Search News Results

CAR: Companies must not profit from blood diamonds

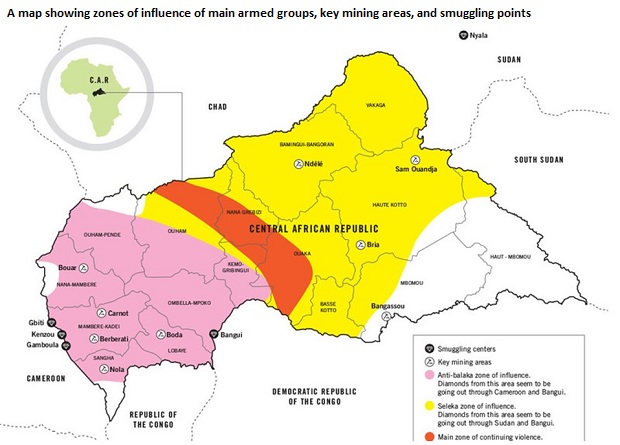

The Central African Republic’s (CAR) biggest traders have purchased diamonds worth several million dollars without adequately investigating whether they financed armed groups responsible for summary executions, rape, enforced disappearances and widespread looting, Amnesty International said in a report published on 30 September 2015.

The report, Chains of Abuse: The global diamond supply chain and the case of the Central African Republic, documents several other abuses in the diamond sector, including child labour and tax abuse.

CAR’s diamond companies could soon start exporting diamonds stockpiled during the on-going conflict in which 5,000 have died. An export ban in place since May 2013 will be partially lifted once the government meets conditions set in July 2015 by the Kimberley Process, which is responsible for preventing the international trade in blood diamonds. Before the conflict, diamonds represented half the country’s exports.

“If companies have bought blood diamonds, they must not be allowed to profit from them,” said Lucy Graham, Legal Adviser in Amnesty International’s Business and Human Rights Team.

“The government should confiscate any blood diamonds, sell them and use the money for the public benefit. The people of CAR have a right to profit from their own natural resources. As the country seeks to rebuild, it needs its diamonds to be a blessing, not a curse.”

Based on interviews with miners and traders, the report details how armed groups – the Christian or animist anti-balaka and predominantly Muslim Séléka – both profit from the diamond trade by controlling mine sites and “taxing” or extorting “protection” money from miners and traders.

It also documents the inspection gaps in diamond trading centres that make it possible for blood diamonds to be traded and sold globally.

Diamond trader fails to prove due diligence

There is a high risk that the country’s biggest buyer of diamonds during the conflict, Sodiam, which has amassed a 60,000 carat diamond stockpile worth US$7 million, has purchased and is still purchasing diamonds that have financed the anti-balaka, the report said.

The UN has already black-listed second-biggest trader, Badica, and its Belgian sister company, Kardiam, for buying and smuggling diamonds from Seleka-controlled areas in the east of CAR.

In May 2015, a Sodiam representative in Carnot confirmed to Amnesty International that the company has been buying diamonds in the west of CAR despite the conflict, and keeping them until they can be exported.

The report documents the significant involvement of the anti-balaka in the diamond trade in the west of CAR. Traders who Amnesty International spoke to in that area were aware of the anti-balaka’s involvement, but none appeared to actively screen out diamonds that may have funded the armed group. One of these traders, who said it was too dangerous for security reasons to visit mine sites, showed Amnesty International receipts for sales to Sodiam. Other traders who sold to Sodiam made similar admissions to the UN.

Sodiam denies ever buying conflict diamonds. The company says that it does not buy diamonds from mines controlled by rebel groups or traders known to associate with them, but Amnesty International challenges their due diligence processes.

Amnesty International wants the CAR government to confiscate diamonds unless Sodiam and other exporting companies can prove they have not financed armed groups. Seized diamonds should be sold and the money used in the public interest.

International diamond companies must address Kimberley Process failure

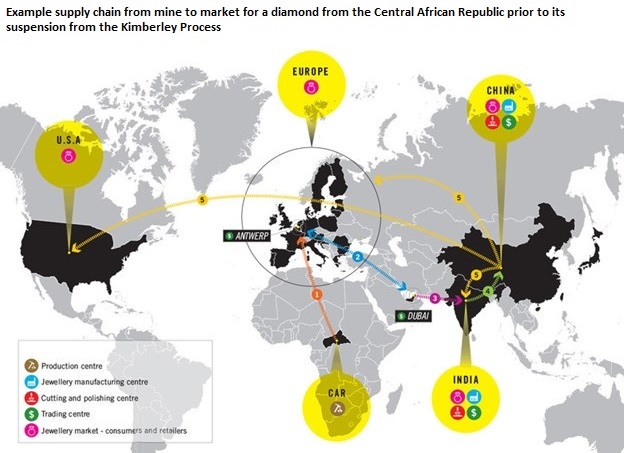

The report – which looks at several countries in the diamond supply chain, from CAR to Belgium and the United Arab Emirates – also details human rights abuses, smuggling and tax dodging throughout the diamond supply chain.

With the diamond industry due to gather at the Jewellery Industry Summit in March 2016 to discuss responsible sourcing, Amnesty

International is challenging governments and international diamond companies like de Beers and Signet to support stronger regulation of the sector. Diamond companies should be investigating their supply chains for human rights abuses, conflict and other illegal or unethical practices, and disclosing the steps taken.

“International diamond companies need to look closely at the abuses along their supply chain, from child labour to tax abuse. By focusing only on conflict diamonds, the Kimberley Process camouflages all the other human rights abuses and unscrupulous practices associated with diamonds,” said Lucy Graham.

“This is a wake-up call for the diamond sector. States and companies can no longer use the Kimberley Process as a fig leaf to reassure consumers that their diamonds are ethically sourced.”

» Download: Chains of Abuse: The global diamond supply chain and the case of the Central African Republic (PDF, 7.25 MB)

Related News

G20 urges reforms for global trade growth

G20 trade ministers on Tuesday agreed to pursue deeper and wider reforms to ensure trade growth as it grew less than the global economy for the first time in the last four decades.

“Only through a comprehensive and international trade system, this trend could be reversed and trade growth could be revived,” the ministers said in a press release issued at the conclusion of a two-day meeting in Istanbul.

Chinese Minister of Commerce Gao Hucheng stressed that China, as a country with a significant trade volume in terms of products and valuable export and import figures, is ready to contribute to the global trade growth.

“In 2016, during China’s G20 presidency, the trade growth and investment will be on top of the agenda and China is ready for cooperation to develop a comprehensive, international trade system,” Gao said at a joint press conference with Turkish Economy Minister Nihat Zeybekci.

Zeybekci also urged G20 countries to reverse the slow pace of global trade growth through implementing policies that fit the needs of the system.

“Our economies should be supported by real sector (production, growth and job creation) instead of fictional factors with inflated values, mostly based on consumption,” said Zeybekci.

Talking about the trade accord reached on Monday between 12 Pacific Rim nations, which is known as the Trans-Pacific Partnership, the Turkish and Chinese ministers spoke of cooperation through regional integrations and creation of institutional structures as means to boost the global trade.

Gao noted that when they meet in the Philippines in November, the APEC members will have a full discussion about the roadmap on a free trade area of the Asia-Pacific, a process initiated in Beijing last year.

Related News

Security bill spat: SA-US relations at risk

South Africa is in danger of being sidelined for project funding by the International Monetary Fund (IMF) and the World Bank as the US lobbies to scrap the controversial Private Security Industry Regulation Amendment Bill.

Yesterday, the US trade mission threatened to withdraw its support for South Africa’s funding applications for infrastructure development projects if certain clauses in the bill were not reviewed, and once more placed the Africa Growth and Opportunity Act (Agoa) on the back foot.

Costa Diavastos, an executive director of the Security Industry Alliance, which is spearheading the lobbying against the cession of the 51 percent stake of foreign-owned security firms to locals, said US trade officials had given an undertaking that they would revoke their support for South Africa’s loans if the amendment came through.

