More private investor involvement in sectors and industries related to sustainable development is crucial, also in order to achieve the Sustainable Development Goals currently being prepared by the United Nations.

By region, investment policy measures related to SDG-sectors were mainly reported for countries in Asia followed by Latin America. Interestingly, all reported measures from Asian countries aim at improving entry conditions and facilitating foreign investment.

By sector, investment policy measures related to infrastructure development (including roads, ports, airports, energy generation and distribution, water supply and sanitation) were dominant (53 percent). Investment policies related to education came next (17 percent). Investment measures related to health services were less prominent.

Related News

USITC makes determinations in five-year (sunset) reviews concerning ferrovanadium from China and South Africa

The U.S. International Trade Commission (USITC) on 14 January 2015 determined that revoking the existing antidumping duty orders on ferrovanadium from China and South Africa would be likely to lead to continuation or recurrence of material injury within a reasonably foreseeable time.

As a result of the Commission’s affirmative determinations, the existing orders on imports of this product from China and South Africa will remain in place.

All six Commissioners voted in the affirmative.

Today’s action comes under the five-year (sunset) review process required by the Uruguay Round Agreements Act.

The Commission’s public report Ferrovanadium from China and South Africa (Inv. Nos. 731-TA-986-987 (Second Review), USITC Publication 4517, January 2015) will contain the views of the Commission and information developed during the reviews.

The report will be available after February 18, 2015. After that date, it may be accessed on the USITC website.

BACKGROUND

The Uruguay Round Agreements Act requires the Department of Commerce to revoke an antidumping or countervailing duty order, or terminate a suspension agreement, after five years unless the Department of Commerce and the USITC determine that revoking the order or terminating the suspension agreement would be likely to lead to continuation or recurrence of dumping or subsidies (Commerce) and of material injury (USITC) within a reasonably foreseeable time.

The Commission’s institution notice in five-year reviews requests that interested parties file responses with the Commission concerning the likely effects of revoking the order under review as well as other information. Generally within 95 days from institution, the Commission will determine whether the responses it has received reflect an adequate or inadequate level of interest in a full review. If responses to the USITC’s notice of institution are adequate, or if other circumstances warrant a full review, the Commission conducts a full review, which includes a public hearing and issuance of questionnaires.

The Commission generally does not hold a hearing or conduct further investigative activities in expedited reviews. Commissioners base their injury determination in expedited reviews on the facts available, including the Commission’s prior injury and review determinations, responses received to its notice of institution, data collected by staff in connection with the review, and information provided by the Department of Commerce.

The five-year (sunset) review concerning Ferrovanadium from China and South Africa was instituted on November 1, 2013.

With regard to China, then-Chairman Irving A. Williamson and Commissioners Dean A. Pinkert, David S. Johanson, Meredith M. Broadbent, and F. Scott Kieff concluded that the domestic group response for this review was adequate and the respondent group response was inadequate but that circumstances warranted a full review. With regard to South Africa, then-Chairman Irving A. Williamson and Commissioners Dean A. Pinkert, David S. Johanson, Meredith M. Broadbent, and F. Scott Kieff concluded that both the domestic group response and the respondent group response for this review were adequate and voted for a full review. Then-Commissioner Shara L. Aranoff did not participate in these adequacy determinations.

Related News

Egypt now turns to East Africa for trade growth through partnerships

EgyptAir has announced that it will resume direct flights to Kenya as it seeks to deepen its business ties with East Africa. The resumption date will be set after negotiations.

At a business forum between Kenya and Egypt held in Nairobi last week, discussions were held on areas of co-operation for development in the business sector.

Kenya’s national carrier stopped flying to Cairo in 2010 because of inadequate traffic on the route. Kenya Airways used to fly the Nairobi-Khartoum-Cairo route in a sharing agreement with EgyptAir.

Karim Sadek, the managing director Qalaa Holdings, a leading investment company in Africa, said, “For EgyptAir, the mainstay of this route are European transit passengers. There are few business travellers on that route,” he said.

Trade negotiations between the two countries are expected to focus on at least 10 Egyptian companies expected to partner with Kenyan enterprises in investment ventures. Kenya and Egypt will also form a joint business council, which meets quarterly, to monitor the business progress between the two countries.

Through bilateral visits and diplomatic missions on the continent, Egypt has been growing trade and economic relations. Sectors looking for immediate partnership with Kenyan companies include home appliances, agricultural equipment, pumps, central conditioning, ventilation systems, irrigation systems, generators, automotive feeding, security systems and educational labs.

“Egypt believes in the importance of co-operation between countries of the African continent to achieve the wellbeing of their people, and enhance the competitiveness of the Comesa economic bloc,” the Egyptian Minister of Foreign Affairs, Sameh Shoukry, said.

Kenyan business analysts say East African countries will only benefit if they focus on technology transfer, especially in the fields of agriculture, manufacturing and energy.

“If we partner with the Egyptian countries only for trade in terms of exports and imports, we are likely to lose because production costs in Egypt are low,” said Emmanuel Manyasa, an economist at Kenyatta University.

East African Business Council executive director Andrew Luzze said trade between East Africa and Egypt is likely to be skewed towards Egypt.

