Search News Results

Combined mid-term review and regional portfolio performance review of the Regional Integration Strategy Paper for West Africa 2011-2015

Executive Summary

In November 2011, the Board approved the Bank’s Regional Integration Strategy Paper for West Africa 2011-2015 (WA-RISP), covering a grouping of 15 member countries of Economic Community of West African States (ECOWAS).

Such group has a diverse mix of political, economic, social and geographic characteristics, ranging from the dominance of Nigeria the regional heavyweight, to the small size of other national markets, including landlocked countries and an island state. The WA-RISP is articulated around two pillars, (i) linking regional markets and, (ii) building capacity for effective implementation of the regional integration agenda.

The main objectives of the MTR-RPPR of the Bank’s WA-RISP are (i) to assess the relevance and effectiveness of the WA-RISP and (ii) propose possible adjustments to current Bank approaches for enhancing regional integration.

Since 2011, West Africa’s growth has accelerated and is estimated to reach 7.4% in 2014, making it the fastest growing region of the continent. However, the region is still home to some of the poorest in the continent. Poverty and inequality are high across the region with poverty levels in some countries averaging more than 60% of the population. Furthermore, gender-related MDGs and indicators have shown moderate improvements.

Arguably one of the most fragile from a political and security stand point, the region is more exposed to fragile situations since the inception of the strategy, further to the crisis in the Sahel and the emergences of new terrorist threats.

The Regional Integration Strategy Framework remains largely shaped by ECOWAS and its Vision 2020. Progress in implementing Vision 2020 has been mixed, so is the status of regional integration, with intra-regional trade still low compared to other groupings.

As of December 1st, 2013, the Bank’s active regional operations portfolio in West Africa included 43 operations, for a global amount of UA 667 million and an average disbursement rate of 31%. The overall implementation status of the WA-RISP is satisfactory: out of the 13 projects provisioned under the two pillars, four were approved between 2011 and 2013, four are in process or under review, and one is postponed until 2016, while four are on stand-by due to limited resources. All planned ESWs have been completed, yet some have been refocused in view of the changing political landscape.

Analysis at mid-term supports that the two strategic pillars identified in the WA-RISP (2011-2015) remain relevant for the remaining period. While the choice of pillars is also consistent with the Ten Year Strategy, this MTR elaborates on adjustments to strengthen the Bank’s contribution to the regional integration. These include focusing the first pillar around infrastructure development and renewed attention at addressing fragility, gender and food security, including through a new program on resilience in the Sahel.

The MTR suggests strengthening Bank support to Sahel and Mano River Union (MRU) countries, and giving greater focus to the “soft” side of the Bank interventions, by (i) integrating trade, transit and trade facilitation in all new transport operations; (ii) strengthening technical assistance on trade facilitation; and (iii) boosting regional knowledge work.

The MTR also recognizes the important role of private sector, including through Private Equity funds, and advocates for a deeper engagement with business organizations at regional level.

The MTR suggests a number of measures to improve performance of regional portfolio, such as strengthening of the role of the Bank’s field offices in managing regional projects; technical assistance on Bank’s procedures; setting-up and building capacity of dedicated units to oversee Bank operations in selected RECs.

Related News

South Africa is ready for investment, says Ramathlodi

South Africa’s government is committed to expanding its mining industry, Mineral Resources Minister Ngoako Ramatlhodi told the African Mining Indaba in Cape Town on Tuesday.

“South Africa is ready for investment,” Ramathlodi told the conference. “We are leaving no stone unturned in providing a stable environment for investment.”

South Africa is the world’s largest producer of platinum and the seventh largest producer of coal.

After his address to the conference, attended by 7 000 of the world’s mining executives and stakeholders, the minister joined Trade and Industry Minister Rob Davies and other high-level panelists at an “investment dialogue”.

Hosted by Brand South Africa, the panel focused on ways to drive competitiveness of South Africa’s mining sector.

Emphasising the need to establish regulatory stability, Ramathlodi said the government was working with speed to finalise amendments to the Mineral and Petroleum Resources Development Bill.

In January, President Jacob Zuma returned proposed changes to the 2002 Act back to the National Assembly on the grounds that they may violate the Constitution.

Diversification

Trade and Industry Minister Rob Davies said diversification was key for African markets – including South Africa – if they were to achieve growth.

“If we are to create a boom for mining, we must create a demand from Africa as well,” Davies said.

There are “inherent competitive qualities” in the minerals chain, which South Africa must harness, he said. “We must use our minerals in a way that benefits African economies.”

The government has invested heavily in developing minerals beneficiation projects, including using platinum to develop fuel cells and a project that turns mineral sands into titanium powder. “We are ready to rock and roll on this,” the minister said.

Davies said a process was already under way to align charters and codes. The government would soon create the post of a commissioner to enforce Black Economic Empowerment regulations – and prevent “fronting”, where BEE points are being claimed but the processes are not implemented.

Energy

The government would also move “with speed” to tackle energy constraints currently affecting the country.

Davies said he was confident that the energy war room would tackle the country’s energy problems, with maintenance of the infrastructure high on the agenda.

The government was also conducting a “significant” build of energy-generating resources. Medupi power station, for example, would generate more electricty than Nigeria once it came online, Davies said.

Mike Teke of the Chamber of Mines said the industry was committed to delivery – especially on the social and labour fronts. “We have seen great successes, but there is room for improvement,” he said.

To solve labour issues and to avoid a repetition of the protracted and violent strikes that have crimped growth in the industry would require all parties to work together.

“We all need one another – mining, regulator, trade unions, mine bosses,” Peter Bailey of the National Union of Mineworkers said. “We must do things differently… If we take hands, we all have a responsibility to ensure this industry remains a sunrise industry rather than a sunset industry.”

Gideon du Plessis of the union Solidarity told the audience that “the time for mining is now”.

“We must make progress,” he said. “This is a promising country. And a promising industry.”

The Mining Indaba is an important event for Cape Town, bringing more than R500-million in direct revenue to the city over the past eight years, creating 4 500 direct and indirect jobs and selling 20 000 hotel nights.

Related News

Tanzania keen to crash barriers

The government has embarked on a project to develop three One Stop Inspection Stations (OSISs) to reduce non-tariff barriers (NTBs) to trade which inhibit intra-trade in the East African region.

According to a statement by TradeMark East Africa (TMEA) which supports the project including other development partners, the three locations have been selected to capture the largest amount of transit traffic.

The three stations will be set up at Vigwaza in Coast Region, Manyoni in Singida Region and Nyakanazi in Kagera Region, where all regulatory authorities involved in vehicle inspection along the Central Corridor will conduct their inspections jointly at one location.

TMEA and the European Union (EU) have funded the preparation of the detailed design, supervision and construction of two of the three OSISs at Manyoni and at Nyakanazi, the statement said. The World Bank has agreed to support the preparation of the detailed design, supervision and construction of the third OSIS at Vigwaza, through the Southern Africa Trade and Transport Facilitation Project.

The stations will combine in one location activities of the Tanzanian National Roads Agency (TANROADS), which controls the weighbridges, the police force, which checks the condition of vehicles and the Tanzanian Revenue Authority (TRA), which carries out customs checks.

“The site at Vigwaza is the first major weighbridge location outside of Dar es Salaam capturing both central corridor and the Dar es Salaam Corridor traffic to Southern Africa.

“The site at Manyoni captures traffic from the central corridor and that from Kenya into Tanzania and the site at Nyakanazi handles Ugandan, Burundian and Rwandan vehicles,” reads the statement in part.

TANROADS has been appointed as the Executing Agency of the OSIS project and will be the primary counterpart within the Tanzania government in implementing the project.

The OSIS project will be a shared facility with an installed relevant ICT infrastructure to enable sharing of information.

It is expected that the stations would reduce time and cost of transporting transit goods along the Central Corridor by only requiring transit trucks to stop at three locations along the central corridor.