“US trade officials are on record saying they would not support our IMF and World Bank applications for funding,” Diavastos said at the presentation of the SA Chamber of Commerce and Industry business confidence index for September, at which the impact of the proposed bill was discussed.

In 2010, the US support proved vital to South Africa securing a $3.75 billion (R50.775bn) loan for the Medupi coal-fired power station.

But now US officials have warned that if the clause was not removed, the US government would see it as an expropriation of US property, a move that would automatically disqualify South Africa from continued participation in Agoa.

Heidi Ramsay, the deputy spokeswoman for the US embassy in Pretoria, said the US’s concerns were that the requirement would force US security firms to sell off their ownership at what would likely end up being fire-sale prices, which could effectively result in an uncompensated expropriation.

Already, South Africa is treading on very thin ice as it pushes for the lifting of the conditional access to Agoa and the restoration of full benefits.

The country missed the end of September deadline as US authorities hardened their attitudes and demanded further concessions on the bill.

Diavastos said the private security sector had invested about R4.5bn into the economy over the past eight years through mergers and acquisitions and acquisition of firms locally. He said it was an R50bn-a-year industry, employing roughly over 500 000 people.

Gordon Institute of Business Science economist Roelf Botha said the security legislation could knock R133.4bn off South Africa’s gross domestic product, R52bn off tax revenue and cost about 850 000 formal and informal jobs. Those would be the effects of the act discouraging foreign investment, losing South Africa’s duty-free access to the lucrative US market through Agoa and likely provoking trade retaliation from US and European countries.

Botha said the American Chamber of Commerce in South Africa, which represents 250 American companies in South Africa, 60 of which are Fortune 500 firms, said reasons given by the government that foreign-owned security companies were a threat to South Africa’s national security were absurd.

“There is a law in South Africa, PSIRA Act 56 of 2001, that requires that management of foreign-owned security companies are South Africans; foreign-owned security companies are registered South African companies; the security companies employ almost 100 percent South Africans and they make up less than 10 percent of the security industry in South Africa,” he said.

Related News

WTO agrees membership terms for Liberia, paving way for formal decision in Nairobi

WTO members negotiating Liberia’s accession agreed by consensus, ad referendum, on the terms of the country’s WTO membership on 6 October 2015, paving the way for the eighth least-developed country to join the organization since 1995. Liberia’s membership terms will be presented to the 10th Ministerial Conference in Nairobi, 15-18 December, for a formal decision by ministers.

Out of the original 48 least-developed countries (LDCs) on the United Nations list, 34 are WTO members, of which seven have negotiated their membership terms since 1995. Seven more LDCs are negotiating to join the WTO. They are Afghanistan, Bhutan, Comoros, Equatorial Guinea, Ethiopia, Sao Tomé & Principe, and Sudan.

WTO Director-General Roberto Azevêdo said:

“I warmly welcome this news which promises to bring a timely boost to Liberia’s economic development. I congratulate the Government of Liberia on this achievement and praise the leadership of President Ellen Johnson Sirleaf. I very much look forward to finalising Liberia’s membership at the WTO Ministerial Conference in Nairobi this December. Helping least-developed countries to trade is a vital part of the WTO’s work and is a priority for me as Director-General.”

Speaking at the Working Party meeting on 6 October, H.E. Mr Axel Addy, Minister for Commerce and Industry of the Republic of Liberia, said:

“We believe in the multilateral trading system and the power of trade to contribute to poverty reduction in our country. My dream is that the work we have done here will pave the way for a better Liberia for all of us and our children so they too can exercise their potential.”

Working Party Chairperson H.E. Joakim Reiter said:

“Liberia’s WTO accession is a strong, positive and clear signal of its commitment to engaging with the global economy in the framework of the rules-based trading system. The conclusion of this least-developed country accession is a critical win-win for LDCs, Africa and the WTO.”

Liberia’s Accession Package will now be put to the Nairobi Ministerial Conference on 15-18 December for formal adoption.

Find out more about Liberia’s WTO accession negotiations.

Related News

OECD report: Global action plan launched against MNCs avoiding tax

G20 nations announce action plan to fix gaps between tax systems in various countries

In a bid to put an end to tax avoidance by multinational companies, a global action plan was announced in Paris on Monday. Developed over the last three years by the Organisation of Economic Cooperation and Development (OECD) at the behest of G20 nations, the Base Erosion and Profit Shifting (BEPS) project, has brought together 60 countries, including India.

BEPS has become a serious problem as gaps between tax systems in different countries are exploited by multinational enterprises to make profits ‘disappear’ or shift to low tax jurisdictions and tax havens. Tax planning has turned into core business for many companies and practices such as transfer pricing are catered to by an entire industry. Globalisation and digital economy exacerbate this problem and international tax rules designed to prevent double taxations have ended up facilitating double non-taxation as well. BEPS lead to annual national revenue losses from 4-10 per cent of global corporate income tax revenues, i.e., $100-240 billion annually, according to a research conducted by OECD since 2013.

These new measures intend taxing enterprises “where economic activities take place and where value is created.” Model provisions have been developed to prevent treaty abuse, including through treaty shopping for which a number of countries work like hubs. Transfer pricing rules have been reinforced, according to the OECD.

This set of 15 measures will be introduced for the renovation of international tax standards and will be presented to and are likely to be adopted by the G20 Finance Ministers on the October 8 in Lima. The instrument will be open for signature to all interested countries in 2016 for information exchange to start from 2017-18. According to OECD, there is large scale consensus for these treaties.

MNEs such as Amazon and Starbucks have announced tax policy shifts to fall in line with BEPS. It’s being hailed as “the most significant rewrite of the international tax rules in a century”. But critics say BEPS will fail to reach the stated objective of ensuring that multinational corporations pay their taxes ‘where economic activities take place and value is created’.

| BEPS AT A GLANCE |

|

“There will be some amount of strengthened cooperation and more information about what’s going on for tax administrations in OECD and G20 countries,” Tove Ryding of Eurodad, a network of 46 NGOs from 20 European countries, told Businesss Standard. “But this action plan doesn’t abolish patent boxes, in fact, it legitimises their use; there’s no agreement on the use of the profit-split method; transfer pricing guidelines are turning more and more complex and the outcome on country by country report is weak,” said Ryding. He feels the lack of clarity in rules is likely lead to an increase in conflicts between tax administrations and multinational corporations. India had earlier said mandatory binding arbitration to resolve tax treaties disputes will impinge on its sovereign rights.

Experts groups say the rich country group OECD is not the appropriate body to set tax cooperation rules and a new global body which offers equal representation should be formed.

Related News

tralac’s Daily News selection: 6 October 2015

The selection: Tuesday, 6 October

World Bank/IMF 2015 Annual Meetings: A guide to webcast events, Event: State of the Africa region, AfDB delegation to strengthen alliances at 2015 Annual Meetings

Africa’s Pulse: October 2015 (World Bank)

The 2015 forecast remains below the robust 6.5% growth in GDP which the region sustained in 2003-2008, and drags below the 4.5% growth following the global financial crisis in 2009-2014. Overall, growth in the region is projected to pick up to 4.4% in 2016, and further strengthen to 4.8% in 2017. Africa’s Pulse notes that overall decline in growth in the region is nuanced and the factors hampering growth vary among countries. In the region’s commodity exporters - especially oil-producers such as Angola, Republic of Congo, Equatorial Guinea, and Nigeria, as well as producers of minerals and metals such as Botswana and Mauritania, the drop in prices is negatively affecting growth. In Ghana, South Africa, and Zambia, domestic factors such as electricity supply constraints are further stemming growth. In Burundi and South Sudan threats from political instability and social tensions are taking an economic and social toll. [Download]

Companion, regional perspectives from the World Bank: South Asia Economic Focus, East Asia Pacific Economic Update, Jobs, wages, and the Latin American slowdown

Sub-Sahara Africa gets over $7.4bn of financing from World Bank (GBN)

