Search News Results

Better tax systems crucial for development

Mobilising the revenues needed to further development and improve people’s lives will depend on broader tax bases, stronger tax institutions, and redoubled efforts to stem both cross-border and domestic tax evasion and avoidance. In many countries billions of dollars are lost every year to narrow tax bases, weak administrative capacity, and poor tax compliance. Helping countries to strengthen their tax systems and achieve the Sustainable Development Goals (SDGs) requires a new framework for action.

In launching the Addis Tax Initiative, over 30 countries and international organisations have now teamed up to strengthen international cooperation in this area. The Initiative highlights the crucial importance of domestic revenue for financing development and specifically stresses the importance of tackling domestic and cross-border tax evasion and avoidance.

Harnessing the momentum of the Financing for Development agenda, the Addis Tax Initiative brings new energy and enthusiasm to the field of domestic resource mobilisation (DRM), emphasizing the importance of building sustainable DRM capacity through increased technical cooperation, strong domestic governance and institutions, and the political will to drive forward tax system reforms.

In the spirit of the Addis Ababa Action Agenda, the countries subscribing to the Addis Tax Initiative declare their commitment to enhance the mobilisation and effective use of domestic resources and to improve the fairness, transparency, efficiency and effectiveness of their tax systems. Concretely, participants commit to step up efforts as specified below:

-

Participating providers of international support will collectively double their technical cooperation in the area of domestic revenue mobilisation and taxation by 2020;

-

Partner countries restate their commitment to step up domestic resource mobilisation as a key means of implementation for attaining the SDGs and inclusive development; and

-

All countries restate their commitment to ensure Policy Coherence for Development.

In addition to broad-based capacity building, participating providers of international support stand ready to expand cooperation in the following areas:

-

Enabling partner countries take advantage of the progress made on the international tax agenda, such as the OECD/G20 Base Erosion and Profit Shifting (BEPS) project and the Global Forum on Tax Transparency and Exchange of Information for Tax Purposes;

-

Integrating partner countries into the global tax debate; and

-

Improving taxation and management of revenue from natural resources.

In addition to routine OECD-DAC reporting, the International Tax Compact (ITC) will play a coordinating role to monitor and report on the increased support facilitated by this Initiative.

An ITC/OECD discussion paper released last week, ‘Examples of Successful DRM Reforms and the Role of International Co-operation’, illustrates country cases where substantial improvements in both DRM capacity and revenues were facilitated by international support. These include an increase of US$55 million collected in Kenya due to better transfer pricing and a ten-fold increase in tax revenue in Colombia.

The following countries have joined the Addis Tax Initiative: Australia, Belgium, Cameroon, Denmark, Ethiopia, European Commission, Finland, France, Italy, Germany, Ghana, Indonesia, Kenya, Korea, Liberia, Luxembourg, Malawi, Netherlands, Norway, Philippines, Sierra Leone, Senegal, Slovenia, Sweden, Switzerland, United Kingdom, and the United States.

In addition, the following international organisations have expressed their support for the Addis Tax Initiative: African Tax Administration Forum (ATAF), Commonwealth Association of Tax Administrators (CATA), Inter-American Centre of Tax Administrations (CIAT), IMF, OECD, World Bank and the Bill and Melinda Gates Foundation

Related News

Africa needs to preserve its policy space in global negotiations, says ECA Chief

As Africa hosts the 3rd Financing for Development meeting in Addis Ababa, Mr. Carlos Lopes, Executive Secretary of the United Nations of Economic Commission for Africa is confident that Africa’s agenda is now influencing how the continent negotiates its deals.

“Africa has been vigorously promoting its own agenda and it is based on that agenda that it negotiates,” said Lopes. “The continent is conscious that all these global compacts are not going to be the transformative elements of Africa’s future. We are trying to get the best we can out of the deal but not confuse that deal with our future”.

He later tweeted that “the test of Africa is to get the best out of the deal but not let the deal affect our future”.

The ECA boss told the FFD participants that two years ago, for the first time in the history African countries decided to establish a high level committee of ten Heads of States that are responsible for all the post 2015 negotiations.

“This committee will define the interest of the continent in relation to the Africa’s defined agenda, which is spelled out in a form of vision and aspirations: ‘Agenda 2063’ and ‘the 10 year-plan’ that was approved in March 2015 by the Conference of Ministers of Finance and Economic Development of the Africa,” said Lopes. He elucidated that Industrialization on the continent is a key message of these documents. “Africa has to industrialize in a different way than what was done by other regions. Africa shall learn from the mistakes of others and will not necessarily need to do the same mistakes,” he affirmed.

With regards to Addis Ababa Financing for Development conference, Lopes believes that the meeting is different from the previous ones held in Monterrey, Mexico in 2002 and Doha, Qatar in 2008.

“The Addis Ababa meeting focuses on financial and non-financial sources of funding, which is unique,” he said. ”There are no new financial resource commitments we should expect. Most of the commitments here will focus on enhancing policy environment to leverage financial and non- financial resources.”

Lopes called for Africa to preserve its policy space saying that the continent should be careful, know what the deal is and avoid giving too much and taking anything.

He also called for clear mechanism for international debts and financial management.

“The outcomes from both Monterrey and Doha include clear commitment towards international debts workout mechanism but what we know is that little has been achieved so far,” he said. “It is crucial for Addis Ababa meeting to introduce clear mechanism in this regards and engage all stakeholders to build on consensus on how to close many gaps that exist in current financial architecture,” he said.

Lopes went on expressing how since 1970 there have been more than 180 sovereign debt restructurings initiatives highlighting that the future international architecture needs concrete and binding mechanism.

Related News

tralac’s Daily News selection: 15 July 2015

The selection: Wednesday, 15 July

From Twitter:

Ambassador Mxolisi Nkosi @Malangenis

The European Commission has lifted a ban on SA ostrich and meat products, imposed in 2011 following the outbreak of FMD in the country. In total, approximately R4bn ($324 million) of exports of meat including game could be exported from SA to the EU.

See the TL of @AdanMohamedCS for a series of tweet updates on Kenya's SGR and procurement issues (following a meeting yesterday between SGR contractors, the China Rail & Bridge Corporation and Kenya's private sector). [Locals losing out to foreign suppliers in new rail project (Daily Nation)]

Selected #FFD3 updates:

Achim Steiner: speech at the Third International Conference on Financing for Development (UNEP)

Which brings me to a central message that I want to share with you today: a significant portion of financial innovation and leadership is coming from the Global South. The People's Bank of China is a leader in green credit policies and is by far the largest investor globally in renewable energies. All Brazilian banks are now mandated to mainstream environmental considerations into lending decisions. India saw over 18 million bank accounts open in one week in that country's efforts to promote financial inclusion. Ladies and gentlemen, mobilizing finance for sustainable development is no longer a North-South issue.

Increasing Africa’s fiscal space: Tax to finance Africa’s sustainable development (UNECA)

“A mere 0.44% increase per annum in tax collection in African states can mobilise about 22 billion a year which can be used to finance development projects,” suggested Mr. Carlos Lopes, ECA’s Executive Secretary to delegates attending a side event in the margins of the ongoing Third International Conference on Financing for Development.

For an extensive summary of statements by finance and development ministers at FFD: see here

Extract: Nhlanhla Nene, Minister of Finance of South Africa, speaking on behalf of the “Group of 77” developing countries and China, expressed deep concern about illicit financial flows and reaffirmed commitments made in the Rio+20 outcome in that regard. He urged the United Nations to pay attention to the 2015 African Union summit outcome on illicit financial flows, which should be replicated in other regions so that agreements could be forged to cap those flows at origin, transit and destination points. The Conference outcome, he added, should embrace high-quality deliverables and resemble the scope of both the Monterrey Consensus and Doha Declaration. The traditional definition of ODA also should be maintained, as should the separation between the financing for development track and the sustainable development goals. The committee on tax matters should be upgraded to an intergovernmental entity.

