Search News Results

Caucus of African Central Bank Governors 2015

On 29 March 2015, the Economic Commission for Africa and the African Union Commission will hold the second Caucus of African Central Bank Governors, in Addis Ababa, on the margins of the eighth Joint Annual Meetings of the African Union Specialized Technical Committee on Finance, Monetary Affairs, Economic Planning and Integration and the Economic Commission for Africa Conference of African Ministers of Finance, Planning and Economic Development.

The main objectives of the Caucus are to identify concrete follow-up measures to the outcomes of the first Caucus, which was held in Abuja in 2014, and measures to enhance the role of governors of central banks in the consultations leading up to the third International Conference on Financing for Development, which will take place in July 2015. The outcomes of the Conference will have direct implications for central banks in Africa. The Caucus, which brings together the governors of central banks of a number of African countries, will provide a unique opportunity for governors to engage in structured dialogue on the issues that they would like to see reflected in the outcome document of the Conference.

The Caucus is intended to come up with concrete proposals on how to fully engage central bank governors from Africa in the consultations leading up to the International Conference on Financing for Development. In addition, the governors will produce a statement on the issues that they would like to see reflected in the outcome document of the Conference. Lastly, an action plan will be developed, outlining a road map for the implementation of the proposals of the first Caucus.

In addition to governors of central banks from Africa, the Caucus will be attended by key actors in the post-2015 development agenda and financing for sustainable development, to ensure synergies between the two processes.

2015 Conference of Ministers

The 8th Joint Annual Meetings of the African Union Specialized Technical Committee on Finance, Monetary Affairs, Economic Planning and Integration and the ECA Conference of African Ministers of Finance, Planning and Economic Development will take place from 25-31 March 2015 in Addis Ababa, Ethiopia. The Conference will tackle the theme, Implementing Agenda 2063 – Planning, Mobilizing and Financing for Development in a Ministerial segment from 30-31 March 2015, which will be preceded by an expert’s segment from 26-27 March.

The Conference will be held against a backdrop of intensive activities leading up to the MDGs 2015 deadline and the global negotiations on the post 2015 development agenda.

In 2013 the Joint Conference focused on industrialization for Africa’s emergence, and shifted attention in 2014, to inclusiveness and transformative development for Africa. A call was made to African countries to adopt dynamic industrial policies with innovative institutions, effective processes and flexible mechanisms to transform their economies to bring about inclusive and sustainable economic and social development.

The format of the Conference will comprise intellectually stimulating plenary sessions, as well as round table debates and side events intended to deepen discussions on the theme. The Conference will also feature the inaugural lecture for the Annual Adebayo Adedeji Lecture Series, launched in Abuja in 2014 and the launch of the annual Economic Report on Africa, which tackles the theme of trade and industrialization.

The report builds on the key messages of the previous editions of ERA focusing on industrialization and structural transformation. Both ERA 2013 and ERA 2014 emphasized the role of trade in fostering industrialization, both at the regional and the global level, and underlined the importance of implementing trade policies in Africa, mainly aimed at overcoming market and institutional failures that hinder export competitiveness. This year’s report further explores the question of how trade can serve as an instrument for accelerating industrialization and structural transformation in Africa.

Related News

Managing rapid urbanization can help Uganda achieve sustainable and inclusive growth

Uganda’s urban population will increase from six million in 2013 to over 20 million in 2040. Policy makers need to act now to ensure that this rapid urbanization is managed well, so it can contribute to Uganda’s sustainable and inclusive growth, a report released on 3 March 2015 by the World Bank Group shows.

For the first time, the report compares data on urban areas and their populations in a consistent manner across Uganda, providing governments and local leaders with analyses to improve planning and coordination to deliver better services, jobs and opportunities, making cities more competitive.

“The typical Ugandan city has grown rapidly, but without sufficient policy coordination. As a result, urbanization has not necessarily resulted in increased productivity, with the majority of jobs created involving low productivity activities,” said Hon. Daudi Migereko, Minister of Lands, and Housing and Urban Development. “This report will help government get a better picture and take action on how to spur the economy from the lackluster growth performance experienced over the past half-decade, to a higher growth path that can catapult the country into middle income status.”

The Fifth Uganda Economic Update, titled: “The Growth Challenge: Can Ugandan Cities get to Work?” focusses on urbanization and notes that while the majority of the population is still concentrated in rural areas, non-agricultural economic growth and jobs are concentrated in urban areas. The report shows that while cities can help propel growth, the speed of urbanization is challenging and can lead to congestion and strain infrastructure, lowering productivity.

“By managing the urbanization process effectively, Uganda will be more likely to achieve middle income status by 2040. However, current patterns of growth pose a significant challenge,” said Philippe Dongier, the Country Director for the World Bank Group for Uganda, Tanzania and Burundi. “Urban population growth multiplies the number of challenges already facing urban areas and hinders their ability to be the sources of growth, to create productive jobs and to provide decent housing to urban residents.”

The Update has been prepared to assist government in ensuring that its cities are ready to accommodate the increasing number of residents expected to settle in urban areas and able to facilitate the growth of business enterprises, thereby creating opportunities for productive employment for a greater proportion of city residents.

“Cities have the potential to propel growth, attracting capital, spurring innovation, providing higher productivity jobs. Services can be provided more cost-effectively, improving access for all,” said Somik Lall, Lead Urban Economist. “To reap these benefits, urban growth needs to be managed well by planning for land use and basic services, connecting to make a city’s markets accessible, and financing to meet infrastructure needs.”

“To ensure the development of functional cities, the public sector will require the coordination of a range of different types of investment, including investment in physical planning for buildings and the provision of transport, housing and social services,” said Rachel Sebudde, Senior Economist and Lead author of the report. “Each layer faces its own coordination challenges. It is better to anticipate and plan for this at the very early stages of the urbanization process, as it becomes very difficult to correct mistakes retrospectively.”

Policy makers at national and municipal levels have an important role to play in ensuring that urbanization is sustainable and inclusive by ensuring that land and property rights are conducive for increasing economic density of cities. They will also have to improve mobility through better transport infrastructure and systems, as well as improve living conditions through better housing policies. Furthermore, it will be critical to improve access to social services such health and education; and levelling access to, and quality of, public services such as water and sanitation services.

Urbanization in Numbers

-

6.4 million Ugandans live in urban areas

-

70 percent of non-agricultural GDP in Uganda is generated in urban areas

-

54 percent of people living in Central region are residing in urban areas

-

Central region has the highest number of people living in urban areas, but, 38 percent of the urban population was connected to the electricity grid

-

The number of firms engaged in real estate and business services in Kampala is 11 times the overall average across districts

-

Over the first decade of the 2000s, cities accounted for 36 percent of overall job growth

-

Walking is the main mode of transport in Kampala, and 70 percent of the residents of Kampala walk to work

-

80 percent of the global economic activity is generated in cities

» The Growth Challenge: Can Ugandan Cities Get to Work? | Uganda Economic Update Factsheet

Related News

Swaziland: Budget Speech 2015/16

The Minister of Finance Senator Martin Dlamini has presented the 2015/16 National budget with emphasis on a strong and resilient economy, macroeconomic stability, private sector competitiveness, expanding trade and industry, agricultural modernisation and enhancing natural resource management. Extracts from the Budget Speech are included below.

This is the second budget of the 10th Parliament of the Kingdom of Swaziland. The budget is not just a collection of numbers as printed in the Budget Estimates Books, but also a reflection of the values and aspirations of the Government and the nation at large.

