Search News Results

tralac’s Daily News selection: 23 July 2015

The selection: Thursday, 23 July

Launched in Windhoek: the Namibia Trade Information Portal

The portal is a web-based platform on which the Government of the Republic of Namibia will publish trade regulatory information from all government offices, ministries, and agencies that impose controls on Namibian trade. The portal will provide a single, authoritative source and will reduce the effort and time required for traders to access the information and documentation required for trade.

Developing a SA-Mozambique forestry value chain (CAJ News)

South Africa’s Department of Trade and Industry is hosting a delegation of government and private sector officials responsible for the forestry sector in Mozambique. “This is an important step in deepening regional integration and the development of agro-regional value chains thus improving the competitiveness of the region. The focus is on the development of Mozambique forestry value chain to foster a mutual relationship with South African companies,” says Minister Rob Davies. The mission follows a Memorandum of Understanding on Forestry Based Industries that was signed between Mozambique and South Africa in 2011, during the Presidential State Visit by President Jacob Zuma to Mozambique.

First SADC financial inclusion Indaba: speech by SA's Minister of Finance (Treasury)

As a result the majority of cross-border remittances between the SADC countries use informal means. South Africa is one of the destination countries for many in the SADC region looking for better opportunities. According to a 2012 study conducted by the Centre for Financial Regulation and Inclusion on behalf of FinMark Trust, the South Africa/SADC remittance market was estimated at R11.2 billion annually, of which an estimated R7.6bn (68% of total remittances) was sent via informal channels.

The use of informal remittance services has two major implications – the integrity of the formal remittance system is severely undermined, whilst particularly low-income migrants face both the high costs and the high risk of using informal means of remitting funds. While there have been notable efforts to improve the situation in the region, the efforts to reduce costs and make remittance services more accessible within the formal remittance market need to be taken a step further. In this context there is a need for a more graduated policy approach - that balances regulation and the risk of exclusion. We hope that this Indaba can take this important aspect forward.

Tanzania: New financial inclusion goal is set at 75% (Daily News)

Zambia: Barclays launches savings charter (Daily Mail)

Mozambique: National strategy for financial inclusion update (StarAfrica)

Time for action: concrete steps for IIA reforms (UNCTAD)

There is a pressing need for systematic reform of the International Investment Agreement regime. As is evident from the heated public debate and parliamentary hearing processes in many countries and regions, a shared view is emerging on the need for reform of the IIA regime to ensure that it works for all stakeholders. By now, IIA reform has become a “must”. Today, the question is not about whether to reform, but about the what, how and extent of such reform. Whatever option countries prefer, they need to bear in mind three challenges: [The author, James Zhan, is Director of the Investment and Enterprise Division]

South Africa: Trade and Industry Portfolio Committee workshop on trade, investment policy: Day 1, Day 2 (Parliament)

Winning Africa’s future: food security for all (International Policy Digest)

In a little less than 7 days, more than 1400 participants will gather in Nairobi on 30-31 July 2015 to discuss how Africa can win its future under the theme “Re-imagining Africa’s Food Security Now and into the Future under a Changing Climate.” Because the discussion occurs just before two big global conferences slated for 2015, it could set the pace for how Africa can catalyze a just future for all. [The programme]

EAC Food and Nutrition Security Policy implementation strategy: short-term assignment (EATH)

Commodity Markets Outlook (World Bank)

The World Bank is nudging up its 2015 forecast for crude oil prices from $53 in April to $57 per barrel after oil prices rose 17% in the Apr-Jun quarter, according to the Bank’s latest Commodity Markets Outlook, a quarterly update on the state of the international commodity markets. The Commodity Markets Outlook also provides detailed market analysis for major commodity groups, including energy, metals, agriculture, precious metals and fertilizers.

In a special feature assessing the roles played by China and India in global commodity consumption, the Outlook finds that demand from China and, to a lesser extent, India, over the last two decades significantly raised global demand for metals and energy—especially coal—but less so for food commodities.

WTO members raise record number of trade concerns on food safety, animal and plant health

The WTO committee dealing with food safety, animal and plant health, formally known as the Committee on Sanitary and Phytosanitary Measures, heard a record number of specific trade concerns when it met on 15–16 July 2015. Several members raised concerns about the European Union’s proposed amendment of its approval procedure for genetically modified food and feed, also known as biotech products. The United States said that the amendment would allow EU member states to restrict or ban the use of such products with no justified reasons. The Committee discussed China’s proposed regulatory change related to biotech products.

The meeting also discussed a few concerns that were raised at previous meetings of the SPS Committee, including the EU’s ongoing work on defining criteria for identifying endocrine disruptors, South Africa’s concern about EU measures on citrus black spot, import restrictions on Japanese food products following the nuclear power plant accident, and concerns expressed by Peru and a number of other countries regarding the application and modification of the EU regulation on novel foods.

Eliminate barriers in sugar exports (Zambia Daily Mail)

Sugar producers in Southern Africa have called on governments to eliminate non-traffic barriers introduced by some COMESA members affecting free movement of sugar within the regional market. Swaziland Sugar Association chief executive officer Mike Matsebula said under the COMESA free trade area, sugar is supposed to move freely within the region. “Instead of implementing zero-tariff obligation, some sugar producers have introduced NTBs to prevent the inflow of sugar. They have introduced derogations, non-transparent import licencing schemes and surcharges. It is a concern that FTA commitments are not complied with,” Dr Matsebula said this last week during a conference hosted by Zambian sugar producers.

KEBS meets importers over new quality marks (Daily Nation)

The Kenya Bureau of Standards has held a briefing for over 200 importers and clearing agents on the new Import Standardization Mark sticker set to take stage this August. According to a statement from Kebs, the new mark provides a levelled playing field for all players in the market as only genuine certified products will be allowed in the market. Importers and clearing agents now have less than 10 days to apply and acquire the new mark for their goods to be accepted into the country. Importers from the East African Community (EAC) member states dealing with goods from Partner States are not required to apply for the sticker, but goods imported from COMESA will require the mark.

Zimbabwe: IMF 2nd SMP review next month (NewsDay)

The International Monetary Fund mission will undertake the review of the second supervised economic reform programme on Zimbabwe next month amid indications the country has made progress under the plan. IMF resident representative in Zimbabwe Christian Beddies told NewsDay that the country made progress on the SMP under the first review held in March. Commenting on the performance of the economy during the first half of the year, Beddies said the economic situation remains difficult with the agricultural sector underperforming due to adverse weather conditions. “Mitigating factors include better performance in other sectors, most notably gold. One of the key tasks of the upcoming mission will be to reassess macroeconomic conditions and if need be revisit growth forecasts,” Beddies said.

Zimbabwe Investment Authority approves $971m FDI projects (New Zimbabwe)

Republic of Congo: IMF concludes 2015 Article IV Consultation

China grants loan to Mozambique for power transmission line (MacauHub)

China will grant a loan of US$400 million to Mozambique, the amount outstanding for the construction of a second power line for energy transmission from the centre to the north of the country, a government spokesman said Tuesday in Maputo. At the meeting the government of Mozambique ratified, among other things, the loan agreement concluded on 11 June, by which the Islamic Development Bank offered to provide US$200 million dollars for the transmission line that will link Chimuara, in Zambézia province, and Nacala, in Nampula province, over a route of just over 600 kilometres.

Chinese tourists to Zimbabwe sees 62% jump in Q1 (People's Daily)

Manufacturers sign financing MoU with DBN (The Namibian)

Namibian manufacturers have signed an agreement with the Development Bank of Namibia through which the Namibian Manufacturers Association will identify opportunities to promote development in manufacturing, primarily through financing of enterprises that are members of NMA.