Ibrahim Index 2015: Banks and customs procedures indicators

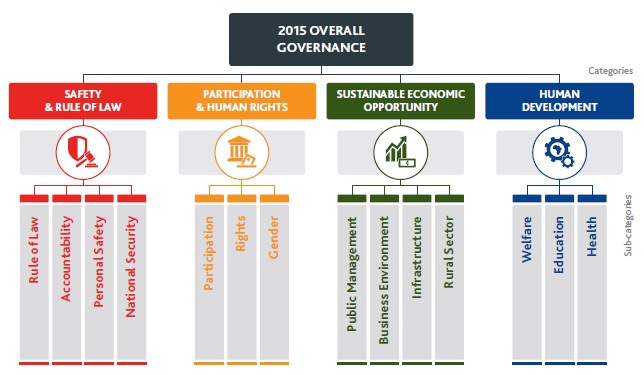

The indicators that are contributing the most to declines in Public Management and Rural Sector are Ratio of External Debt Service to Exports (-3.4) and Agricultural Policy Costs (-5.7) respectively. However Business Environment has shown the most concerning trend, exhibiting the most deteriorated score of any sub-category in the IIAG since 2011 (-2.5), having shown a year-on-year deterioration for four consecutive years. This trend has been largely driven by the two most deteriorated indicators in the IIAG, at the African average level: Soundness of Banks (-11.0) and Customs Procedures (-9.0). These are both concerning. Reliable financial institutions are the foundation of any growing economy – if people are losing trust in African banks, then sustainable economic growth is more remote than ever. Efficient customs, meanwhile, is absolutely essential for trade across African borders. The African Union thinks intra-African trade is fundamental to Africa’s economic future, and it’s not a good sign that, despite the continental body’s efforts, customs procedures are getting worse instead of better. [Various downloads available]

Nairobi MC10: submission by the G-33 (WTO)

We, the G-33 members, strongly renew the long-standing calls for global trade reforms that address inequities and imbalances in the Uruguay Round Agreement on Agriculture so that all WTO Members would be governed by a multilateral trading system under the WTO which is not only open, transparent, and market-oriented but also, more importantly, development-oriented, fair and provides a level playing field.

Amid uncertain outlook for farm talks, WTO members consider the 'Nairobi Package' (WTO)

Ambassador Vitalis gave a detailed account of the status of the four inter-related elements of the agricultural negotiations. These are: 1) domestic support; 2) market access; 3) export competition; and 4) cotton. He also updated members on the separate talks regarding public stockholding for food security purposes. He reported “a very serious situation” in both the domestic support and market access pillars of the agricultural negotiations. “In fact, in my summing up of both discussions I drew the obvious conclusion: that the failure to find convergence in domestic support and market access has wider implications and these are not positive”.

Kenya's @AMB_A_Mohammed yesterday tweeted a series of comments following her meeting with G7 trade ministers: view her TL

The African Union Commission and its technical office, IBAR, have supported the training to improve the quality and effectiveness of participation of African member States in the activities of the WTO SPS Committee. The specific training objectives were to:

Trans-Pacific Partnership - selected updates: Technical summary of the agreement (DFAIT Canada), Obama finally gets the TPP, a massive trade deal covering 40 percent of the world’s economy (Foreign Policy), In Pacific trade deal, Australia gets bigger US sugar allocation (Reuters), DG Azevêdo congratulates TPP ministers (WTO), China expresses hesitant support for the Trans-Pacific Partnership (TIME)

African Grain Trade Summit concludes with clear commitments towards structured grain trade (EAC)

The summit ended with recommendations from the delegates who fronted for a private sector-led Action Group that would champion the identification of key issues and to drive policy engagement with governments to ensure the grain sector thrives. Regional harmonization of trade policies among countries and among regional economic blocs, was supported unanimously by the delegates. The Eastern Africa Grain Council was tasked to drive the regional trade harmonization agenda, including policies on Warehouse Receipting Systems, Post-harvest Management, storage systems and technologies that support regional trade. The summit also brought together, for the very first time, the Eastern Africa Grain Council, the Southern Africa Grain Network and the West Africa Grain network, where it was agreed on the need of collaboration on Marketing Information and Capacity Building. The delegates further agreed to the formation of the African Grain Council (AGC).

Policy, not technical challenges, is the real hurdle for smallholder farmers, says civil society (UNCTAD)

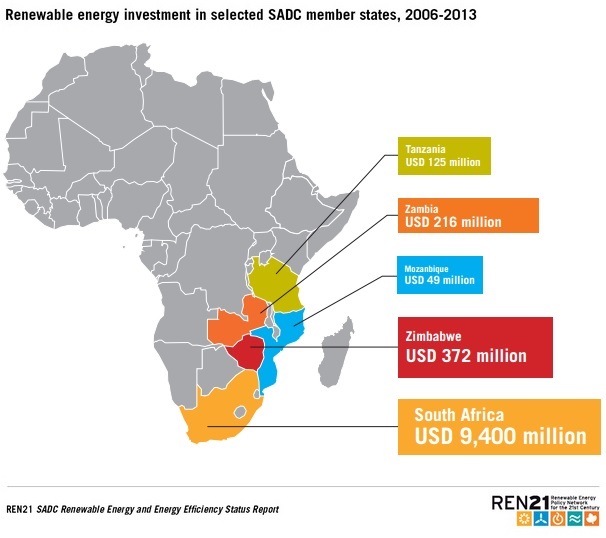

The SADC Renewable Energy and Energy Efficiency Status Report (REN21)

The Southern African Development Community is one of the oldest regional economic communities on the African continent. The region is now becoming a key player in the international trend towards development of renewable energy resources and energy efficiency. However regional challenges persist particularly around energy access, health and environment, energy security, infrastructure and financing. The SADC Renewable Energy and Energy Efficiency Status Report provides an comprehensive overview of where the opportunities and challenges lie for meeting the region’s need for accessible, clean and sustainable energy. As with other REN21 reports, it is for policymakers, industry, investors and civil society to make informed decisions with regards to the diffusion of renewable energy. By design, it does not provide analysis or forecast.

Synergising and optimising mineral infrastructure in regional development strategies (E15 Initiative)

The purpose of this paper is to explore the potential of mineral infrastructures as “anchors” for economic development and cross-border cooperation. It proposes some policy recommendations to make better use of existing frameworks to foster the utilisation of mineral infrastructures. It also points out that in some cases, rules may not be the most appropriate way to stimulate broader economic development out of resource infrastructures. Sometimes incentives and strategic partnerships are more efficient and effective ways to realise certain objectives. [The author: Isabelle Ramdoo]

EAC seeks 'common borders' for education (New Times)

The East African Community is looking into the adoption of a common education protocol to ease movement of learners and teachers within the region. Regional experts behind the plan say the creation of a common EAC Higher Education Area (EACHEA) implies that qualifications will be appropriately recognised in all partner states both for continuation of studies as well as in the labour market. When the EAC is declared as an EACHEA in November, according to Prof. Mayunga Nkunya, the executive secretary of the Inter-University Council for East Africa, the most important development will be the elimination of the disparity in the national education systems. “And I must say that we are the first region in Africa to have devised this kind of system. Once operational, all these challenges which we are seeing in movement of students from one partner state to another will end.”

Zimbabwe: Exports to SA down 37% (The Herald)

According to the latest trade data from ZimStat, Zimbabwe exports to its neighbour were down 37,3% to $86,3m in August from $137,6m, while imports from South Africa climbed 5,4% from $189,3m to $199,6m. The weakening rand has made imports from South Africa land much cheaper in Zimbabwe. This is despite the policy measures, meant to curb imports, introduced by Government at the Mid Term Fiscal Policy Review. Zimbabwe’s trade deficit for August stood at $316,2 million from $291,4m recorded in July this year. This represents an increase of 8,5% from the July figures. Overall Zimbabwe’s trade deficit for the year to August 2015 now stands at $2,02bn reflecting the over dependency on imports and the decline in exports as the local economy continues to be hamstrung by capacity constraints and lack of competitiveness. [Zimtrade to tackle trade facilitation issues (The Herald)]

Swaziland: IMF completes 2015 Article IV Mission (IMF)

The mission encourages the authorities to step up efforts to raise the country’s potential for inclusive growth in order to address social and economic challenges. To this end, the mission recognized that the loss of AGOA eligibility raises the importance of enhancing economic diversification and competitiveness. To this end, the mission highlights the importance of fast-tracking policy efforts in multiple areas to promote export diversification (through private sector development), enhance access to financing, and improve the business climate.