Milestones

Despite the various recent challenges including the loss of AGOA, the Kingdom has achieved significant milestones in its socio-economic transformation over the recent years. To highlight a few:-

i) Universal Primary Education now covers Grades 1 to 7, thus reaching the target we set ourselves in the Constitution;

ii) Anti-Retroviral Therapy take up has more than doubled since 2009, with about 105,000 people with HIV accessing free treatment;

iii) The proportion of Swazis with access to clean water has increased to 76 percent; and

iv) Our business and economic environment has generally improved, thanks to improved fiscal conditions and reforms, coupled with peace and security. This augurs well for our future economic growth prospects.

Challenges

The challenge going forward is to consolidate our past achievements and to ensure that we sustain this growth trajectory towards the desired social and economic transformation of the Kingdom. “Kungako sitsi lamaphakelo alonyaka, atawuba yincenye yesisekelo sentfutfuko yelive”.

This Budget is a continuation of our journey towards Vision 2022. To quote the Programme of Action, we aim for a Swaziland where ‘all citizens are able to sustainably pursue their life goals, and enjoy lives of value and dignity in a safe and secure environment.” The theme for the 2015/16 Budget is therefore “Achieving more with less spending: sustaining economic growth and protecting social development.”

The budget will focus on implementing priority development programmes over the next year and medium term, within a tightly constrained resource envelope. The main focus will be on education, health and agriculture; new roads; and measures to create the right conditions for private sector investment.

This Government believes that the Swazi nation can together build a future that is prosperous, just, and secure.

Economic performance and outlook

International developments

As a small open economy, the prosperity of Swaziland to a large degree is influenced by the strength of the global economy. At present, the world economy faces an uncertain future, and is still grappling with overcoming the effects of the recent global financial crisis. The world economy is expected to continue to grow modestly. According to the recent IMF’s World Economic Outlook, global economic growth was estimated at 3.3 percent in 2014, and stabilising at 3.7 percent over the medium term. This rate remains below the average recorded in the decade prior to the 2008 global crisis. On a positive note, the recent decline in international oil prices is good news for domestic inflation and trade prospects.

Regional developments

Projections indicate that the Sub-Sahara Africa’s economy will continue to grow. Growth is projected at 4.9 percent in 2015, rising to 5.2 percent in the medium term. We need to work harder to benefit from this strong regional growth.

South Africa is the destination for 63 percent of our exports. In 2014, the South African economy is projected to have grown by only 1.4 percent, against a target growth of 2.5 percent. Growth will be sluggish at 2.3 percent in 2015, increasing to 2.8 percent in the medium term. Their performance presents a significant challenge for our economy and reminds us of the need to diversify into other markets.

Domestic Developments

Real GDP Growth

On the domestic front, preliminary estimates indicate a slower pace of economic activity over the past year. Real GDP growth slowed down to 2.5 percent, in 2014 from an estimated growth rate of 3.0 percent in 2013. This slowdown has been largely due to a weak performance in mining and manufacturing sectors. The mining sector contracted by 23 percent in 2014, compared with growth of 19 percent in 2013. Falling commodity prices in the international market, and internal administrative issues were behind this weak performance. The manufacturing sector slowed down to 1.3 percent in 2014 from 1.9 percent the previous year. This stemmed from weakened performance in the textile industry, labour disputes and falling commodity prices in the sugar industry.

On the other hand, the 2.5 percent overall growth was supported by robust agricultural and construction sectors. Improved weather conditions and targeted interventions in the agricultural sector, under the LUSIP and food security programmes were the main drivers for growth in agriculture. The construction sector also remained buoyant, driven by major capital projects including the construction of roads, Information Technology and Biotechnology Parks, and the International Convention Centre and Hotel.

Over the medium term, the objective of Government as per the Programme of Action 2013-2018 is to attain real GDP growth of at least 5 percent per year. This is the minimum level of growth that could achieve the desired social economic transformation by 2022. Taking steps towards this goal will require continued implementation of economic reforms identified in the Investor Road Map.

Balance of Payments

Swaziland’s balance of payments continued to reflect strong performance in 2014 according to data for the first half of the year. The current account surplus more than doubled in the first half of 2014 compared with the year before. The current account surplus for the two quarters ending June 2014 stood at E1.2 billion. The trade surplus and high SACU receipts were the main factors contributing to the increase in the current account surplus.

22. Exports increased strongly, by 29 percent in the first two quarters of 2014 compared to the same period the previous year, whilst imports increased by a lower 13 percent over the same period. Our strong performance stems from the depreciating exchange rate during 2014, and is an encouraging sign of economic vitality.

Budget Strategy for 2015/16

His Majesty the King in His Speech from the Throne this year, counselled to ‘save for rainy days during good years’. Given our difficult fiscal circumstances, these are our priorities for Budget 2015/16:

i) A strong and resilient economy, with a particular focus on macroeconomic stability, private sector competitiveness, expanding trade and industry, agricultural modernisation and enhancing natural resource management;

ii) Enhancing human capital, with increased focus around access and quality of healthcare and education, and enhancing the welfare of the vulnerable;

iii) Enhancing service delivery, through improving institutional governance, transparency and accountability;

iv) Strategic infrastructure rehabilitation and expansion, focusing on roads, railway, aviation, water and sanitation, tourism and rural development.

This budget strategy is aimed at sustaining economic growth, employment and poverty reduction. The strategy also ensures that Government facilitates the private sector as directed by His Majesty the King in His Speech from the Throne, by implementing measures that improve efficiency and lower the cost of doing business.

Revenue and Expenditure for 2015/16

Revenue and grants

Total revenue including grants for 2015/16 is estimated at E14.6 billion compared with an estimated E14.8 billion in 2014/15. In GDP terms, this is a drop of three percentage points. SACU receipts have fallen from E7.4 billion in 2014/15 to E6.9 billion in 2015/16, a reduction of around E560 million. SACU receipts are again expected to decline further in 2016/17, as Swaziland will be required to effect a sizeable repayment during 2016/17, as indicated by the SACU Secretariat. External grants will amount to E270 million, a reduction from last year, as one-off European Union grants for agricultural developments fall.

Expenditure

Expenditure is estimated at E15.9 billion, including payments for public debt and other statutory obligations, which amount to E1.0 billion. Total expenditure for 2015/16 thus represents an additional E646 million above the appropriated level for 2014/15. The estimated budget deficit, of E1.3 billion, will be financed by a mixture of external loans to projects, of around E450 million net, and additional domestic borrowing of around E1 billion. This is a sustainable budget in difficult circumstances. A variety of revenue and expenditure measures have led us to a responsible budget for 2015/16, that prepares us for a difficult year in 2016/17.

Revenue Measures

Government is proposing various revenue measures. These will assist Government in mobilizing additional resources for protecting essential services, while SACU revenues fall in the medium term.

These initiatives include an amendment of the Income Tax regulations, including removal of the tax allowance exempting gains on the disposal of business assets. However, the amendments would also reduce taxation on medical aid for the private sector.

Other initiatives intended by the Income Tax Order include the introduction of taxation of residents on their worldwide income. Currently, residents are taxed depending on source, meaning that tax is imposed on income generated within Swaziland only. This has a limitation in that there is a growing trend of Swazi residents (including individuals and companies) earning income beyond our borders. Increasing tax justice is an idea whose time has come. Our neighbours, including South Africa, have already shifted from source-based taxation to world-wide taxation.

The VAT Refund Agreement between Swaziland and South Africa is ready. From the 1st of April 2015, residents simply declare the VAT of their purchases at any of our border posts, and Government receives the revenue from South Africa. This replaces the current arrangement where declaring residents are charged twice, and must retrieve refunds from South Africa, often months later. The projected additional revenue from increased declarations is over E120 million per year. I would urge all Swazis to declare their purchases, so that vital funding for Government services can be secured.