Zambia: Kwacha to stabilise, assures Kalyalya (Daily Mail)

Kenya: CBK curbs banks’ daily forex trade to save the shilling (Business Daily)

Africa impact evaluation course: event notification (IPA, J-PAL)

SADC urges journalists to foster regional integration (Nyasa Times)

Kenya: The epicenter of the future of African entrepreneurship (CPI Financial)

We have very strong neighbours, we have Egypt in the north, we have the DRC and Mozambique on the side, Zambia as well and Somalia. This is a natural market for us; the average age is around 25 and when you look at that, the opportunity, these are very connected people. That is the space, with the demographics right, the innovation right, if I look at the innovation hubs, the ICT hubs, the technology labs in Nairobi today, the silicon savannah we talk about in Kenya; Technology is going to be a big frontier. Nairobi is bubbling globally for the innovation and technology. [The author, Joshua Oigara, is Chief Executive Officer of KCB Group]

Latin America/Caribbean: Promoting growth through effective policy (World Bank)

The conference, early in July, was jointly organized by the World Bank and the government of Peru, as a preparatory event for the 2015 Annual Meetings of the World Bank and the International Monetary Fund. The topics discussed included productivity improvement, job creation, infrastructure provision, and poverty alleviation. [Download the presentations]

Lin Songtian: 'China, Africa industrial capacity co-operation aims for win-win' (Capital FM)

China has accumulated successful experience in the process of its fast growth, and also paid a hard price for environment. As a sincere friend and reliable partner of Africa, we never want to see African countries follow the path of “pollution first and cleaning up later”. The Chinese government will give full support to African countries to set up industrial access standards and environmental threshold and will regulate Chinese businesses to abide by the four principles of industrial capacity cooperation. [The author is Secretary-General of the Chinese Follow-up Committee of Forum on China-Africa Cooperation]

Sylvia Mishra: 'How will the Trans-Pacific Partnership affect India?' (Observer Research Foundation)

Even though the magnitude of impact from trade diversion on India when the TPP is in place can be debated, it is certain that trade and investment diversions hurting the Indian economy is most likely to occur. Some of this impact may be mitigated due to a combination of inclusion in RCEP and other bi-lateral agreements. India should also re-engage the US in advancing BIT negotiations. However, a new 'trade order' is expected with much higher standards congruous to TPP standards and hence, efforts are required on the domestic front for India to acquire preparedness across industries to be able to compete globally.

SUBSCRIBE: To receive the link to tralac’s Daily News Selection via email, please »click here to subscribe«.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome. Richard Humphries (Email: This email address is being protected from spambots. You need JavaScript enabled to view it.; Twitter: @richardhumphri1)

Related News

Increasing stockpile of trade-restrictive measures “a cause for concern”

The increasing stockpile of trade-restrictive measures introduced by WTO members remains a cause for concern, and continued vigilance is required, according to the latest report on trade-related developments presented on 23 July 2015 by WTO Director General Roberto Azevêdo.

On the positive side, an increasing number of trade-liberalizing measures, such as tariff-cutting measures, were adopted by WTO members during the period under review, 16 October 2014 to 15 May 2015.

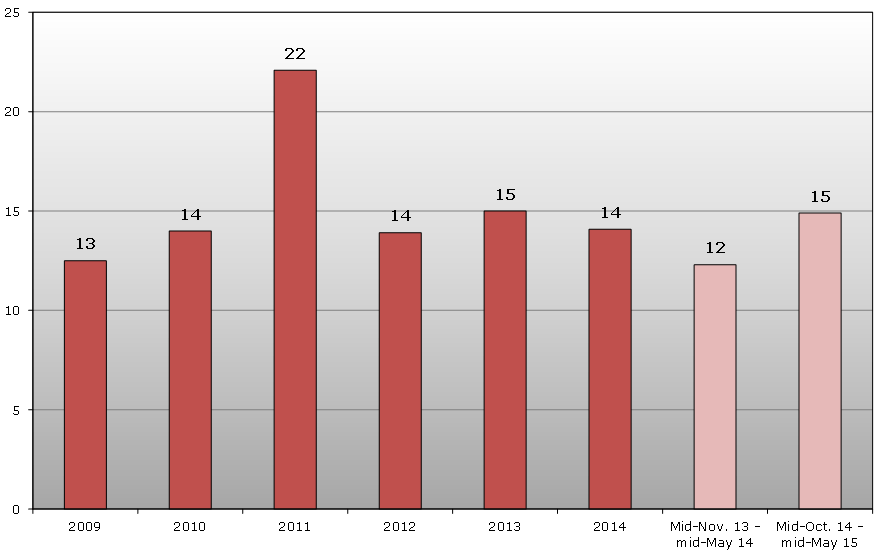

The report confirms that WTO Members continue to show some restraint in introducing new trade-restrictive measures with the introduction of such measures (excluding trade remedies) relatively stable since 2012. During the period under review, 104 new trade-restrictive measures were put in place – an average of around 15 new measures per month.

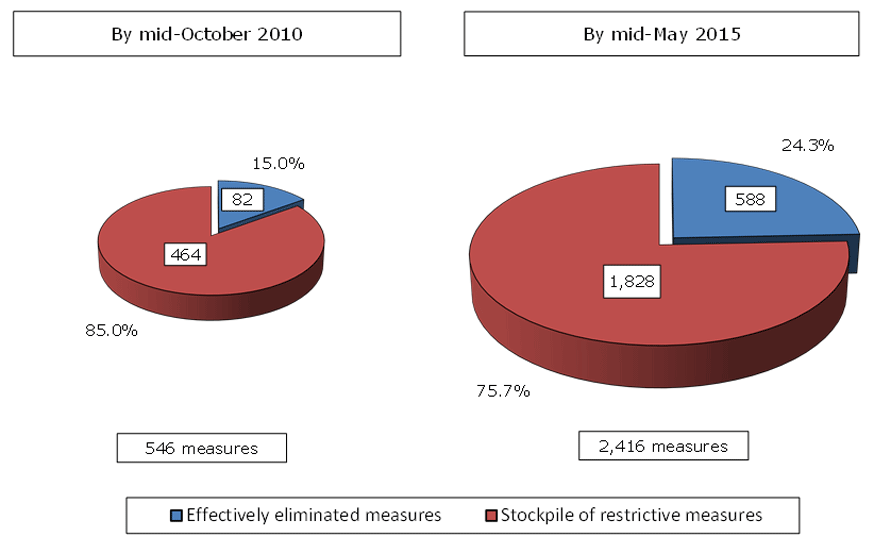

Nevertheless, the slow pace of removal of previous restrictions means that the overall stock of restrictive measures is continuing to increase. Of the 2,416 restrictions (including trade remedies) recorded by the monitoring exercise since October 2008, only 588 have been removed. In other words, the total number of those restrictive measures still in place currently stands at 1,828 – up by over 12% compared to the last report. The addition of new restrictive measures, combined with a slow removal rate, remains a persistent concern. With the share of removals of total restrictive measures still under 25%, the longer-term trend in the number of trade-restrictive measures remains an area where continued vigilance is required.

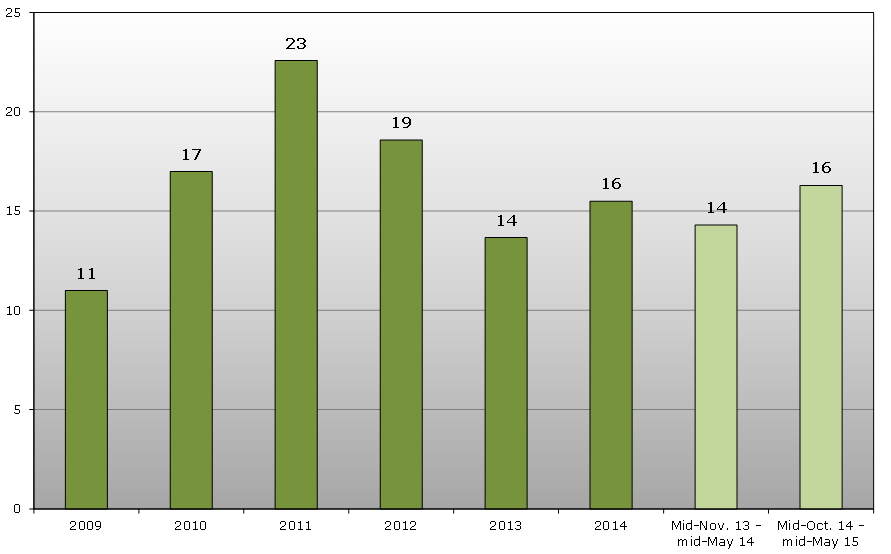

More encouragingly, WTO Members continued to adopt measures aimed at facilitating trade, both temporary and permanent in nature. Members implemented 114 new trade-liberalizing measures during the period under review – an average of more than 16 measures per month. When counted without trade-remedy actions, WTO Members have adopted more liberalizing trade measures than restrictive measures since the end of 2013.