Political support in Addis summit seen as key in global tax reforms (The East African)

Addis FFD: an intergovernmental tax body? (Alex Cobham Blog)

Declaration of the Independent Commission for the Reform of International Corporate Taxation

Third ISID Forum: 'Financing for inclusive and sustainable industrial development' (UNIDO)

Carlos Lopes, Amina J. Mohammed: 'Financing for Africa’s transformation' (UNECA)

Rwanda: Financing inclusive development (World Bank)

The eighth edition of the Rwanda Economic Update, Financing Development: The Role of a Deeper and More Diversified Financial Sector, explores options for how the financial sector can develop an efficient, sound, and inclusive financial sector to help the government achieve its development vision and the benefits from a well-managed, broad-based financial sector can benefit more Rwandans.

This time last year, we estimated the 2014 growth rate at 5.7%. Against all odds, the economy grew by 7%. However, growth outlook is not entirely bright. While the oil price decline has brought a positive impact on inflation and trade, recent economic indicators show some weaknesses. Also, global risks (an increase in US interest rate, slow down of Chinese and Euro economies, and an appreciation of the US dollar) are emerging. In the medium to long-term, Rwanda’s economic resilience will not be achieved without keeping high investment rates. [Download]

Building financial capability in Rwanda (World Bank Blogs)

Cement producers raise alarm on import ‘cheats’ (Tanzania Daily News)

Revenue authorities in the East African region have reported over 60bn/- loss through misinvoicing and other malpractices, a study by the East Africa Cement Producers Association (EACPA) has stated. The Tanzania Portland Cement Company (TPCC) Managing Director and Area Manager East Africa, Mr Alfonso Rodriguez, said the matter has been reported in several occasions to relevant authorities. He said importation of substandard cement is mainly a threat to the end user and security of buildings and infrastructure in the region, especially Tanzania. "Lack of proper quality certification at origin and permissively of Tanzania Bureau of Standards (TBS) officials has allowed uncertified cement to dump products in the domestic market. creating unfair competition situation that needs to be addressed," he said.

Deadline looms for COMESA to ease travel rules (Business Daily)

Kenya and its 18 trading partners from eastern and central Africa have only two months to provide timelines for removing border controls that have curtailed movement of people and slowed the pace of trade in the region. The new deadline, set for September 30, follows the signing of a Tripartite Free Trade Agreement in June.

Kampala to host regional intelligence centre (New Vision)

Uganda is to host a regional intelligence coordination centre for the East African Community and IGAD member states to facilitate sharing information on regional threats. The proposal to set up the facility in Uganda is scheduled to be endorsed on Wednesday at a meeting of intelligence and security chiefs from the regions in Kampala. The joint intelligence centre to be established in Kampala will be supported by the African Union and is different from the facility established in Kenya.

TIPS Annual Forum 2015: 'Regional industrialisation and regional integration' (TIPS)

The conference [which concludes today] aims to deepen understanding of regional industrialisation, the role of South Africa in that context, the value chains operating across the region, and the links between regional industrialisation and regional integration.

Trade between China and Portuguese-speaking countries falls between January and May (MacauHub)

Trade between China and Portuguese-speaking countries recorded an annual decline of 28.18% in the period from January to May to US$38.31bn, according to Chinese customs data recently published in Macau. In the first five months of the year, China sold goods to the eight Portuguese-speaking countries worth US$16.513bn (-2.84%) and bought goods amounting to US$21.797bn (-40.03%), registering a trade deficit of US$5.284bn. With Angola, two-way trade registered an annual contraction of 46.70% to US$8.789bn, with China selling goods worth US$1.908bn (+ 11.58%) and purchasing goods totalling US$6.881bn (-53.45%).

Kenya to host India-Africa Expo 2015 (Daily Nation)

India and Kenya are planning India-Africa ICT Expo 2015 that will bring together over 100 top companies. These companies are leading in IT software and training and are looking to invest in the African market as they begin partnering with local firms. India and Kenya have growing trade and commercial ties with bilateral trade amounting to $4.47 billion in 2013-14. India's exports to Kenya are currently at $4.18 billion; the balance of trade is heavily in India's favour.

Global implication of lower oil prices (IMF)

Most countries in sub-Saharan Africa regulate fuel prices with discretionary adjustments, resulting in a low pass-through to the fall in oil prices. Slightly more than half of African countries regulate fuel prices in a discretionary way, while 40% rely on automatic adjustment formulas. Retail prices fell in most countries in the second half of 2014, but at a slower pace than the drop in international prices. In some countries (Angola, Cameroon, Ghana, and Madagascar), domestic prices rose in the context of fuel pricing reforms. As in other regions, the pass-through among net oil exporters was smaller (close to zero).

Madagascar: Trade Policy Review documentation (WTO)

Weak shilling sends CBK back to the drawing board (Business Daily)

AirNam flying illegally to SA (The Namibian)

Malawians fronting Chinese interest in illegal timber harvesting licences (Malawi24.com)

SADC: Ministerial Committee of Organ on Politics, Defence and Security meets in Pretoria (Angola Press)

Justice Phumaphi to preside over Lesotho crisis (Mmegi)

IGC Mozambique Growth Week 2015

Mozambique: Twelve Portuguese companies employ 22,000 people (MacauHub)

Zambia hikes petrol, diesel prices by 13% - energy regulator (Reuters)

Investing in Sustainable Development Goals (UNCTAD)

SUBSCRIBE: To receive the link to tralac’s Daily News Selection via email, please »click here to subscribe«.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome. Richard Humphries (Email: This email address is being protected from spambots. You need JavaScript enabled to view it.; Twitter: @richardhumphri1)

Related News

Rwanda Economic Update: Financing inclusive development in Rwanda

A strong, diversified financial sector can help the government gradually transition from aid, finance its development and benefit a larger group of Rwandans, according to a new report from the World Bank Group.

The eighth edition of the Rwanda Economic Update, Financing Development: The Role of a Deeper and More Diversified Financial Sector, explore options for how the financial sector can develop an efficient, sound, and inclusive financial sector to help the government achieve its development vision and the benefits from a well-managed, broad-based financial sector can benefit more Rwandans.

“Despite recent international and domestic economic developments in Rwanda the Bank’s growth projection is optimistic at 7.4 percent in 2015 and 7.6 percent in 2016,” says Yoichiro Ishihara, World Bank senior economist. “Developing a stable, sound and efficient financial sector will contribute to the government’s goal to transform the country into a middle-income country by 2020.”

After successfully weathering a drop in aid financing in 2012, Rwanda’s economy surpassed expectations with a jump in the Gross Domestic Product (GDP) from 4.7% in 2013 to 7.0% in 2014. The country’s financial sector has made great strides towards modernizing, yet limited access to external investments and anemic exports threaten to undermine progress.

The report’s recommendation to develop a sound, stable and diverse financial sector to support the country’s development comes on the heels of recent domestic budget issues that offer mixed signals on Rwanda’s future economic direction. Internal financial issues such as low tax to GDP ratio, a significant reliance on declining foreign aid, and a deterioration in current account deficits (from 7.4% of GDP in 2013 to 11.8% in 2014) dampen the country’s forward moving economy.

The government has invested in economic development but has not developed vibrant tradable sectors such as export crops, manufacturing and mining. The combination of high public investment and low export revenues has increased reliance on foreign financing, mainly in aid. Steps to diversify and strengthen the country’s financial investments and institutions will stabilize Rwanda’s positive economic growth, and help ensure the poverty rate continues to decrease as expected, to 54% in 2016, down from 63% in 2011.