Furthermore, Government plans to review the Customs and Excise Act; and accommodate a number of modernization initiatives aimed at enhancing revenue collection and improving our Doing Business rank. I am pleased to observe that the SRA is introducing the accreditation of preferred traders. SRA will reward those taxpayers who have a proven record of tax compliance, by issuing certificates of accreditation which grants faster treatment at our borders. Lessening delays in the declaration, clearance and release of goods, and the ability to prepay, will reduce the cost of doing business in Swaziland. Upgraded trade software, which allows electronic signature and documentation, will reduce barriers to trade.

Appropriation

This budget concerns “Achieving more with less spending: sustaining economic growth and protecting social development.”

By virtue of the responsibility entrusted to me as Minister of Finance, I now present to this Honourable House, the Budget Estimates for financial year 2015/16, as follows:

-

Revenue plus grants: E14,606 million;

-

Appropriated recurrent expenditure (excludes Statutory): E11,737 million;

-

Capital expenditure: E3,217 million;

-

Total expenditure: E15,952 million; and

-

Deficit: E1,346 million.

Conclusion

There is a higher ambition than merely to stand superior in the world. It is to step down, and lift mankind a little higher than where they are. This Budget is a tough Budget. However, it has tried to focus our meagre resources towards those areas that will lift up Swazis a little higher than where they are currently.

Related News

U.S. and East African Community join to increase trade competitiveness and deepen economic ties

Obama Administration to Expand Trade Africa Initiative

U.S. Trade Representative Michael Froman and trade ministers from the East African Community (EAC) marked a milestone for Trade Africa on 25 February 2015; signing a Cooperation Agreement that will increase trade-related capacity in the region and deepen the economic ties between the United States and the EAC.

During the ceremony, Ambassador Froman announced that the United States will begin looking to expand Trade Africa beyond the EAC (Burundi, Kenya, Rwanda, Tanzania, and Uganda).

“Today’s agreement builds on our progress. It’s an important milestone for deepening what has already proven itself to be a promising and impactful partnership,” said Ambassador Michael Froman. “By tackling tasks in important areas, this agreement will help us lift the burdens that trade barriers impose, unlocking opportunity on both our continents.”

The Cooperation Agreement will build capacity in three key areas: Trade Facilitation, Sanitary and Phytosanitary (SPS) Measures, and Technical Barriers to Trade (TBT). Implementing critical customs reforms, harmonizing standards, and undertaking multilateral commitments will support greater EAC regional economic integration and strengthen its trade relationship with the United States and other global partners.

The Trade Africa initiative was announced by President Obama during a visit to Africa in 2013, aimed at supporting greater U.S.-Africa trade and investment, beginning initially with the EAC.

Trade Africa has contributed to a number of successes in the region – notably, improvements at the ports of Mombasa and Dar es Salaam, construction of one-stop border posts in East Africa, and more effectively linking the U.S. and EAC private sectors under the U.S.-EAC Commercial Dialogue.

The Obama Administration is now looking to expand Trade Africa beyond the EAC, laying the foundation for a more mature and comprehensive 21st century U.S.-Africa trade and investment relationship over the medium to long term.

“We see this agreement and all our work with the EAC to date as an important steppingstone, not the final destination,” Ambassador Froman added. “The global economy is evolving and the U.S.-Africa economic relationship must evolve, too. Together, we can tackle more tasks, support more jobs, and unlock more opportunities for the American and African people alike.”

The Office of the USTR has also worked closely with the Commerce Department to ensure a strong and vibrant private sector voice to expanded U.S.-African trade. Following the morning session, the Commerce Department will host the first U.S.-East Africa Commercial Dialogue, which will develop joint public-private sector initiatives to boost our trade and investment in the region by focusing on issues such as through customs modernization, electronic payments, cold chain development and access to capital, among others.

During a series of meetings following this signing, the U.S. and the EAC governments, private sector, and other stakeholders also discussed the strategic way forward for the U.S.-EAC trade and investment relationship, including the need for a seamless renewal of AGOA; discussed a regional strategy to help the EAC countries to take better advantage of AGOA; and held the inaugural meeting of the U.S.-EAC Commercial Dialogue with the U.S. and EAC private sectors.

The United States is committed to using all the tools at its disposal to help support greater African regional economic integration and U.S.-African trade and investment to help create jobs and opportunities for the American and African people alike.

» Click here to view a fact sheet on the U.S.-EAC Cooperation Agreement

Related News

Nigeria is Africa’s leading ecommerce market

Online shopping in Africa has blossomed in recent times, riding on the back of improved broadband access. Nigeria, Africa’s largest economy, is leading the way in e-commerce growth, with 65 percent of the country’s 50 million internet users having at one time or the other shopped online.

This is according to a recent study conducted in Nigeria by Ipsos, a global market research company, on behalf of PayPal. Those who have not shopped online, making up 24 percent of the country’s total internet users expect to do so in the future.

The results of the study confirm Nigeria as Africa’s leading e-commerce nation in the amount of potential and existing online shoppers, which is at 89 percent, compared to South Africa’s 70 percent and Kenya’s 60 percent.

Drivers of Growth

There are several key drivers that would encourage even more e-commerce in Nigeria. Out of the 500 adults involved in the survey, 53 percent of those who have shopped online in the past said faster delivery of goods would encourage them to shop online more often. 40 percent indicated that safer ways to pay was a key driver while 31 percent indicated lower product costs as a driver to do more shopping online.

Although Nigerian shoppers have identified reasons to increase online shopping patronage, some concerns have been raised. These concerns are major impediments to increasing the number of people who shop online in Nigeria.

Security of Online Payment and Delivery Costs

The research shows that security of online payments and delivery costs are among main concerns preventing consumers from conducting more online shopping. 31 percent of those who have not shopped online give concerns about security of payments as a reason for not currently shopping online, and 27 percent say that the cost of delivery is a reason for not currently shopping online. However, the cash on delivery option provided the much-needed alternative to putting account details online.

Fear over security of online payments means that cash on delivery is still the most used and preferred payment method when shopping online. The study sponsored by Paypal noted that 39 percent of online shoppers use cash. 32 percent also described cash payment as a preferred payment method for online purchases.

“Online security matters. This is why PayPal provides a simpler, easier and more secure way to shop and pay on millions of websites around the world,” says Efi Dahan, Regional Director for Africa and Israel at PayPal. “The fact that PayPal does not share financial information with the seller when authorizing a transaction keeps the consumers’ financial details more secure”.

Although PayPal has been present in Nigeria for up to a year, consumers who already know the payment service agree PayPal is a fast (85 percent), convenient (83 percent) and safe (73 percent) way to pay online. 72 percent of online shoppers aware of PayPal agree that it is the safest online payment method.

Popularity of Mobile Online Shopping

According to the research, another driver of online shopping in Nigeria is increased mobile penetration. The results show the overwhelming usage of mobile phones to shop online. 90 percent of online shoppers that own a smartphone or a feature phone have used it to shop online while 51 percent use their device to shop online once a month or more.

Shopping on mobile browsers seems to be the most popular way to do mobile shopping with 43 percent of Nigerian mobile shoppers stating a preference to shop using the phone’s browser, compared to 34 percent who prefer to shop from an app.

However, some barriers remain for mobile shopping. Security of payments was flagged as a concern to Nigerians with 30 percent of mobile shoppers saying security of online purchases from a mobile device is a reason for not shopping online using a mobile phone more often, while 30 percent also flagged concerns about internet usage costs on mobile as a barrier to mobile shopping.

What Nigerians Buy Online

Nearly half (47 percent) of online shoppers in Nigeria purchased digital goods in the past year, followed by 39 percent that purchased adult clothing, footwear & accessories online, and 33 percent that purchased physical entertainment such as books and CDs online. The research also found that one in every four Nigerian online shoppers purchased consumer electronics online in the past year. 40 percent – 69 percent of online shoppers have indicated they expect to spend the same or more on the following categories next year: digital goods (62 percent), adult clothing footwear & accessories(69 percent), physical entertainment (60 percent), jewelry and watches (53 percent), consumer electronics (54 percent) and children clothing (40 percent).