Also, in the area of trade remedies, a slight deceleration has been observed in the number of initiations of anti-dumping investigations during the period under review. Initiations of countervailing investigations and safeguard investigations have also declined recently.

The broader international economic context also supports the need for continuing vigilance and action. Trends in world trade and output have remained mixed since the last monitoring report, as merchandise trade volumes and GDP growth picked up in the second half of 2014 but appear to have slowed in the first quarter of 2015. Economic activity remained uneven across countries as the United States (US) and China slowed in Q1 while growth in the euro area and Japan picked up. Plunging oil prices and strong exchange rate fluctuations – including an appreciation of the U.S. dollar and a depreciation of the Euro – generated uncertainty to the economic outlook. Lower prices for oil and other primary commodities were expected to provide a boost to importing economies, but reduced export revenues weighed heavily on commodity exporters. In light of these developments, the Secretariat’s most recent forecast (14 April 2015) predicted a continued moderate expansion of trade in 2015 and 2016, although the pace of recovery was expected to remain below historical averages. According to this forecast, growth in the volume of world merchandise trade should increase from 2.8% in 2014 to 3.3% in 2015 and further to 4.0% in 2016.

This report shows that WTO Members introduced 75 new general economic support measures. The main beneficiaries were selected industries in the manufacturing sector, activities related to the agricultural sector and a number of programmes to assist SMEs. A variety of financial aid schemes appear by design to seek to encourage or boost exports while others identify conservation and the environment as overall objectives. A significant number of programmes which seek to eliminate or reduce subsidy schemes for gasoline and other fuels were identified during the period under review.

From transparency and systemic points of view, important developments took place in the WTO’s TBT and SPS Committees. The SPS Committee has witnessed a significant growth in notifications from developing countries leading to the highest number of notifications to date. An increase in the number of notifications does not, however, automatically imply greater use of measures taken for protectionist purposes. Another noteworthy development was a significant increase in the number of new specific trade concerns (STCs) raised in the TBT Committee.

A number of recent policy developments in services were recorded during the review period. These include reforms of the insurance and pension sectors and easing of the rules on foreign investment in the construction and railway transportation sectors in India, as well as the lifting of restrictions on foreign investment in several service sectors in China. Also noteworthy is the amendment of the Russian Law on Foreign Investment in Strategic Companies; several important reforms in the audio-visual and ICT sectors by Argentina, Belgium, Mexico, Madagascar, Myanmar, Poland, the Russian Federation, Sierra Leone and the United States (US); and also in financial services by China, India, Myanmar and the Philippines.

The overall assessment of this monitoring report is that the continuing increase in the stock of new trade-restrictive measures recorded since 2008 remains of concern in the context of an uncertain global economic outlook. WTO Members – individually and collectively – must show leadership and reinforced determination towards eliminating existing trade restrictions and refrain from implementing new ones.

The multilateral trading system has proven its usefulness in providing a predictable and transparent framework governing trade between nations and in helping Members resist protectionist pressures as a response to the global economic and financial crisis and thereafter. The role of the multilateral trading system in providing a stable, predictable and transparent trading environment should be kept in mind as Members prepare for the WTO’s MC10 in Nairobi in December. Decisive progress in eliminating remaining trade-restrictive measures combined with further multilateral trade liberalization would be a powerful policy response.

Key findings

104 new trade-restrictive measures (excluding trade remedy measures) were put in place in the reporting period 16 October 2014 to 15 May 2015 – an average of around 15 new measures per month.

This monthly rate has remained relatively stable since 2012, though the overall stock of measures nevertheless continues to rise.

Of the 2,416 measures recorded since October 2008, less than 25% have been removed, leaving the stock of restrictive measures still in place at 1,828. This represents an increase of 12% compared to the last report.

This remains a cause for concern and continued vigilance is required from WTO members.

More encouragingly, WTO Members have adopted more trade-liberalizing measures (excluding trade remedy actions) than trade-restrictive measures since the end of 2013. Continuing this trend, during the period under review, WTO Members implemented 114 new trade-liberalizing measures – an average of more than 16 measures per month.

The broader international economic context supports the need for vigilance and action with regard to trade-restrictive measures. According to the WTO’s most recent forecast (14 April 2015), growth in the volume of world merchandise trade should increase from 2.8% in 2014 to 3.3% in 2015 and further to 4.0% in 2016, but remaining below historical averages.

The multilateral trading system has proven its usefulness in providing a predictable and transparent framework governing trade between nations and in helping Members resist protectionist pressures as a response to the global economic and financial crisis and thereafter.

This role in providing a stable, predictable and transparent trading environment should be kept in mind as Members prepare for the WTO’s tenth Ministerial Conference in Nairobi in December.

Trade-restrictive measures, not including trade remedies (Average per month)

Trade-facilitating measures, not including trade remedies (Average per month)

Stockpile of restrictive measures1

Related News

Commodity prices expected to remain weak in 2015 despite slight rebound in oil price

Special feature assesses how China and India play significant roles in world commodity markets

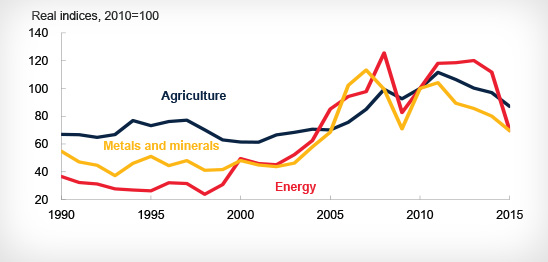

The World Bank is nudging up its 2015 forecast for crude oil prices from $53 in April to $57 per barrel after oil prices rose 17 percent in the Apr-Jun quarter, according to the Bank’s latest Commodity Markets Outlook, a quarterly update on the state of the international commodity markets.

The Bank reports that energy prices rose 12 percent in the quarter, with the surge in oil offset by declines in natural gas (down 13 percent) and coal prices (down 4 percent). However, the Bank expects energy prices to average 39 percent below 2014 levels. Natural gas prices are projected to decline across all three main markets – U.S., Europe, and Asia – and coal prices to fall 17 percent. Excluding energy, the World Bank reports a 2 percent decline in prices for the quarter, and forecasts that non-energy prices will average 12 percent below 2014 levels this year.

“Demand for crude oil was higher than expected in the second quarter. Despite the marginal increase in the price forecast for 2015, large inventories and rising output from OPEC members suggest prices will likely remain weak in the medium-term,” said John Baffes, Senior Economist and lead author of Commodity Markets Outlook.

Iran’s new nuclear agreement with the US and other leading governments, if ratified, will ease sanctions, including restrictions on oil exports from the Islamic Republic of Iran.

Downside risks to the forecast include higher-than-expected non-OPEC production (supported by falling production costs) and continuing gains in OPEC output. Possible upside pressures may come from closure of high-cost operations – the number of operational oil rigs in the US is down 60 percent since its November high, for example – and geopolitical tensions.

In a special feature assessing the roles played by China and India in global commodity consumption, the Outlook finds that demand from China and, to a lesser extent, India, over the last two decades significantly raised global demand for metals and energy – especially coal – but less so for food commodities.

China’s consumption of metals and coal surged to roughly 50 percent of world consumption, and India’s to a more modest 3 percent for metals, and 9 percent for coal. These patterns reflect different growth models and commodity consumption patterns in the two countries.

If the two countries catch up to OECD levels of per capita commodity consumption, or if India’s growth shifts towards industry, demand for metals, oil, and coal could remain strong. In contrast, given that the level of per capita consumption of food in China and India is already comparable with the world, pressures on food commodity prices are likely to ease as their population growth – one of the key determinants of food commodity demand – slows.

“China and India have played a significant role in driving global consumption of industrial commodities especially since the early 2000s. Going forward, while demand from India is likely to be a major factor in shaping consumption of industrial commodities, China will be important in driving global demand for energy given its efforts in rebalancing growth,”said Ayhan Kose, Director of the World Bank’s Development Prospects Group.