Uganda: IMF staff completes review mission (IMF)

Rwanda: Ministry of Trade and Industry improves export base (New Times)

Côte d’Ivoire: Support to industrial competitiveness enhancement project (AfDB)

Regional Oversight Mechanism for DRC and the Great Lake Region: update (SADC)

HPCL seeks Mozambique gas for Gujarat LNG terminal (LiveMint)

Global Forum on Competition: Does competition kill or create jobs? Contribution from CUTS

Given the above, the international competition fraternity and indeed national policymakers need to explore ways in which fair markets influence jobs – especially in the developing world. As an advocate of competition reforms across the developing regions of the world, CUTS presents its views on the linkage between competition and employment, under the following three heads especially relevant for developing countries like India:

Competition policy within the context of Free Trade Agreements (E15 Initiative)

OECD/G20 BEPS Project for discussion at G20 Finance Ministers meeting (OECD)

The OECD presented the final package of measures for a comprehensive, coherent and co-ordinated reform of the international tax rules to be discussed by G20 Finance Ministers at their meeting on 8 October, in Lima, Peru. The OECD/G20 Base Erosion and Profit Shifting (BEPS) Project provides governments with solutions for closing the gaps in existing international rules that allow corporate profits to ‘disappear’ or be artificially shifted to low/no tax environments, where little or no economic activity takes place. Revenue losses from BEPS are conservatively estimated at USD 100-240bn annually, or anywhere from 4-10% of global corporate income tax revenues. Given developing countries’ greater reliance on CIT revenues as a percentage of tax revenue, the impact of BEPS on these countries is particularly significant.

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome. Richard Humphries (Email: This email address is being protected from spambots. You need JavaScript enabled to view it.; Twitter: @richardhumphri1)

Related News

Reaffirming development: MC10 Nairobi and Post MC10 Nairobi – Submission by the G-33

We, the G-33 members, strongly renew the long-standing calls for global trade reforms that address inequities and imbalances in the Uruguay Round Agreement on Agriculture (AOA) so that all WTO Members would be governed by a multilateral trading system (MTS) under the WTO which is not only open, transparent, and market-oriented but also, more importantly, development-oriented, fair and provides a level playing field.

Developed Members have expansive flexibilities in the AOA which make their farmers and exporters artificially competitive. These flexibilities include, amongst others, huge and high ceilings in trade-distorting subsidies in both production and exports; non-transparent and complex TRQ and tariff systems including tariff peaks and escalations; as well as the highest entitlements to the special safeguard provisions (SSG). Considering these flexibilities, developing Members’ tariffs have not been able to match these wide-ranging flexibilities enjoyed by developed Members and increase their levels of competitiveness and the capacity needed to compete in a market of fair competition.

In order to continue the fundamental reform in agriculture and to address the inequities and imbalances, our Ministers in the Uruguay Round inscribed the “built-in” agenda under Article 20 of the AOA. The agenda has been carried through and further reinforced by the Doha Development Agenda (DDA) in 2001 (WT/MIN(01)/DEC/1) which puts “development” and special and differential treatment (S&DT) for developing Members at its core.

The objectives enshrined in the DDA can only be achieved once all the elements of the agriculture negotiations have a comprehensive and development-oriented outcome. Until the same is achieved we firmly believe that the negotiations must continue towards and after the 10th Ministerial Conference (MC10) Nairobi, building on the various Ministerial decisions/declarations and the development framework we have agreed to date since 2001.

The Group is willing to engage constructively and contribute to a credible and balanced outcome, which withstands the test of development at MC10 Nairobi and beyond.

As part of the balancing and S&DT instruments, the G-33 has long been calling for meaningful Special Products (SP) and an accessible and effective Special Safeguard Mechanism (SSM). These tools are needed for sustaining investments in agriculture for food security, livelihood security and rural development, as well as addressing the destabilizing and crippling effects of import surges and downward price swings in the increasingly volatile global agricultural markets largely due to huge subsidies in productions and exports by the developed Members.

Also the Group firmly believes that there should be a permanent solution on public stockholding for food security purposes as mandated.

Related News

Ibrahim Index 2015: ‘Governance progress in Africa is stalling’

How well is your country governed? This is the question the Ibrahim Index of African Governance seeks to answer. This year’s results are bad news for the continent as a whole, and South Africa specifically. But what’s going right in Zimbabwe?

Sudanese billionaire Mo Ibrahim believes most of Africa’s problems are rooted in poor governance, and there are few who would disagree with him. He also believes that governance can and should be measured, accurately and objectively, and that critiques and policy should be based on numbers rather than conjecture. To this end, he created the Ibrahim Index of African Governance (IIAG), which is now in its ninth iteration.

The 2015 edition – which includes South Sudan for the first time, as there is now enough data for Africa’s newest country – reveals a continent in governance limbo, with no overall improvement or decline. This headline statistic masks plenty of activity at country and category level, however – some of it surprising. We’ve trawled through the data to find the most interesting trends.

African governance is stagnating

This is the major takeaway from this year’s results. “The results of the 2015 IIAG reveal that overall governance progress in Africa is stalling. Improvements in (index categories) Participation & Human Rights and in Human Development are outweighed by deteriorations in Safety & Rule of Law and Sustainable Economic Opportunity,” said Ibrahim.

Should we be concerned? Absolutely. The Mo Ibrahim Foundation is desperate not to reinforce negative stereotypes of Africa, which makes this a particularly painful admission – there are few stereotypes more prevalent than that of poor African leadership, and this data will prove many an Afro-pessimist’s point.

Which is why Ibrahim is at pains to stress that this overall trend does not tell the whole story. “Africa is not a country. The scores and trends seen in the 54 individual countries on the continent are diverse, each showing specific patterns in their own right, along a wide range of results, with more than a 70-point gap between the top-ranking country, Mauritius, and the bottom-ranking country, Somalia,” he said.

The star performers

Over the last four years, only six countries improved across all four Ibrahim Index categories. These star performers are: Cote D’Ivoire, Morocco, Rwanda, Senegal, Somalia and Zimbabwe. An interesting mix which includes democracies, dictatorships, a monarchy and a conflict zone – in other words, no matter what the ideologues may tell you, there are several different formulas for better governance in Africa.

Côte d'Ivoire deserves a special mention, showing by far the greatest overall improvement. Credit for this must go to President Alassane Ouattara’s government, who have done a decent job of imposing stability following the 2010-2011 political crisis.

What’s going right in Zimbabwe?

It’s hard to ignore Zimbabwe’s presence in the top six improvers. In fact, it has shown the second largest overall governance improvement since 2011 – an uncomfortable statistic for President Robert Mugabe’s many critics, and one which will no doubt be trumpeted on the front page of The Herald come Tuesday morning.

Drill down a little further, and the data is even more puzzling. Zimbabwe’s biggest category-level improvement came in Participation & Human Rights, with strong showings in the sub-categories of Rights and Gender. The country also did well in National Security, Personal Safety, Public Management and Infrastructure, Welfare and Health (it helps, of course, that the country is coming from such a low base).

For the Mo Ibrahim Foundation, results like these are potentially embarrassing, but also demonstrate the utility of the Ibrahim Index: like it or not, some things have improved in Zimbabwe over the last few years, probably as a result of increased political stability, and here are the numbers to prove it.

South Africa papers over the cracks

South Africa is the fourth-best-governed country in Africa, behind only Mauritius, Cape Verde and Botswana. The good news is that we’ve maintained that position for years, and are even showing small signs of overall improvement (up 0.9 points since 2011, although this is well within the margin of error).

But the devil is in the details. Our high ranking conceals some concerning trends at sub-category level, in particular our exceptionally poor performance in Personal Safety and National Security. For its citizens, South Africa is still an unacceptably dangerous country.

More surprising is the deterioration in the Participation & Human Rights category, driven by declines in the Gender and Rights sub-categories. Specific indicators showing significant declines include Freedom of Association & Assembly, Freedom of Expression, and Legislation on Violence Against Women.

