Search News Results

Improving market access for the least developed countries in the 2030 Agenda for Sustainable Development

A new UNCTAD Policy Brief focuses on key questions concerning how to achieve target 17.11 of the Global Goals though improving market access conditions faced by the least developed countries.

The sustainable development goals (SDGs) in the 2030 Agenda for Sustainable Development aim to double the share of global exports of the least developed countries (LDCs) by 2020.

The agenda also calls for providing duty-free and quota-free (DFQF) market access to LDCs as one of the main pillars of international support for export expansion by LDCs. DFQF market access is important, but will it be sufficient to double the export share of LDCs? And will it contribute to sustainable development?

What kind of market access conditions are least developed country exports facing today?

Least developed country exports receive preferential market access in most developed countries. In 2014, 89.5 per cent of the value of the exports of LDCs to developed countries was duty free. Developing countries also provide preferential market access to LDC exports. Average applied tariff rates to LDC exports continued to fall even after the financial crisis in 2008-2009. As the presence of import quotas has diminished in international trade, market access conditions faced by LDCs are moving closer to DFQF market access. However, the true value of preferential market access is determined by the tariff margins, that is the difference between the tariff rates applicable to LDC exports and those applicable to the exports of competitors.

UNCTAD has estimated the preferential tariff margin of LDC exports relative to the exports of non-LDC countries competing in the same markets in 2008 and 2013. The relative preferential margin in 2013 increased from the 2008 level except in Latin America, where LDC competitors enjoy better market access conditions through regional trade agreements (RTAs). The fall in relative preferential margins in low-income countries and South Asia may have resulted from a compositional shift of LDC exports from low-tariff products (e.g. fuels) to higher-tariff products (e.g. foodstuffs).

What will genuinely improve the market access conditions faced by the least developed countries?

Considering market access conditions as one of the binding constraints to the export growth of LDCs in the post-2015 development agenda (along with constraints related to infrastructure, energy and transport), UNCTAD proposes the following package of six international actions:

-

Provide duty-free and quota-free market access

-

Implement the WTO ministerial decision on the services waiver and fulfil article IV.1 and 3 of the General Agreement on Trade in Services

-

Reduce future trade costs by cooperating in SDG implementation

-

Physically connect LDCs to the international market

-

Target aid for trade to upgrade the productive and export capacity of LDCs

-

Help LDCs use their export growth to achieve sustainable development

Related News

Food prices lower for longer

FAO maps decline in both trade volumes and volatility for key agricultural commodities

Agricultural commodities are going through a period of lower and less volatile prices, according to the FAO Food Outlook released on 8 October 2015.

After several dramatic upward price spikes from 2007 through early 2011, most cereal and vegetable oil prices are on a trajectory that is both steady and declining, the Outlook reports in a special feature.

Among the reasons are high inventory levels, sharply lower oil prices and the renewed strength of the U.S. dollar, none of which appear likely to be reversed in the short term, although unexpected shocks, such as weather-driven impacts on harvests, can never be excluded.

The FAO Food Price Index, a trade-weighted index tracking international market prices for five major food commodity groups, fell to a six-year low in August. New figures, also released today, show it inched up by about two-thirds of a percentage point from its August low to 165.3 points, which is still 18.9 percent less than a year earlier.

“The takeaway message here is that statistically, the most recent shifts in behaviour foresee downward price momentum with lower volatility,” Adam Prakash and Friederike Greb, both commodity specialists at FAO, write of their analytical findings.

The price path of the past few years, and the prospective path ahead, are not the same for all food groups. Rice prices tend to move independently from other grains, while sugar prices have always been volatile, having lost and gained over half their value more than 12 times since 1990. Meat and dairy products fit the broad trend but, as more perishable commodities, they often do so with a time lag.