Commodity Markets Outlook also provides detailed market analysis for major commodity groups, including energy, metals, agriculture, precious metals and fertilizers.

Metals prices declined marginally in the quarter as most are still in surplus, particularly iron ore where prices are off two-thirds from their 2011 high. The World Bank projects metals prices to average 16 percent below 2014 levels this year, revised downward from 12 percent in April.

The largest decline is expected for iron ore (down 43 percent) due to new low-cost mining capacity coming online this year and next (mainly in Australia). Metals markets are adjusting by closures of high-cost operations and reduced investment. Markets will eventually tighten, in part due to large zinc mines closures, and as Indonesia’s ore export ban weighs on supplies, notably nickel.

Agricultural prices fell 2.6 percent in the quarter, due to large declines in food commodities – especially edible oils and grains – on further improvements of supply conditions and despite some adverse weather in North America and El Niño fears. The World Bank expects agriculture prices to average 11 percent below 2014 levels this year, revised downward from 9 percent in April.

Fertilizer prices, a key cost for most agricultural commodities, are likely to decline 5 percent on weaker demand and ample supply.

» Full forecast and historical data, and detailed market commentary, are available here.

Commodity price indices

Related News

Nexit – Will Namibia be able to sustain rand parity?

Since 1993 when Namibia introduced its national currency, the Namibia dollar, the country has maintained a policy of strategic parity between the Namibian dollar and the rand.

This was done for a number of reasons but principally to reassure business at the time of independence that the conduct of policy in Namibia was in safe hands and that when they invested in the country they could take out their profits at a fixed exchange rate.

For over 20 years this has been at the heart of macroeconomic and exchange rate policy in Namibia but now it looks increasingly under pressure.

On 17 June, the Bank of Namibia announced that the nation’s foreign exchange reserves had fallen to N$12,1 billion – down from N$15,7 billion just two months earlier. With its regular but increasingly perfunctory comments, the Bank of Namibia’s Monetary Policy Committee (MPC) added its usual caveat that the reserves remain sufficient to sustain rand parity. But are they?

Certainly, Namibia has enough foreign exchange reserves to cover imports for a period of approximately seven weeks given the most recent decline but reserves are certainly moving in the wrong direction. In 2012, Namibia’s foreign exchange holdings were enough to cover four months of imports. By international standards anything above three months is considered reasonably adequate.

But by the end of last year the import cover had fallen to two months and the substantial decline of reserves in 2015 should be a wake-up call to policy makers that the country is on an unsustainable path of importing far more than it is exporting and that this, unless checked, will increase the country’s vulnerability to external shocks.

PRETTY

From the 1990s up until the global economic crisis of 2008, Namibia’s balance of trade was pretty much in balance with exports and imports of goods growing in tandem. Then with the beginning of the global economic crisis in 2008 imports started to balloon and, while export growth has been adequate, especially in 2014 when diamond earnings improved, it has not been enough to pay for the country’s growing appetite for imports.

The Bank of Namibia’s MPC puts the blame squarely on the country’s appetite for imported luxury goods, in particular expensive cars. The NSA data on imports of motor vehicles does show a rapid rise over the last few years but the figures are probably vastly underestimated given the growth of normally under-valued second-hand cars. In 2014 Namibia is said to have imported some N$12,4 billion up by N$3 billion or 37,4% from the year before.

There is a more benign interpretation of events in Namibia. Some argue that the decline in foreign exchange reserves is simply a result of imports of capital equipment for new mines such as the Huisab Uranium Mine and the B2Gold Mine and that once this is over the balance of payments will return to balance as exports of minerals will increase while imports will slow. But after five years of ever widening trade deficits such a view is now dangerously optimistic.

Namibia’s worsening trade situation is no doubt compounded by the government’s budget deficits over the last few years which is resulting in ever more imports.

None of the options for addressing the nation’s trade imbalance are pleasant for the government or for the Namibian people. The politically safe approach to an impending balance of payments crisis in most countries is to use monetary policy to restrict access to credit i.e. a credit squeeze.

BLAME

This puts less blame directly on government and shifts it to the Bank of Namibia. But a credit squeeze is a dull instrument that can often lead to the destruction of many an otherwise sound business. A similarly blunt instrument that the government has to restrict spending is the use of its fiscal policy to cut government spending and raise taxes. To say the least, this is a very unpopular approach to dealing with deficit problems – just ask the Greeks how much the people like this sort of approach.

So how should the government react? If the Bank of Namibia’s MPC is correct in its assertion that the purchase of luxury automobiles lies at the heart of the import surge, a number of more focused monetary policies to push the banks to limit access to credit in these sectors is in order.

But in an economy like Namibia where funds can flow in from South Africa with ease there are too many ways around credit restrictions to one sector or another.

The other option is to impose a new series of new taxes on automobiles coming into the country, especially the larger and more expensive ones. It is not possible to impose import duties on vehicles made in Sacu but it is certainly possible to impose higher excise tax and a large scrappage or environmental fee on all new and second-hand cars.

LUXURY

With luxury new cars costing from N$800 000 to well over a million, many Namibians are moving to second hand imports. Many of these, especially the older vehicles coming from Botswana, are massively undervalued and the government needs to stop the process of VAT collection based on fictitious valuations. Instead, taxes need to be imposed based on international ‘Blue Book’ values of second-hand cars.

Irrespective of what policy measures the government chooses to impose to deal with the unsustainable trade imbalance, it is slowly running out of both foreign exchange reserves and time. The time for government to act is now before the reserves fall to what is often seen as a critical minimum i.e. approximately four weeks import cover.

While four weeks is still enough to cover imports, it is commonly seen as the point at which investors will see the writing on the wall for the Namibian dollar – rand parity and start to move ever more foreign exchange out of the country. This exit of financial capital will only hasten a crisis.

Unless the optimistic and benign approach is taken then after five years of increasing trade deficits it is time to act and use both fiscal restraint as well as tax policy to assure that we do not have a ‘Nexit’ – an exit from Namibian dollar parity with the rand and a devaluation of the Namibian dollar.

The immediate impact of devaluation would be a rise in the price of imported goods. That would not only lower living standards across the board but in the long term it would weaken Namibia’s reputation as a safe place to invest. The longer policy makers wait to address the issue of the trade deficit the greater the pain will eventually be. As the old adage goes ‘a stitch in time still saves nine’.

Roman Grynberg is professor of economics at the University of Namibia. The views expressed are entirely his own.

Related News

Africa is not a country – President Kaberuka advises on better ways of doing business on the continent

Africa is not a country but a continent of 54 states, which, in spite of many similarities, differ from one another in many respects, African Development Bank President, Donald Kaberuka told a development think-tank in Beijing on Monday, 20 July 2015.

Kaberuka said making this distinction had become necessary to ensure that potential business opportunities in African countries are not jeopardised by a single story line whereby negative issues in one country are attributed to all 54 countries on the continent. He was speaking at a round table discussion on “Investment Opportunities in Africa” organised by the Centre for China and Globalisation (CCG).

Citing the Ebola epidemic which hit three countries in West Africa, Kaberuka said it was improper to use this to scare potential businesses destined for other parts of the continent.

In the same way, he said, it was unfair to associate China’s business relationship with Africa in terms of natural resources. This is because it is varied and more sophisticated, dating back to the 1970s when the less endowed China at the time had begun to finance infrastructure projects in Africa.

Having realised the fastest industrialisation in history, China now has an opportunity to help Africa emulate its successes through new development vehicles that are sustainable and beneficial to both parties.

The world is changing and the traditional way of doings things are no longer working, Kaberuka said, noting that development actors were ill-equipped to cope with some aspects of globalisation.

“The institutions we have today for managing globalisation are lagging behind the process,” he said.

The AfDB is innovating and adapting to the changing dynamics, Kaberuka said, noting that the 2008 global financial crisis would have hit Africa much harder if the Bank did not adopt counter-cyclical measures to assuage the impact of the crisis on the regional member countries.

Furthermore, the situation would have been much worse if the emerging markets did not step in to avert the disaster.

Kaberuka said the AfDB would continue to partner with countries and institutions that devise more innovative approaches to development.