According to the Government of Tanzania’s Tanzania Programme “Big Results Now” (BRN) Initiative the project will reduce the number of official checks for Transit Trucks from 17 to 3 along the Central Corridor. “Not only will the OSIS reduce congestion of trucks parked along the roadsides and reduce accident rate caused by exhaustive drivers, but also most importantly, reduce time and costs through joint checks from the Police, TANROADS and Tanzania Revenue Authorities at the three sites,” adds the statement.

Related News

EAC Secretariat refutes report of financial abuse

The Secretariat of the East African Community (EAC) has rejected an audit report that showed it was abusing the bloc’s funds.

The audit, tabled before the East African Legislative Assembly (Eala) in Arusha, Tanzania, last week, was done by the EAC Audit Commission, which comprises auditors-general of all the five EAC partner states. The audit covered activities of the bloc for the financial year 2012/2013.

Yesterday’s rebuttal follows a series of articles in regional media in which the EAC Secretariat, the executive organ of the bloc, particularly came under attack for what was portrayed in the report as gross misuse of financial resources.

The unflattering audit report had pointed to cases of wasteful expenditure during staff interviews, over expenditure, and even indicated that the Arusha-based Secretariat spent about $3.4 million during the financial year in review on uncalled-for procurement of air tickets.

In statement, however, the Secretariat said in the Financial Year 2012/2013, all EAC organs and institutions received an unqualified (clean) audit opinion from the commission.

“This is the first time all organs and institutions receive a clean audit from the Audit Commission. In the previous years, many EAC-related institutions received qualified or disclaimer opinions. This clean audit is testimony of the hard work of leaders and staff of the Community,” the statement reads in part.

It also claims that the audit report does not portray misuse or loss of any funds, nor governance weaknesses or executive negligence but “simply tables audit findings that point to areas that need to be strengthened.”

For reporting period, the statement adds, there was no over expenditure since from the funds appropriated by the Assembly, $1.67 million was transferred to the EAC General Reserve account at the end of the financial year, as a result of factors, including “improved efficiency within the EAC.”

EAC management says $384,834 is mentioned as an ‘irregularity’ because it was released to staff to meet obligated commitments toward the end of the financial year.

“These funds were not misused. They were used to meet duly approved and executed EAC activities.”

Accordingly, details of those activities and obligations will be resubmitted to the Assembly during its next sitting in Bujumbura, Burundi, next month, the statement says.

Last month, Eala adjourned debate on the audit report to allow the Council of Ministers and the EAC management to clarify and additional information “not adequately captured in the report,” in order to allow for informed debate by MPs during Eala’s upcoming session in Bujumbura.

The Council of Ministers has the oversight of the Audit Commission.

Procurement of tickets

The Secretariat explained that procurement of tickets is done through a framework contract agreement with travel agents for a defined period of two years, after which it is re-advertised.

Unutilised air tickets are presented for refund to the travel agents and, given the importance of this expenditure, “periodic internal audit of the procurement of tickets is carried out, and internal control systems continuously strengthened.”

Regarding the reported wasteful expenditure during staff interviews, the Secretariat said 2012/2013 was the first time the EAC contracted an independent reputable international firm to help with the recruitment process.

“This was aimed at getting value for money, as well as shortening this process, which has been less than optimal in the Community. This policy is beginning to bear results, although it has had its teething problems,” reads part of the statement.

Despite financial control systems in place, including making amendments to Financial and Procurement Regulations, and automating most of processes using latest information management software, EAC management admits that an unqualified (clean) audit opinion “does not mean that we have reached perfection.”

The Audit Commission and the Eala Committee on Accounts noted some issues in the EAC Organs and Institutions that require improvements. To this, the Secretariat said it was “working on resolving the indicated issues.”

» Public Notice: EAC Audited Accounts (Financial) for the FY ended 30th June 2013

Related News

Is Southern Africa’s agro-industry delivering food security?

Has the predominance of the agricultural sector in Southern Africa translated into food and nutrition security in the region? Evidently not! Food security remains a major socio-economic and political challenge in the region with some analysts arguing that food insecurity is a new threat to national security.

Agriculture is the dominant economic sector in the SADC regional economy contributing up to 35 percent to its GDP. Approximately 70 percent of the population in Southern Africa depend on agriculture for food, income and employment while agricultural commodities and produce are the principal exports in many countries, on average contributing approximately 13 percent to total export earnings and 66 percent to the value of intra-regional trade.

ECA Southern Africa Regional Office will be convening an Expert Group Meeting on Agro-industry development for food and nutritional security in Southern Africa to discuss and review the state of the agriculture sector in Southern Africa. The meeting with take place from 9th to 10th March 2015, in Victoria Falls, Zimbabwe.

An issues paper on Agro-industry development for food and nutritional security in Southern Africa will be the major discussion paper. The two day meeting is expected to provide concrete recommendations on how to strengthen the agro-industry sector through among others partnerships, best practices and lessons from other regions.

Agricultural sector performance has a strong influence on the economic growth, employment, demand for other goods, economic stability, food security and overall poverty of SADC member States and the region as a whole. Whether looked at from exports or domestic market, the agro-industry is fundamental to income and employment creation in the region.

Participants to the meeting will include agro-industry and agribusiness experts from government institutions, the private sector, SADC institutions, civil society, academia and others development partners.

Related News

Mozambique has conditions to adopt the Chinese model of Special Economic Zones

Mozambique has the necessary conditions to successfully adopt the Chinese model of Special Economic Zones, which helped to boost the Chinese economy, according to researchers Fernanda Ilhéu and Hao Zhang.

In the study The Role of Special Economic Zones in Developing African Countries and Chinese Foreign Direct Investment, researchers from the Lisbon School of Economics and Management noted that over 35 years, the Special Economic Zones have had “a decisive role in the development of places like Shenzhen, Zhuhai, Xiamen, Shantou, Hainan and Shanghai, and that African countries can leverage this experience.

In 2006, the Forum on China-Africa Cooperation gave “significant priority” to creating up to 50 SEZs abroad, which are being implemented, with US$700 million invested by Chinese companies in 16 EEZ, according to information from China’s Trade Ministry.

Increasingly focused on business abroad, China needs raw materials and African markets to which to export its products, but can also benefit from shifting some of its industries to Africa, as the cost of Chinese labour increases.

The approach to Africa has involved through loans and financing for the construction of infrastructure, and “the development of African countries requires China’s increasing involvement,” including “collaborating in the development of SEZs,” the authors argue.

Regarding Portuguese-speaking countries, the average annual growth of trade between 2002 and 2012 totals 37 percent, turning China into the largest trading partner and largest export market for those countries.

The relationship has proved to be “dynamic in both directions,” they added, with hundreds of companies from Portuguese-speaking countries operating in China and Chinese investment in those countries of around US$30 billion, according to China’s Trade Ministry.

As for the SEZ, the two researchers focused their attention on the Mozambican Manga-Mungassa (Beira, Sofala province) SEZ, established in May 2012, under the management of China’s Dingsheng International Investment Company (Sogecoa Group), which has plans to invest close to US$500 million.

Nearing completion, the first phase includes the construction of warehouse units, followed by the “operational” phase, with construction of additional infrastructure such as hotels and housing, and finally the free industrial zone, where high tech units will be installed.

“In terms of knowledge transfer, Mozambique has made active steps in learning from the experience of Chinese SEZs and using this model to attract foreign investment,” they said.

In 2012 the Mozambican government created the Office for Economic Areas with Accelerated Development (Gazeda) that in addition to Manga-Mungassa, is responsible for the projects of the Belulane Industrial Park, the Locone and Minheuene Free Industrial Zones and the Crusse and Jamali integrated park.

On 6 May, 2014 the Mozambican government approved the establishment of the Mocuba SEZ, a sign of the “determination to create more conditions and to look for more opportunities and economic measures to create jobs and generate wealth,” in the country, the study said.