“We export raw materials to Egypt, and Egypt sells them back to us as finished products. Opening up the market to them will increase their exports into the region,” said Mr Luzze. “Even if they form partnerships, they stand to benefit more. Partnering with our local companies is just an entry point for them into the region.”

Until the issue of Rules of Origin, which has been a setback in trade between EAC and Egypt, is cleared, there will be trade imbalance between the countries.

“Some sectors like the edible oils will be affected because there will be unfair competition from Egypt,” said Mr Luzze.

EAC manufacturers exporting to Egypt are required to observe the 35 per cent threshold of value addition to qualify for free access to Comesa, of which Egypt is a member. However, Egypt uses a 45 per cent rate that it introduced.

Vimal Shah, the chairman of the Kenya Private Sector Alliance (KEPSA), said Egypt repackages goods like sugar from Brazil, electronic equipment and paper materials from other countries, and exporting them as their own goods. In 2011, Egypt raised its local value addition requirement for East African goods to 45 per cent.

Mohamed El–Hamzawi, the Egypt’s deputy assistant minister for Nile Basin countries Affairs said the issues of trade imbalance and rules of origin are being addressed.

“We have to look at this partnership from both sides and how each of us will benefit,” said Mr Hamzawi.

Laila El Maghraby, the executive director of the Engineering Export Council of Egypt (EEC-EG) said, “Egyptian companies are looking at forming business partnerships in Kenya that can link us to the entire East African region in the long run, because Kenya is the trading hub of the region,” she said.

Ms El Maghraby said they aim to export $60 million worth of engineering products into Kenya by the end of the year through trade partnerships, up from the current $23million.

“EEC–EG plans to establish a big commercial and logistic centre in Mombasa and Nairobi in the next two years as a strategy to cement our exports into the region,” she said. “Kenya is strategically placed because of the sea, and therefore it is better placed to start.”

Eric Musau, an analyst at Standard Investment Bank, said Egyptian companies have the competitive advantage of cheaper electricity, oil and gas.

“The issues of energy, high cost of raw materials, infrastructure and bureaucracy raise the cost of production in East Africa,” said Mr Musau, adding that technology in the region is not advanced enough to produce goods for a large market.

Colgate Palmolive, Procter & Gamble, Eveready and Cadbury moved their manufacturing operations from Kenya to Egypt because of the low cost of production. Egypt gives a 30 per cent subsidy to its industries, lowering the cost of production.

Related News

New plan sets Senegal on course to become emerging economy

A new development plan designed to help Senegal exit a trap of low growth and high poverty can boost the economy if it is consistently implemented, the IMF staff said in its regular review of the West African country.

The plan presents a unique opportunity to unlock broad-based and inclusive growth that will make Senegal a regional hub and an emerging economy.

Senegal’s growth in recent years has been sluggish, which has hampered progress toward inclusiveness and poverty reduction. Continued prudent policies have helped preserve macroeconomic stability in Senegal, but slow implementation of structural reforms continues to weigh down growth.

A period of relatively strong, although still under-par, growth in 1995-2005 of 4.5 percent led to a substantial decline in poverty from 68 to 48 percent. However, in 2006-2013 growth decelerated to an average of 3.4 percent, reflecting a poor business climate, problems in the energy sector, poor infrastructure, low efficiency of public investment, and unproductive subsidies.

Series of shocks

In addition, Senegal was hit by a series of externally sourced shocks, such as spikes in food and fuel prices, the global financial crisis, regional droughts and floods, and more recently, the spillovers from the Ebola outbreak. As a result, poverty has declined only slightly in recent years and stands at about 47 percent.

The IMF staff report on Senegal’s economy projects that GDP growth can rise to 4.5 percent in 2014 and reach 7 percent by 2019. Consistent implementation of reforms set out in the new development plan, while preserving fiscal and debt sustainability, are key preconditions for such growth acceleration.

The authorities are taking steps in this direction. The fiscal outlook has improved owing to stronger revenue performance and expenditure control, and the overall deficit is expected to fall to about 5 percent of GDP in 2014. The 2015 budget targets a further reduction in the deficit to 4.7 percent of GDP.

The authorities expect to limit the deficit by holding back appropriations for new public investment projects until feasibility studies are ready. The authorities remain committed to bringing the fiscal deficit in line with the target set by the West African Economic and Monetary Union of 3 percent of GDP in the medium term.

The plan for the future

The pdf “Plan Sénégal Emergent” (7.20 MB) is the authorities’ plan designed to help Senegal exit the trap of low growth and high poverty of recent years. It intends to make Senegal a hub for West Africa by achieving high rates of equitably shared growth. The plan is articulated around three pillars:

-

Higher and sustainable growth through structural transformation;

-

Human development and social protection; and

-

Improved governance, peace, and security.

The plan envisages structural reforms to attract foreign investment and increase private investment. It also calls for constraining public consumption and increasing public savings to generate fiscal space for higher public investment in human capital and public infrastructure.

Priority will be given to making delivery of public services more efficient, improving the impact of public spending through public financial management reforms, containing public consumption to generate the fiscal space for investment in human capital and public infrastructure, and strengthening social safety nets.