Related News

EAC states’ great expectations of securing stronger trade ties with US

East African Community countries have presented a list of issues they hope the United States government will address to expand its trade partnership with the region.

Trade ministers from the five EAC partner states have made a formal request to the US government asking it to relax the stringent measures imposed on their agricultural exports to the US and also review the high tariffs on some agricultural products such as sugar and cotton.

They are in fact seeking removal of tariffs on all agricultural exports from East Africa as well as creation of more quotas, which they say would be consistent with US obligations under the UN Millennium Development Goals and would fulfil a key demand from these countries in the World Trade Organisation.

The economic and international trade officer in Kenya’s Ministry of Foreign Affairs, James Kiiru, said that the EAC also expects US President Barack Obama, who is visiting Kenya this week for the Global Entrepreneurship Summit, to address issues raised earlier “to pave the way for us to utilise the quota-free US market under the Africa Growth and Opportunity Act (Agoa).

“Of priority are the stringent measures imposed by the US on agriculture exports, especially the sanitary and phytosanitary measures that raise the cost of exports enough to offset any additional competitiveness gained through lower tariffs,” said Mr Kiiru.

The US has imposed stringent SPS measures for agricultural products such as fresh produce and beef, and the majority of East African producers are often unable to meet the standards.

“This has made it hard for the East African countries to lobby for even more products to be added on the Agoa list, since it takes a much longer time for approval,” Mr Kiiru added.

The East African states are also pushing for a prior renewal of another 10-year term that was last month reauthorised for renewal for 10 years by the US House of Congress. The Agoa pact will be renewed in October, immediately after the current agreement expires at the end of September.

President Obama, who will attend the Global Entrepreneurs Summit in Nairobi, is likely to address the trade partnership between the EAC and the US.

Earlier this month, the US Department of State said it was reviewing Burundi’s eligibility for the trade preferences available to it under the Agoa.

“We will be taking into consideration ongoing violence and instability and the government of Burundi’s lack of respect for the rule of law in determining their eligibility for these trade preferences moving forward,” said the US State Department statement.

Trade among the EAC countries and the US amounted to $2.8 billion in 2014: US exports to the EAC reached $2 billion while American imports from the region, which rose by 52 per cent from 2013, totalled $743 million.

The main exports of agricultural products to the US are cocoa paste and powder, citrus fruits, edible nuts, wine, unmanufactured tobacco, horticultural products and vegetables.

Most agricultural exports from sub-Saharan Africa already enter the US tariff-free. There are, however, a number of products where the US retains high tariffs, such as sugar and cotton, which, if reduced, would stimulate further trade. Except for imports of sugar and cotton, imports under Agoa that are in-quota enter the US at zero tariffs.

The US retains various trade barriers on a range of agriculture goods that, if reduced, would be likely to lead to increased exports.

Sugar, meat, dairy, vegetables, processed fruit and other processed goods such as dried garlic, apricots, shea butter, yoghurt, ghee, cashew nuts, sugarcane products, sugar-containing cocoa products, oil seeds, shrimp and prawns, bananas and other vegetables and fruit such as mangoes are products facing trade barriers in accessing the US markets.

“The US should also look to where it can streamline its import procedures, reducing costs and delays to market,” said Mr Kiiru.

The renewal and extension of the Agoa period is expected to give African countries ample time to build competitive capacity in the global market. It accords preferential market access system to 39 countries in sub-Saharan Africa, including all the East African countries, to develop their economies and create free markets.

Peter Njoroge, director of economics at Kenya’s Ministry of EAC Affairs, Commerce and Tourism, says that the East African countries have not been able to fully utilise the US quota-free market under Agoa because the agreement does not comply with the WTO’s framework for free trade agreements and has been relying on a 10-year conditional special exemption window that expires in September.

“Agoa is a short-lived initiative yet investments under Agoa need to be long-term, which does not attract investors,” said Mr Njoroge. “EAC partner states will lobby the US government to give Agoa a long-term lifespan so as to give investors predictability.”

He added that the five EAC countries are expected to push for a prior renewal of another 10-year term. Although the Act provides for about 6,000 products, Kenya has only been exporting textiles and apparel.

Unlike the EU market, Mr Njoroge said, transportation costs to the US market are high, caused by lack of direct flights and sea transport from the EAC countries to the US, affecting export of products such as cut flowers to the US.

“It is expected that Kenya will soon have direct flights to the US that will also be of benefit to the other EAC partners,” noted Mr Njoroge, adding that the provision on rules of origin has been proposed for revision under the Agoa reauthorisation.

Stringent rules of origin

Agoa rules of origin are based on those in the US GSP programme. To be eligible for Agoa benefits, products must be grown, produced or manufactured in one or more of the beneficiary countries and exported directly from an Agoa beneficiary country to the US.

“With these conditions, most of the products from eligible countries cannot access the US market,” said Mr Njoroge. “Moreover, unless ‘wholly obtained’ from a single Agoa country, goods are subject to a 35 per cent value-content rule.”

According to industry sources, in some sub-Saharan African countries, activities such as tuna processing have difficulty achieving the threshold and cannot therefore be exported to the US duty-free under Agoa.

The restrictive rules of origin also do not reflect the current market reality, given that African textile mills cannot in general produce yarns or fabric in sufficient variety and quantity to meet the needs of African apparel producers or the requirements of retailers in developed countries.

Despite the challenges and the high expectations by the EAC states from President Obama’s visit, efforts are under way to ensure that they fully exploit the US market as a region. They are working on a joint sustainable strategy to exploit the US preferential trade market.

Related News

China, Africa industrial capacity co-operation aims for win-win

Recently, industrial capacity cooperation has become a catchword in China-Africa cooperation. Many African countries are eager to embrace the historic opportunity brought about by China’s economic transformation and upgrading, and become the first places to host Chinese investors, so as to add fuel to their own industrialization strategies.

There are mutual needs and complementarity between China and Africa to carry out industrial capacity cooperation and a rare historic opportunity has come for the two sides, which can help China and Africa to achieve win-win cooperation for common development, make the world more balanced, stable and prosperous, and benefit the people of China, Africa and around the world.

Industrial capacity cooperation between China and Africa is the urgent need for Africa to realize independent and sustainable development. Since the middle of the last century, African countries have achieved national independence one after another, and sought to promote economic development through international cooperation. However, some countries outside the region are only willing give Africa “fish” instead of “teaching Africa how to fish”. Many African countries still suffer from hunger and under-development.

It is impossible to realise real political independence without economic independence. By giving others fish, one might help to address the immediate needs of others. Only after “learning how to fish” can Africa sets up its own industrial system, move out of the disadvantage of exporting raw materials at a low price and importing expensive finished products, thus realizing independent and sustainable development and controlling their own destiny.

Industrial capacity cooperation is to “let African countries know how to fish”, helping Africa to get rid of the two persistent bottleneck constraints hindering its development and industrialization, i.e., insufficiency in infrastructure and talent. The Chinese government encourages Chinese businesses to invest in Africa, transfer their technologies bring more job opportunities, foreign exchange, tax revenue and added value of primary products to the local people, thus translating Africa’s abundant natural and human resources into real development results.

Industrial capacity cooperation between China and Africa is the natural trend of China’s economic transformation and upgrading. After more than 30 years of reform and opening up, China has developed a large number of leading industries which provide advanced equipments and products to the world, and numerous internationally competitive businesses have grown in China. At the same time, due to increase of labour cost, a large number of labour-intensive businesses in China need to move overseas for new development. China can and need to bring its industrial capacity overseas, and help other countries to develop while achieving China’s own development. This is also in line with the rule of world economic development. Japan and the four Asian tigers all realized economic takeoff after taking over industrial capacity from overseas, and later became source countries to export industrial capacity to overseas markets.

Africa has a population of close to 1.1 billion, which might reach 1.4 billion by 2025. The huge demographic dividend will make it one of the most ideal locations for investments from other parts of the world. In order to realize industrialization, Africa needs advantageous industrial capacity from countries such as China. The Chinese government is sincere in helping Africa to improve both “software” and “hardware” of investment, assisting them to “build a nest to attract phoenix”, and creating better environment for industrial capacity transfer. It is fair to say that China and Africa have respective advantages and mutual need for industrial capacity cooperation, helping Africa is helping China itself.