A Regional Perspective

The study also considered how often Nigerians purchase goods online from other countries on the continent. The results showed that intra-African trade is significant with 36 percent of Nigerian cross-border shoppers buying from elsewhere in Africa in the past 12 months. South Africa is the main destination with 30 percent of Nigerian cross-border shoppers buying from the country in the past 12 months. It is followed by Kenya with 2 percent, Egypt with 1 percent, and the rest of the continent with 3 percent.

Related News

South African trade gap widens to record as mining exports fall

South Africa’s trade deficit widened to the largest since at least 2010 in January as gold and platinum exports fell and oil imports increased.

The trade gap of 24.2 billion rand ($2.1 billion) compared with a revised surplus of 6.7 billion rand in December, the Pretoria-based Revenue Service said in an e-mailed statement on Friday. The median estimate of 16 economists surveyed by Bloomberg was for a deficit of 7.8 billion rand.

The volume of oil imports rose 64 percent in January as the price dropped to an almost six-year low and importers such as Eskom Holdings SOC Ltd. stepped up their purchases. The utility is burning increased amounts of diesel as it struggles to meet demand in the continent’s most industrialized economy.

“The impact of sharply lower global commodity prices is being reflected in the data,” Manisha Morar, an economist at ETM Analytics, said by phone from Johannesburg on Friday. Subdued global demand and domestic electricity shortages “are likely to offset the potential benefit of lower oil prices on the import bill.”

A widening trade deficit has added to pressure on the current account, the broadest measure of trade in goods and services, and the rand. The current-account gap probably averaged 5.8 percent of gross domestic product in 2014 and will narrow to 4.5 percent this year, according to the National Treasury.

Rand Weakens

The rand weakened 0.8 percent to 11.6289 per dollar as of 2:36 p.m. in Johannesburg, bringing its decline since the start of last year to 9.8 percent. Yields on government rand bonds due December 2026 rose eight basis points to 7.65 percent.

Large external deficits “in the form of the current-account and trade balance will ensure that a level of vulnerability remains entrenched in the rand,” Morar said.

Exports dropped by 23.1 percent to 67.1 billion rand in January as shipments of precious metals and stones fell by 5.2 billion rand, or 35 percent. Exports of mineral products, which include coal and iron ore, declined by 4.4 billion rand, or 19 percent. Vehicle and transport equipment shipments were 2.4 billion rand, or 27 percent, lower.

Imports rose by 13.3 percent to 91.3 billion rand as purchases of machinery and electronics increased by 2 billion rand, or 10.2 percent. Purchases of equipment components rose 1.9 billion rand, or 45 percent, and mineral products, which include oil, were 1.1 billion rand, or 6.2 percent, higher.

The monthly trade figures are often volatile, reflecting the timing of shipments of commodities such as oil and diamonds.

The revenue service revised its data in November 2013 to include trade with Botswana, Lesotho, Namibia and Swaziland.

SA Trade Statistics for January 2015 (SARS): Highlights

The R24.22 billion deficit for January 2015 is due to exports of R67.08 billion and imports of R91.30 billion. Exports decreased from December 2014 to January 2015 by R20.19 billion (23.1%) and imports increased from December 2014 to January 2015 by R10.70 billion (13.3%).

The trade data excluding BLNS for January 2015 recorded a trade deficit of R31.33 billion. This is a result of exports of R57.72 billion and imports of R89.04 billion. Exports decreased from December 2014 to January 2015 by R19.81 billion (25.5%) and imports increased from December 2014 to January 2015 by R10.67 billion (13.6%).

Trade statistics with the BLNS for January 2015 recorded a trade surplus of R7.11 billion. This is a result of exports of R9.36 billion and imports of R2.25 billion. Exports decreased from December 2014 to January 2015 by R0.38 billion (3.9%) and imports increased from December to January by R0.02 billion (0.9%).

Trade highlights by category

The month-on-month export movements:

| R’ million | ||

|

Section:

|

Including BLNS:

|

|

|

Precious Metals & Stones

|

- R5 228

|

- 35.4%

|

|

Mineral Products

|

- R4 401

|

- 19.4%

|

|

Vehicle & Transport Equipment

|

- R2 349

|

- 27.3%

|

|

Machinery & Electronics

|

- R2 090

|

- 25.0%

|

|

Base Metals

|

- R1 462

|

- 13.5%

|

The month-on-month import movements:

|

R’ million

|

|

|

|

Section:

|

Including BLNS:

|

|

|

Machinery & Electronics

|

+ R2 005

|

+ 10.2%

|

|

Equipment Components

|

+ R1 896

|

+ 44.7%

|

|

Base Metals

|

+ R1 523

|

+ 40.6%

|

|

Vehicle & Transport Equipment

|

+ R1 288

|

+ 14.8%

|

|

Mineral Products

|

+ R1 093

|

+ 6.2%

|

Trade highlights by world zone

The world zone results for January 2015 are given below.

Africa:

Exports: R20 018 million – this is a decrease of R3 614 million from December 2014

Imports: R12 029 million – this is an increase of R1 978 million from December 2014

Trade surplus: R7 989 million.

This is a 41.2% decrease in comparison to the R13 581 million surplus recorded in December 2014.

America:

Exports: R6 594 million – this is a decrease of R2 527 million from December 2014

Imports: R9 831 million – this is an increase of R1 521 million from December 2014

Trade deficit: R3 237 million

This is a comparison to the R 811 million surplus recorded in December 2014

Asia:

Exports: R20 236 million – this is a decrease of R8 146 million from December 2014

Imports: R41 439 million – this is an increase of R4 026 million from December 2014

Trade deficit: R21 203 million

This is a 134.8% increase in comparison to the R9 031 million deficit recorded in December 2014

Europe:

Exports: R16 262 million – this is a decrease of R3 055 million from December 2014

Imports: R26 493 million – this is an increase of R2 881 million from December 2014

Trade deficit: R10 231 million

This is a 138.2% increase in comparison to the R4 295 million deficit recorded in December 2014

Oceania:

Exports: R 877 million – this is a decrease of R 433 million from December 2014

Imports: R1 356 million – this is an increase of R 175 million from December 2014

Trade deficit: R 479 million

This is a comparison to the R 129 million surplus recorded in December 2014

For further information, visit the SARS website.

Related News

Greater collaboration needed for air cargo to unlock intra-African trade potential

African airlines have called for greater intra-regional trade, better connectivity and more carrier cooperation if they are to take advantage of the continent’s potential, delegates heard yesterday [25 February 2015] at Air Cargo Africa in Johannesburg.

Africa is “the last frontier of globalisation” and its potential is huge – but many of its problems must be resolved by its own governments and companies, while trade opportunities need to be opened up, they argued.

Fitsum Abady, managing director of Ethiopian Cargo Services, listed a diverse array of challenges that the continent faced, including trade imbalance, lack of infrastructure and integrated multilmodal solutions, high operational charges, bureaucracy, inefficiency and corruption – as well as the more recent ebola outbreak and terrorism.

But one of the keys to growth, Mr Abady noted, was that there was very little intra-African trade and collaboration.

“The co-operation between carriers is still not there; there is no codesharing, no interlining. That could help contribute to air cargo growth.”

His words echoed rival operator South African Airways acting CEO Nico Bezuidenhout, who had said: “African countries don’t trade sufficiently with each other – a huge opportunity, going forward.”

World Bank figures show that intra-Africa accounts for just 10-12% of total trade, compared with 40% of the total emanating from regional trade in North America and 60% in Europe.

Mr Bezuidenhout added: “African countries have to open up. We are quick to offer open skies to others, but there is very limited co-operation between African carriers.”