“A stable financial sector provides a foundation for the achievement of all of the government’s strategic objectives, including in social development and governance,” says Carolyn Turk, World Bank’s Country Manager for Rwanda. “The steps in this economic update can accelerate the development of the financial sector in Rwanda, which is essential in financing development and for maintaining the economy’s strong expansion.”

To help Rwanda accelerate the development of an efficient, strong and inclusive financial sector the update makes several recommendations:

-

Expand into an integrated regional market to achieve a larger scale to improve the ability of regional firms to access capital markets for long-term financing needs. As part of this effort, Rwanda and Kenya have recently connected their stock markets electronically.

-

Support institutions to facilitate domestic and foreign debt financing, including through bond issuance, and accessing international capital markets.

-

Encourage institutional investors, such as pension and insurance funds, to invest in long-term projects. The most important source of such long-term financing in Rwanda is the Rwanda Social Security Board.

-

Strengthen the ability of banks to include the currently unbanked into the banking system, to support inclusion and ultimately realize the benefits of economies of scale.

-

Carefully weigh the benefits against the costs of borrowing, while allowing for the exchange rate risk that comes with borrowing in foreign currency.

Related News

Partnerships key for implementation of post-2015 development agenda and financing inclusive and sustainable industrialization, say participants at Addis event

Multi-stakeholder partnerships for mobilizing financing for industrial infrastructure and industrial projects, ranging from small and medium-sized enterprises to international large-scale investments, were the focus of an international event that took place in the Ethiopian capital on Tuesday.

The third Forum on “Financing for inclusive and sustainable industrial development” was organized by the United Nations Industrial Development Organization (UNIDO), together with the governments of Ethiopia and Senegal, and the United Nations Economic Commission for Africa (UNECA), on the margins of the Third International Conference on Financing for Development.

“Achieving the Sustainable Development Goals (SDGs) requires more than finances. I am convinced that partnerships are the means to implement the post-2015 development agenda. When countries industrialize in an inclusive and sustainable way, they can create decent jobs and preserve their resources without exploiting the environment or people,” said Ban Ki-moon, UN Secretary-General. Inclusive and sustainable industrialization is more than likely to play a significant role in the post-2015 development agenda. The first official ‘zero draft’ of the SDGs features Goal number 9 which aims to “build resilient infrastructure, promote inclusive and sustainable industrialization and foster innovation”.

LI Yong, the Director General of UNIDO, said: “The crucial challenge that the global community has gathered here in Addis Ababa to address is how to finance the achievement of the SDGs. In my view, this challenge is so immense that no single entity or institution will be able to overcome it on their own. I firmly believe that it can only be resolved through effective multi-stakeholder partnerships bringing together all the major players in the development process, including governments, bilateral and multilateral development agencies, national and international development finance institutions, the private sector, civil society and academia.”

Hailemariam Desalegn, Prime Minister of Ethiopia, noted that his country’s overall goal of attaining middle-income status rested on the growth of the manufacturing sector. “My government is not only continuing to heavily invest in infrastructure and on developing the necessary human capital with the required skills and know-how, but also in setting up industrial zones and agro-food parks which are expected to serve as the epicenter of the agro-industrial transformation process in our country,” he said. Commending UNIDO’s Programme for Country Partnership, being implemented in Ethiopia and Senegal, Desalegn said it will help further develop suitable institutional capacity and an enabling infrastructure, and facilitate the creation of a vibrant private sector and an overall conducive business environment “for the realization of inclusive and sustainable industrial development, which can only be achieved in partnership with all stakeholders”.

Speaking about the Plan Sénégal Emergent, which aims to make his country an emerging economy by 2035, Amadou Ba, Minister of Economy and Finance of Senegal, said the plan focuses, among other matters, on the development of the country’s industrial potential. “In this regard, UNIDO’s Programme for Country Partnership enables quality technical assistance delivery, and introduces innovative financing models through the synchronization and the coordination of resources from the government, the private sector and development partners within an integrated framework,” he said. According to the minister, the Government of Senegal has decided to allocate national financial resources for the implementation of the Programme for Country Partnership for Senegal.

Participants discussed public finance for industrial infrastructure and its benefits for attracting investment, job creation and export promotion, and ways to align private finance to the industrial strategy of governments and to attract quality foreign investment in large industrial projects. They also looked at challenges for future official development assistance, and at prospects for investments in developing and emerging countries, as well as at UNIDO’s role as a neutral broker in coordinating and forging partnerships, creating synergies and facilitating technology transfer. At the end of the Forum, participants took part in a field visit to the Eastern Industrial Zone, an industrial park where light manufacturing factories have recently been established as a result of foreign direct investment.

Related News

Trade Policy Review: Madagascar

The third review of the trade policies and practices of Madagascar takes place on 14 and 16 July 2015. The basis for the review is a report by the WTO Secretariat and a report by the Government of Madagascar.

Report by the Secretariat: Summary

Madagascar is slowly recovering from the sociopolitical crisis which broke out in 2009 and was brought to an end by the December 2013 presidential elections. The economic upturn which began in 2014 has been boosted by the strong performance of rice farming and the extraction and subsequent exportation of heavy metals such as nickel, cobalt and titanium. Trade reforms, especially in the area of trade facilitation, have also played a part.

Madagascar has experienced far-reaching changes in the structure of its merchandise trade since the previous review of its trade policy in 2008. The country has become a major exporter of nickel and other minerals and ores. Agrifood exports have become more diversified, reflecting the immense wealth of Madagascar’s land and of Malagasy know-how. Services exports have also grown, representing a market of close to US$1.4 billion, in view of the importance of tourism. Exports of made-up clothing, traditionally Madagascar’s leading export group, plummeted with the end of the preferences granted by the United States under the AGOA, which were reinstated in June 2014.

Overall, economic growth in the period 2009-2014 (averaging less than 1% per year) remained well below its potential, as Madagascar emerged from its fourth sociopolitical crisis in 20 years. These recurrent crises have discouraged external partners and plunged the population into severe poverty: more than 90% of the country’s inhabitants (compared to less than 70% in 2005) are living on less than 2 US dollars a day, and many people suffer from malnutrition. Madagascar will be unable to achieve most of the Millennium Development Goals (MDGs) by 2015, even those which had been considered achievable before the most recent crisis.

The crisis and its various consequences (including the rundown state of basic infrastructure – transport, energy and water in particular, the worsening of the country’s governance problems and the subsequent drying up of all forms of foreign aid), caused a sharp fall in government revenue. With operating expenses remaining high, the public deficits which should have ensued were contained by cuts in the investment budget. Even so, the fiscal deficit (including grants) amounted to 3.5% of GDP in May 2015. The Central Bank has contributed, in accordance with its statutes, to financing the budget deficit, and the other domestic banking institutions have also made contributions. The resulting crowding-out effect, along with a judicial environment inspiring but little confidence (including in regard to the realization of bank guarantees), has been instrumental in maintaining lending rates at very high levels approaching 50%.

Inflation in Madagascar, the main determinants of which include the prices of agricultural products (especially food products) on local markets and the prices of imported petroleum products, has been gradually lowered from 10.3% in 2007 to around 6% recently, as a result of State subsidies in the form of a parallel preferential exchange rate (overvaluation of the national currency, the ariary) for imports, together with several successful rice-growing seasons. The import subsidies on petroleum products did, however, contribute to the shrinking of the country’s international reserves (equivalent, on average, to 2.9 months of goods and non-factor services imports between 2008 and 2013), leading to the reintroduction of the requirement that a portion of export earnings be repatriated and converted into ariary. The national currency has fluctuated somewhat, with an overall trend towards appreciation of the real effective exchange rate and, therefore, towards a less competitive domestic economy. Overall, the sharp decline in imports and exports of goods and services, which fell from 80% to less than 70% of GDP between 2008 and 2014 despite the growth in mining exports, reflected, among other things, a slight dip in the importance of trade for Madagascar.