While these have yet to affect South Africa’s overall governance performance, it’s clear that these declines are the canaries in the coal mine – and should provide further evidence, if any was needed, that all is not well in the Rainbow Nation.

Banks and customs

Across the Ibrahim Index’s 93 indicators, the two showing the biggest decline over the last four years are Soundness of Banks (-11 points) and Customs Procedures (-9 points). These are both concerning.

Reliable financial institutions are the foundation of any growing economy – if people are losing trust in African banks, then sustainable economic growth is more remote than ever. Efficient customs, meanwhile, is absolutely essential for trade across African borders. The African Union thinks intra-African trade is fundamental to Africa’s economic future, and it’s not a good sign that, despite the continental body’s efforts, customs procedures are getting worse instead of better.

The biggest losers

No surprises that the biggest declines in governance in the last few years come from war zones. South Sudan, the Central African Republic and Mali fare particularly poorly. The lesson here is crushingly obvious, but is worth repeating anyway: conflict remains the biggest impediment to good governance in Africa.

Foreword

The 2015 Ibrahim Index of African Governance (IIAG) is the 9th iteration since we launched in 2007. The IIAG has been refined and strengthened each year since then under the guidance of the Board of the Foundation, the IIAG Advisory Council, and our friends and partners, to all of whom I wish to extend our thanks and gratitude.

The results of the 2015 IIAG reveal that overall governance progress in Africa is stalling. Improvements in Participation & Human Rights and in Human Development are outweighed by deteriorations in Safety & Rule of Law and Sustainable Economic Opportunity. Over the last four years, only six countries out of 54 were able to achieve progress in all four components of the Index. If we drill down a little further, to sub-category level, gains achieved in Participation, Infrastructure or Health are of course heartening, but the drops registered by National Security, Rural Sector, and, most of all, Business Environment, are cause for concern.

However, Africa is not a country. The scores and trends seen in the 54 individual countries on the continent are diverse, each showing specific patterns in their own right, along a wide range of results, with more than a 70 point gap between the top ranking country, Mauritius, and the bottom ranking country, Somalia. The 2015 IIAG results also point to a shifting landscape. Over the last four years, half of the top ten performing countries have registered a decline of their governance performance. Meanwhile, half of the ten largest improvers over this period include countries which already rank in the upper rungs of the Index, and may well be potential powerhouses.

2015 is a milestone year for Africa. The future African landscape will be defined by the new Sustainable Development Goals, which are meant to guide us for the next 15 years, and the decisions that will come out of COP21. What is crucial is that the complexity of Africa is appreciated within these discussions, that the decisions made are based on data and sound information and that their implementation will be closely monitored according to results.

In that context, my hope is that this Index can be a useful tool.

Key findings of the IIAG 2015 include:

-

The African average score for overall governance in 2014 is 50.1, a slight improvement since 2011 (+0.2). Over the last four years, only half of the top ten governance performers managed to improve their overall governance score, and 21 of the 54 countries have deteriorated.

-

The Sustainable Economic Opportunity category exhibits both the lowest continental average score (43.2) and the largest performance drop since 2011 (-0.7). Sustainable Economic Opportunity includes the most deteriorated sub-category in the IIAG since 2011, Business Environment (-2.5). This sub-category includes the most deteriorated indicator in the IIAG over this time period, Soundness of Banks (-11.0).

-

Among the generally negative trend of the Sustainable Economic Opportunity category, four countries, Morocco (+11.2), Togo (+9.5), Kenya (+5.9) and Democratic Republic of Congo (+5.4), exhibit impressive gains of more than +5.0 points.

-

The overall governance score range between the best regional performer, Southern Africa, and the poorest regional performer, Central Africa, is more than 18.1 points in 2014. This has widened by +1.7 points since 2011.

-

With a 79.9 score for overall governance in 2014, Mauritius stands over 70 points higher than the continent’s weakest governance performer, Somalia, which achieved a score of 8.5.

-

The top three countries, Mauritius, Cabo Verde and Botswana, all exhibit a decline in overall governance and in at least two of the four components over the last four years, calling into question whether these countries will continue to dominate the top of the rankings in future.

-

The bottom three countries in overall governance are Central African Republic (24.9), South Sudan (19.9) and Somalia (8.5). Two of these, South Sudan (-9.6) and Central African Republic (-8.4), have also registered the most extreme deteriorations, along with Mali (-8.1).

-

The top ten improvers in overall governance over the last four years represent almost a quarter of the continent’s population. Five of these countries, Senegal (9th), Kenya (14th), Morocco (16th) Rwanda (11th) and Tunisia (8th), already rank in the top 20 of the IIAG, leading to the question of whether they might become the continent’s next powerhouses.

Related News

Amid uncertain outlook for farm talks, WTO members consider the “Nairobi Package”

The Chair of the agriculture negotiations, Ambassador Vangelis Vitalis of New Zealand, updated WTO members on the current state of the negotiations on 2 October at a meeting open to all members. “Unfortunately, the areas of divergence remain and our challenge is to see what is still possible to narrow the gaps and precisely where,” he told members.

Ambassador Vitalis gave a detailed account of the status of the four inter-related elements of the agricultural negotiations. These are: 1) domestic support; 2) market access; 3) export competition; and 4) cotton. He also updated members on the separate talks regarding public stockholding for food security purposes.

He reported “a very serious situation” in both the domestic support and market access pillars of the agricultural negotiations. “In fact, in my summing up of both discussions I drew the obvious conclusion: that the failure to find convergence in domestic support and market access has wider implications and these are not positive”.

On export competition – an area of the farm talks that many see as a possible key element in any Nairobi package – the Chair said that despite the perception of less divergence in this pillar, “there is not a consensus on the overall contours of such a package, let alone its precise content nor indeed how this might relate to what happens after Nairobi.”

The Chair highlighted cotton as a priority issue for Nairobi, citing the need to engage in a more focused negotiation on what could constitute a possible outcome in relation to export competition, market access and domestic support. The Bali ministerial decision on cotton stresses the need to level the playing field for cotton producers in developing countries, especially in impoverished African regions.

Finally, on public stockholding for food security purpose, Ambassador Vitalis said he would continue to consult widely on this matter and intended to hold a separate process on public stockholding in the coming weeks.

The Chair invited members to express views on the possible outcomes at the Nairobi conference.

Noting the limited time before Nairobi, many members underlined the need to focus on a smaller package. There is a shared sense that export competition is more mature and stabilized than other areas. Positive trends were noted in members’ export-related policies as reflected in an earlier Secretariat report (G/AG/W/125/Rev.3). This is in particular the case with export subsidies, which have fallen to zero, with the exception of a few members.

Other issues mentioned as possible outcomes for the Nairobi conference include the Special Safeguard Mechanism (SSM) – a mechanism for developing countries to temporarily raise import tariffs in response to import surges or price falls. Many developing members maintain that the SSM would help to protect farmers suffering from subsidies by big players, citing that the mechanism was agreed in principle in the Hong Kong Ministerial Declaration. Opponents of the proposal, however, noted that distortions in agricultural trade should not be fought with more distortions.

Some members also listed elements in all three pillars of the agriculture talks, referring to ‘Rev 4’ (the 4th revision of agricultural modalities in July 2008), as important issues to be considered. Many reiterated that the work on removing domestic support and reducing trade barriers in the agricultural sector should not stop after Nairobi. The least developed countries (LDC) group informed members they are working on a proposal of specific issues of interest to LDCs – likely to be submitted by the end of the month – to be considered for the Nairobi conference.

In conclusion, the Chair said that members understood the centrality of agriculture and development to the wider negotiations and that there was agreement on the need to secure an agriculture outcome for Nairobi, even if there was no consensus yet on precisely what this might look like. He said there was a shared sense of urgency about the process given the limited time remaining before the WTO’s Tenth Ministerial Conference in Kenya.