One source, on the sidelines of the event, believed this was as a result of government-owned airlines in monopolistic positions failing to see the advantages of closer co-operation, opting for rivalry instead of seeing an opportunity to grow the market together.

The eight-strong opening panel – from just two African companies – agreed that despite the many challenges, there was huge opportunity for growth.

A second panel, on Africa, called for greater collaboration between Customs to facilitate regional trade.

Sanjeev Gadhia, CEO of regional carrier Astral Aviation, said that while intra-African trade was the fastest-growing sector in the market, at about 15%, “the stumbling block in Africa is Customs. I’d like to see us all working towards a common goal.”

Ivin George, vp air freight for sub-Saharan Africa, at DHL Global Forwarding added: “The amount of bureaucracy at border posts is amazing, and that’s where we lose efficiency. If it all goes well, it takes 12 days to get from Johannesburg to Luanda becuase of the amount of documentation.”

With mobile connectivity in sub-Saharan Africa set to reach 930 million people by 2013 – a change which leads to a direct economic impact of 0.8% growth in GDP in developing countries – e-commerce was likely to be another significant growth area.

“African consumers don’t have the luxury of ordering something on the internet and receiving it next day,” said Mr Gadhia. “There is a gap in the market where the integrators have not offered that service. There is high demand – but it takes a long time for products to reach the consumer.”

Growth beyond the continent, interestingly, is not framed as many might have predicted.

“We are seeing growth of Asian-African trade, rather than the traditional north-south,” said Barry Nassberg, COO of Worldwide Flight Services, which has expanded its operation in Africa significantly in the past couple of years. “Because of the investment by Asian countries, especially China, some of the growth is staggering. We do see it changing.”

Mr Bezuidenhout also pointed out that it was taking time for African countries to establish their trades. “There is a slow change to the make-up of the economies. Countries will start to specialise: South Africa, for example, is strong on motor manufacturing and that has been a natural progression. It will all have an impact.”

While economies may be continuing to develop, investment remained challenging.

“Africa represents about 8% of our tonnage, but in the past five to six years it has been about 80% of our investment,” said Nils Pries Knudsen, head of global cargo at Swissport. “We want to improve infrastructure but there needs to be a payback. We would like to carry on but we have to be selective.”

Mr Nassberg added: “We are at very early stages, in terms of what the market is demanding in infrastructure. Shippers are looking for a world standard, but the ability to meet those needs goes hand in hand with the opening of those markets.”

Operating costs in Africa are also very high, noted delegates. Jet fuel prices, for example, currently average twice the global price, said Mr Abady. “Africa is not benefiting from the the fuel price plunge,” he said.

But, he added, “so many landlocked countries, and the growth of the middle class, means air cargo will be a driving force for development.”

Related News

Trans Kalahari Project still on hold

Minister of Infrastructure Science and Technology, Nonofo Molefhi says the commencement of the Trans Kalahari Railway (TKR) project is on hold pending sourcing of funds.

The 1447-kilometre railway line will link Botswana’s Mmamabula coalfields with the Walvis Bay Port in Namibia.

Briefing Parliament on Tuesday, Molefhi said he was uncertain when work on the project would start, as they had not found private investors to assist them spearhead the development, adding that the project was too costly for both governments.

The project is expected to cost P136 billion.

Molefhi said the two governments had agreed to conduct feasibility studies first and only then, engage the private sector. Botswana and Namibia signed a Memorandum of Understanding on the Trans Kalahari Railway project in 2010.

The pre-feasibility studies for the project were completed in 2011 with the bilateral agreement signed in March 2014.

Molefhi explained that the project management office, which was planned to open in January this year, was not yet open since it is still undergoing refurbishment. “A consultant has completed a study which will be critical in informing the governments on how to go forward with the Trans Kalahari Railway project,” he said.

The TKR will avail a viable evacuation route for coal miners in Botswana to export their produce to international markets.

Once completed, the railway line will also afford alternate transportation routes for landlocked SADC countries such as Malawi, Zambia and Zimbabwe. It will be ideal for exportation of bulky goods destined for Europe, Asia and America while also serving as relief to the already congested corridors within SADC.

In Botswana, the TKR route alignment will follow the existing Trans Kalahari Corridor starting from the central district in Botswana, where there are coal fields and connect to the existing railway line alignment down to Rasesa passing through Molepolole-Kang road until Morwamosu to join Trans Kalahari Corridor through to Mamuno border.

Botswana can currently export as much as 1.7 million tonnes per annum to international markets using existing railways through Mozambique. Experts have, however, said the slow pace of infrastructure development might cause Botswana to lose market opportunities. The existing rail links between Botswana and Maputo offer available capacity of 20 million tonnes per annum.

The proposed new routes to Walvis Bay and Ponto-Techobanine are yet to demonstrate commercial viability, but offer potential long-term solutions for more than 100 million tonnes per annum.

Related News

SADC completes industrial strategy interim report

SADC member states have completed an interim report outlining the regional industrialisation strategy expected to prioritise value addition and beneficiation.

The interim report, prepared by experts, was presented to the SADC Ministerial Taskforce on Regional Economic Integration which is holding a series of meetings in Harare to reflect on progress and give guidance to expedite the development of regional industrial strategy. This is in preparation for the Extra ordinary Summit to be held in April to discuss the matter.

In August last year, SADC Summit mandated the Ministerial Taskforce on Regional Economic Integration to come up with a strategy and roadmap for industrialisation. This was after a realisation that industrialisation strategy cannot be over emphasised given the challenges facing the region.

President Mugabe, who took over as SADC chairman last year told journalist at the end of the summit that it was critical for the region to prioritise value addition and beneficiation ahead of market liberalisation.

He said collective industrialisation would help the region to derive higher value from its resources. “Some of the elements that members states have been highlighting as key for regional industrialisation is development and participation in regional value chains,” Industry and Commerce Permanent Secretary Abigail Shonhiwa said yesterday. “It is therefore important that national processes should take place so that member states will be able to take advantage and benefit from industrialisation strategy.”

Mrs Shonhiwa said the taskforce agreed that the strategy should put forward concrete proposals on how to “frontload” industrialisation and properly sequence targets outputs on industrialisation development against those on markets integration.

Earlier, Industry and Commerce Minister Mike Bimha told delegates that trade among SADC member states had grown much slower as compared with that of other parties. “This could be a reflection of the fact that most member states lack capacity to beneficiate and value add their raw materials,” he said.

“Therefore, we are forced to import finished products from outside the region. During our tenure of office as chairperson of SADC, and in line with the theme of the 34th SADC Summit, it is our intention to work with fellow member states and put in place mechanisms meant to leverage on the abundant diverse human, mineral and agriculture resource in the region.”

The theme for last year’s summit was “SADC Strategy for Economic Transformation: Leveraging the Region’s Diverse Resources for Sustainable Economic and Social Development”.

The proposed regional industrialisation strategy, which places emphasis on value addition and beneficiation also dovetails into the Zimbabwe Agenda for Sustainable Socio Economic Transformation’s “value addition and beneficiation cluster”.

Visit the SADC Resources page for additional legal and policy documents.

Related News

SME finance in Ethiopia: addressing the missing middle challenge

The private sector is expected to play a key role in Ethiopia’s journey to become a middle income country in the next decade. However, Ethiopian firms face significant financial constraints, because financial institutions do not accommodate their needs, a new World Bank Group (WBG) study found.

The report reveals that without adequate support from financial institutions, small and medium businesses are not able to grow, or create more job opportunities.

The study used both supply and demand research to offer a complete picture of small and medium enterprises’ finance practices in Ethiopia. While there was already anecdotal evidence that small firms were lacking suitable access to finance, the study was able to provide empirical evidence of the existence of a “missing middle phenomenon.” The study also offers recommendations to help reduce financial challenges and promote the growth of small and medium enterprises.