The mining sector owes its strong performance to major foreign direct investment in two mining projects, despite the country’s political instability. Since the start of operations to extract nickel, cobalt, titanium and other heavy metals in 2013, the Malagasy economy has become essentially mining-based, and now obtains a third of its export earnings from these products. Nevertheless, the mining sector’s contribution to GDP is just 4%, as the products exported are generally unprocessed, and gold and precious stones are extracted and exported for the most part on an informal basis. In any event, at present Madagascar does not have the infrastructure needed to produce electricity in the quantity normally required by a mineral processing industry.

Restructuring the electricity operator JIRAMA and upgrading the country’s electricity supply had already been identified as priorities in Madagascar’s previous review, in 2008. These priorities remain as relevant as ever, and Madagascar’s per capita electricity consumption is less than one tenth of average African consumption. Although the sector is, de jure, open to competition, the fact that electricity selling prices are fixed by the State at low levels (below production cost) does not encourage the entry of new operators. Some economic operators are obliged to lease costly and polluting generators in order to produce their own power.

In the petroleum sector, the State has also intervened in many trade-related areas, such as price setting, the suspension of duties and taxes, and a parallel preferential exchange rate. Some services, in particular maritime cabotage of petroleum products and the provision of aviation fuel, are currently in the hands of suppliers holding monopolies. In this connection, the drop in global prices in 2014 should prompt the Government to reinstate the “true price level” of these products on the domestic market and undertake a reform of the sector. Customs duties on mining and energy products are 7% on average, with rates ranging up to 20%.

Madagascar’s agriculture has also been through very difficult years since 2010, with virtually zero growth over the review period and a sharp decline in 2013, when the rice and maize harvests were destroyed by swarms of locusts, a cyclone, floods and drought. Unlike a number of African LDCs, Madagascar appears to have been unable, over the past decade, to adopt the means needed to bring about a real increase in food production; in 2013, net food production per capita had fallen back to its 2004 level. As a result, there has been a substantial increase in imports of most food products since 2008.

The agricultural sector also offers tremendous export potential through a range of niche products, such as cloves, vanilla, lychees, honey, foie gras, groundnuts, cocoa paste and unroasted coffee. Madagascar still has vast swathes of potentially arable, but still unexploited land on which to develop such production, but the land problem is currently one of the key challenges to investment in the country. A wide-ranging reform of land legislation, initiated in 2005, has already led to significant progress in making property ownership more secure. It would be sensible to broaden this reform to encompass the conditions of access to real estate by foreigners, which might be re-examined and published on the Internet. Although foreigners have access only to titled, state-owned land by means of long leases, many other texts contain references to the “acquisition” of land by foreigners, and some companies change nationality or use nominees for this purpose.

Madagascar has substantial fishery and aquaculture potential, and its shrimp and crab exports are significant. However, deep-sea fishing in Madagascar’s waters takes place under trading conditions which are favourable to foreign companies, in that there are no maximum catch limits. Reforms are needed in order to achieve sustainable management of resources while maximizing income from fisheries. Forest management has been affected by serious abuses, and the authorities have not yet succeeded in halting exports of rare timbers (palisander and rosewood), or of crocodiles and other wild animals, despite commitments made within CITES. The average level of protection of the agricultural sector (including plant, animal, fisheries and forestry production) is 14.1%, slightly higher than in 2008 (13.9%).

Provided that appropriate policies are introduced, the manufacturing sector offers exceptional opportunities, especially in the agrifood and handicrafts areas, because of Madagascar’s abundant flora and fauna, its rich waters and the wealth of Malagasy know-how. It is highly likely that growth in these areas will largely come from small-scale SMEs, as long as the State does away with the excessive, complicated and less than transparent taxation which is currently discouraging them from moving out of the informal economy. Industries, especially those which are export-oriented, are adversely impacted by the high taxes on businesses and cumbersome labour legislation, as well as by the difficulty of obtaining foreign currency to purchase inputs and the high rates of duty on the latter, long delays in the payment of VAT refunds, the high cost of customs controls and quality controls, burdensome export documentation requirements and, lastly, the requirement that a portion of earnings be repatriated and converted into the national currency.

The Free Zones and Enterprises (ZEF) regime, under which a large number of enterprises have registered (in many cases fictitiously), could provide a partial solution to the problem. The bulk of industrial investment in Madagascar would not have taken place without this regime, which offers all manner of generous benefits to investors that undertake to export, in principle, 95% of their production. However, as the regime is being widely abused it is a prime candidate for far-reaching reforms, with a view to better integration in the ordinary law regime.

During the period under review, significant progress was made in the area of trade reforms, especially as regards trade facilitation. Madagascar continues to grant at least MFN treatment to all its trading partners. It has never been involved as either complainant or defendant in a WTO dispute settlement process. The country has recently made remarkable efforts to update its WTO notifications; its WTO Reference Centre is operational, and local participation in WTO online training courses has increased significantly as a result. Madagascar is party to trade agreements covering around 50 trading partners, including COMESA and the SADC, the most recent of these being the interim Economic Partnership Agreement (EPA) between the EU and the Eastern and Southern Africa States, which entered into force in 2012. Madagascar grants duty-free entry to all its SADC and COMESA partners, on a non-reciprocal basis. Tariff reduction under the EPA began in January 2014.

There have been a number of tariff reductions, essentially on agricultural inputs, bringing Madagascar’s simple average applied (mainly ad valorem) MFN rates down from 13% in 2008 to 12.2% in 2015. However, less than one third of tariff lines are bound; a few of the applied rates exceed the bound level; and less than 6% of the applied tariff is zero-rated. Having lowered its customs duties, Madagascar would do well to resist the temptation to generate tax revenue from import and export flows by increasing the rates of other duties, as illustrated by the new excise duty on imported vehicles. Import taxes (levied internally and on entry), which account for more than half of tax revenue, still figure prominently in the government budget, and this is thwarting attempts to eliminate taxes on international trade.

Madagascar has been striving constantly since 2005 to improve its customs services. Since March 2015, minimum import values are reportedly no longer being used for customs valuation purposes. Significant progress has been made with the electronic Single Window, and the move towards paperless customs clearance procedures is very close to completion. The MIDAC System, an integral part of the Single Window, now allows several of the numerous control institutions required to approve import and export transactions to transmit their respective authorizations electronically to the Customs. However, work still remains to be done to ensure that the fees assessed actually reflect the services provided. Technical and financial assistance to upgrade the legislative and institutional framework for standards and technical regulations, such as sanitary and phytosanitary measures, seems essential, particularly in order to boost Malagasy exports.

Government procurement volumes fell sharply in 2009, probably owing to the sociopolitical crisis. Foreign sources of supply accounted for a mere 0.6% of total government procurement in 2013. Madagascar is neither a member nor an observer of the Plurilateral Agreement on Government Procurement concluded under WTO auspices. The country has nevertheless made significant efforts to be transparent by publishing its automated government procurement management system on the Internet.

The authorities are aware that any reform of trade policy will be ineffective if it is not underpinned by improvements in Madagascar’s sociopolitical system. These would involve, in particular, strengthening political and constitutional stability and ensuring the rule of law, enhancing the legal protection of persons, strengthening real-estate ownership rights and improving governance, including within the many state-owned enterprises. If these reforms are achieved, the Malagasy people, who have seen most of their social and economic indicators plummet over the past seven years, will have renewed cause for optimism.