Keep debt sustainable

While welcoming the authorities’ plan, the IMF recommended remaining vigilant and anchoring plan-related scaling up of public investment on long-term debt sustainability within a medium-term budget framework. Creating the fiscal space needed for the development plan will require further strengthening of tax and expenditure policy measures, in particular improved public investment efficiency.

All related investment should be consistent with the authorities’ earlier fiscal consolidation plans and Senegal’s absorptive capacity. Decisions to contract nonconcessional financing should be carefully weighed.

Also, IMF staff underscored that the plan’s success depends on structural reforms of public financing and a strengthening of budget institutions. Reforms in this important area should focus on key areas such as macro-fiscal policy design, development of a medium-term expenditure framework and improved fiscal discipline in budget execution.

Focus on farms

While Senegal’s export base is relatively well diversified, high-quality exports bear a comparatively low weight. Sectors where the quality of exported products is comparatively low, such as food and live animals, constitute a large share of exported products. With Senegal’s labor force concentrated in agriculture, policies fostering agricultural product quality may be useful to supplement foreign investment-driven export diversification.

Other areas of structural reform recommended by the IMF include further improvements in the business climate, governance, investment in human capital and public infrastructure, and strengthening social safety nets. A comprehensive restructuring of the energy sector and increasing export competitiveness will also be important.

Financial sector vulnerabilities, especially the quality of bank assets, should be addressed. Continued vigilance of the high level of nonperforming loans is also needed in close cooperation with the regional central bank, the Banque Centrale des Etats de l’Afrique de l’Ouest, and with the West African Economic and Monetary Union’s Banking Commission, as is better access to financial services.

Experience of peers

An IMF staff paper accompanying the main report reviews experience of other countries and suggests that Senegal’s ambition to rise to emerging economy status within the next two decades is achievable.

Between 1990 and 2013, about 40 countries across the world have achieved average growth in real purchasing power per capita GDP of 5 percent or more. Those that Senegal could emulate include Cape Verde, Guyana, Indonesia, Mauritius, Sri Lanka, Tunisia, Uganda, and Vietnam. Several African countries have already begun the journey traveled by the Asian tigers to move from low-income to middle-income emerging market status.

Experience of peers suggests that structural reforms could lift Senegal’s growth to 7 percent in the medium term, driven by foreign investment-generated exports.

The authorities have already engaged with a few comparator countries to develop an active peer learning effort to roll out the required reforms. A high-level brainstorming on “Transforming Senegal into a Middle-Income Economy” held at IMF headquarters in Washington, D.C. on December 15-17, 2014, was the first step in this direction.

Fund targets US$1bn in African trade

The newly-launched Eastern and Southern African Trade Fund is looking to raise up to US$1bn to support intra-African trade finance transactions.

The fund, set up in December last year, is being managed by Mauritius-based Eastern and Southern African Trade Advisers Limited (ESATAL), which is jointly owned and managed by multilateral development bank PTA Bank and private investment advisory firm GML Capital.

As yet, the fund has not received any investments, but GTR understands that the first closing – of US$150mn – is likely to happen in the next couple of months. “We are in the process of finalising all the legal contracts and agreements with the relevant stakeholders,” Yogesh Gokool, head of international banking at AfrAsia, tells GTR. AfrAsia is acting as the cash custodian of the fund in Mauritius, responsible for, among other things, cash and treasury management.

The Mauritius-domiciled fund is open-ended and will soon be inviting subscriptions from international investors.

Set up to provide trade finance support to exporters and importers in PTA Bank’s 18 African member states, the fund will only support intra-Africa trade and “will try to foster and address the trade finance deficit in the Comesa countries”, explains Gokool. It will target both the private and public sector.

At this stage no trade finance transactions have been identified. “There is a pipeline,” says Gokool, “but this will need to be approved by the investment managers and the board of the fund before any investment takes place.”

Admassu Tadesse, president of PTA Bank said in a statement issued by the bank last year: “This fund will make a significant contribution towards addressing the trade financing deficit in Eastern and Southern Africa, and will, through blending and leveraging regional, international, private and public sources of capital, facilitate regional trade and economic integration, in line with the mandate of PTA Bank.”