The Chair further observed with regret, however, that he had not heard much that was particularly new on most of the issues considered by members in the informal session of the agriculture negotiations. Notwithstanding this, Ambassador Vitalis did observe that the exchanges on 2 October had confirmed a shared sense that the issue of export competition was both the most stable and mature of the issues under negotiation at this point. This was encouraging, he said.

Taken together, the Chair indicated that he intended to proceed by intensifying consultations with all members, recalling that the WTO could not be a “Melian Dialogue” – it had to be a fully inclusive and transparent process. In this regard, the Chair expected work to proceed with members across the entire suite of agriculture-related issues ahead of Nairobi, including in particular on export competition. In terms of the latter element, Ambassador Vitalis commented that the forward process would be shaped and informed by members’ views on the key issues through a “define by doing” approach. More broadly, the Chair underlined and welcomed the commitment of members to redouble and intensify their efforts over the coming weeks ahead of the Nairobi conference.

Earlier, in a briefing on 17 September, Director-General Roberto Azevêdo called for more clarity from members “by mid to end of October” in order to prepare the ground for a successful ministerial conference. “Given the very limited time left before the Ministerial and the sombre account the DG provided of the current state of negotiations”, the Chair told the members, “I share the DG’s view that there is an urgent need for more clarity on what can be done – or cannot be done – before Nairobi. We need to reach an understanding of what is realistic in the time we have and we clearly have no time to waste.”

Chair’s assessment of the current negotiations

Domestic support

-

During the meeting on domestic support on 23 September, one member introduced ideas that had already been shared with some members in early September and subsequently outlined during a meeting on 17 September.

-

That proposal combined some non-binding commitments with limited binding commitments on certain types of trade distorting domestic support, such as market price support and input subsidies.

-

It’s fair to say that these ideas provoked diverse reactions from members. Some of you welcomed them with interest. Others made it clear that these ideas were not a basis for forward movement.

-

If I may summarise, there appeared to me to be five specific issues identified in our discussions. These included a perception that the ideas presented: 1) may constrain developing countries’ flexibilities and notably the use of their de minimis; 2) failed to distinguish between commercial and subsistence farmers; 3) targeted two programmes some developing countries are using the most; and 4) have an impact on the public stockholding debates; 5) imply that two specific programmes were considered more trade distorting than others.

-

Several members, while showing a readiness to discuss new ideas, indicated their preference for limiting trade distorting support in general, and/or for the OTDS (overall trade distorting domestic support) concept in particular.

-

Some members said they were ready to work with the AMS (Aggregate Measurement of Support) concept.

-

Other members focused on Rev.4 in particular, stating that this was “the most promising/viable starting point”.

-

Some of you expressed an interest in transparency-related issues, with at least one member suggesting an exploration of the monitoring and transparency provisions (as per Annex M of Rev.4) as a potential deliverable for Nairobi.

-

And, finally, in light of a possible nil outcome in domestic support, the question of the post-Nairobi scenario has become an increasingly important matter for many of you – indeed some of you suggested this is an urgent issue to clarify.

-

In short, my conclusion was that points of disagreement – and some of these were sharp-edged – far outweighed the points of agreement.

-

On the positive side, I heard an agreement about the importance of the domestic support pillar, and that the WTO remains the only place where it can be dealt with. There was a sense too that agriculture and development are closely related. There was widespread agreement too that Nairobi should include an outcome on agriculture. There was also a shared understanding that even after the Nairobi Ministerial we would need to work on this.

-

Unfortunately, members disagreed on pretty much everything else. There was, for instance, no agreement on new ideas, nor was there agreement on what I called the “not so new ideas”, nor indeed on the way forward. Nor was there agreement on how to move forward on domestic support.

-

As to the post-Nairobi agenda, notwithstanding the sense that domestic support would need to be focused on after Nairobi, there was certainly no agreement on how precisely this would be done and what the architecture of this would look like.

-

Put simply, we are far from agreeing on the content or the contours of an outcome in domestic support. Unless I hear something new or different today – and I do hope I do (I am an optimistic person from the New World after all), we are certainly going to need to confront directly an existential question in the area of domestic support.

Market access

-

Turning to market access, in my consultations on Monday (28 September) I invited members to share any new thoughts or contributions that could make a difference and help us to move forward on this pillar of the negotiations.

-

I regret to report back to you that it’s clear from these consultations that we are still faced with largely the same questions that have bedevilled our process for some time now.

-

Let me start with the points of agreement. There was agreement that agricultural market access mattered. There was also agreement that we have a limited amount of time to deliver an outcome for Nairobi in this area. There was also agreement that the failure to secure an outcome on market access for agriculture would have wider implications for the negotiations – and a sense that those implications were negative. Those were the points of agreement.

-

Unfortunately the points of disagreement were considerable.

-

There were serious question about our shared level of ambition, with on the one hand calls for what some members called “realism” while on the other hand, there was an insistence on bearing in mind the development aspects of this pillar and therefore calling for high ambition in tariff reductions.

-

There were a wide range of views of how and even whether to address other market access elements already discussed in these negotiations.

-

On this list of issues you raised, there were references to minimum cuts, tariff escalation and tariff capping provisions, safeguards, including the SSM, tropical products, tariff rate quotas, special and sensitive products, and specific provisions for special and differential treatment.

-

It is clear to me that many, if not necessarily all of these, remain firmly on the agenda for some countries, while equally some, if not necessarily all of these, were equally firmly rejected – or set within the context of the overall process of the negotiations, noting in particular the lower ambition.

-

More specifically, I heard a range of views about tariff reduction approaches, but again there was certainly no convergence apparent on any one approach.

-

Some members suggested particular elements that could be addressed regardless of what level of ambition was chosen, but others were not prepared to consider these in the absence of possible, let alone meaningful, tariff reductions.

-

As in domestic support, therefore, both the content of a possible market access outcome and the contours of such an outcome are very unclear.

-

With respect to discussions relating to what would be possible for Nairobi and post-Nairobi, it’s safe to say by the end of the consultations that we are no closer to reaching a common understanding on this.

-

My question of how to strike the optimal balance between ambition and political viability, in the context of a low ambition outcome in this pillar, remains unanswered.

-

And again, as with domestic support, members – I believe – face an existential moment on market access for agricultural products.

Export competition

-

On export competition, I have started consulting with a number of delegations and these contacts are continuing. I will progressively broaden the scope of my consultations.

-

I know that some of you consider this pillar as a possible key element in any Nairobi package.

-

That may well be the case, but I must be very clear that there is not a consensus on the overall contours of such a package, let alone its precise content nor indeed how this might relate to what happens after Nairobi.

-

I am very conscious of these inter-related elements. Indeed, be assured that I have heard these diverging views. These have helped me frame, shape and inform the way I have conducted and will conduct my consultations on this pillar.

-

Let us be honest, however, this divergence does not make our task easier. Let us also be frank with one another that there are also issues within the pillar itself that we will need to grapple with.

-

Some of you have raised questions about the internal balance of any outcome. And then there is the question of the “external balance” across the wider negotiation.

-

And that is notwithstanding the fact that this element has been considered as more mature than the two others and that at least on this pillar we have a well-developed text to work from.

-

These divergences exist – but at the same time, I sense a willingness to see what may yet be possible – a kind of “define by doing” approach at least as we take this forward.

-

In my continuing consultations therefore my objective will be to identify with you the precise scope of the remaining issues and work towards agreed formulations for dealing with these.

-

I will be looking for opportunities to engage in broader consultations in a variable geometry format, including formats like this one as we head towards Nairobi.

Cotton

-

Let me be both clear and up front on this issue. Cotton remains a priority issue for Nairobi.

-

As noted by my predecessor in July, we need to engage in a much more focused negotiation on what could constitute a possible outcome on cotton in relation to export competition, market access and domestic support. I have made it clear that I share John’s assessment and am proceeding on that basis.

-

During my first round of consultations, I therefore asked very directly some of the key interested members and, in particular of course the Cotton-4 members, to detail as specifically as possible their views on what could constitute such an outcome on cotton, taking into account the overall negotiation context.

-

My intention is to intensify my consultations on cotton in the coming weeks.

Public stockholding

-

I continue to consult widely on this matter and I understand the importance some members attach to this, noting also the divergent views on the process going forward.