This gives origin to the so-called missing middle phenomenon whereby small enterprises are more credit constrained than either micro or medium/large enterprises,” said Francesco Strobbe, WBG senior financial economist.

The study used both supply and demand research to offer a complete picture of small and medium enterprises’ finance practices in Ethiopia. While there was already anecdotal evidence that small firms were lacking suitable access to finance, the study was able to provide empirical evidence of the existence of a “missing middle phenomenon.” The study also offers recommendations to help reduce financial challenges and promote the growth of small and medium enterprises (SMEs). Those recommendations were discussed after the launch of the study during a two-day forum with high-level policy makers and stakeholders. The forum also enabled participants to learn from global best practices from Turkey, Nigeria and Ghana, which were able to successfully implement financing activities for SMEs.

The WBG supports the Ethiopian government’s efforts to create jobs through analytical studies and investment operations. The Ethiopian government has prepared a private sector development strategy to improve the productivity and modernization of the agricultural sector, and boost the technological sophistication and economic input of the industrial sector. It has also identified, the development of micro, small and medium enterprises (MSMEs) as a key industrial policy direction for creating employment opportunities for millions of Ethiopians. However, all this is not sufficient and much more remains to be done to unleash the full potential of SMEs, said Guang Zhe Chen, WBG country director for Ethiopia.

“To help fill in some of the gap through microfinance institutions, the World Bank Group, in cooperation with DFID and CIDA is supporting the Women Entrepreneurship Development Project,” Chen said. “In addition, through the $250 million Competitiveness and Job Creation Project, the WBG is also helping to create dedicated industrial zones.”

The government’s second Growth and Transformation Plan (GTPII), currently under preparation, will place even more emphasis on the importance of private sector development and therefore on easing access to finance for SMEs. The government has put in place helpful public support programs but much more is needed to properly address the missing middle challenge.

“By increasing the capacity of the financial sector to properly serve the segment of small enterprises with adequate financial products, we hope to address lack of access to finance which is a key obstacle that is currently preventing small enterprises from fully playing their role in the industrialization process of Ethiopia and in contributing to the job creation agenda as envisaged in the GTP I and GTP II,” said H.E Ato Desalegn, state minister of Urban Development Housing and Construction.

Taking into consideration the findings and recommendations of the study, the WBG will help support the government in designing new initiatives to better serve the financial needs of SMEs and create an “SME finance culture.” These interventions will complement the positive results of ongoing operations such as the Women’s Entrepreneurship Development Project and the Competitiveness and Job Creation Project by linking SMEs with larger enterprises in the industrial zones and contributing to the creation of a “private sector ecosystem” around the industrial zones.

“The SME finance study contains important policy recommendations that will need to be taken into account in the design of a new SME Finance project,” Desalegn added. “I’m confident that the inputs will help promote an SME finance culture in Ethiopia that will greatly contribute to the industrial policy objectives of the GTP and ultimately to the well-being of our country.”

Related News

Trade in Environmental Goods and Services: Issues and Interests for Small States

Increased trade in environmental goods and services (EGS) is a global climate change mitigation strategy. This is because use of these goods can result in more environmentally friendly outcomes compared to alternatives. Hence, reducing their costs, including through tariff reductions, can incentivise their use over conventional alternatives therefore improving global environmental outcomes.

Efforts to conclude on a list of EGS at different levels, multilateral as well as regional, have been underway for some time, but lately have received a renewed impetus. Since the Doha round of multilateral negotiations under the World Trade Organization (WTO) stalled, plurilateral negotiations have commenced between likeminded countries under the Environmental Goods Agreement (EGA). Regional efforts among members of Asia-Pacific Economic Cooperation (APEC) to liberalise EGS have also accelerated. Negotiations for a new global climate change framework to be agreed under the auspices of the United Nations Framework Convention on Climate Change (UNFCCC) are ramping up in time for the next decisive round of negotiations for a new international climate change agreement to be held in Paris in December 2015. Although the liberalisation agenda of EGS negotiated under the auspices of the WTO is not directly related to the UNFCCC process, an agreement by members could provide an important signal of intent towards the mitigation of global climate change.

This issue of Commonwealth Trade Hot Topics takes stock of negotiations for the liberalisation of environmental goods and services, and outlines the major issues for consideration by Commonwealth small states (CSS). The methodological approach undertaken here confirms the relevance of the list approach for CCS, and based on this assessment potential negotiation approaches have been identified. The paper is concluded with discussion as to the potential synergies between the trade and climate change regimes that could be sought within a liberalisation agenda, which promotes the mitigation of climate change and global public environmental goods.

Related News

South Africa gives Brics port of entry visas

Business and diplomatic travellers from South Africa's Brics partners will receive port of entry visas into the country, Home Affairs Minister Malusi Gigaba said on Thursday.

"I have approved the issuance of port of entry visas to Brics business executives for up to 10 years, with each visit not to exceed 30 days," he told the Cape Town Press Club. The visas had been in effect since December 23 last year.

"This applies to diplomatic, official/service, and ordinary passport holders." Gigaba said the relevant individuals would receive a long-term visa allowing them multiple entry into the country for the duration of the passport's validity, not exceeding ten years. The department would continue to meet a turnaround time of five days for short-term business visas. It had consulted extensively with the Brazil, Russia, India, China, and South Africa (Brics) business council and the trade and industry department.

Gigaba said the four countries presented an "important investment potential". Together with South Africa, they comprised 40% of the world's population. "Business people from Brazil, Russia, India, and China want to come to our country, buy and sell an increasing array of products and services, and invest in our companies and growth sectors," he said.

"At home affairs we are completely committed to enabling this by facilitating the efficient entry of these commercial visitors, and will continually look for opportunities to improve in this regard." The department had not demanded reciprocal arrangements from Brics partners.

Gigaba smiled when asked if his announcement would anger countries that had long-established trading relationships with South Africa. "No, every good thing must start somewhere," he said. The arrangement may well be extended to other countries which had "significant investments" locally.

"These are issues that you undertake as you improve your systems." He said a "trusted traveller system" would be available to business people outside Brics. Leisure travellers could extend their visa while in the country, but needed to return home if required to apply for a new visa.

These new regulations had been introduced to counter a "complete abuse" of the local immigration system, which had seen people apply for jobs while on a tourist visa to avoid police clearance and issues with financial statements.

Gigaba said he would soon announce a panel of experts to conduct a complete review of the system used to issue visas.

Related News

Congo Eyes Stake in Uganda's Crude Export Pipeline

Congo wants to participate in the development of the proposed crude oil export pipeline on the Ugandan side of the Lake Albertine rift basin, Uganda's energy and minerals minister said Wednesday, as the project continues to entice more upcoming oil producers in the region.

Discussions are ongoing between Uganda and Congo about Kinshasa's potential investment in the project, which could cost up $4.5 billion, Irene Muloni told The Wall Street Journal in an interview.

Lambert Mende, Congo's information minister, confirmed the development, which underscores a potential thaw in the relations of the two neighboring nations who have bickered for years over the ownership of oil fields that straddle their poorly marked common border. Congo becomes the latest nation after South Sudan, Rwanda and Kenya to show interest in the project, which is expected to link the recently discovered vast oil reserves to international markets through the Kenyan port of Lamu.

"We are welcoming more partners, we want an optimum utilization of the pipeline," Ms. Muloni said. Uganda has confirmed some 6.5 billion barrels of crude reserves in the Lake Albertine Rift basin. The Congolese side could potentially have as much as 3 billion barrels of crude, according to Fleurette Group, which owns two blocks in Congo. Total SA (TOT), which has operations in Uganda, also has interests in one of the blocks on the Congolese side.