Related News

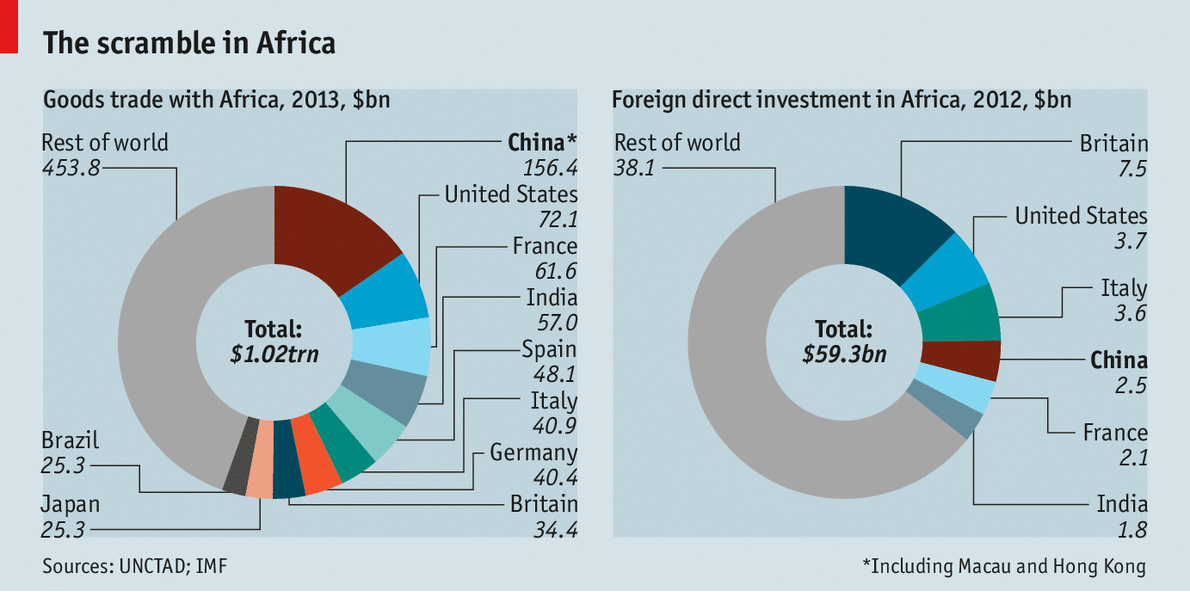

China in Africa: One among many

China has become big in Africa. Now for the backlash

Across Africa, radio call-in programmes are buzzing with tales of Africans, usually men, bemoaning the loss of their spouses and partners to rich Chinese men. “He looks short and ugly like a pygmy but I guess he has money,” complained one lovelorn man on a recent Kenyan show. True or imagined, such stories say much about the perceived economic power of Chinese businessmen in Africa, and of the growing backlash against them.

China has become by far Africa’s biggest trading partner, exchanging about $160 billion-worth of goods a year; more than 1m Chinese, most of them labourers and traders, have moved to the continent in the past decade. The mutual adoration between governments continues, with ever more African roads and mines built by Chinese firms. But the talk of Africa becoming Chinese – or “China’s second continent”, as the title of one American book puts it – is overdone.

The African boom, which China helped to stoke in recent years, is attracting many other investors. The non-Western ones compete especially fiercely. African trade with India is projected to reach $100 billion this year. It is growing at a faster rate than Chinese trade, and is likely to overtake trade with America. Brazil and Turkey are superseding many European countries. In terms of investment in Africa, though, China lags behind Britain, America and Italy (see charts).

If Chinese businessmen seem unfazed by the contest it is in part because they themselves are looking beyond the continent. “This is a good place for business but there are many others around the world,” says He Lingguo, a sunburnt Chinese construction manager in Kenya who hopes to move to Venezuela.

A decade ago Africa seemed an uncontested space and a training ground for foreign investment as China’s economy took off. But these days China’s ambitions are bigger than winning business, or seeking access to commodities, on the world’s poorest continent. The days when Chinese leaders make long state visits to countries like Tanzania are numbered. Instead, China’s president, Xi Jinping, has promised to invest $250 billion in Latin America over the coming decade (see article).

The growth in Chinese demand for commodities is slowing and prices of many raw materials are falling. That said, China’s hunger for agricultural goods, and perhaps for farm land, may grow as China’s population expands and the middle class becomes richer.

Yet Africans are increasingly suspicious of Chinese firms, worrying about unfair deals and environmental damage. Opposition is fuelled by Africa’s thriving civil society, which demands more transparency and an accounting for human rights. This can be an unfamiliar challenge for authoritarian China, whose foreign policy is heavily based on state-to-state relations, with little appreciation of the gulf between African rulers and their people. In Senegal residents’ organisations last year blocked a deal that would have handed a prime section of property in the centre of the capital, Dakar, to Chinese developers. In Tanzania labour unions criticised the government for letting in Chinese petty traders.

Some African officials are voicing criticism of China. Lamido Sanusi, Nigeria’s former central bank governor, says Africa is opening itself up to a “new form of imperialism”, in which China takes African primary goods and sells it manufactured ones, without transferring skills.

After years of bland talk about “win-win” partnerships, China seems belatedly aware of the problem. On a tour of the continent, the Chinese foreign minister, Wang Yi, said on January 12th that “we absolutely will not take the old path of Western colonists”. Last May the prime minister, Li Keqiang, acknowledged “growing pains” in the relationship.

China has few political ambitions in Africa. It co-operates with democracies as much as with authoritarian regimes. Its aid budget is puny. The few peacekeepers it sends stay out of harm’s way. China’s corporatist development model has attracted few followers beyond Ethiopia and Rwanda. Most fast-growing African nations hew closer to Western free-market ideas. In South Sudan, the one place where China has tried to flex its diplomatic muscle, it has achieved embarrassingly little. Attempts to stop a civil war that is endangering its oil supply failed miserably.

Chinese immigrants in Africa chuckle at the idea that they could lord it over the locals. Most congregate in second-tier countries like Zambia; they are less of a presence in hyper-competitive Nigeria. Unlike other expatriates, they often live in segregated camps. Some thought, after a decade of high-octane engagement, that China would dominate Africa. Instead it is likely to be just one more foreign investor jostling for advantage.