Related News

Investing in women is vital to ending poverty, boosting needed growth

Closing persistent gender gaps is vital to boosting sustainable growth and ending poverty by 2030, World Bank Group President Jim Yong Kim said Tuesday, calling for scaled-up efforts to expand women’s access to good jobs, assets, and infrastructure.

“Economic growth is the most powerful tool we have for realizing a world free of poverty. The world economy needs to grow faster and more sustainably,” he told a panel in Addis Ababa alongside the Third International Conference on Financing for Development. “It needs inclusive growth that promotes opportunity for all, and that requires the full participation men and women.”

Aid targeting gender equality has risen in recent years, contributing to significant gains in health and education in many countries. But aid aimed at leveling the playing field for women remains low in what the OECD calls the “economic and productive sectors” of transport and storage, communications, energy, banking and business, industry, mining, construction, and trade.

Women’s jobs in these sectors are lower-paying and less secure. Globally, they still earn less, own less, run smaller businesses, employ fewer people, and create fewer jobs than men, and they remain vastly more vulnerable to poverty. They are also far less likely than men to have access to a bank account, mobile money provider, or other financial service, according to the latest Global Findex report. IFC, the Bank Group’s private sector arm, meanwhile estimates the annual financing and capacity gap facing women-owned small and medium enterprises in emerging markets at US$260 billion-$320 billion.

All of this adds up to a costly missed opportunity for women, families, and economies, research shows. The OCED estimates that on average, across its member countries, a 50 percent reduction in the gender gap in labor force participation along would boost GDP an extra 6 percent by 2030, with a further 6 percent gain if gaps closed entirely.

“When women earn more, public finances will improve and commercial profits increase because of increased demand and productivity,” President Kim said. “When we promote true equality – including equal pay for equal work – we all stand to benefit, because better educated mothers produce healthier children, and women who earn more invest more in the next generation.”

“We have fallen short in bringing women’s assets, earnings, and employment in line with those of men. This should galvanize us to arm ourselves with the best possible evidence about what works to close these gaps, leverage new partnerships and funding streams, and sharply scale up the smartest, most promising programs to meet these challenges.”

Along with other multilateral development banks (MDBs) and the IMF, the World Bank Group announced plans July 10 to extend more than US$400 billion in financing over the next three years and work more closely with private and public sector partners to mobilize the resources needed to achieve the historic new Sustainable Development Goals (SDGs).

To finance those goals, “collecting taxes fairly, efficiently, and transparently is critically important – in ways that don’t penalize women when they bring home a second income, for example, or spend money on food and other goods that sustain their families,” President Kim said. “So is government spending on the smartest possible investments that lift constraints and unleash the potential of all citizens. Foreign direct investment, bond issuance, and financing from institutional investors are also needed.”

The SDGs are ambitious and demand equal ambition in using the “billions” of dollars in current flows of official development assistance (ODA) and all available resources to attract, leverage, and mobilize “trillions” in investments of all kinds – public and private, national and global.

ODA, estimated at US$135 billion a year, provides a fundamental source of financing, especially in the poorest and most fragile countries. But more is needed. Investment needs in infrastructure alone reach up to US$1.5 trillion a year in emerging and developing countries.

The Bank Group is now concluding global consultations on a new gender strategy, to be launched in late 2015. Participants from government, civil society, and the private sector have stressed that along with healthcare and education, women need equal access to good jobs, training, financial resources, safe public transportation and other key infrastructure, and support in caring for others.

Related News

Secretary-General asks business to join forces with UN on Framework for financing global priorities

Meeting on Tuesday with CEOs, heads of state and ministers at a forum on the sidelines of a global finance summit, Secretary-General Ban Ki-moon called on the corporate community “to be our partners in supporting and financing this agenda.”

The call came on the second day of a global conference on “financing for development”, tasked with finding resources for a 17-point, 15-year plan on meeting human needs, protecting the planet and ending poverty. These Sustainable Development Goals will be up for final approval at the UN General Assembly in September.

“I urge private sector leaders – including CEOs and institutional investors – to be part of the solution, and to consider new commitments for investment in sustainable development,” the Secretary-General added, noting that the UN Global Compact, has rallied business behind these important issues and, with over 8,000 companies and 4,000 non-business stakeholders in 170 countries, it can “mobilize a global force of businesses for good.”

The 14 July International Business Forum attended by the Secretary-General was held at the Hilton Hotel in Addis Ababa, Ethiopia. In its morning session, more than 400 CEOs and business leaders heard addresses from H.E. Sam Kahamba Kutesa, President of the United Nations General Assembly; H.E. Hailemariam Desalegn, the Prime Minister of Ethiopia; Jim Yong Kim, President of the World Bank Group; and former basketball star Dikembe Mutombo, Chairman and President of the Dikembe Mutombo Foundation, Inc.

The Addis Ababa Action Agenda under negotiation represents a global consensus on a working relationship between private, philanthropic and public sectors, on addressing social justice and sustainable production and consumption, and on closing a yawning infrastructure gap.

However, the meeting takes place in a period of low expectations for global economic growth rates, weakened international trade, declining investment flows to developing countries, and persistent problems regarding debt, including in developed countries, noted both in the United Nations World Economic Situation and Prospects, mid-year update, 19 May, and the 9 July update to the World Economic Outlook of the International Monetary Fund.

A report of an intergovernmental committee of experts released last year said that lack of capital is not the issue, It cited estimates of “robust” annual global savings from private and public sources of $22 trillion, and of total global financial assets of about $220 trillion. Nevertheless, constraints on government budgets indicate a crucial role for the private sector and responsible business practices in helping to mobilize resources for pressing global needs.

The International Business Forum was organized by:

International Chamber of Commerce (Chair)

Columbia Center on Sustainable International Investment

European-American Chamber of Commerce

Foundation Center

Global Clearinghouse for Development Finance

International Finance Corporation

Principles for Responsible Investment

World Business Council for Sustainable Development

World Economic Forum

Women’s World Banking

United Cities and Local Governments

UN Global Compact

UN Foundation

Related News

UNCTAD: Investing in Sustainable Development Goals

Action Plan for Promoting Private Sector Contributions

The United Nations’ Sustainable Development Goals need a step-change in investment

Faced with common global economic, social and environmental challenges, the international community is defining a set of Sustainable Development Goals (SDGs). The SDGs, which are being formulated by the United Nations together with the widest possible range of stakeholders, are intended to galvanize action worldwide through concrete targets for the 2015-2030 period for poverty reduction, food security, human health and education, climate change mitigation, and a range of other objectives across the economic, social and environmental pillars.

Private sector contributions can take two main forms; good governance in business practices and investment in sustainable development. This includes the private sector’s commitment to sustainable development; transparency and accountability in honouring sustainable development practices; responsibility to avoid harm, even if it is not prohibited; and partnership with government on maximizing co-benefits of investment.

The SDGs will have very significant resource implications across the developed and developing world. Estimates for total investment needs in developing countries alone range from $3.3 trillion to $4.5 trillion per year, for basic infrastructure (roads, rail and ports; power stations; water and sanitation), food security (agriculture and rural development), climate change mitigation and adaptation, health and education.

Reaching the SDGs will require a step-change in both public and private investment. Public sector funding capabilities alone may be insufficient to meet demands across all SDG-related sectors. However, today, the participation of the private sector in investment in these sectors is relatively low. Only a fraction of the worldwide invested assets of banks, pension funds, insurers, foundations and endowments, as well as transnational corporations, is in SDG sectors, and even less in developing countries, particularly the poorest ones (LDCs).