Japan's Toyota Tsusho is currently carrying out a feasibility study and initial designs for the 1,300 kilometer pipeline. The pipeline to Lamu will run through Lokichar basin in northwest Kenya, where the U.K.'s Tullow Oil PLC (TLW.LN) has discovered about 600 million barrels of crude. The pipeline will also provide an alternative export route for South Sudan's crude. Currently, Juba relies on a pipeline through its northern neighbor and former war foe Sudan. Rows between the two have disrupted crude exports.

According to Ms. Muloni, Ugandan projects will come on stream by 2018, "most likely when global crude prices have recovered from the current slump."

Related News

Southern African Utilities Develop Efficient Lighting, Appliances and Equipment Roadmap

Fifty participants from the public and private sector participated in the workshop SADC Regional Action Plan for Leapfrogging to Efficient Lighting, Appliances and Equipment. The workshop was jointly organized by the UN Environment Programme (UNEP), the Department of Energy of South Africa (DoE) and the Southern African Power Pool (SAPP).

According to UNEP, by switching to efficient products, Southern Africa could reduce its electricity consumption by more than 35 TWh and save 5,000 MW in power capacity, which could serve to electrify 16 million homes in the region. Under the leadership of the SAPP, the Southern African utilities have developed a roadmap to achieve a permanent and sustainable transition to efficient lighting, appliances and equipment in the Southern African Development Community (SADC). A number of priority actions have been identified, which, once implemented, will generate significant climate, environmental and economic benefits for the region.

Workshop participants included representatives of SAPP's Secretariat and its member utilities, members of governments and regulatory bodies from Southern Africa, national and regional key stakeholders working on appliance and equipment efficiency, and international actors such as the UN Development Programme (UNDP), the International Copper Association (ICA), and representatives of leading lighting, appliances and equipment manufacturers, including Philips, Osram, ABB and Arçelik.

In her opening speech, Cecilia Kinuthia, UNEP's Head of Sub-regional office, emphasized the need to move towards efficient lighting, appliances and equipment. She highlighted the coordinated approach Southern African utilities have been taking to energy efficiency as a means to address the extremely constrained and vulnerable power systems causing frequent black-outs and slowing down economic activity. She argued that leapfrogging SADC to efficient products will help the region to address its power crisis and contribute to its electricity saving goals at low cost, while generating significant climate and environmental benefits.

According to preliminary estimates by UNEP, leapfrogging to efficient lighting, refrigerators, room air conditioners and distribution transformers will reduce SADC's current electricity consumption by 35 Terra Watt hours and free 5,000 Megawatt of power capacity. This would allow for the electrification of 16 million households in the region and reduce its CO2 emissions by 20 million tons per year in 2030.

The proposed regional roadmap builds on the Integrated Policy Approach developed under the UNEP-GEF (Global Environment Facility) en.lighten initiative that is being successfully implemented in over 30 countries worldwide. Lighting, refrigerators, air conditioners, water heaters and distribution transformers have been identified as the priority products for SADC as they offer the most cost-effective and fastest way to save energy in the region.

Workshop participants requested UNEP and UNDP to provide support to the implementation of the roadmap by assisting the region in catalyzing technical and financial resources. Participants also encouraged all SADC countries to engage and share leadership in this initiative through their Ministries of Energy and Environment, and to identify sources of finance. They adopted a communiqué that will be submitted to the Ministries of Environment and the Ministries of Energy of SADC, inviting them to endorse the roadmap.

This initiative is part of the Global Partnership on Appliances and Equipment, a global effort led by UNEP with the support of the Global Environment Facility (GEF), to leapfrog global markets to high efficiency and affordable products, as a means to curb greenhouse gas emissions and combat climate change. Along with its international partners, including UNDP, ICA, CLASP, the Natural Resources Defense Council (NRDC) and various key players from private sector, this public-private partnership is a contribution to the Sustainable Energy for All (SE4ALL) initiative of UN Secretary-General Ban Ki-moon.

The workshop SADC Regional Action Plan for Leapfrogging to Efficient Lighting, Appliances and Equipment was held on 19-20 February 2015, in Johannesburg at the premises of the South African utility Eskom.

Related News

Uganda: Government wins Heritage Oil case

Uganda Revenue Authority (URA) will not have to reimburse about Shs1.1 trillion to Heritage Oil after United Nations Commission on International Trade Law (UNCITRAL) ruled in its favour in a London court on Tuesday.

The legal battle between Uganda and Heritage Oil Tax which emerged after the latter sold its stake to Tullow has been going on since 2011. Should the case have gone the oil company’s way, it would mean that URA would have had to surrender Shs1.2 trillion it collected from the company as a Capital Gains Tax.

Capital Gains Tax is a tax on the profit when you sell (or dispose of’) something (for example an asset) that’s increased in value. It’s the gain you make that’s taxed, not the amount of money you receive.

Landmark

“The award is a historic ground breaking precedent on stabilisation clauses and duty of oil companies to meet their tax obligations. It is a true testament to URA’s resolve to assess, collect and defend taxes in local and international adjudication bodies,” Mr Ali Ssekatawa, assistant commissioner litigation URA, stated. He added: “We pay tribute to URA, government team and the external lawyers Curtis, Prevost Mallet for their unbreakable spirit and professionalism.”

According to Uganda statement issued by the tax body yesterday, on February 24, the UNCITRAL Tribunal in the Heritage arbitration against Uganda issued a unanimous award dismissing all claims and ordering Heritage to pay more than $4 million (about Shs11.5 billion) of costs incurred by Uganda in connection with the case.

Related News

Zimbabwe: ‘Government stifling transparency in mining sector’

The Zimbabwe Environmental Law Association (Zela), which also runs the Publish What You Pay chapter that advocates transparency in mining revenue, said although national budgets from 2011 expressed government promises to adopt EITI and disclose information about mining contracts and revenue, there has not been any progress in that regard.

“Transparency initiatives from 2011 to 2014 in the National Budget statements have been pointing at either the adoption of the Extractive International Transparency Initiative (EITI) or adapting EITI through a domestic initiative called the Zimbabwe Mining Revenue Transparency Initiative (ZMRTI), but no real and meaningful progress was made by government on these initiatives,” Zela said in its 2015 budget analysis report.

“The initiatives appear to have faced a lot of political resistance.”

The environmental lobby group said although the 2015 National Budget called for the resuscitation of ZMRTI, the budget statement failed to give clear guidelines and projected dates of implementation, thus casting doubts on government’s commitment to public transparency and accountability on mineral revenues.

“To compound matters, no provision for dividend revenue from diamonds was made despite that government owns no less than 50% stake in all the five companies operating in Marange. The only significant disclosure on Marange diamonds was that there should be transition from alluvial to conglomerate diamond mining.”

Zela said budget statements in the past four years parroted mineral revenue transparency without any meaningful changes on the ground and also called on the Ministry of Mines and Mining Development to work closely with the Finance ministry to curb incidents of undervaluation of diamonds by the United Arab Emirates.

“Further, the Ministry of Mines representatives in the Kimberley Process Certification Scheme (KPCS) should support efforts to have the issue of under-valuation of diamonds to be discussed by the KPCS.”

Related News

Infrastructure development within the context of Africa’s cooperation with new and emerging development partners

Foreword

The turn of the Millennium has marked important developments for Africa. Three stand out in significance. First the “African lion” is becoming an important growth pole in the world economy. Continent-wide growth rates in the first decade of the century were more than double those of the 1990s, and have been more than fifty percent higher than global growth rates. Second, many African economies are resource rich and have benefitted greatly from the post 2002 commodities price boom. And, third, the centre of gravity of global growth is moving from the high income economies of the north to rapidly growing and often very large middle and low income economies of the south.