-

As I noted earlier I do intend a separate process on public stockholding and I expect to hold a meeting on this in the coming fortnight or so.

Conclusion

-

Taken together, I have given you a sense of where matters stand in the consultations on the agriculture components. I have explained 1) the process, 2) the context and 3) the substance of the consultations thus far, including in some detail on all of the areas we are working on collectively.

-

Unfortunately, the areas of divergence remain and our challenge is to see what is still possible to narrow the gaps and precisely where.

-

As I noted at the outset, these kinds of open-ended consultations matter – this negotiation is, as I have already said no Melian Dialogue. Today is another opportunity for all members – all members – large and small, developed, developing and LDCs to consult, discuss and engage with one another and to help inform and guide my process as Chair going forward.

-

I look forward to hearing from you today on your assessment of where we are at, including in particular on the possible outcomes for Nairobi.

Related News

Drop in global commodity prices, electricity bottlenecks, and security risks slow Africa’s economic growth

As difficult global conditions combined with domestic challenges buffet many African countries, Sub-Saharan Africa’s economic growth will continue to slow in 2015 to 3.7 percent from 4.6 percent in 2014, according to new World Bank projections.

The end of the commodity price super cycle − with a substantial drop in the price of oil, copper and iron ore − a slowdown of the Chinese economy, and tightening global financial conditions underpin the deceleration in growth, according to the World Bank’s latest Africa’s Pulse, the twice-yearly analysis of economic trends and the latest data on the continent.

The anticipated 2015 growth in GDP marks the lowest growth rate in Sub-Saharan Africa since 2009, and falls below the robust annual 6.5 percent growth in GDP that the region sustained in 2003-2008, the report notes. “The good news is that domestic demand generated by consumption, investment, and government spending will nudge economic growth upwards to 4.4 percent in 2016, and to 4.8 percent in 2017,” said Punam Chuhan-Pole, Acting Chief Economist, World Bank Africa Region and Author of Africa’s Pulse.

Countries Buck the Trend

The analysis points out that some countries in the region are bucking the weakening regional trend and continuing to post robust growth. For example, Cote d’Ivoire, Ethiopia, Mozambique, Rwanda and Tanzania are expected to sustain growth at around 7 percent or more per year in 2015-17 due to investment in large-scale projects in energy and transport, consumer spending, and investment in the resource sector.

More broadly, economic activity will pick up in 2016-2017 as commodity prices make a slow recovery, fiscal consolidation eases, and governments take steps to alleviate power supply bottlenecks.

In a special analysis, Africa’s Pulse examined the region’s policy response to the global downturn in 2008-09, with an eye to discovering whether countries have the adequate macroeconomic policy space to withstand new, rising external headwinds that affect their economic growth.

When the global financial crisis hit the region, some countries were able to use government investment in infrastructure and other built-in buffers to finance policy responses to enable growth. Overall, the analysis shows that before the current bout of global difficulties these policy buffers were already showing signs of vulnerability from overvalued currencies and growing fiscal deficits. Today, these policy buffers are lower than before the global financial crisis, according to the report, and will make it more difficult for countries to grow in the current situation.

Gains in Poverty Reduction

Africa’s Pulse found that progress in reducing income poverty in Sub-Saharan Africa has been occurring faster than previously thought. According to World Bank estimates poverty in Africa declined from 56 percent in 1990 to 43 percent in 2012. At the same time, Africa’s population saw progress in all dimensions of well-being, particularly in health (maternal mortality, under-5 mortality) and primary school enrollment, where the gender gap shrank.

Yet African countries continue to face a stubbornly high birth rate, which has limited the impact of the past two decades of sustained economic growth on reducing the overall number of poor. Countries still lag behind those in other regions in making progress on the Millennium Development Goals (MDG). For example, Africa will not meet the MDG of halving the share of population living in poverty between 1990 and 2015.

Weaker Commodity Prices

Sub-Saharan Africa’s rich natural resources have made it a net exporter of fuel, minerals and metals, and agricultural commodities. These commodities account for nearly three-fourths of the region’s goods exports. Robust supplies and lower global demand have accounted for the decline of commodity prices across the board. For instance, the drop in the prices of natural gas, iron ore, and coffee exceeded 25 percent since June 2014, according to the report.

Africa’s Pulse notes that overall decline in growth in the region is nuanced and the factors hampering growth vary among countries. In the region’s commodity exporters − especially oil-producers such as Angola, Republic of Congo, Equatorial Guinea, and Nigeria, as well as producers of minerals and metals such as Botswana and Mauritania, the drop in prices is negatively affecting growth. In Ghana, South Africa, and Zambia, domestic factors such as electricity supply constraints are further stemming growth. In Burundi and South Sudan threats from political instability and social tensions are taking an economic and social toll.

Fiscal deficits across the region are now larger than they were at the onset of the global financial crisis, the report finds. Rising wage bills and lower revenues, especially among oil-producers, led to a widening of fiscal deficits. In some countries, the deficit was driven by large infrastructure expenditures. Reflecting the widening fiscal deficits in the region, government debt continued to rise in many countries. While debt-to-GDP ratios appear to be manageable in most countries, a few countries are seeing a worrisome jump in this ratio.

“The dramatic, ongoing drop in commodity prices has put pressure on rising fiscal deficits, adding to the challenge in countries with depleted policy buffers,” says Chuhan-Pole. “To withstand new shocks, governments in the region should improve the efficiency of public expenditures, such as prioritizing key investments, and strengthen tax administration to create fiscal space in their budgets.”

Looking Forward

The report recommends governments begin structural reforms to address domestic bottlenecks and support renewed economic growth. Investments in energy capacity and attention to drought and its effects on hydropower will help build resiliency in the power sector. Governments can boost revenues through tax reform and improved tax compliance. In addition, governments can improve the efficiency of public expenditures to create fiscal space in their country’s budget in order to respond to external and internal shocks.

Africa’s Pulse describes the combination of external headwinds and domestic difficulties that are impacting economic activity in Sub-Saharan Africa. The report’s main messages are:

-

External headwinds and domestic difficulties are weighing on growth in Sub-Saharan Africa, although some countries in the region are continuing to post strong growth.

-

The region is entering a period of tightening borrowing conditions amid growing domestic and external vulnerabilities.

-

Fiscal deficits across the region are now larger than they were at the onset of the global financial crisis, and government debt has continued to rise in many countries.

-

Current account deficits, combined with the strong appreciation of the U.S. dollar, kept currencies across the region under pressure throughout the year.

-

On the domestic front, political uncertainty associated with elections in a number of countries, civil conflict, and fiscal vulnerabilities are the major risks.

-

A protracted Chinese slowdown, lower oil prices, and a sharper and faster normalization of unconventional monetary policies in the United States remain key external risks.

-

Governments should embark on structural reforms, such as building resiliency in the power sector and tax reform to boost revenue that can support economic growth and reduce poverty.

Related News

Renewable energy rising in Southern Africa

SADC becoming a key player in the international trend towards development of renewable energy resources and energy efficiency. Renewables now account for 23.5% of generation

An understanding of the SADC region’s emerging renewable energy industry, market development and growth is critical to realising the region’s potential and to scaling-up investment opportunities. In order to do so, REN21 and UNIDO have teamed up to produce the SADC Renewable Energy and Energy Efficiency Report which was launched on 5 October 2015 at SAIREC, the South African International Renewable Energy Conference.

The SADC report provides a comprehensive overview of the status of renewable energy and energy efficiency markets, industry, policy and regulatory frameworks, and investment activities in the region. The report draws on information from national and regional sources to present the most up-to-date summary of sustainable energy in the region.

There is huge untapped renewable energy potential in the region. In four rounds, South Africa’s REIPPPP solar PV has accounted for 1899 MW and CSP 400 MW (not all of this capacity has been commissioned). Botswana, Malawi, Namibia and Tanzania are developing large-scale solar PV projects, and Swaziland and Zimbabwe are joining this trend.

Wind power is also taking up speed in the SADC region. As with solar, South Africa has led the way in sector development through its tender process with wind projects being implemented in Tanzania and Mauritius.