Industrial capacity cooperation between China and Africa is the objective need to safeguard world peace and prosperity. African refugees are flooding to Europe. Poverty and underdevelopment have always been the root causes of instability and unrest in Africa, which also provide the breeding ground for terrorism. Stability and development in Africa bear on sustained peace and prosperity of the world.

By investing in Africa and developing industrial capacity cooperation, especially helping African countries to develop labour-intensive industries, the Chinese businesses will create a large number of job opportunities for the local people, improve their living, and enable more African youth to go to factories, workshops, farms and office buildings to work. In that case, no one would move to the jungles to join terrorist organizations or leave their homelands to become refugees, thus Africa and the world will become more harmonious and stable.

Chinese leaders attach high importance to developing a new type of partnership with Africa featuring win-win cooperation. The essence of the policy of the new Chinese leadership is that China is willing to integrate its own development with independent and sustainable development of African countries, so as to realize common development and make the world more balanced, harmonious and prosperous.

Recently, Chinese Foreign Minister Wang Yi summarized the four principles China adheres to in international industrial capacity cooperation, which are “the right approach to righteousness and benefit, win-win cooperation, openness and inclusiveness, and market-based operation”. Wang Yi stressed that China’s industrial capacity cooperation with other countries will not come at the cost of environment and long-term interests of others. China will never take the old colonial path of looting and damaging others’ resources. So China says, so China does.

Ethiopia does not have rich oil and other energy resources, but China is committed to developing mutually beneficial cooperation with Ethiopia. In Ethiopia, the first city ring road, the first express way, the first city light rail, the first electrified railway, and the first wind power generation project are all financed by China, which have created good conditions for Ethiopia to attract foreign investment and the rapid growth of local industries and economy.

The Oriental Industrial Park built with private investment from China is the first industrial park in Ethiopia, which has attracted a host of Chinese investors. Among them, Huajian Group, a large shoe maker, with only 35 Chinese employees, offers more than 3500 jobs for local people, and contributes over US$10 million to Ethiopia every year.

China is Angola’s biggest crude oil exporting destination. Over the past 10 years and more, through the model of a package cooperation, China has helped Angola to build 39 hospitals, 78 schools, 14 power transformation stations, 20 water processing factories, 7,500 hectares of agricultural irrigation projects, upgrade 223 community networks, construct 1,343 kilometres of railway, 892 kilometres of roads, 736 kilometres of power transmission and transformation lines, making important contribution to Angola’s national reconstruction and economic development.

The oil and mineral resources of African countries like Nigeria and Chad are monopolized by western countries. It’s only natural to wonder whether western countries are also sincere in helping African countries to develop as China does for Angola and Ethiopia.

To help and support African countries to realize lasting peace and sustainable development is in line with the common interests of people across the world, and is a common responsibility of the international community. It is a pity that some countries still take Africa as their zone of influence or “back garden”, and try to rely on their traditional influence and practical deterrence to rudely interfere in Africa’s internal and external affairs, including with whom African countries should make friends and develop cooperation. They themselves are not sincere in helping African countries to develop, and try every means to disturb others’ cooperation with Africa.

While China-Africa industrial capacity cooperation is about to set sail, some western media, far away from Africa and with their eyes closed, claim that China will transfer unwanted industrial capacity and pollution to Africa. They appear to be concerned about the ecological environment of Africa, but actually are worried that Africa might advance its industrialization and realize real political and economic independence.

China has accumulated successful experience in the process of its fast growth, and also paid a hard price for environment. As a sincere friend and reliable partner of Africa, we never want to see African countries follow the path of “pollution first and cleaning up later”. The Chinese government will give full support to African countries to set up industrial access standards and environmental threshold and will regulate Chinese businesses to abide by the four principles of industrial capacity cooperation. Jidong Development, a company from China, takes the lead in applying cement surplus heat power generation technology in its cement factory in South Africa, which can save 17,000 tons of industrial coal consumption every year, thus setting the highest standard for the cement sector in South Africa. This also serves as the model for industrial capacity cooperation, which welcomes international oversight.

Tide rises and falls. Colonial time has ended and “zero-sum” mentality must be abandoned. Africa belongs to the African people, and is an important member of the international community. Only by giving up bias and selfishness and taking off “coloured glasses” can the international partners work in concert, African countries get more benefits and the world become better and more harmonious.

The author is Secretary-General of the Chinese Follow-up Committee of Forum on China-Africa Cooperation, Director-General of the African Department of the Ministry of Foreign Affairs of China, Former Chinese Ambassador to Liberia and Malawi.

Related News

Winning Africa’s future: Food security for all

In a little less than 7 days, more than 1400 participants will gather in Nairobi on 30-31 July 2015 to discuss how Africa can win its future under the theme “Re-imagining Africa’s Food Security Now and into the Future under a Changing Climate.”

Because the discussion occurs just before two big global conferences slated for 2015, it could set the pace for how Africa can catalyze a just future for all. A future where there will be food and shelter for all – where images like those from the Mediterranean Sea showing Africa’s youth risking and often losing their lives in an attempt to flee the continent will be no more.

In September, New York will host the meeting on the new Sustainable Development Goals. Climate change will be the focus of the December conference in Paris. Taken together, these two conferences represent a once-in-a-generation opportunity for Africa’s development. As the African saying goes: “When the music changes, so does the dance.” To put all countries firmly on the path to a secured food system as well as inclusive growth, there needs to be a change in the music. A new approach is therefore urgently needed to build an inclusive food system that is robust enough to create jobs and wealth for all in Africa, including the youth.

The Years in Retrospect

Sometimes looking backwards serves to provide the impetus needed to leap forward. Africa has registered impressive milestones in its thousand mile journey towards sustainable inclusive growth. The 1990s marked the release of Nelson Mandela from prison, a continental icon who demonstrated the power of dogged perseverance to one’s course. Today’s course for each and every one of us is that of charting a sustainable food secured pathway where productivity, job creation and collective wellbeing for all are the norm and not the exception.

The 2000s marked the beginning of Africa’s decade of growth – averaging 5.1% beginning in the year 2000, and doubling the average growth rate of the 90’s. This spilled over to post 2010, with estimates pegging Africa’s GDP growth at approximately 6% annually, with 6 of the world’s 10 fastest growing economies being African, and a growing middle class with 20% of the population having daily incomes of over USD 10 as of 2012.

These improvements may well be from a very low base. However, the trajectory of Africa’s transformations is undeniable. The question that will be on the mind of every participant at this year’s 2nd Africa Ecosystem based Adaptation for Food Security (EBAFOSC 2) is how best to achieve Africa’s Food Security Future that is inclusive and works for all.

How do we create enough well-paying jobs for a billion people in less than 25 years when already about 60% of our youth are unemployed? How do we harness EBA-driven agriculture to stimulate job creation, growth, and value additional partnership in Africa? How do we catalyze investments and policy support for EBA-driven agriculture as well as incentivize private sector involvement in EBA-driven agriculture to bring in capital and enhance competitiveness? These are just some of the questions EBAFOSC2 conference will be discussing. Although registration for the conference has now closed, the proceedings can be followed on Twitter at #EBAFOSC.

Africa Food Security Policy Framework

The 2003 Maputo Declaration, marked the continent’s intentions to modernize agriculture resulting in the establishment of the Comprehensive Africa Agriculture Development Programme (CAADP). The most prominent decision of this declaration was the commitment by AU member states to allocate at least 10% of national budgetary resources to agriculture and rural development, a policy implementable within five years.

A decade into this declaration, 13 countries had met or surpassed the 10% target and average continental agriculture spending increased by over 7% annually in the period. In marking this decade, the AU launched “the year of agriculture and food security” in 2014, whose climax was the adoption of the Malabo Declaration by AU Heads of State and Government. The Malabo Declaration on Accelerated Agricultural Growth and Transformation for Shared Prosperity and Improved Livelihoods is a commitment by the AU Heads of State and governments to end hunger by 2025 and reduce post-harvest losses by 50%. To operationalize the Malabo Declaration, the AUC and NEPAD launched the implementation strategy and road map to achieve the 2025 vision on CAADP. EBA-driven agriculture is recognized as among priority mechanisms for delivering the 2025 Vision on CAADP, a remarkable milestone for EBA. However, this reported growth and declarations of good intent are amidst a plethora of challenges.