According to the authors, Mozambique has a strategic location, the ability to attract investment through the diaspora, as well as its model of economic growth and development in its favour, although there remain difficulties in infrastructure and technological development.

“The Chinese SEZ model can be successfully applied to the Manga-Mungassa area,” they concluded.

Related News

Mining companies can help turn on the lights across sub-Saharan Africa, says World Bank

Mining companies can play a key role in harnessing Africa’s abundant clean sources of energy to overcome the lack of electricity which affects at least one in three Africans, says a new World Bank report released in Cape Town on 9 February 2015 at Mining Indaba.

In its report, entitled “Power of the Mine: A Transformative Opportunity for Sub-Saharan Africa”, the Bank calls on the mining industry to work more closely with electricity utilities in the region to meet their growing energy demands. Rather than supplying their own energy on site, mines can become major and reliable customers for electricity utilities or independent power producers (IPPs) which can then grow and develop better infrastructure to bring low-cost power to communities.

Power is critical to mining companies’ operations and, by becoming “anchor customers” for electricity utilities, mines can save hundreds of millions of dollars in supplying their own power.

Sub-Saharan Africa, as a region, only generates 80 gigawatts of power each year for 48 countries and a population of 1.1 billion people. Two-thirds of people in the region live entirely without electricity and those with a power connection, suffer constant disruptions in supply. Without new investment and with current rates of population growth, there will be more Africans without power by 2030 than there are now.

The report finds that mining’s demand for power in Sub-Saharan Africa will likely triple between 2000 and 2020 to reach over 23,000 MW. This could be higher than non-mining demand for power in some countries. Yet, many mining companies are still opting to supply their own electricity with diesel generators rather than buy power from the grid – often because of shortcomings in national power systems in the region.

According to the report, another 10 gigawatts of electricity will be added to meet mining power demand by 2020 from 2012 levels – and a part of this is projected to come from “self-supply” arrangements costing mining companies up to $3.3 billion.

But new models of power supply for mines are emerging across Sub-Saharan Africa – including mines self-supplying and selling to the grid or serving as anchor consumers for IPPs. The report estimates around $6 billion in potential public-private partnership opportunities for new power generation from clean energy sources (including natural gas and hydropower) in Guinea, Mauritania, Tanzania and Mozambique – countries with strong expected growth in power demand from the mining sector.

“Power-mining integration can bring substantial cost savings to mines, electrification to communities and investment opportunities to the private sector. But to be successful, we need governments, power utilities and mining companies to work together,” said the World Bank’s Vice President for Africa Makhtar Diop. “Lack of energy stunts the economic growth that’s needed to reduce poverty and boost prosperity for all Africans. Integrating mining demand into national and regional power systems – especially in mineral rich and energy-poor countries – can bring enormous benefits to countries and communities.”

The report cites the example of Guinea, where mining contributes more than half of the country’s total exports and provides more than 20 percent of all fiscal revenues – but where national electrification rates are among the lowest in Africa. For instance, by joining a number of mines together and contracting an independent power producer to generate and transmit electricity to the mines through a high voltage mini-grid, the mining companies would save an estimated $640 million in self-supply costs while bringing affordable and reliable energy to at least 5 percent of Guinea’s people.

“By choosing grid-based and cleaner power sourcing options, which are typically priced lower than self-supplied electricity from diesel or heavy fuel oil, mining companies will be able to meet their electricity needs while also helping to light up the community,” said Anita George, Senior Director of the World Bank’s Energy and Extractives Global Practice. “In turn, countries will benefit from improved competitiveness of the mining companies, greater tax revenues from mines and more job opportunities for local people.”

The report states that though there are risks associated with power-mining integration – for example from falling commodity prices or a shortage of transmission links – regulatory and financial solutions can help mitigate these risks. A key element is for countries across Sub-Saharan Africa to continue with their power sector reforms and create an attractive operating environment for IPPs, including renewable energy developers.

The report was funded by the Energy Sector Management Assistance Program (ESMAP) and the South African Fund for Energy, Transport and Extractives (SAFETE).

Resources

» Infographic: Power of the Mine

» Africa Power-Mining Database

» World Bank Live | The Power of the Mine: A Transformative Opportunity for Sub-Saharan Africa

Related News

IMF Note on Global Prospects and Policy Challenges

The following Executive Summary is from a note by the Staff of the IMF prepared for the 9-10 February 2015 G-20 Finance Ministers and Central Bank Governors Meeting in Istanbul, Turkey.

While global growth will receive a boost from the decline in oil prices, the outlook has been revised down. The oil price decline, which reflects to an important extent higher supply, mainly a rise in production in the United States and OPEC’s decision to maintain current production, will boost global growth by lifting private demand. However, this boost is projected to be more than offset by negative factors, including the drag in investment associated with diminishing medium term growth prospects. Accordingly, global growth in 2015-16 is revised down by a ¼ percentage point to 3.5 and 3.7 percent, respectively.

Market volatility has increased and there have been adjustments in credit and currency markets. Currencies have depreciated and spreads have risen in many emerging markets, notably but not only in commodity exporters. Spreads on high-yield bonds and products exposed to energy prices have widened, but long-term government bond yields have declined in advanced and emerging economies.

Risks are more balanced than in October. Upside risks arise from the demand boost due to lower oil prices, but uncertainty about their future path, which depends on the drivers of the price decline, has also increased. Downside risks linked to financial market sentiment – given prospects for U.S. monetary normalization – are compounded by potential external and balance sheet vulnerabilities in oil exporters. Stagnation and low inflation remain a concern in the euro area and Japan and geopolitical risks continue to be high.

Strong policy action is needed to raise growth and mitigate risks:

-

Advanced economies should maintain supportive policies. In most advanced economies substantial output gaps and below-target inflation suggest that the boost to demand from lower oil prices is welcome, and that the monetary stance should remain accommodative. Where risks of further decline in inflation expectations are present – notably the euro area and Japan – continued monetary accommodation is needed, and the recent ECB announcement of an asset purchase program is welcome. Fiscal policy should be growth friendly, including by moderating the pace of consolidation and enhancing infrastructure investment in countries with identified needs, large output gaps, and relatively efficient investment processes.

-

In many emerging economies policy space to support growth remains limited. In some, lower oil prices will alleviate inflationary pressures, allowing for a more gradual tightening of monetary policy. Oil exporters that have accumulated savings and have fiscal space can let fiscal deficits increase and allow a more gradual adjustment of public spending. For others with less policy space, exchange rate flexibility will be a critical buffer to the shock. Some will have to strengthen their policy frameworks to avert persistently higher inflation and adapt to a protracted deterioration in terms of trade. Similar to advanced economies, and with the same caveats, infrastructure investment is needed to ease supply bottlenecks in some emerging economies.

-

Lower oil prices offer an opportunity to reform energy subsidies and taxes in both oil exporters and importers. The removal of general energy subsidies should be used toward more targeted transfers and to lower budget deficits where relevant.

-

There is an urgent need for structural reforms to raise potential output across the G-20 members. Labor market reforms in advanced economies undergoing population aging should aim at raising labor participation, and actions to increase labor demand and remove impediments to employment are also needed in euro area economies and some emerging markets. Reforms to improve the functioning of product markets are also needed in Japan and the euro area, and reforms to improve productivity and raise potential output are key in many emerging economies. A new momentum is needed in the global trade dialogue.

Related News

Environmental Goods Agreement talks focus on clean energy products

A fifth discussion round on the “green goods” trade talks was held at the end of January in Geneva, Switzerland between the now 15 participating WTO members.