Current potential hydro resources in the region amount to just under 41,000 MW. Installed hydro capacity is just under 12,000MW, representing about 21.5% of total electricity capacity. Of this 97.6% is large-scale is hydro. With 2,431 MW, South Africa has the largest operational capacity with the DRC having the largest potential (39 GW).

Biomass – for electricity generation and industrial heating – is growing. The potential for biomass-generated electricity in the region is estimated at 9,500MW, based on agricultural waste alone.

SADC countries aim to increase renewable energy contribution to electricity supply to 27% in 2020 and 29% in 2030. SADC energy ministers recently gave approval to the formation of a SADC Centre for Renewable Energy and Energy Efficiency (SACREEE), selecting Namibia as the host country.

Attracting investment is becoming easier as interest in Africa and in renewable energy increases. Six SADC member states – Botswana, Mozambique, South Africa, Tanzania, Zambia and Zimbabwe are ranked as being attractive to investors. Mauritius, South Africa and Tanzania accounted for USD 5.8 billion in 2014, with South Africa alone accounting for USD 5.5 billion.

Related News

WTO Committee on Sanitary and Phytosanitary Measures: Communication from the African Union Commission

AUC SPS Related-Activities

The African Union Commission (AUC) organized the Inaugural Conference of the Specialized Technical Committee (STC) on Agriculture, Rural Development, Water and Environment from 5-9 October, 2015. The STC reviewed the relevant strategic goals, facilitate mutual accountability and identify synergies, linkages and complementarities in on-going agriculture, rural development, water and environment related initiatives, and their implications on the achievement of the overarching goals of Africa Accelerated Agricultural Growth and Transformation (3AGT) agenda for attaining food and nutrition security, reduce poverty, boost intra-African trade, and enhance resilience of production systems and livelihoods to climate change and related shocks. The Subcommittee on Agriculture, Rural Development, Livestock and Fisheries considered a total of 32 documents for endorsement and implementation and 12 of these were directly aimed at facilitating trade.

The African Union Commission (AUC) and UNCTAD organized a training workshop on Trade in Services for CFTA negotiators (English) from 24-28 August 2015 in Nairobi, Kenya. The aimed at enhancing the capacity of the African CFTA negotiator to have a common understanding of critical terminologies and operating principles governing trade in services in preparation of the CFTA negotiation starting in April 2016.

The African Union Commission (AUC) facilitated the development of the Continental Agribusiness Strategy. The strategy outlines mechanisms of mobilizing different partners including the AU, RECs, member States, farmer organizations, private sector, development partners and other actors around a set of high priority strategies designed to support the growth of a robust and inclusive private sector-led African agribusiness. When implemented, the strategy will provide significant impetus in contributing to the goals outlined in the Malabo Declaration, including boosting intra-African trade. Whereas the strategic thrusts identified by the continental agribusiness strategy will be the foundation for vibrant agribusiness and agritrade promotion in Africa, the strategy builds on existing initiatives at continental, regional and national levels. Further, the continental agribusiness strategy seeks to improve coordination, mobilization, advocacy, and communication among various actors in the agribusiness landscape in Africa by proposing key institutional developments.

The African Union Commission through the Partnership for Aflatoxin Control in Africa (PACA), a consortium coordinating aflatoxin mitigation and management across health, agriculture and trade sectors in Africa continued to provide consistent coordination and coherent leadership to the continental efforts on aflatoxin control. The AUC through the PACA Secretariat directly supports governments to achieve large scale change in aflatoxin control in Africa. It also forges strong partnerships and works jointly with RECs, private sector and other key stakeholders to improve governments’ effectiveness. Amongst other activities implemented in this period, PACA convened the regional workshop on “Revamping the Groundnut Value Chain in West Africa through aflatoxin Mitigation” 1-2 September 2015, Dakar Senegal.

The European Commission, in partnership with African Union Commission, the ACP Secretariat, the European Investment Bank and the Technical Centre for Agricultural and Rural Cooperation (CTA) organized a conference on Agri-Business Investments in partnership with farmer organisations in ACP countries, 14-15 October 2015. The aim of the conference is to engage stakeholders and partners to work on a common blue print for smart agri-business investments in ACP Countries in partnership with farmers’ organisations. The event will build on examples of agri-business investments, and development in Africa; success stories and lessons learnt on gaining access to regional and international markets for farmer organisations in ACP countries among others. The results of the conference will guide European Union and AUC future activities in this area.

AU-IAPSC SPS Related Activities

The AU-IAPSC (African Union Interafrican Phytosanitary Council) provided technical backstopping in prioritizing the capacity building areas under the Australia – Africa Plant Biosecurity Programme. 16 African experts will be trained in Australia in different areas of plant biosecurity.

AU-IBAR (African Union Interbureau for Animal Resources)

African Union Commission and its technical office IBAR have supported the training to improve the quality and effectiveness of participation of African member States in the activities of the WTO SPS Committee. The specific training objectives were to:

-

Improve communication and circulation of information between relevant national stakeholders within African countries prior to the regular meetings of the WTO SPS Committee;

-

Improve communication and circulation of information between African countries before the regular meetings of the WTO SPS Committee;

-

Identify potential Specific Trade Concerns that could be raised by African countries or against African countries (by third countries), and prepare coordinated action by/support to the African countries involved; and

-

Harmonize/coordinate the submission of information to the SPS Committee made by countries, RECs and the AU.

Related News

Obama finally gets his Pacific trade deal

In what could become the most significant foreign-policy legacy of President Barack Obama’s administration, negotiators from 12 nations inked the Trans-Pacific Partnership (TPP), one of the largest free trade agreements in history.

The deal will boost trade among a dozen nations comprising 800 million people and making up 40 percent of the global economy. But it was in doubt as late as Sunday, as negotiators in Atlanta wrangled over the smallest details of how the deal would shape trade in the Asia-Pacific region. On Monday, U.S. Trade Representative Michael Froman announced what he called a “historic agreement” that came after more than five years of seemingly endless negotiations.

TPP “helps define the rules of the road for the Asian-Pacific region,” Froman said.

As talks in Atlanta creeped into the weekend, it was unclear whether concerns about dairy-market access and biologic medicines could be resolved.

The president must wait 90 days after the TPP agreement is done before he signs it. Then it goes to Congress for a vote. The text of the deal must be public for at least 60 of those days.

The trade deal, the centerpiece of Obama’s rebalancing to Asia, has sparked opposition from both the left and the right, angering environmentalists, trade unions, and lawmakers representing Rust Belt states who fear the pact will accelerate the exodus of U.S. manufacturing jobs. Some presidential candidates, including the front-runners, Republican Donald Trump and Democrat Hillary Clinton, are also opposed to the deal. Bernie Sanders, the independent senator from Vermont who is running as a Democrat, is also opposed to TPP.

Obama does have one advantage: fast-track trade authority, won in June, to quickly review trade bills and get an up-or-down vote from Congress. Administration officials insist the deal is necessary to keep the United States competitive in the 21st century.

“It will strengthen the hand of American workers and ensure that our businesses can compete on a level playing field in some of the world’s most significant markets,” U.S. Commerce Secretary Penny Pritzker said in a statement Monday.

The deal touches on nearly every aspect of trade between the United States and 11 other countries in the Asia-Pacific. It calls for the gradual reduction or elimination of tariffs on hundreds of goods and services, from cars and trucks to rice and cheese. It also clarifies intellectual property rights for movies and pharmaceutical drugs, as well as the Internet, and is meant to create new standards for environmental protection and labor rights in participating countries. The deal also creates a novel dispute-resolution mechanism.

The economics of the deal, including potential trade gains and job losses for different sectors, loom largest for leaders and legislative branches. The deal has proved unpopular among Canadian farmers, who fear their protected dairy industry could come under assault by international rivals, and among car-parts makers in Mexico, who fear outside competition.

But the geopolitics of the deal are a major selling point for the White House as well. In a statement on Monday, Obama underscored his view that a deal “strengthens our strategic relationships with our partners and allies in a region that will be vital to the 21st century.”