Turning Africa’s Challenges into Opportunities

About 240 million people in the continent go to bed hungry; over 200 million suffer the debilitating symptoms of chronic to severe malnutrition, which also contributes to over 50% of infant mortality on the continent. The region currently spends more than USD 35 billion annually on food imports while recorded annual productivity losses amount to USD 48 billion as postharvest losses, and a further 6.6 million tonnes as potential grain yields are lost due to degraded ecosystems: food enough to meet the annual calorific needs of approximately 30 million people. Exacerbating these challenges is rapid population growth projected to hit 1.5 billion by 2030 and 2.4 billion by 2050, youth unemployment currently at 60% with an additional estimated 350 million young people entering the labor market by 2035, and climate change expected to hit the crucial agriculture sector with 11-40% yield reductions on key staples.

While these grim statistics are a resounding call to action, the continent’s inherent agriculture potential is a source of solace…

Africa’s Abounding Solutions

Africa holds up to 65% of the world’s arable land and 10% of internal renewable fresh water sources. On incomes and poverty reduction, the World Bank reports that in Africa, a 10% increase in crop yields translates to approximately a 7% reduction in poverty. Neither the manufacturing nor service sectors can achieve an equivalent impact. Nevertheless, current sector productivity is low, contributing a lowly 25-34% of continental GDP. However, the agriculture sector which currently employs up to 60% of the continent’s labour can potentially ensure inclusive and sustainable growth if its value chain is optimized holistically, and productivity losses stemmed. It can create jobs for many of the 17 million youth entering the job market annually while feeding Africa. A climate proof agriculture sector based on EBA techniques that work with nature and augment farm productivity with value addition strategies to unlock income opportunities along the entire agro-value chain will potentially result in yield increases of 116-128% and accompanying farmer income increases, and be two to four times more effective in reducing poverty relative to other sectors.

A Call to Action

The EBAFOSC 2 builds on the findings of the continental task force report “Towards a Comprehensive Strategic Framework to Upscale and Out-scale EBA-driven Agriculture in Africa.” Based on the taskforce findings, EBA driven agriculture augmented with value addition along the agro-value chain can potentially ensure not only food security, but livelihood security, enhance community climate resilience hence climate adaptation, enhance ecosystem productivity and unleash numerous income and job opportunities along the value chain by linking supply and demand side value chains.

Given the central role agriculture plays in socio-economic development in Africa, this conference presents a golden opportunity to put the continent’s food systems on track, now and well into posterity, and thereby guarantee sustainable and inclusive growth going forward.

Jointly discussing Africa’s challenges and solutions will propel Africa into the shining city on a hill, where collective prosperity for all will no longer be an elusive dream. As the African saying goes, “If you want to go fast, go alone, if you want to go far, go together.” Let’s go together to catalyze a food secured Africa and guarantee sustainable and inclusive growth for the collective benefit of all.

Related News

tralac’s Daily News selection: 22 July 2015

The selection: Wednesday, 22 July

Featured commentary: Nexit - will Namibia be able to sustain rand parity? (The Namibian)

Irrespective of what policy measures the government chooses to impose to deal with the unsustainable trade imbalance, it is slowly running out of both foreign exchange reserves and time. The time for government to act is now before the reserves fall to what is often seen as a critical minimum i.e. approximately four weeks import cover. While four weeks is still enough to cover imports, it is commonly seen as the point at which investors will see the writing on the wall for the Namibian dollar - rand parity and start to move ever more foreign exchange out of the country. This exit of financial capital will only hasten a crisis. Unless the optimistic and benign approach is taken then after five years of increasing trade deficits it is time to act and use both fiscal restraint as well as tax policy to assure that we do not have a 'Nexit'- an exit from Namibian dollar parity with the rand and a devaluation of the Namibian dollar. [The author: Roman Grynberg]

Govt gets 15% in diamond deal (The Namibian)

The Namibian government and De Beers company have agreed on a new 10-year sales agreement but the deal falls short of what the government was demanding. Last month, Cabinet said it wanted up to 30% of rough diamonds produced by Namdeb Holdings, to be supplied to local factories under the new sales agreement. Namdeb, which has land and sea operations, is owned 50/50 by the government and De Beers.

BoN sets daily limits for kwanza exchange at border towns (The Namibian)

A BIT far? Geography, investment agreements, and FDI (World Bank Blogs)

Despite hard times at home, emerging market multinationals (EMMs) continue their impressive rise in the global marketplace. In 2014, outward foreign direct investment (FDI) by developing and emerging economies increased by 23 percent, reaching a record level of $468 billion or 35 percent of global FDI flows. In little more than a decade, emerging market firms like India’s Tata Group, South Africa’s SABMiller, and China’s Haier, have established operations around the world, becoming global leaders in their respective products.

Yet, the fast and far-reaching geographic spread of these global giants is not the norm among this particular brand of multinationals. Our recent book “New Voices in Investment” where we surveyed over 700 firms from four emerging economies – Brazil, India, Korea, and South Africa—shows that, in fact, a large majority of EMMs look primarily within their regions when deciding where to invest. Although 40 percent of respondents claimed that market size and business opportunities were the main factors influencing their location decisions, their revealed preference seems to be for closer destinations. How does geography affect the investment decisions of emerging market multinationals? [The authors: Gonzalo Varela, Laura Gomez-Mera]

Is Africa’s growth sustainable in the face of climate change? (ICTSD)

So while GDP growth is laudable, its conversion to poverty reduction for the Base of Pyramid (BoP) has not always occurred. Consequently, African growth has not always been inclusive, and its long-run sustainability is therefore brought into question. Two critical concerns about Africa’s growth and future outlook are addressed in this article. Can the agriculture sector contribute toward enhancing inclusive growth and job creation on the continent? Considering the overriding threat of climate change to Africa’s growth, what is the continent’s likely position at the UN climate meeting this December in Paris, France? [The authors: Richard Munang, Robert Mgendi]

Africa: Sendai Framework starts moving (PreventionWeb)

First half of 2015 ‘hottest six months on record'- UN (WMO)

The objectives of this paper are, first, to identify how susceptible are the EAC economies to asymmetric shocks; second, to assess the value of the exchange rate as a shock absorber for these countries; and third, to review adjustment mechanisms that would help ensure a successful experience under a common currency-EAC. While the analysis draws on recent experience, backward-looking measures are imperfect for a forward-looking assessment. The paper thus also draws attention to likely further structural changes in the EAC economies (for example, large oil discoveries in some countries) as well as the intrinsic endogeneity of further integration to the currency union project itself. The paper main findings are as follows: [Download]

Integrating West African economies PPP-wise (World Bank Blogs)

What do Benin, Niger, Guinea-Bissau, Togo and Mali have in common? Apart from being members of the eight-country strong West African Economic and Monetary Union , they share a common status as low-income countries, faced with huge infrastructure needs and financing challenges. Furthermore, they have decided that one way to address these challenges and sustain their economic growth was to promote public-private partnerships through a regional framework and strategy. The issues we covered included the need to: [The author: Francois Bergere]

Over the past two days, we have had robust debate on matters close to our respective nations and how they affect our region. Politics, defence and security matters shape the development trajectory of our region. It is therefore imperative that we meet annually to take stock of the progress we are making, and if needs be re-adjust our strategies and goals, to address the security challenges of our times. While there have been remarkable developments in some areas where the region has experienced political and security challenges, there needs to be ongoing political and security engagement within the region.

Promoting peace, security and sustainable development in East Africa: GPF conference (IPPMedia)

Africa and the First Conference of States Parties to the Arms Trade Treaty: an update (ISS)

Feasibility study on the navigability of Shire-Zambezi Waterways (SADC)

From 14th to 17th July, 2015, the 14th meeting of the Joint Technical Committee (JTC) was held, at the SADC-Secretariat Headquarters in Gaborone, Botswana. The purpose of the meeting included: validating the navigability and technical investigations, transport economics and market surveys, environmental and social impact analysis, components of the Draft Final Study Report...