The latest round of talks towards securing a tariff-cutting deal on select environmental goods made progress at the end of January, trade sources say, with several participating countries presenting indicative lists of product nominations related to cleaner and renewable energy, as well as energy efficiency. Following another discussion round next month, the talks for an Environmental Goods Agreement (EGA) could move into full negotiation mode in the second quarter of this year, officials confirmed, as long as the process continues to head in the right direction.

The US and the EU are said to have tabled the largest lists of indicative product nominations in the energy-focused round, with Australia, Canada, Japan, New Zealand, South Korea, and Switzerland also proposing products to include. China has not yet come forward with indicative product nominations for either this round or the ones preceding it, although it reportedly promised to do so for the EGA’s next session in mid-March, citing the need for more time in order to co-ordinate internally.

The January meeting reportedly saw some technical discussion on renewable energy products, including in relation to component parts. Several participants backed including equipment used in hydropower applications in the eventual EGA. Sources say that some participants also expressed preferences for including goods related to nuclear power, biodiesel, methanol, wood products, as well as hybrid vehicles, all of which are likely to prompt some further conversations within the group.

These talks are the result of a pledge made a year ago at the World Economic Forum (WEF) gathering in Davos, Switzerland, where a group of 14 WTO members announced plans to negotiate this Environmental Goods Agreement. Formal talks then began last July.

In the past, EGA participants said that they would build on a list of environmental goods under 54 tariff lines agreed to by the Asia-Pacific Economic Cooperation (APEC) forum in 2012, with the possibility of including other products. The 21-country APEC group has committed to lowering applied tariffs on these 54 tariff lines to five percent or less by the end of this year.

From discussion to negotiation

March’s discussion round will focus on environmental monitoring, analysis, and assessment, environmentally-preferable products, and resource efficiency. Sources have confirmed that the discussion approach has served to help participants fine-tune their product proposals, particularly in terms of “ex-outs,” which are product descriptions where international customs codes are not detailed enough. A total of five technical discussion rounds have been held so far in Geneva, Switzerland, each examining product nominations related to specific environmental goods categories or sectors. EGA participants have said that this “category approach” is geared towards ensuring the environmental credibility of the products nominated and selected for inclusion in the eventual list slated for tariff cuts.

EGA negotiators reportedly agreed at the January session that each participant’s initial product nominations – across each of the environmental goods categories discussed – should be put forward by the beginning of April. That date represents a soft deadline, however, with participants agreeing to be flexible if necessary. Once EGA participants come forward with these compiled lists, the talks would then move into a second phase geared more towards concrete negotiations, beginning with a week of consultations in early May. Two further rounds were reportedly agreed to at the January session, one planned for 15-19 June and another for 27-31 July.

Climate context

While January’s discussions focused on the details of trade in energy-related products, delegates are reportedly keeping in mind parallel efforts to negotiate a global climate deal under the UN Framework Convention on Climate Change (UNFCCC), in time for this December’s Conference of the Parties (COP) in Paris, France. A number of EGA participants have said that the deal offers an opportunity for trade policy to do something positive on climate action. With the energy supply sector being the largest contributor to global greenhouse gas (GHG) emissions, according to UN climate scientists, boosting trade in clean energy and energy efficiency products could play a role in curbing man-made climate change.

“Reducing tariffs on environmental goods can enable innovation and deployment to other countries, thus helping to scale up low carbon development,” said Danish Ambassador to the WTO Carsten Staur at an event hosted by ICTSD in January on the EGA’s climate potential.

A number of goods relevant for the supply of clean energy, in particular solar cells, panels, and modules, are already duty-free in all EGA markets due to the initiative’s current participants also being signatories to the WTO’s Information Technology Agreement (ITA) – a separate plurilateral tariff-cutting initiative covering select information and communication technology (ICT) products. Various other goods in this area could, however, still usefully be added to the list according to some researchers.

EGA participants have set themselves the goal of reaching some form of agreement by the WTO’s tenth ministerial conference this December in Nairobi, Kenya. Whether the EGA talks could have come far enough along to deliver a signal of success in time for the Paris climate talks, which are scheduled prior to the WTO’s Nairobi meet, remains an open question and will be difficult to evaluate until participants move into more formal negotiations.

ITA lessons?

In the corridors at the January session, some delegates reflected on the need to learn from the ITA experience, particularly around a review process for the eventual EGA list. Efforts among a subset of the ITA’s signatories to expand the deal’s product coverage to reflect the realities of today’s trade – given the technological advances seen since the original agreement was finalised in 1996 – have repeatedly stalled in recent years. The negotiations are currently deadlocked over a disagreement between China and South Korea.

Some experts have argued that it would be important for the EGA negotiations to create a review mechanism as part of the EGA in order to ensure a “living list.” This could be useful in the context of evolving climate mitigation and adaptation technologies and needs, for example, as well as keeping pace with other environmental challenges. However, no detailed formal discussion has yet taken place on this topic, although some sources suggest that a forthcoming EU non-paper on draft elements for the eventual EGA text – which the 28-nation bloc has suggested it will circulate to other EGA participants following internal consultations – could possibly prompt further talks in this area.

New members

The latest round saw Israel formally join the talks, following domestic approval by existing members, bringing total EGA participants to 15. Turkey and Iceland have also applied to join the initiative, and sources say that the various domestic procedures among other participants will likely have concluded in time to bring these two nations into the talks by the March round.

This article is published in BioRes, Volume 9 - Number 1, by the International Centre for Trade and Sustainable Development (ICTSD).

Related News

The LPI gender strategy: a learning tool for empowering women

The Expert Group Meeting (EGM) organized by the Land Policy Initiative (LPI) on 4 and 5 February 2015 in Entebbe, Uganda, was successful in reviewing and validating the Gender Strategy of the organization. The meeting provided further recommendations for the finalization of the document, and identified key follow-up actions and activities as well as the actors to play specific roles in their implementation.

“We are grateful to all participants for their valuable suggestions on improving the Gender Strategy,” said Ms Joan Kagwanja, Chief of the LPI, during the closing session. She pointed to fact that the meeting developed a clear action plan, and “therefore holds LPI accountable for the implementation.”

The meeting was officially closed by Ms Naome Kabanda, representative of the Uganda Ministry of Lands, Housing and Urban Development. In her closing remarks, Ms Kabanda noted that some countries, such as Rwanda and Ethiopia, can be crucial partners and good case studies on land and gender issues. She added that the LPI Gender Strategy “will be quite instrumental as a learning tool for other institutions, and for empowering women.”

The meeting was attended by 20 experts drawn from land and gender Ministries of Member States, Regional Economic Communities (RECs), research institutions, civil society organizations, international organizations, and United Nations agencies.

Background

The LPI has developed the draft gender strategy as a guide to mainstreaming gender in the land policy development and implementation processes in Africa. The main objective of the meeting was to review and provide inputs to the LPI Gender Strategy, with a view to validating information, data, and evidence presented in the document.

“Today, in many African rural communities, women still do not have access to, and control of land needed for production. They benefit less from economic opportunities than men, because they are not land owners,” noted in her opening remarks Ms Sarah Kulata–Basangwa, acting Director of Land Management, representing the Ministry of Lands, Housing, and Urban Development of Uganda. She highlighted the need for Africa to close the gender gaps, in order to achieve significant productivity gains. Ms Kulata–Basangwa further noted the need for gender responsive public awareness initiatives, and the importance of developing land policy action plans with gender inclusive monitoring and evaluation indicators.

Ms Joan Kagwanja, Chief of the LPI, noted that the EGM happens at the heels of the declaration by the African Union of 2015 as the “Year of Women Empowerment and Development towards Agenda 2063.”

“We start our contribution to the AU year of women’s empowerment by providing an avenue to address the challenges of women’s access to, and control of land as an entry points to achieving the goals of the Agenda 2063,” added Ms Kagwanja.

Main recommendations provided by the EGM will contribute to the finalization of the strategy by the LPI.