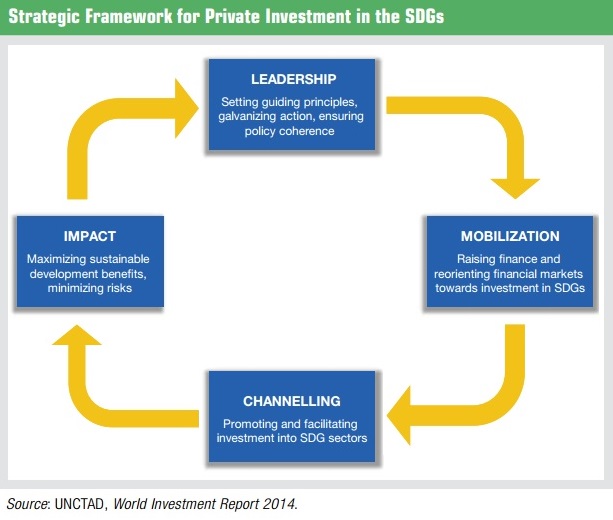

UNCTAD proposes a Strategic Framework for Private Investment in the SDGs

A Strategic Framework for Private Investment in the SDGs addresses key policy challenges and solutions, related to:

-

Providing Leadership to define guiding principles and targets, to ensure policy coherence, and to galvanize action.

-

Mobilizing funds for sustainable development – raising resources in financial markets or through financial intermediaries that can be invested in sustainable development.

-

Channelling funds to sustainable development projects – ensuring that available funds make their way to concrete sustainable-development oriented investment projects on the ground in developing countries, and especially LDCs.

-

Maximizing impact and mitigating drawbacks – creating an enabling environment and putting in place appropriate safeguards that need to accompany increased private sector engagement in often sensitive sectors.

A set of guiding principles can help overcome policy dilemmas associated with increased private sector engagement in SDG sectors

The many stakeholders involved in stimulating private investment in SDGs will have varying perspectives on how to resolve the policy dilemmas inherent in seeking greater private sector participation in SDG sectors. A common set of principles for investment in SDGs can help establish a collective sense of direction and purpose. The following broad principles could provide a framework.

-

Balancing liberalization and the right to regulate. Greater private sector involvement in SDG sectors may be necessary where public sector resources are insufficient (although selective, gradual or sequenced approaches are possible); at the same time, such increased involvement must be accompanied by appropriate regulations and government oversight.

-

Balancing the need for attractive risk-return rates with the need for accessible and affordable services. This requires governments to proactively address market failures in both respects. It means placing clear obligations on investors and extracting firm commitments, while providing incentives to improve the risk-return profile of investment. And it implies making incentives or subsidies conditional on social inclusiveness.

-

Balancing a push for private investment with the push for public investment. Public and private investment are complementary, not substitutes. Synergies and mutually supporting roles between public and private funds can be found both at the level of financial resources – e.g. raising private sector funds with public sector funds as seed capital – and at the policy level, where governments can seek to engage private investors to support economic or public service reform programmes. Nevertheless, it is important for policymakers not to translate a push for private investment into a policy bias against public investment.

-

Balancing the global scope of the SDGs with the need to make a special effort in LDCs. While overall financing for development needs may be defined globally, with respect to private sector financing contributions special efforts will need to be made for LDCs, because without targeted policy intervention these countries will not be able to attract the required resources from private investors. Dedicated private sector investment targets for the poorest countries, leveraging ODA for additional private funds, and targeted technical assistance and capacity building to help attract private investment in LDCs are desirable.

When implementing IIA reform and choosing the best possible options for designing treaty elements, policymakers have to consider the compound effect of these options. Some combinations of reform options may “overshoot” and result in a treaty that is largely deprived of its basic investment protection raison d’être. For each of the reform actions, as well as their combinations, policymakers need to determine the best possible way to safeguard the right to regulate while providing protection and facilitation of investment.

» Read more in Investing in Sustainable Development Goals, Part 1

Reforming the International Investment Regime: An Action Menu

The IIA regime is at a crossroads; there is a pressing need for reform

Growing unease with the current functioning of the global IIA regime, together with today’s sustainable development imperative, the greater role of governments in the economy and the evolution of the investment landscape, have triggered a move towards reforming international investment rule making to make it better suited to today’s policy challenges. As a result, the IIA regime is going through a period of reflection, review and revision.

As evident from UNCTAD’s October 2014 World Investment Forum (WIF), from the heated public debate taking place in many countries, and from various parliamentary hearing processes, including at the regional level, a shared view is emerging on the need for reform of the IIA regime to make it work for all stakeholders. The question is not about whether to reform or not, but about the what, how and extent of such reform.

World Investment Report 2015 offers an action menu for such reform

WIR15 responds to this call for reform by offering an action menu. Based on lessons learned, it identifies reform challenges, analyses policy options, and offers guidelines and suggestions for action at different levels of policymaking.

IIA reform can benefit from six decades of experience with IIA rule making. Key lessons learned include (i) IIAs “bite” and may have unforeseen risks, therefore safeguards need to be put in place; (ii) IIAs have limitations as an investment promotion and facilitation tool, but also underused potential; and (iii) IIAs have wider implications for policy and systemic coherence, as well as for capacity-building.

IIA reform should address five main challenges:

-

Safeguarding the right to regulate for pursuing sustainable development objectives. IIAs can limit contracting parties’ sovereignty in domestic policymaking. IIA reform therefore needs to ensure that such limits do not unduly constrain legitimate public policymaking and the pursuit of sustainable development objectives. IIA reform options include refining and circumscribing IIA standards of protection (e.g. FET, indirect expropriation, MFN treatment) and strengthening “safety valves” (e.g. exceptions for public policies, national security, balance-of-payments crises).

-

Reforming investment dispute settlement. Today’s system of investor-State arbitration suffers from a legitimacy crisis. Reform options include improving the existing system of investment arbitration (refining the arbitral process, circumscribing access to ISDS), adding new elements to the existing system (e.g. an appeals facility, dispute prevention mechanism) or replacing it (e.g. with a permanent international court, State-State dispute settlement, and/or domestic judicial proceedings).

-

Promoting and facilitating investment. The majority of IIAs lack effective investment promotion and facilitation provisions and promote investment only indirectly, through the protection they offer. IIA reform options include expanding the investment promotion and facilitation dimension of IIAs together with domestic policy tools, and targeting promotion measures towards sustainable development objectives. These options address home- and host-country measures, cooperation between them, and regional initiatives.

-

Ensuring responsible investment. Foreign investment can make a range of positive contributions to a host country’s development, but it can also negatively impact the environment, health, labour rights, human rights or other public interests. Typically, IIAs do not set out responsibilities on the part of investors in return for the protection that they receive. IIA reform options include adding clauses that prevent the lowering of environmental or social standards, that stipulate that investors must comply with domestic laws and that strengthen corporate social responsibility.

-

Enhancing systemic consistency. In the absence of multilateral rules for investment, the atomised, multifaceted and multilayered nature of the IIA regime gives rise to gaps, overlaps and inconsistencies between IIAs, between IIAs and other international law instruments, and between IIAs and domestic policies. IIA reform options aim at better managing interactions between IIAs and other bodies of law as well as interactions within the IIA regime, with a view to consolidating and streamlining it. They also aim at linking IIA reform to the domestic policy agenda and implementation.

WIR 2015 offers a number of policy options to address these challenges. These policy options relate to different areas of IIA reform (substantive IIA clauses, investment dispute settlement) and to different levels of reform-oriented policymaking (national, bilateral, regional and multilateral). By and large, these policy options for reform address the standard elements covered in an IIA and match the typical clauses found in an IIA.