Related News

Reviving Trade Routes: Evidence from the Maputo Corridor

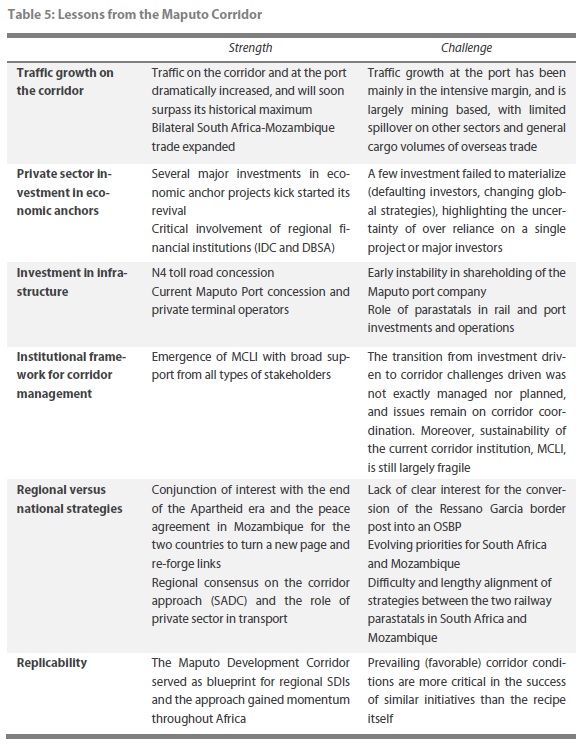

Most trade moves along a few high-density routes: the corridors. Improving their performance has emerged as a necessary ingredient for growth and integration into the regional and global economy. In Africa, this is recognized at the continental level, where PIDA for instance, the Program for Infrastructure Development in Africa, has identified 42 corridors that should form a core network for regional integration and global connectivity.

Several distinctive features appear to be necessary conditions for a successful corridor, namely (i) a combination of public and private investments to improve infrastructure, (ii) an institutional framework to promote and facilitate coordination, (iii) a focus on operational efficiency of the logistics services and infrastructure, and (iv) a proven economic potential. However, the presence of all the ingredients is not a sufficient condition: it is critical to also make sure that the fundamentals are appropriate and in sync and their management and coordination are sound.

Reviewing the experience of an apparently successful corridor can help us learn the optimal mix and trade-offs among the ingredients and enable replication of success on other corridors. The Maputo Corridor, which had fallen in disuse during the troubled period in Mozambique, is widely regarded as one the successful corridors. It has experienced tremendous growth, attracted large industrial and transport investments, and strengthened ties between neighboring countries over its almost two decade long history since the end of the apartheid era in South Africa and the Peace Agreement in Mozambique. What makes the Maputo Corridor ideal as a source of learning lessons is that it has many contrasting facets – it is an established trade route with a development focus, as well as an hinterland corridor, a mining and resourcebased corridor – whereas other corridors may have a far less diverse nature. The lessons that can be learnt from the Maputo Corridor thus have relevance for a wider variety of corridors.

The lessons from the Maputo Corridor can help the regional economic communities (REC), countries, corridor users and development partners to better focus their corridor strategies to maximize economic growth. The present work focuses on three aspects of its revival:

-

Corridors as enablers of trade and economic development

-

Improvement of logistics through investments and reforms

-

Institutional framework adapted according to objectives

Featured infographics

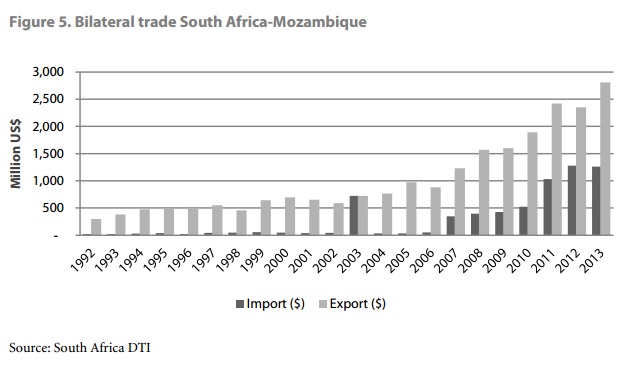

Opening up the corridor for trade had not only a positive impact on the transit trade flows (translating mainly in railways and port levels of activities), but also on regional trade, notably between South Africa and Mozambique. The dominant trade flow is from South Africa to Mozambique, and consumers in Maputo can now find everything that used to be available only in South Africa. However, exports from Mozambique, which were negligible, have picked up, and average now half of the value of imports.

Several of the original objectives of the Maputo Corridor revival have been achieved: (i) the current traffic activity of the railways and the port has reached the pre-independence levels, and prospects for sustained growth are bright, with increasingly well integrated markets (regional trade has expanded and any consumable that can be found in South Africa is now available in Mozambique); (ii) the core corridor transport infrastructure has been rehabilitated and expanded, with a port that will see its capacity double over the coming years, with sustainable funding to maintain the road infrastructure, and with commitment from railways parastatal to develop rail services and capacity; and (iii) private sector investment in large economic anchor project has been realized.