The Land Policy Initiative is a joint programme of the tripartite consortium consisting of the African Union Commission (AUC), the African Development Bank (AfDB), and United Nations Economic Commission for Africa (ECA). Its mandate is to facilitate the implementation of the AU Declaration on Land Issues and Challenges in Africa.

Related News

24th AU Summit: Decision on the Report of the High Level African Trade Committee (HATC) on Trade Issues

The Assembly,

1. TAKES NOTE of the Report of the High Level African Trade Committee held in January 2015 and ENDORSES the recommendations contained therein;

On the Continental Free Trade Area (CFTA)

2. TAKES NOTE of the progress towards the establishment of the Tripartite Free Trade Area involving the Southern African Development Community (SADC), the East African Community (EAC) and the Common Market for Eastern and Southern Africa (COMESA) and the launch of the Economic Community of West African States (ECOWAS) Common External Tariff (CET) with effect from January 2015;

3. URGES Member States to expedite the accession and ratification to the regional free trade agreements;

4. REQUESTS the Ministers of Trade to propose options on levels of trade liberalization to serve as an indicative basis on which to start CFTA negotiations;

5. EMPHASISES the importance of involving various stakeholders such as the Private Sector, Parliamentarians, Civil Society, Academia, etc. in the process of establishing the CFTA through appropriate mechanisms so as to ensure ownership of CFTA by the peoples of Africa;

6. MANDATES the Chairperson of the HATC in collaboration with the Chairperson of the Commission to engage in High Level consultations for the establishment of the CFTA;

7. REQUESTS the Commission, in collaboration with UNECA and RECs, to undertake technical work, required studies and preparation in advance of the negotiations including the preparation of the draft negotiating texts;

8. REAFFFIRMS the commitment to launch CFTA negotiations in June 2015 and in this regard MANDATES Ministers of Trade to meet and finalise preparations for the launch;

On the World Trade Organisation (WTO)

9. WELCOMES the breakthrough in the WTO Doha negotiations and REITERATES the importance of African countries speaking in one voice to ensure that Africa’s interests are adequately addressed within the multilateral trading system;

10. URGES Member States to identify key issues in the post-Bali work programme that facilitate the achievement of Africa’s strategic structural transformation and regional integration agenda;

On African Growth and Opportunity Act (AGOA)

11. NOTES WITH APPRECIATION the announcement made by President Obama on the occasion of the Africa-US Summit held in August 2014 expressing commitment towards the reauthorization of AGOA;

12. CALLS UPON the US Congress to preserve AGOA as the cornerstone of Africa-US trade and investment partnership by ensuring the timely reauthorization of AGOA co-terminus with the Third Country Fabric Provision;

13. FURTHER CALLS UPON AGOA-eligible countries to enhance the advocacy to complement the efforts of the African Group of Ambassadors in Washington, USA towards the reauthorization of AGOA.

Related News

24th AU Summit: Decision on the Report of the Commission on Development of the African Union Agenda 2063

The Assembly,

-

TAKES NOTE of:

-

the Report of the Commission on the development of the African Union Agenda 2063, as well as the Agenda 2063 Framework Document; Agenda 2063 Popular version; and the Agenda 2063 First Ten Year Implementation Plann;

-

the presentations of the Report of the Follow-Up Ministerial Committee on Agenda 2063.

-

-

ONCE AGAIN WELCOMES the consultative nature of the Agenda 2063 Development Process;

-

EXPRESSES its appreciation to the Commission for the excellent work accomplished;

-

ALSO EXPRESSES its high appreciation to the Ministerial Follow up Committee for its proactive work towards the smooth implementation of the Bahr Dar Ministerial Retreat conclusions of January 2014;

-

RECALLS Decision EX.CL/Dec. 832(XXV) taken at the 25th Ordinary Session of the Executive Council held in June 2014 in Malabo, Equatorial Guinea, requesting Member States to conduct national consultations on the Agenda 2063 Framework Document and Popular Version, and to provide inputs to the Commission by 31 October 2014 as well as Decision EX.CL/855(XXVI) adopted at the 26th Ordinary Session of the Executive Council in Addis Ababa, Ethiopia, in January 2015;

-

ADOPTS the Agenda 2063 Framework Document and Popular Version;

-

REQUESTS:

-

the Commission to intensify measures aimed at popularizing the fifty-year continental agenda;

-

Member States and the RECs to accelerate the domestication of Agenda 2063 and integrating it into their respective Development Initiatives and Plans;

-

the Commission to finalize all necessary consultations on the First Ten Year Implementation Plan of Agenda 2063 with a view to submitting it at the June 2015 meetings of the AU Policy Organs.

-

-

TAKES NOTE of the commendable progress made in the formulation and development of the following Agenda 2063 Flagship projects and promoting reconciliation in Africa:

-

Integrated High Speed Train Network;

-

Great Inga Dam;

-

Single African Aviation Market;

-

Outer Space;

-

The Pan African E-Network;

-

Creation of an Annual African Consultative Platform;

-

Establishment of the Virtual University;

-

Free Movement of Persons and the African Passport

-

The Continental Free Trade Area;

-

Silencing the Guns by 2020;

-

Development of a Commodity Strategy;

-

Establishment of the Continental financial Institutions, including the African Central Bank by 2030.

-

-

REQUESTS the Commission to:

-

present detailed road maps for the implementation of each of the flagship projects for consideration by the AU Policy Organs in June 2015;

-

ensure that the issues and concerns of African Island and Landlocked States are adequately mainstreamed into all continental frameworks for political, social, cultural and economic development, including the addition of a representative of Island States to the Bahr Dar Ministerial Follow-up Committee;

-

facilitate access to funds required by Island States, including under the Agenda 2063 Resource Mobilization Strategy, as well as Climate funds by 2020.

-

-

AUTHORISES the convening of a Ministerial Retreat as proposed by the Commission and the Ministerial Follow-Up Committee in between the two summits to brainstorm on the draft 1st 10 year Implementation Plan of Agenda 2063 as well as other relevant issues including all flagship projects, and those pertaining to agricultural transformation and eradication of poverty, so as to report at the next Summit in June 2015. In the same vein REQUESTS the Commission to pursue consultations with the RECs and other stakeholders so as to gather all contributions from all concerned partners in this process;

-

UNDERSCORES the need to undertake the restructuring of the Commission to enable it to carry out the critical mandate linked with the implementation of Agenda 2063 with requisite human and financial resources and institutional capacity. In this regard, CALLS UPON the Commission to pursue its efforts in ensuring prudent management of its financial resources and on Member States to fulfil their financial obligations to the AU and CALLS ON Partners to release the pledged funds in a timely manner to enable the AU carry out its programmes in predictable and sustainable manner. In the interim, REQUESTS the Commission to establish a temporary structure to oversee the conclusion of the First Ten-Year Plan, and coordinate finalisation of the identified fast track projects;

-

ALSO CALLS UPON Member States to take necessary measures for the effective implementation of the 1999 Yamoussoukro Decision on the Liberalisation of Air Transport Markets in Africa and adopt its regulatory texts in this respect;

-

UNDERSCORES the need for the continent to fully integrate the Blue Ocean Economy and its great opportunities within the framework of Agenda 2063 through development of requisite expertise;

-

STRESSES, at continental and regional levels, the need to ensure smooth division of labour on the basis of the principles of subsidiarity and complementarity among all stakeholders, particularly the AUC, the RECs and the NPCA in Agenda 2063;

-

TAKES NOTE of the budgetary requirement of the Pan African E-Network amounting to USD 230,000.00 and AUTHORISES the Commission to mobilize resources in this regard;

-

ALSO TAKES NOTE of the offer by the Arab Republic of Egypt to host the proposed African Space Agency after the conclusion of the draft space policy that is being developed by the AU Space Working Group as articulated in AU Agenda 2063.