A number of strategic choices precede any action on IIA reform. This includes whether to conclude new IIAs; whether to disengage from existing IIAs; or whether to engage in IIA reform. Strategic choices are also required for determining the nature of IIA reform, notably the substance of reform and the reform process. Regarding the substance of IIA reform, questions arise about the extent and depth of the reform agenda; the balance between investment protection and the need to safeguard the right to regulate; the reflection of home and host countries’ strategic interests; and how to synchronize IIA reform with domestic investment policy adjustments. Regarding the reform process, questions arise about whether to consolidate the IIA network instead of continuing its fragmentation and where to set priorities as regards the reform of individual IIAs.

When implementing IIA reform and choosing the best possible options for designing treaty elements, policymakers have to consider the compound effect of these options. Some combinations of reform options may “overshoot” and result in a treaty that is largely deprived of its basic investment protection raison d’être. For each of the reform actions, as well as their combinations, policymakers need to determine the best possible way to safeguard the right to regulate while providing protection and facilitation of investment.

» Read more in Investing in Sustainable Development Goals, Part 2

Related News

tralac’s Daily News selection: 14 July 2015

The selection: Tuesday, 14 July

Making regional trade work for Africa: turning words into deeds (UNCTAD)

In its latest Policy Brief, UNCTAD identifies some of the barriers to implementing regional trade agreements in Africa and proposes remedial actions that may be taken by national Governments, development partners and regional institutions. A well-known characteristic of the regional integration process in Africa is the multiplicity of regional trade agreements (RTAs). There is recognition by African leaders that RTAs have enormous potential to foster regional trade and development in the region. However, the low rate of their implementation has left this potential largely locked up. To realize this potential, national Governments, development partners and regional institutions need to boldly and creatively tackle the drawbacks to effective implementation of RTAs. This policy brief identifies some of the main barriers to implementation and proposes remedies for them. [Download]

Selected updates from the FFD conference:

A comprehensive summary of presentations at Day One plenary sessions (UN)

President Macky Sall: 'Africa’s opportunity in Addis' (Project Syndicate)

Multilateral Development Banks to work more closely and with private and public sector partners

UNSG: Strong partnerships needed to turn billions into trillions for sustainable development

Harnessing innovative financing for nutrition in Africa (Common African Position)

Helen Clark: speech at launch of UNDP-OECD collaboration on ‘Tax Inspectors without Borders’ (UNDP)

Speech by DG Roberto Azevêdo (WTO)

The estimate for the value of unmet demand for trade finance in Africa is between 110 and 120 billion dollars. By bridging this gap we would unlock the trading potential of many thousands of individuals and small businesses across the continent. At the WTO, we have been working with regional development banks to support the creation and expansion of trade finance facilitation programmes. We are working together to close those gaps. And very soon we will be launching a new initiative with this goal in mind.

WTO members to start discussion of a possible cotton outcome in Nairobi (WTO)

WTO members exchanged views on a possible outcome on cotton at the Nairobi Ministerial Conference to be held in December, when they participated in a discussion aimed at enhancing transparency in relation to the trade aspects of cotton on 9 July. They also heard an update on the market situation and latest policy measures in cotton trade.

DR Congo signs the COMESA Regional Bond (COMESA)

The DRC has begun implementing the COMESA Regional Transit Customs Bond Guarantee. This follows the signing of the Inter Surety Agreement by the Director General of the DR Congo National Surety (Societe Nationale d'Assurances – (SONAS) Mrs Agito Amela Carole, Friday 10 July 2015. “The participation of SONAS in issuing one single Customs Bond for transit goods from the point of departure to destination sets the stage for the operationalization of Single Customs Territory between Congo D R and other COMESA Member States that are in the process of rolling out the CVFTS,” COMESA Secretary General Sindiso Ngwenya who witnessed the signing said.

Mozambique: Integrated Growth Poles Project (World Bank)

The Project Development Objective is to improve the performance of enterprises and smallholders in the Zambezi Valley and Nacala Corridor, focusing on identified high growth potential zones (growth poles). In the last six months project implementation has not advanced substantially due to weak procurement capacity and lack of a well-functioning and autonomous Project Coordination Unit (PCU) within the Ministry of Economy and Finance (MEF).

IGAD Ministers of Finance plead for the positive effects of remittances for the region (IGAD)

The objective of this Intergovernmental Authority on Development (IGAD) High Level Ministerial Roundtable Discussion on Remittance was to review the linkages between remittances, financing of development, and household food security in IGAD Member Countries with a view to formulating appropriate policies that enhance remittance contribution to local, national and regional economies and while protecting the remittance flows. The other objective is to assess the impact of challenges that Money Transfer Operators (MTOs), or remittance companies, especially after legislation in the US, UK and Australia made it increasingly difficult for people to transfer money to receiving countries. [Presentation]

Botswana: latest financial inclusion data (FinMark Trust)

50% of the population are banked, indicating an increase from 45% in 2009, while 39% use informal mechanisms to manage their finances. The percentage of those who do not have/use any financial products/services, neither formal nor informal is at 24% – these individuals save their money at home, and they rely on family and friends to borrow money. Financial inclusion is higher among adults residing in cities and towns (86%) compared to those living in urban villages (78%) and rural areas (64%). There is a higher rate of inclusion among males (79%) than females (73%). The study shows that Botswana ranks number 5 in the SADC region with regards to financial inclusion.

China buys US$3.5 billion of graphite extracted in Mozambique (MacauHub)

Graphite mining operations in Mozambique can now move ahead after Chinese companies signed long-term purchase contracts worth US$3.5 billion, according to the Economist Intelligence Unit. The most advanced of the projects underway is one run by Australia’s Triton Minerals in Nicanda (Cabo Delgado), already considered the world’s largest graphite reserve, which recently signed a contract with Chinese raw materials trading company Shenzhen Qianhai Zhongjin, securing financing of US$200 million. In addition to this financing, split into equity in the project and credit, the Chinese partner has committed to buying 200,000 tons of graphite in the long term.

Zimbabwe: Govt urged to stop cheap sugar imports (The Herald)

The future of nearly 20 000 workers employed in the Lowveld sugar industry is under threat owing to an influx of smuggled cheap sugar amid reports that over 50 000 tonnes of the commodity is being dumped into the country every year. Cheap low quality sugar is reportedly being smuggled into the country mainly from Malawi. The parliamentary portfolio committee on Land, Agriculture Mechanisation and Irrigation last Friday implored Government to stem the rampant smuggling of sugar and issuing of import licences to save the local multi-million sugar industry from collapse.

Speaking after a tour of the Lowveld, the committee said there was an urgent need to arrest the ongoing dumping of cheap and low quality sugar onto the local market. Zimbabwe produces about 480 000 tonnes of sugar every year against a local demand of 300 000 tonnes leaving the country with a surplus of about 180 000 tonnes. Some of the surplus sugar is exported but declining world sugar prices have left Zimbabwe short of international markets.

ZimTrade calls for removal of non-tariff barriers (The Herald)

Zimbabwe’s foreign trade promotion body, ZimTrade, says there is a need to streamline the country’s regulatory framework as part of critical steps in narrowing the $3 billion trade deficit. An outdated or improperly constituted regulatory framework can act as a barrier to effective trade. ZimTrade CEO Ms Sithembile Pilime said there was need for a complete review of the country’s regulatory structure to ensure that it is not inadvertently hindering the country’s exports.

Trade between Angola and Brazil totals US$2.371mn in 2014 (MacauHub)

Trade between Angola and Brazil totalled US$2.371mn in 2014, the Brazilian Agency for Export and Investment Promotion (Apex-Brazil) said Friday in a statement. Apex-Brazil also said that last year Brazilian exports to Angola reached US$1.261mn and imports of Angolan products totalled US$1.109mn, giving Brazil a trade surplus of US$152mn.