In an earlier OSAA Report entitled Africa’s Cooperation with New and Emerging Development Partners: Options for Africa’s Development published in 2009, the rapid entry into Africa of seven New and Emerging Partners (NEPs) was assessed, chronicling the rapid growth in their trade, aid and investment relations with Africa. China stood out in from the pack, but each of the remaining six emerging economies – Brazil, India, Korea, Malaysia, Russia and Turkey – have also been rapidly deepening their presence in the continent.

This new OSAA Report sharpens the focus of enquiry into the activities of these seven NEPs in Africa by examining their participation in Africa’s economic and social the infrastructural sectors. Weak and deficient infrastructure is widely acknowledged to be one of the binding constraints on the rate and sustainability of Africa’s growth and development. Amongst other objectives, the Report seeks to asses the extent to which this growing presence is driven by the desire of these seven NEPs to gain access to Africa’s abundant natural resources. It also seeks to assess whether this involvement has a character which is distinct from the involvement of Africa’s traditional partners in its infrastructural development.

Not much is known about the participation of the NEPs in Africa’s growth in general, and their infrastructure sectors in particular. The World Bank has constructed a database on the involvement of China in Africa’s infrastructure sectors, but it does not explicitly address their links with the resource sector. This Report seeks to augment this World Bank database by including a wider sample of infrastructure projects, from a greater number of countries. Through a careful search of published materials, consultation with key informants and a thorough review of material available on the web, a total of 239 infrastructure projects involving the seven NEPs was identified. In addition an analysis was conducted of Africa’s imports of capital equipment used in the infrastructure sectors. This is of course only a partial sample of the involvement of these NEPs in African infrastructure and the Report is frank in acknowledging that it is unsure how representative this sample may be. On the other hand, aside form the World Bank’s smaller database on Chinese projects in Africa, there is no other such source of material and at the very least, this Report provides a starting point for more systematic enquiry and raises a number of issues of policy relevance.

In addition to identifying the rapidly growing role of these seven NEPs – and particularly China – in Africa’s infrastructure sectors, two important conclusions emerge from the detailed analysis of this database. First, few of the activities of the NEP economies in Africa’s infrastructural sectors were, as is widely believed to be the case, focused directly on the extraction and export of commodities. This does not mean that they did not have the longer term and indirect objective of developing mutual relations in order to gain access to Africa’s raw materials in the future. Second, a distinctive feature of China’s involvement in Africa, increasingly being replicated by other NEPs, is its bundled character. Participation in large infrastructure projects involves a complex combination of aid, commercial finance, foreign investment and use of many inputs from China, frequently repaid through the receipts of commodity exports. This is known as “the Angola Mode”, following its early application in China’s support for Angola’s infrastructural development. This strategic “bundling’ is distinctive from the participation of Africa’s traditional northern partners.

But at the moment the rewards of bundling are largely reaped by the NEP economies who use it to gain business for their infrastructure firms, to foster their supplier industries and to gain access to Africa’s abundant resources. The key policy challenge facing Africa, consequently is to proactively develop its own “bundling strategy”. Since raw materials are increasingly scarce and costly, Africa is in a position to leverage access to these natural resources in return for a range of developmental assistance packages. The Sicomines venture in the DRC involves significant synergies between economic infrastructure, social infrastructure and training in return for access to mineral deposits which will be used to repay China’s investments. This may be a template which other Africa economies – and perhaps even groups of Africa economies – may use to persuade the NEPs and other partners involved in the commodities sector to devote more resources to the development of economic and social infrastructure on the Continent.

Much remains to be done in the development of infrastructure in Africa, in the contribution which the NEPs can play in the development of this infrastructure, and the lessons which can be learned by Africa to promote deeper and more beneficial involvement of other partners in its infrastructural development.

For too long African policy development has occurred in a knowledge vacuum. The key challenge is to develop evidenced-based policies to promote growth and development. However imperfect the database contained in this Report may be, it provides some level of evidence which can be used to promote more effective policies and to stimulate the development of larger and more reliable data to support the design and implementation of policies appropriate for the development not just of the continent’s infrastructure sectors, but of all sectors of economic and social activity

The report was prepared by the Office of the Special Adviser on Africa (OSAA) under the guidance and direction of David Mehdi Hamam, Director

Related News

The world economy and South Africa: extracts from SA Budget documentation

The South African economy faces a difficult few years ahead. Some of the difficulties are the result of a weak global outlook, while others have to do with the structure of our economy. But the net result is that economic growth is likely to remain subdued over the medium term, rising from a projected 2 per cent of GDP in 2015 to 3 per cent of GDP in 2017.

Slow growth means that the economy does not generate the tax revenue needed to balance our budget. To continue increasing our stock of debt, and the interest payments that will consume R420.8 billion over the next three years, would jeopardise the sustainability of the public finances. This requires government, as the custodian of public money, to take deliberate steps to narrow the budget deficit.

The 2015 Budget proposes revenue and spending measures needed to stabilise the public finances.

Economic outlook

Lower commodity prices, slow growth among major trading partners and volatility in global monetary policy and capital flows will directly affect South Africa over the next several years. The European monetary stimulus is expected to have a muted impact on GDP growth in Europe, and the anticipated weakness of the euro will limit South Africa’s currency competitiveness. Weaker commodity demand from China in particular is expected to have a negative effect on South Africa’s exports.

The net result of these trends, however, is offset by several developments. South Africa’s deepening trade links with sub-Saharan Africa, where investment has begun to diversify towards manufacturing, services and infrastructure, should continue to provide expanded export markets, though there may be negative effects from reduced Chinese demand. In the short term, lower oil prices are expected to reduce transport costs and improve the terms of trade. Disciplined government spending will reduce the economy’s vulnerability to capital outflows, and create sufficient space for monetary policy to support investment and a competitive real exchange rate.

Despite a more competitive rand, export growth has been revised down from 4.2 per cent to reflect supply-side constraints. Exports are projected to grow by 3.3 per cent in 2015 and by 5 per cent in 2017.

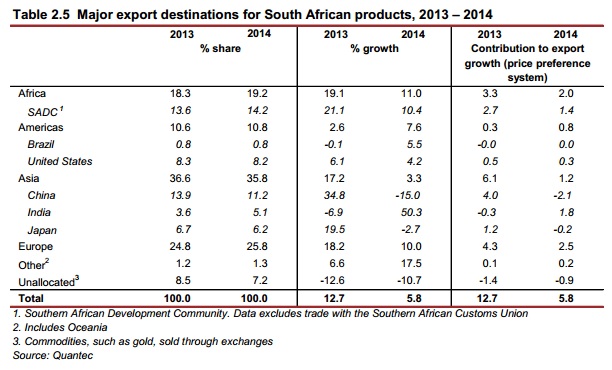

Import growth has also been revised down in line with weaker domestic demand and reduced imports of capital equipment. Exports to China fell by 15 per cent in 2014 in response to lower commodity demand. In contrast, exports to Africa grew by 11 per cent. The continent now accounts for 19.2 per cent of the export portfolio. The share of exports to Europe has also increased, to 25.8 per cent in 2014, mainly due to strong vehicle sales. Gold exports declined significantly.

Agriculture has become more export focused. Labour-intensive horticultural exports (such as grapes, citrus and tree nuts) are growing as a share of output, replacing highly mechanised grain exports such as maize. Investment growth has averaged over 10 per cent since 2010.

Related News

Kenya: Foreigners can now compete with locals for maritime sector

Foreign-owned shipping lines are set to extend their dominance of Kenya’s maritime sector after the High Court overturned a section of the law that has confined them to cargo haulage in the last five years.

A ruling delivered by Justice George Odunga on January 23 effectively renders section 16(1) of the Merchant Shipping Act, 2009 ineffective, denying State agencies a weapon that they have used to block shipping lines from engaging in other businesses.