Related News

AU Assembly Special Declaration on Illicit Financial Flows

We, the Heads of State and Government of the African Union, having met at our Twenty Fourth Ordinary Session of the AU Assembly in Addis Ababa, Ethiopia, from 30 to 31 January 2015;

Recognizing the Conference of Ministers Resolution 886 (XLIV) which established the high-level panel on Illicit financial flows from Africa,

Concerned with the increasing scale and extent of Illicit Financial flows from Africa, particularly from our extractive industries and natural resources which constitute a drain on the resources required for Africa’s development. Whereby, it is estimated that Africa has lost up to US$ 1.8 trillion between 1970 to 2008 and continues to lose extensive finances estimated up to US$150 billion annually through Illicit Financial Flows (IFF) or “Illicit Capital Flight” mainly through tax evasion, mispricing of trade and services by multi-national companies;

Aware that the problem of illicit financial flows is exacerbated by corrupt tendencies of government agencies, lack of or weak African institutions both at national and continental levels in all sectors, governance challenges, political instability and conflicts, weak tax administration, and lack of capacity to monitor and curb such criminal activities among others;

Realising the growing need for domestic resource mobilisation for the attainment of our continental development visions and goals particularly Agenda 2063 and the Common African Position on the post 2015 Development agenda, which both call for inclusive growth, sustainable development and social and economic structural transformation of Africa through optimal utilization of our natural resource endowments;

Conscious that the amount of illicit financial flows from Africa is greater than the inflow of Overseas Development Assistance;

Convinced that curtailing illicit financial flows through, inter alia, institutionalizing prudent legal and regulatory regimes, including fiscal policies that disallow financial secrecy, fight corruption, institute and/or strengthen African institutions, build African member states capacity for contract negotiation, tax administration and identify and return the resources lost through illicit financial flows can greatly contribute to the alternative sources of financing Africa’s development agenda;

Further Convinced that the time is now for Africa’s Renaissance, for the continent to regain ownership of its natural resources and to implement sound, prudent management and good governance, with a view to optimizing the benefits derivable from its natural resources in particular extractive sectors and mineral resources for present and future generations while limiting negative environmental and macroeconomic impacts;

Noting the diligence manifested and extensive amount of work undertaken by the High-level Panel on Illicit Financial Flows from Africa, involving extensive consultations with a range of stakeholders in Africa and partners in the United States of America and Europe,

Acknowledging the report of the High Level Panel, and taking note of its findings and recommendations,

Expressing appreciation to the chair H.E. Mr. Thabo Mbeki, Former President of the Republic of South Africa and members of the High Level Panel for the rigorous and comprehensive report produced,

Further Expressing Appreciation to African Governments and organizations and to Africa’s partners and development agencies for their overwhelming support for the work of the Panel,

We hereby:

-

ENDORSE the findings and recommendations of the High Level Panel on Illicit Financial Flows from Africa;

-

DECLARE our COMMITMENT to end the chronic illicit financial flows from Africa which is a huge hindrance to sustainable social and economic development of our continent;

-

RESOLVE to ensure that all the financial resources lost through illicit capital flight and illicit financial flows are identified and returned to Africa to finance the continent’s development Agenda. In this regard DIRECT AUC, supported by member states, to mount a diplomatic and media campaign for the return of illicitly outflown assets.

-

FURTHER DECLARE our COMMITMENT to adopt and implement the findings and recommendations of the High Level Panel on Illicit Financial Flows from Africa and in this connection, we REQUEST the Commission, in collaboration the Economic Commission for Africa, African Development Bank and the RECs to follow-up on the implementation of the recommendations of the High Level Panel report and submit progress reports on the achievements to the Assembly annually

-

CALL UPON the International community to adopt and implement the findings and recommendations of the High Level Panel on Illicit Financial Flows from Africa

-

DIRECT the Commission, the Economic Commission for Africa, and African Development Bank, to disseminate the findings and recommendations of the Panel and undertake further research and capacity-development activities in this regard within the continent and at the global level;

-

REQUEST the continued engagement of the chair H.E. Mr. Thabo Mbeki, Former President of the Republic of South Africa and the Panel in carrying out advocacy work to disseminate the Panel’s findings and to galvanize support from a broad coalition of partners including civil society and private sector to implement the Panel’s recommendations;

-

FURTHER REQUEST the Commission, Economic Commission for Africa, African Development Bank, African Capacity Building Foundation and other development partners to build capacities of African Union member States and institutions, particularly in contract negotiation, tax management, regulatory and legal frameworks, policies, money laundering, asset recovery and repatriation, and resource governance for effective and optimal Management and Governance of our Natural resources.

-

EXPRESS the need to ensure that Illicit Financial Follows and their impact on domestic resources mobilization is given the necessary attention by the 3rd International Conference on Financing for Development, and in this regard, stress the need for robust international cooperation to address the problem.

Related News

France scrambles for ‘New Deal’ with Africa at Paris conference

All eyes were firmly on Africa at the France-Africa forum, which ended on Friday. Business leaders and heads of state gathered in Paris to thrash out new ways of sharing the continent’s staggering growth – this time without the shady connections that have long shaped bilateral relations in the past, they said.

“Africa is our future,” a jetlagged French President belted out at the close of the first round of discussions at the France-Africa forum. “It’s our future because it is the continent with the fastest economic growth in recent years.”

The IMF expects the sub-Saharan region’s economy to grow by 4.9 per cent in 2015, above the global projected growth of 3.5 per cent. And last year, its growth went up by 5.8 per cent.

It was thus no surprise that Hollande made a pitstop to the event between flights from Kiev to Moscow. “I’ve proved by being here, that Paris is the capital of the world,” Hollande quipped.

By inviting African leaders from Senegal, Gabon, Côte d’Ivoire and Nigeria to the French fiunance ministry, Hollande proved France wants Africa to be the centre of its world.

The continent’s rapid growth is largely linked to a fast-growing population, with 70 per cent of Africans now under the age of 35. But many are unskilled and youth unemployment continues to be a scourge on an otherwise impressive record.

“If you don’t give young people something to do, they will find something else to occupy themselves with and it won’t necessarily be pleasant,” said Chris Kirubi, director of Kenyan-based Centum Investment Group.

During one of several round table discussions, Kirubi flagged up the rise of armed groups such as Boko Haram and the growing number of boat-people fleeing Africa for Europe as signs that Africa’s youth needs to be harnessed.

Participants at the forum thus welcomed the announcement of a new Africa-France foundation, geared towards providing skilled training for young African adults.

Spearheaded by Franco-Beninese economist Lionel Zinsou, with the support of the French government, the foundation will have a sister organisation in every country across the continent to offer Africa’s youth better business opportunities and the necessary funding.

The foundation itself has a bankroll of three million euros from the French government but will rely on contributions from other governments and businesses thereafter.

“We are a professional network, we aim to put young people in touch with French businesses so they can work together,” Lionel Zinsou told RFI.

Asked whether France was truly engaging in a win-win partnership with its former colonies, Zinsou replied: “Africa needs forces from everybody…. France, China, Latin America, everyone that can bring experience and knowledge.”

Africa’s growth he says is not enough on its own, he argues.

“Growth at five per cent only provides jobs for 10 million, so you have a gap of 10 million to fill. If we don’t go from five to seven per cent we will not put our youth in the proper jobs, that’s what Africa has to gain.”

And the past? Is the past, Zinsou insists. For French companies, Africa is no longer an inferior but a partner.

Related News

Oil prices positive for trade deficit, foreign reserves

Oil prices hit their lowest level in over five years on 13 January 2015 when Europe Brent was traded for US$45,13 (N$518,53) per barrel.

On 16 March 2009 oil was traded at US$44,12 per barrel and on 3 September 2009 oil cost the equivalent of N$518,52 per barrel based on the daily exchange rate.

Compared to a high of US$115,19 pb on 19 June 2014, prices slumped by 61% and are currently some 56% lower than a year ago and 54% in Namibia dollar terms.