Tanzania: Forest ecosystems in the transition to a green economy and the role of REDD+ (UNEP)

Deforestation in Tanzania could cost the national economy 5,588 billion Tanzanian Shillings (US$3.5 billion, based on 2013 exchange rates) between 2013 and 2033 on current trends, highlighting the importance of investing in the forestry sector to alleviate poverty and boost growth, according to a new report. This based its analyses on the annual deforestation rate of at 372,816 hectares per year between 1995 and 2010, an estimate provided by the National Forest Monitoring and Assessment 2014.

SE4All expert report details concrete ways to boost finance for sustainable energy

The report by the Finance Committee of SE4All’s Advisory Board, ‘Scaling Up Finance for Sustainable Energy Investments’, identifies four broad ‘investment themes’ where action could help drive increased investment: developing the Green Bond market, using Development Finance Institutions’ de-risking instruments to mobilize private capital, exploring insurance products that focus on removing specific risks; and developing aggregation structures that focus on bundling and pooling approaches for small-scale projects. [Download]

Kenya dismisses Somalia suit in border dispute (Business Daily)

Kenya is confident of winning a court battle against Somalia which on Monday formally filed a complaint with the International Court of Justice over a long-running border dispute linked to lucrative oil and gas reserves in the Indian Ocean. Attorney-General Githu Muigai said the case filed by Somalia was “baseless and lacked the relevant backing of international law on maritime issues”.

Judges to combat money laundering, financing of terrorism (New Era)

Senior judges and magistrates from 13 out of 17 Eastern and Southern African Anti-Money Laundering Group Member States will gather in Swakopmund next week for a judicial retreat. The main purpose of the meeting will be to deliberate on issues related the effective and timely adjudication of civil and criminal matters involving money laundering, financing of terrorist activity and proliferation financing, including identification of assets, as well as freezing and forfeiture of assets obtained with the proceeds of crime. The retreat, scheduled for July 13 to 15, is the first of its kind to be held in Sub-Saharan Africa.

Tanzania to ratify African charter on statistics to influence policymaking (IPPMedia)

Tanzania will ratify the African charter on statistics chiefly to help identify underlying political economy issues related to the collection, analysis and use of data for policy-making. Deputy permanent secretary in the finance ministry, Prof Adolf Mkenda said yesterday that the government was committed towards ratifying the document that was initially signed early 2012. The document has been adopted by 16 countries in Africa with exception of the East African countries of Kenya, Tanzania, Uganda, Rwanda and Burundi. Delivering the key note speech at the opening of a joint regional workshop AfDB/SADC/COMESA and ECOWAS on GDP compilation in the framework of implementing the 2008 System of National Account, he said: “We will ratify the charter.”

Cecilia Malmström: 'Modernising trade policy - effectiveness and responsibility' (European Commission)

Nigerian entrepreneurs in Istanbul's textile markets (IMI)

Mega-projects approved for years are still not running in Mozambique - IESE (Club of Mozambique)

ECA, Germany, World Bank to launch new network of excellence on land governance (UNECA)

Ufa Declaration: the house that BRICS are building (Daily Maverick)

SUBSCRIBE: To receive the link to tralac’s Daily News Selection via email, please »click here to subscribe«.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome. Richard Humphries (Email: This email address is being protected from spambots. You need JavaScript enabled to view it.; Twitter: @richardhumphri1)

Related News

Financing for Development Conference in Addis Ababa: Multilateral Development Banks to Work more closely and with private and public sector partners

The third international conference on Financing for Development opened on 13 July 2015 in Addis Ababa, Ethiopia. The opening plenary meeting was opened by the UN General Secretary, Ban Ki-moon. The African Development Bank (AfDB) was represented by Mrs. Geraldine Fraser-Moleketi, its Special Envoy on Gender.

The summit is to discuss new and innovative ways of soliciting funds to pay for the second generation of development programs known as sustainable development goals (SDGs). The SDGs, a UN-sponsored blueprint, has much wider and loftier ambitions than the Millennium Development goals (MDGs

During an earlier a meeting on 13 July, the Heads of the Multilateral Development Banks (MDBs) vowed to work more closely and with private and public sector partners to help mobilize the resources needed to meet the historic challenge of achieving the new initiative – Sustainable Development Goals (SDGs).

The keys points of discussions included:

- The SDG agenda is ambitious and will require significantly more resources than the MDGs. While the discussion during the MDGs was on aid and debt forgiveness, the conversation has now changed and is about what countries can do for themselves. Hence the focus is much more on domestic resource mobilization and creating an environment for crowding in private sector finance.

- Africa in 2015 is very different from the Africa at the turn of the century. With over a decade of sustained economic growth, Africa today has options which it did not previously have. More and more African countries are becoming creditworthy and accessing international capital markets – more than US$ 7 billion in 2014 alone. Similarly, African economies are increasingly financing their own development themselves through increased domestic revenues. During the last fifteen years, there has been a 4 fold increase in domestic revenues mobilized by African economies – in excess of $500 billion in 2015. That is ten times the amount of aid that Africa received in that year.

- The African Development Bank is at the center of this process of transformation and has a Ten Year strategy designed to meet the changing needs of the continent. The AfDB is innovating with new instruments, such as providing qualified ADF only countries with access to ADB resources; the creation of the Africa 50 Fund to scale up infrastructure financing; and an innovative exposure exchange with other multilateralism to leverage our balance sheet to scale up lending to North Africa, where we have high levels of exposure.

- In the coming years, MDBs will need to reevaluate the efficacy of their business models to make sure that they evolve with the changing needs of their clients in order for them to make sure that they remain true partners in development.

The group comprises African Development Bank, Asian Development Bank, European Bank for Reconstruction and Development, European Investment Bank, Inter-American Development Bank, World Bank Group (referred to as the MDBs), and the International Monetary Fund.

» From Billions to Trillions: MDB Contributions to Financing for Development (PDF, 1.61 MB)

Related News

Azevêdo urges UN’s Financing for Development summit to ‘close gaps’ in trade finance

Speaking at the opening session of the Third International Conference on Financing for Development in Addis Ababa on Monday 13 July, WTO Director-General Roberto Azevêdo outlined the major gaps which exist in the provision of trade finance, particularly in Africa and Asia, and the major impact that this can have on growth and development. He urged development partners to continue working together to help close these gaps.

The session was attended by UN Secretary General Ban Ki-moon, the President of the UN General Assembly, H. E. Sam Kahamba Kutesa, the President of the World Bank, Dr Jim Yong Kim, the Prime Minister of Ethiopia, Mr Hailemariam Desalegn, and many other heads of state and government, ministers and leaders of international organisations.

The Director-General said:

“Trade played a major role in the successful global effort to halve extreme poverty – and it can do a great deal more in the years to come. A range of policy measures are needed to make sure that the poor feel the full benefits of trade.

“We have identified trade finance as a key issue here. Up to 80% of global trade is supported by some sort of financing or credit insurance. But developing countries are still suffering from the consequences of the 2008 crisis. The supply of credit has not yet returned to normal levels. And so we are seeing big financing gaps, particularly in Africa and Asia.

“The estimate for the value of unmet demand for trade finance in Africa is between 110 and 120 billion dollars. By bridging this gap we would unlock the trading potential of many thousands of individuals and small businesses across the continent. The smaller the business, the bigger the gains.

“In Asia, the unmet demand for trade finance is estimated at over 1 trillion dollars. As a result, all too often, opportunities for growth and development are missed. Businesses are deprived the fuel they need to grow. And we are prevented from leveraging trade's full power as a source of development.

“We need to respond to this problem. At the WTO, we have been working with regional development banks to support the creation and expansion of trade finance facilitation programmes. We are working together to close those gaps and will be redoubling our efforts in the months ahead with a new initiative to achieve this goal.”