However, on a few other counts, the corridor is a work in progress and the results are not yet clear. A case in point is the institutional framework for the corridor, which has not evolved as initially planned. Rather there has been adaptation and the emergence of pragmatic solutions. When the investment-driven phase failed to evolve, it left a void that had become detrimental to the proper functioning and further development of the corridor.

Related News

Azevêdo: India’s support “vital” in WTO negotiations this year

Director-General Roberto Azevêdo, in his address to the Partnership Summit of the Confederation of Indian Industry in Jaipur on 16 January 2015, said: “It is in the interest of developing countries that the WTO is seen as an organization that delivers. So we must succeed in these efforts – and, as ever, India’s leadership will be vital.” This is what he said:

Minister Sitharaman,

Director-General Banerjee,

Distinguished delegates,

Ladies and gentlemen,

It is a great pleasure to be here today.

As you know, the WTO marked its 20th anniversary on New Year’s Day – just over two weeks ago. And I’m happy to say that this is my first major public event to mark this important milestone in our history.

I thought that this conference would be an ideal opportunity to mark the occasion, as India is a very prominent member of our organization – and the Confederation of Indian Industry is a valued partner.

As we look back after two decades, there is no doubt that the WTO has achieved a lot, or about the fact that it has made a major contribution to the strength and stability of the global economy.

This organization, and the global system of transparent, multilaterally-agreed trade rules that it embodies, has helped to:

-

boost trade growth,

-

prevent protectionism, particularly in response to the 2008 financial crisis,

-

and, crucially, it has helped support developing countries to integrate into global trading flows.

We have also helped to resolve numerous trade disputes.

In fact, over these 20 years, we have received almost 500 requests for consultations on disputes – which is a huge increase on the 300 disputes that our predecessor the General Agreement on Tariffs and Trade received in 47 years.

Resolving disputes is also of significant economic value. Indeed, the disputes that the WTO has dealt with relate to over 1 trillion US dollars in trade flows. So this is clearly important work.

And, since 1995 we have significantly expanded the rule of law. Indeed, our organization has evolved considerably over this period.

We have welcomed 33 new members to the WTO, ranging from some of the world’s largest economies to some of the least developed. Today our 160 members account for approximately 98% of global trade.

Moreover, at our 9th Ministerial Conference in Bali in 2013, we took our first major step in updating the multilateral trade rules. I’ll come back to this in a moment.

But I want to be clear that there is no complacency here. We face some real challenges as an organization and I am determined that we should do everything we can to tackle them – starting now, during this anniversary year.

For example, I know that the pace of negotiations remains a particular source of frustration. I am conscious that we need to deliver more outcomes, more quickly – and we will do everything we can to work towards this over the next 12 months.

Nevertheless, as we look back on these two decades, I think it is clear that the WTO has been shown to be an indispensable pillar of global economic governance. If it didn’t exist today, I think that we would have to invent it.

Indeed, I think that India’s experience helps to demonstrate the value of the system.

India and the WTO

India is a founding member of the WTO – and has played a very prominent role in the organisation over the last two decades.

India’s economy is far more open and connected today than it was 20 years ago – and Indian industry is competing on a global level as never before.

Of course there are many factors behind this, but there is no doubt that the opportunities provided by the multilateral trading system have played an important role.

India’s applied tariffs have dropped from around 39% in the early days of the WTO to around 13.5% now.

Indian exports have risen to ten times the level they were at in 1995.

And India has made good use of the other elements of the WTO system – to settle disputes, and to gain practical support to build the capacity to trade.

I think that India’s experience helps to illustrate the key issue that we are addressing today – that is the importance of WTO’s role in supporting development.

So let me elaborate on this point.

WTO & Development

The WTO supports development in many ways, but first and foremost, it provides developing countries with a seat at the table. Every WTO member, large or small, has a say in the decision making process.

This inclusiveness assumes even greater significance when viewed in the context of the increasing number of regional and bilateral trade initiatives, many of which do not include developing and least-developed countries.

On this basis it is essential that the WTO continues to provide a genuinely inclusive, multilateral forum.

Indeed, I don’t think that most people realize just how open and democratic the WTO is.

All decisions are taken by consensus – and at the WTO the voice of developing countries is just as important as that of the developed.

As Director-General I have made development my number one priority because I believe it is central to the organization’s mission.

After all, more than two thirds of our members are developing or least developed. And without such a central focus on development I don’t think we will be able to help these countries grow economically and address their developmental concerns.

That’s why I think we are seeing the WTO becoming even more responsive to its developing members – and this is the reason they are playing an even bigger role than ever in influencing the agenda.

This was clear in the Bali package which members agreed in December 2013.

Developing countries played a key role throughout the Bali negotiations and their support was instrumental in making it a success.

Bali simply would not have happened without their leadership and very vocal support. And of course the package contained some vital outcomes for developing countries.

Breaking the impasse

I’m sure you are all aware that despite the success achieved at Bali, we hit an impasse last summer in implementing what we had agreed in Bali.