However, prices recovered slightly towards the end of January to US$46,07 per barrel, which is still 58% below prices a year ago.

CONSENSUS

There appears to be consensus among most experts that oil prices will remain at these levels during 2015 while some expect such price levels to prevail over the next two to three years.

The oil price developments are caused by supply and demand as well as the politics of the Organisation of the Petroleum Exporting Countries (OPEC).

Global oil demand increased on average by 1,5% annually between 2009 and 2013 from 84,8 million barrel per day (mb/d) to 90 mb/d, but slowed down to 1,1% between 2013 and 2014.

Demand is expected to grow by some 1,3% in 2015 to 92,3 mb/d. Subdued global economic growth is one of the contributing factors to the slow growth in oil demand, along with technological advances, concerns about climate change, and a shift from primary and secondary sector activities to the service industries.

Oil supply has risen faster due to the boom in shale oil production in the USA and Canada. Oil production in the USA rose by 39% between 2009 and 2013, making the country the third largest oil producer behind Russia and Saudi Arabia.

BALANCE OF PAYMENT

The lower prices also strengthen the balance of payment position. Oil imports accounted for 9% of total imports in Namibia in 2013 amounting to some N$7 billion.

Oil imports ranked as the third largest import item after transport equipment and chemicals. Hence lower oil prices will reduce Namibia’s trade deficit and improve foreign exchange reserves. Motorists are benefiting from substantially lower fuel prices that have dropped in February 2015 to some 20% below pump prices a year ago - levels last seen in the middle of 2012. However, low oil prices are not only good news. Depending on how long they will prevail, they can have a negative impact on oil exploration activities in the country in the medium to long term. In addition, demand from Angolans living in Namibia or coming for shopping could decline once the lower oil prices impact on salary levels, economic activities in Angola, and the value of their currency. Furthermore, since gas prices are linked to oil prices, the price decline can have an impact on the development of the Kudu Gas project, the financial viability of which has been questioned by some experts recently.

COMMODITY PRICES

There was much talk about a looming currency war, meaning countries would devalue their currencies in order to strengthen their competitive position. The current fears indicate the lack of coordinated responses by central banks across the world to the current economic challenges.

The Namibia dollar has appreciated against the Euro since 1 January much stronger than against the US dollar and GBP.

Once the European Central Bank actually starts buying bonds, it can be expected that ‘cheap’ money is looking for better returns in emerging markets as well, as it was the case during the Quantitative Easing in the USA. Quantitative easing is an unconventional form of monetary policy where a Central Bank creates new money electronically to buy financial assets, like government bonds. This process aims to directly increase private sector spending in the economy and return inflation to target.

This could put further upward pressure on the recipient countries’ currencies, such as the Namibia dollar. Copper prices like oil prices have been especially hard hit recently, but have been on a downward trend since the second half of 2013 with some fluctuations along the way. The price for copper dropped to its lowest level since 22 July 2009, when it traded at US$5,340 per ton on 29 January 2015. The metal has lost a quarter of its value over the past twelve months, which is not good news for the Namibian copper mines in particular the commencement of production at the new Tschudi copper mine that is expected towards the end of the first half of 2015.

The drop in prices is a reflection of declining demand because of lower economic activities in particular in China. Uranium prices have lost some ground again after reaching an almost two year high on 17 November 2014 at US$44 per pound. Uranium was traded at US$36,75 per pound end of January 2015, representing a gain of 5% over January 2014.

Related News

Now USA second biggest buyer of Kenyan products

The value of Kenya’s exports to United States increased by nearly a third in the first 11 months of 2014, rendering the US her second most important market after Uganda.

Latest official data show the US bought goods worth Sh35.53 billion by November, 28.5 per cent higher than the Sh27.64 billion raked in over a similar period in 2013.

The US is catching up fast with Uganda, the biggest buyer of Kenyan goods, but whose purchases over the period slumped by 11.4 per cent to Sh43.31 billion, from Sh48.87 billion in the previous year.

USA has leapfrogged the United Kingdom, Tanzania and Netherlands from the fifth position in 2013. This has been attributed to favourable trade policies between it and the African continent, notably through the African Growth and Opportunity Act, which offers export incentives on many commodities.

Kenya’s imports from the US have also grown rapidly over the same period, owing to capital goods such as aircraft, locomotives and spare parts.

In the 11 months, Kenya’s total purchases from USA were worth Sh162.58 billion, more than triple the Sh51.42 billion worth of goods shipped in by end of November 2013.

The AGOA deal is set to expire on September 30 after a 15-year run, which is likely to put a damper on Kenya’s exports to the US if not renewed.

Kenyan trade officials are nonetheless optimistic that it will be renewed by then despite the bureaucracies involved.

“This is not the first time we have been in a situation like this; it’s not an easy process to make recommendations and get institutions that have to approve, especially like the Congress,” Moses Ikiara, managing director of Kenya Investment Authority, told the Star in the sidelines of a Federation of Kenya Employers conference two weeks ago.

Under the Act, Kenya exports tonnes of textiles and clothing to the US but barely utilises its quota fully.

Ikiara said there are plans to host a Kenya-US business conference in Nairobi in September as a follow up to a US-Africa Business Summit held last August.

“Kenya is fast emerging as a major business partner for the US, and as the rest of Africa, it is becoming more important. To manage the trade imbalance, there must then be a chance to export to the US through arrangements such as AGOA,” he said.

Under AGOA, Kenya can export up to 6,000 different products but only does a few currently, in what Ikiara cites as “domestic supply constraints”. The country must thus build a critical mass of the various goods allowable to make sense of exporting, he said, including standardisation.

“It is not so much about market access,” Ikiara, adding that KenInvest, Ministry of Foreign Affairs and International Trade, and embassies are coordinating to benchmark progress on extension of the trade pact.

Related News

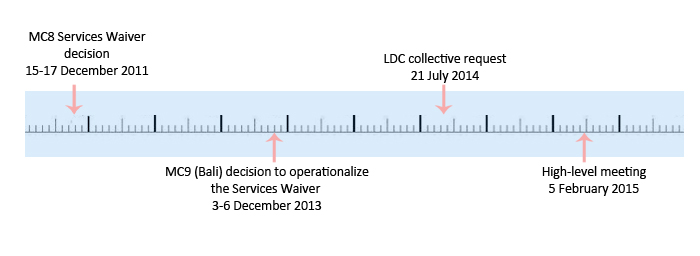

Members move to enact Bali decision on LDC services waiver

At a high-level meeting of the WTO Services Council on 5 February 2015, members discussed measures which would support the growth of services trade in least-developed countries (LDCs) by providing their services exports with preferential treatment. This was an important step in implementing a key Bali decision in support of LDCs, which aims to enhance their participation in world services trade.

At the meeting, over 25 members indicated services sectors and modes of supply from LDCs to which they would give preferential treatment.

In a video message to open the meeting, Director-General Roberto Azevêdo said:

“It is vital that we implement all the elements of the Bali Package without delay – and particularly the decisions on LDC issues. The decision on Operationalising the LDC Services Waiver is one of these, and is extremely important. Services exports from LDCs are increasing rapidly, though of course they are starting from a very low base. We have a duty to support the growth of this sector. I urge potential preference-granting members to indicate where they intend to provide preferential treatment to LDC services and service suppliers. ”

Chairperson Choi Seokyoung of the Republic of Korea reported a “very high level of engagement ” from developed and developing countries in a position to do so who considered treating services exports from LDCs more favourably than those of other WTO members. In their indications, members addressed most of the 74 services sectors in which LDCs have requested preferences.

Some preferences would include: expanding access for the temporary movement of businesspeople (Mode 4) from LDCs for a range of services professions and occupations; waiving fees for business and employment visas for LDC persons; not imposing economic needs and labour market tests for LDC members; and extending the duration of stay of LDC professionals in the markets of preference granting members. These preferences will be implemented once these members have completed their domestic processes and have notified the WTO.