SADC China infrastructure investment seminar (SADC)

The main focus of the seminar (held in Beijing) was to showcase priority infrastructure projects contained in the Short Term Action Plan (STAP) 2012-2017 and in particular those in the Energy, Transport and Water Sectors. The objective of the Conference was to bring to the table, a number of bankable projects and those under preparation for consideration and possible funding. The estimated cost of the projects in the Five-Year Plan is about USD 64 billion, and it is expected that private sector will play its key role by financing some of these key projects. The Seminar was attended by major Chinese business community and other International Cooperating Partners, Investors, and Business Organizations.

Kaberuka shares his experiences with African diplomats in Beijing (AfDB)

China-Africa Entrepreneurs Forum in Pretoria: speech by Ambassador Tian Xuejun (MFA, China)

Expect more investors from China, World’s largest bank tells Kenya (Daily Nation)

3AGT: AUC, NEPAD charged on alternative sources of funding (Vanguard)

The African Union Commission and the NEPAD Planning and Coordinating Agency have been urged to facilitate the mobilisation of investment finances required for the operationalization of the Malabo Declaration on Accelerated African Agriculture Growth and Transformation (3AGT). The call was made by participants at the just concluded two-day Leadership Retreat for engagement with Permanent Secretaries /Heads of Ministries of Agriculture in AU Member States held in Nairobi, Kenya.

In a communiqué issued at the end of the retreat, the participants underscored the urgency of reviewing National Agricultural Investment Plans to align them and recommended the strengthening of CAADP activity coordination within countries to give greater impetus to the implementation of the Malabo Commitments. The Retreat also called upon Member States, that have not already done so, to fast track the development ofNational Agriculture Implementation Plans.

The updated and expanded 2015 edition of the Trade Capacity-Building Resource Guide includes profiles of 31 multilateral agencies and 37 bilateral donors. The trade-related services of 31 countries from the OECD and 16 G20 countries, some of which are also OECD members, are also reflected in the Guide. The Guide reveals that many of the OECD Development Assistance Committee (DAC) members support triangular cooperation, and other DAC members are considering introducing such support. All developing countries included in the Guide mention active participation in South-South cooperation, with Argentina, Brazil, China, Indonesia, Mexico and the Russian Federation being particularly engaged. The Guide highlights how both multilateral agencies and bilateral donors encourage and support South-South and triangular cooperation, and provides examples of projects and services for almost all multilateral and regional agencies.

Making USAID fit for purpose: a proposal for a top-to-bottom program review (Center for Global Development)

Kenya Budget 2015 guide and analysis (IEA)

UNCTAD and TradeMark East Africa strengthen collaboration

Egypt: Trade Ministry considers website for businessmen eyeing Africa (State Information Service)

Charles Brewer: 'Trade integration key to reduce poverty and support Africa’s growth' (New Times)

World Bank Group at the WTO's 5th Global Review of Aid for Trade

Pacific ACP seeks to conclude 11 years negotiation with EU (Matangi)

Work moves ahead on TPP trade pact, but nations still divided over deal (Pew Research Center)

Nigeria: World Bank to spend $2.1bn to rebuild North-east (Vanguard)

SUBSCRIBE: To receive the link to tralac’s Daily News Selection via email, please »click here to subscribe«.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome. Richard Humphries (Email: This email address is being protected from spambots. You need JavaScript enabled to view it.; Twitter: @richardhumphri1)

Related News

Trade integration key to reduce poverty and support Africa’s growth

Africa continues to remain vastly unexplored, and making Africa’s most remote regions accessible for trade will not only promote prosperity in those regions, but also elevate the continent’s continued growth path, according to The Role of Trade in Ending Poverty report recently released by the World Bank Group and World Trade Organisation.

It is important that leaders on the continent understand the role that international trade plays in development and poverty reduction in Africa. The value of trade is measured by the extent to which it delivers better livelihoods, measured through higher incomes, greater variety of choice and a more sustainable future, among others, the report indicates.

While countries need to continue to establish better trade relations with international partners, enabling trade routes within the continent can yield numerous benefits for the region and its people.

Since 1978, when DHL entered the African market, there has been a degree of transformation both economically and socially, simply due to access to new services. If we look at Cape Verde, for instance, a small country consisting of 10 islands, the quickest and most reliable way of transporting goods to and from the country is by air.

Currently, there are three commercial airlines operating in the area and given that commercial airlines offer priority to passenger baggage, offloading of cargo from these planes was a regular occurrence. In order to better service the area, we introduced a DHL flight which operates between Senegal and Cape Verde weekly. This dedicated flight route provides various trade opportunities and greatly improves connectivity in the region.

So to effectively reduce poverty, growth needs to be inclusive, and poor people are not often located where growth takes place. The World Bank and the World Trade Organisation estimate that one billion 15 per cent of the world’s population remains in extreme poverty, and that of this number, 415 million are concentrated in sub-Saharan Africa. The report states that extreme poverty in many countries is predominately a rural phenomenon, and that an estimated 75 per cent of the extreme poor in Africa live in rural areas.

Dr Jim Yong Kim, the World Bank Group president, says that beyond expanding trade, more must be done, such as building roads that connect farmers to markets: “We must always connect the poorest to trade opportunities.”

That is why connecting rural areas to trade opportunities should be a key focus for any government and business on the continent. “We have made great progress in making the global market and the world at large more accessible and connected by increasing the number of points where customers can access DHL and our global network. We now have over 4,500 retail outlets across sub-Saharan Africa. This allows anyone - from a student to a small business – access over 220 countries and destinations that we serve.

The report paints trade as a key enabler of facilitating growth in developing countries and highlights that lower trade costs and fewer barriers between countries is vital to eliminating extreme poverty.

Dr Kim said trade plays an essential role in driving private sector-led growth and job-creation and can be a powerful force in reducing poverty and increasing incomes.

Therefore, there should be a collaborative effort between the public and private sector to work together to ease doing business across borders. We work very closely with the government and custom authorities in each country on solutions to make doing business easier. There is ongoing progress with a number of successful trade blocs in place focusing on better connecting the region, and we look forward to seeing Africa continue on its growth path in years to come.

The author is the managing director of DHL Express for sub-Saharan Africa.

Related News

Is Africa’s growth sustainable in the face of climate change?

The “Africa rising” cliché, has generated a lot of views across the world. In the face of climate change, however, can Africa continue to grow?

Africa’s steady GDP growth sustained for over the last 10 years has generated significant positive reviews. African GDP has grown at about six percent per year and, over the past decade, six of the world’s ten fastest growing countries were African. The continent’s middle class is growing and 20 percent of the African population make a daily income of over US$10. Going forward, GDP growth in Sub Saharan Africa (SSA) is expected to rise to 5.5 percent in 2015, reversing a multi-decade pattern of low growth and instability.

Seen from a different angle, however, the picture is not as rosy. Aggregate poverty levels have hardly shifted and the World Bank reports that almost one in every two African lives in extreme poverty. As of 2014 Africa's growth was intangible for nearly half a billion women and men trapped in rural poverty. Looking ahead, it is estimated that under any plausible scenario, most of the world’s poor will be living in Africa by 2030.

On food security, the UN Food and Agriculture Organization (FAO) in 2010 found that nearly 240 million people, or one in every four persons in SSA lacks adequate food. On population, the World Bank also estimates that another half a billion people will be added to the continent by 2030, culminating in a total estimated population of two billion people by 2050. Youth make up 60 percent of the unemployed on the continent. Moreover, these millions of unemployed young people constitute an impending threat to stability in Africa, a possibility acknowledged by the African Union.

So while GDP growth is laudable, its conversion to poverty reduction for the Base of Pyramid (BoP) has not always occurred. Consequently, African growth has not always been inclusive, and its long-run sustainability is therefore brought into question.

Two critical concerns about Africa’s growth and future outlook are addressed in this article. Can the agriculture sector contribute toward enhancing inclusive growth and job creation on the continent? Considering the overriding threat of climate change to Africa’s growth, what is the continent’s likely position at the UN climate meeting this December in Paris, France?

African agriculture and inclusive growth