This had a paralyzing effect on negotiations across the board – which was of particular concern to many developing countries who desperately wanted to see progress in all areas of the Doha development agenda.

In November, the impasse was finally resolved. And I want to acknowledge the role that India played in this – and particularly to thank Minister Sitharaman and Prime Minister Modi for showing the leadership which made this possible.

It was a major breakthrough – and it enabled WTO members to come together and take a number of important decisions that have helped to bring things back on track.

The first decision, and clearly the most important for India, was a clarification of the Bali Decision on Public Stockholding for Food Security Purposes, namely to unequivocally state that the peace clause agreed in Bali would remain in force until a permanent solution is found.

I am very pleased that the WTO, and its members, could deliver for India on this important issue – both in Bali and in Geneva.

But of course, it is just the beginning of this work. Members now have to work constructively together towards finding a permanent solution on this issue.

We have a target date to conclude the negotiations of December this year. So we don’t have any time to lose. I look forward to India playing a leading role in this regard in the coming months.

The second decision that members took was to formally add the Trade Facilitation Agreement to the WTO rulebook.

This clears the path for the Trade Facilitation Agreement that was agreed in Bali to be implemented and for it to come into force. Members are now working to ratify the Agreement according to their domestic procedures.

Here too, I am grateful for the support that Indian industry, and in particular the CII, has given to our work on trade facilitation. I’m sure that you will soon begin to see its positive effects.

It is estimated that the Agreement will reduce trade costs by up to 15% in developing countries. And I think you are likely to see benefits in a number of ways, including from the boost that it will bring to south-south trade.

Trade between India and Africa, for example, has grown exponentially in recent years. This Agreement will cut the costs of that trade, helping to boost those trading links yet further.

Moreover, there will be practical support to make this happen. For the first time in the WTO’s history, this Agreement states that assistance and support must be provided to help developing countries achieve the capacity to implement it. So, for those countries with less-developed customs infrastructure, the Agreement will mean a boost in the technical assistance that is available to them.

During 2014 I worked closely with the coordinators of the WTO’s key developing country groupings to ensure that this commitment is honoured. And together we launched a new initiative called the Trade Facilitation Agreement Facility.

This Facility will ensure that developing and least-developed countries get the help they need to develop projects and access the necessary funds to improve their border procedures, with all the benefits that that can bring.

This Facility is already in place and is now formally operational.

Donors are already very interested. We have already received a great deal of support and interest – and we have built strong partnerships with a number of organisations in support of this work, including the World Bank.

It has the potential to make a big difference, particularly for countries like India, and for industries like those represented in this room which have an interest in seeing India’s productivity and exports increase.

Post-Bali work

Members also took a third decision in November, regarding the WTO’s post-Bali work.

Members agreed that this work will resume immediately and that they will engage constructively on the implementation of all the Bali Ministerial Decisions.

This means taking forward:

-

the Bali decisions on agriculture – and cotton specifically,

-

the creation of a monitoring mechanism to look at how special and differential treatment for developing countries is being applied,

-

and the decisions on least developed country issues relating to duty-free-quota-free, services and rules of origin.

It is vital that we use the momentum we have now to take these decisions forward with the priority they deserve.

Moreover, this decision means that we have to agree on a work programme on the remaining issues of the Doha Development Agenda.

While progress on the DDA has been painstakingly slow, it is significant that all 160 WTO members are committed to delivering the work programme by a new target date of July 2015.

So I think this is an important moment – and a real opportunity.

The big, tough issues of agriculture, services and industrial goods will all be back on the table.

So I urge you all to be prepared and to engage proactively in this work.

Indian leadership

It is in the interests of developing countries that the WTO is seen as an organization that delivers. So we must succeed in these efforts – and, as ever, India’s leadership will be vital.

Countries look to India to raise issues of importance for developing countries. That role carries real responsibility. And I think we are seeing India take its rightful place at the centre of the world stage.

I have been closely following the very welcome policy measures that Prime Minister Modi’s Government has taken recently.

I think there is a real sense of positive energy and momentum which is capturing people’s attention around the world. In particular, the Prime Minister’s "Make in India" initiative – inviting the world to produce, invest and do business here – is very significant in the context of the work we do in the WTO.

For example, reducing trade barriers and implementing the Trade Facilitation Agreement will be important in supporting this initiative. Moreover, we want to help countries integrate into global value chains, and to build supply-side capacity and trade-related infrastructure through the Aid for Trade initiative.

Each of these measures can help develop in India an even more friendly environment for doing business, which will play a fundamental role in attracting productive investments and innovative industries.

And of course India is also playing an increasingly important role in south-south development cooperation.

Development support to improve trading capacity is particularly vital. And India has been playing an increasingly important role in this regard, as illustrated in the India-Africa forums that CII has organized each year, and in which the WTO has participated.

In this context let me also appreciate the partnership we have been building with the CII, especially on Aid for Trade – which is an important element of our development work.

We will be holding the Fifth Global Review of Aid for Trade at the WTO in Geneva from 30 June to 2 July this year.

I will be using the event to bring together numerous key figures – heads of agencies, donors and regional development banks – to see what more we can do to further support developing countries to build their trading capacity and further the good work that is already being done.