Members based their announcements on a collective request that the WTO Group of LDCs submitted on 21 July 2014, in which they indicated services sectors and modes of supply of interest to them.

The WTO services agreement, the General Agreement on Trade in Services, specifies that each member shall provide non-discriminatory treatment to services and service suppliers of other WTO members (Most-Favoured Nation principle). The LDC Services Waiver, adopted at the WTO Eighth Ministerial Conference (MC8) in 2011, allows non-LDC members to grant preferences to provide all LDCs greater access to their markets. For the first time, this decision allows WTO members to deviate from their Most-Favoured Nation obligation under the services agreement.

In light of the absence of notifications of specific preferences, Ministers from WTO members decided at the Ninth Ministerial Conference (MC9) in Bali, Indonesia, on 3-6 December 2013 to take further steps towards the operationalization of the waiver.

Building LDCs capacity in services trade

At the high-level meeting, many WTO members mentioned various technical assistance initiatives to improve LDC services export capacity. The initiatives include training programmes for LDC service suppliers and support to upgrade infrastructure. Some members announced new initiatives and measures.

In his concluding remarks, the chairperson noted that this meeting was “one important stepping stone towards the operationalization of the waiver, but not the final concluding step. Today's indications show that we are firmly on the way of a joint journey”.

Bangladesh’s Minister for Commerce, Tofail Ahmed MP, spoke about the potential of services to support growth in his country. His full speech is available here.

In her remarks, Uganda’s Minister of Trade, Industry and Cooperatives, Amelia Anne Kyambadde, said: “If converted into notifications, many of the interventions today can provide the WTO with a strong deliverable in response to our collective request and contribution to the DDA for the poorest members.” Uganda is coordinating the WTO LDC Group. Her full speech is available here.

Next steps

The Director-General will help to take forward the outcomes of the meeting and will discuss these issues with the LDC Group on 18 February.

WTO members will assess this high-level meeting at the next Services Council meeting on 19 March.

Members agreed that delegations shall endeavour to notify preferences at the earliest possible, and no later than 31 July 2015.

» Learn more about trade in services in the WTO.

Related News

Building negotiating capacity in Africa to make the most from mining deals

When it comes to negotiating complex mining contracts, governments can often feel that the playing field is tilted in one direction, favoring the private sector.

This is a major challenge for Africa. In the 2013 “Africa Progress Report,” Kofi Annan, the former UN Secretary-General, says poorly negotiated contracts are partly responsible for countries not benefiting from their mineral wealth. The study compared the selling price for five mining assets in the Democratic Republic of Congo with an independent assessment of their value, and found the difference to be over $1 billion.

Global leaders at the G7 Summit also recognized the issue last June by launching an initiative to provide developing country partners with capacity building opportunities for negotiating complex commercial contracts, focusing initially on the extractives sector.

Negotiating mining contracts is an extremely complex endeavor that requires a clear set of objectives articulated by leadership; a variety of technical skills in law, engineering, economics, finance, and other areas; a high level of coordination across relevant government entities and the ability to pursue a consistent course over time.

To reach an agreement that is stable over time, the investor-state relationship must be perceived to be fair by the foreign investor and the host government, as well as local communities, broader civil society and the business community. A key to achieving the perception of fair negotiations is incorporating transparency into the process from the outset. When negotiations leave one party at a disadvantage, stakeholders notice and this can lead to long-term grievances and possibly even instability that can negatively impact the country and investors.

“Mining contracts that are negotiated in a fair and transparent fashion are more sustainable in the long-term for all the stakeholders involved and they better reflect the country’s best interests,” said Paulo de Sa, Practice Manager of the Energy and Extractives Global Practice of the World Bank Group.

To build global capacity on the negotiation of mineral development agreements, the World Bank Group hosted two international training workshops that brought together government representatives from 18 countries. In May 2014 the first workshop was held in Arusha, Tanzania with 35 representatives from Anglophone Africa including from Sierra Leone, Tanzania, Ethiopia, Zimbabwe, Mozambique, Liberia, Uganda, Malawi and Rwanda. The second training workshop for Francophone Africa was held in Ougadougou, Burkina Faso in October 2014 and included 35 representatives from countries spanning Senegal, Congo, Burkina Faso, Guinea, Mali, Niger, Togo, Madagascar and Mauritania.

One of the workshop attendees, Venance Bahati, Tax Audit and Analysis Manager at the Tanzanian Minerals Audit Agency said that “the course was very relevant to the Tanzania situation, especially on the issues of negotiation preparation skills and issues such as community aspects and fiscal items.”

Technical training at the workshops focused on the contract negotiations process (including intergovernmental coordination, negotiations techniques) and the general terms and conditions related to mineral development agreements (including fiscal instruments, community development, and local content).

Daye Kaba, Partner at Fasken Martineau law firm and an international expert in mining law and contract negotiations, presented at the workshop and emphasized that “building of capacity within governments not only enables countries to negotiate better agreements and have a better grasp of the implications of the agreements they enter into, but is also welcomed by mining companies as it facilitates the negotiation process.”

These capacity building workshops were made possible by support from the World Bank Group through the Extractive Industries-Technical Advisory Facility (EI-TAF) trust fund, as well as the African Legal Support Facility (ALSF), the International Institute for Sustainable Development (IISD), and the Sustainable Development Strategies Group (SDSG).

Related News

Update on the Tripartite Free Trade Area Negotiations: Statement by Mr Sindiso Ngwenya, Secretary General of COMESA

Statement by Mr Sindiso Ngwenya, Secretary General of COMESA and Chairperson of the COMESA-EAC-SADC Tripartite Task Force, to the African Union High Level African Trade Committee (HATC)

Addis Ababa, January 2015

I wish, at the very outset, to express appreciation to the African Union Commission for, firstly, inviting me to this meeting of the High Level African Trade Committee in my capacity as the Chairman of the COMESA, EAC and SADC Tripartite Task Force on the Tripartite FTA to share with the High Level Committee our experiences of the on-going negotiations for the establishment of the COMESA-EAC-SADC Tripartite Free Trade Area whose implementation will be an important contribution to the Continental Free Trade Area scheduled to be launched in 2017.

BACKGROUND TO THE COMESA-EAC-SADC TRIPARTITE NEGOTIATIONS

Given the overlapping membership of the 3 Regional Economic Communities of COMESA, the EAC and SADC, the Heads of State of the 3 RECs decided, in 2008, that to overcome this challenge, there was need to establish a single FTA for the 26 countries that constitute the membership of the 3 RECs.

The Heads of State, therefore, launched negotiations for the establishment of the COMESA-EAC-SADC Tripartite Free Trade Area in 2011 and agreed that these negotiations should be completed by 2014.

Negotiations on trade on goods have more or less been finalised and the COMESA-EAC-SADC Tripartite countries should launch a trade in goods FTA later in the year.

Negotiations on trade in services and other trade-related areas such as competition policy and intellectual property rights will commence soon after the launch of the trade in goods FTA.

The Tripartite FTA, with 26 countries or 48% of the membership of the African Union (AU), 51% of its Gross Domestic Product and 56% of its population (2013 data, the World Bank), will be a significant step towards the establishment of the African single market.

The Tripartite FTA will not only be a major boost to intra-regional trade but would also stimulate the level of economic activity across the region, reducing poverty through employment creation and generation of wealth.

COMESA-EAC-SADC TRIPARTITE NEGOTIATION PROCESS AND STATUS

Negotiations Principles and Modalities

Negotiations for the Tripartite FTA were guided by 11 principles that were adopted by the Heads of States and Government. These were:

-

that the negotiations would be REC and/or Member State driven;

-

Variable geometry;

-

Flexibility and Special and Differential Treatment;

-

Transparency;

-