And I have no doubt that India, and CII, will play its full role in that initiative.

Conclusion

The WTO has delivered in many areas over the last 20 years – including on development. But big challenges remain.

We must deliver more through our negotiating work. We know that many of our poorest members are still not adequately integrated into the trading system – and many that do export still need to move up in the value chains and diversify their production and markets.

So as we look ahead to this anniversary year we know there is a lot of work to do.

We will be holding our 10th Ministerial Conference in Nairobi in December – the first time that the WTO will have held a Ministerial Conference in Africa.

We will be working to implement all aspects of the Bali package – including a permanent solution on public stockholding.

And we have a full negotiating agenda – including the July deadline to produce a detailed work programme on the remaining issues of the DDA.

Success in each of these areas would be the best way to mark our anniversary – and to reaffirm the contribution that the WTO has made to improving the lives and prospects of people in developing countries over the last two decades.

I look forward to your support – and India’s leadership – in all of these efforts.

Thank you.

Related News

Poverty Status Report 2014: Structural Change and Poverty Reduction in Uganda

The 2014 Poverty Status Report uses new evidence to present an updated analysis of Uganda’s poverty trends and status. The report’s thematic focus is the relationship between structural change and poverty reduction, exploring the complementarities between some of Government’s most important policy objectives: economic growth, job creation and poverty reduction. The report also analyses the reasons that many households remain vulnerable even as the economy continues to modernise. This evidence is brought together to recommend a set of complementary policy measures for structural change that generates productive employment, and reduces poverty and vulnerability.

Understanding poverty trends

Uganda has continued to reduce the number of people living in poverty. The national poverty rate fell to 19.7 percent in 2012/13, from 24.5 percent in 2009/10. Even with significant population growth, the total number of Ugandans living below the poverty line declined from 7.5 million to 6.7 million over the same period. There are now almost twice as many Ugandans in the middle class – living above twice the poverty line – as there are poor. In 1992/93, there were more than five Ugandans below the poverty line for every Ugandan in the middle class.

Significant poverty reduction has occurred across all regions of the country. In the last 10 years, poverty reduced by 18 percentage points in the Central region; 19 percentage points in the Northern region; 22 percentage points in the Eastern region; and 24 percentage points in the West. The Northern region remains the poorest part of the country, but the gap has narrowed significantly since the restoration of peace in 2006. More recently, it is the east that has seen the slowest progress in reducing income poverty. This mainly reflects adverse weather conditions, a high dependency ratio and growing population pressures contributing to land fragmentation and soil degradation. However, the region has seen significant progress in other dimensions of welfare, including education, health, housing conditions and access to information.

The considerable reduction in poverty over the years is attributed to Uganda’s general economic development, significant public investment in physical infrastructure, and several targeted Government interventions. Lower trade costs across the country, driven by improved transport infrastructure and better-integrated agricultural value chains, have been particularly important in ensuring agricultural households share the benefits of economic growth. Increased demand in the context of rapid urban growth and an increasingly connected region have created numerous income-earning opportunities for poor households. Government supported SACCOs have enabled many households to grow their enterprises, particularly those which emerged to advance the common economic interests of a particular group. Government interventions such as the Vegetable Oil Development Project in Kalangala have also had a transformative impact on the livelihoods of smallholder farmers. Gaps in public service delivery have successfully been addressed, through the Peace, Recovery and Development Programme in the north for example.

Uganda’s progress in reducing income poverty is strongly reflected in other dimensions of welfare such as education, health, housing conditions and access to information. To monitor and analyse these various dimensions of wellbeing, the report constructs the first nationally defined Multidimensional Poverty Index (UMPI). Uganda’s progress against this more comprehensive measure of welfare has been even more impressive than the country’s reduction in income poverty. In just three years between 2009/10 and 2012/13, the share of the population classified as multidimensionally poor reduced by 10.1 percentage points. On the other hand, the multidimensional poverty index provides a higher threshold for the minimum acceptable living standards; a significant proportion of households living above the income poverty line remain poor in the other dimensions considered. This underlines the need for Government to broaden its development objectives beyond the 19.7 percent of the population living below the poverty line.

Structural change and poverty reduction

Uganda’s first National Development Plan (NDP I) launched in 2010 rebalanced the policy agenda towards long-term issues related to structural change, wealth creation and the productive capacity of the economy. This signalled a broadening of Government’s objectives, beyond the narrower focus on extreme poverty which characterised the Poverty Eradication Action Plan (PEAP). With most gaps in basic public services addressed, to sustain progress Government increasingly needs to harness the poverty-reducing potential of structural change – or shifts in the sectoral share of employment and GDP in favour of more productive and dynamic activities. Chapter 3 of this report demonstrates the numerous channels through which growth and structural change help to reduce poverty. Economic growth is required to create jobs to employ the working poor and their children, but there are many more indirect benefits. For instance, demand resulting from growing urban markets and an increasingly connected region have benefited the large majority of the poor engaged in agricultural production, and created a growing number of off-farm income-earning opportunities. Growth of agro-processing, financial services, telecommunications, transport and storage services and many other sectors is also benefitting agricultural households.