Staple grains are at the core of the declining price trend, as a result of several years of robust harvests around the world as well as stockpiling that has taken reserves to record highs. Such precautionary reserves are now being slowly unwound, and global cereal stocks will likely close the 2016 season at 638 million tonnes, down four million tonnes from their opening levels, according to new forecasts in FAO’s latest Cereal Supply and Demand Brief.

Meanwhile, this year’s world cereal production projection was notched down to 2.534 billion tonnes, six million tonnes below last month’s forecast, and 0.9 percent below 2014’s record level, due mostly to reduced output of U.S. maize, for which prices have fallen by half since July 2012.

Low prices and food security

Lower food prices “seem to be a boon to food security” and are indeed just that for households who spend a large share of their income on food purchases, the authors note.

Indeed, the global food import bill is expected to fall in 2015, dropping to USD1.09 trillion, a five-year low, and down almost 20 percent from the record high of USD1.35 trillion in 2014. That drop, to which cereals, dairy products, meat and sugar all contributed substantially, was also encouraged by declining freight rates.

However, the authors warn that calculating overall benefits also requires considering that lower prices reduce farmers’ incomes.

Slimmer margins for rural farmers are likely to reduce on-farm investments, whose past inadequacy was largely blamed for the sharp price hikes of the last decade. Low returns may also require more incentives for more investments in agriculture and rural economic services ranging from credit, to roads and warehouse facilities.

Trade flows declining

While global production is robust and inventory still high, the volume of cereals being traded internationally is declining, and forecast at around 364 million tonnes for the 2015/16 season (July/June), down 2.9 percent from the previous period.

The downward trend is driven by wheat, mostly due to lower imports in Asia – especially the Islamic Republic of Iran – and North Africa, and by coarse grains, where demand from Asia is lower, even though Africa and Europe are both expected to increase their imports.

Trade in cassava, meanwhile, is poised to grow by 19 percent and to hit a record high, due mostly to demand from China for a cheaper raw material for its animal feed, energy and industrial sectors.

Trade volumes in seafood are also rising. Currency movements cast a heavy shadow over this sector, as a strong dollar has made the U.S. a major destination for shrimp exports while weaker currencies elsewhere impact a range of sectors from Norwegian salmon to Chinese fish processors reliant on imports. Still, overall fish production is forecast to grow by 2.6 percent this year, driven by aquaculture expanding at nearly twice that rate.

Related News

East and West Africa build trade ties

Kenyan and Ghanaian government officials are set to gather in November, with the aim of opening new economic frontiers to boost development and intra African trade between the countries.

The President of the two countries met earlier in the year and agreed on protocols regarding ICT, farming and tourism to establish a co-operation between the two countries.

The core contribution to East Africa’s trade flow is informal trade which accounts for 30 to 40 per cent.

Sarah Warren, Structured Trade Transactor at Rand Merchant Bank, shared a relative example that a preliminary report of informal trades in Gauteng showed that R2.6 billion is contributed to Johannesburg’s economy by them coming across South Africa’s borders and purchasing goods to take back.

“We are not talking about small numbers despite the fact that a lot of these informal traders are small scale traders on an overall basis, we are still looking at very big numbers,” shared Warren.

An identified concern in this sector is that many of these traders are moving unprocessed goods across the value chain and they do not retain much from that. Warren said there are regulations that are aiming to formalise the informal sector in the EAC (East African Community).

“There are some clear benefits, they would increase tax revenues because often this kind of trade evades normal tax procedures, also for security processes, tracing them back and moving them in the banking sector,” Warren said.

James Ngomeli, Managing Director of Brands and Beyond, said, “We see a lot of opportunity in the intra-trade between the two countries. Ghana is mainly an import country and Kenya has a lot of talent.”

Although the geography of the two countries is a challenge, Ngomeli said the trade would create an incentive to build the Trans-Africa freight that has been in talks, because trade between the countries faces a big obstacle when there are large volumes of goods.

Warren said another important consideration for policymakers is safety, establishing if the goods and products moving across the borders are being safety-checked correctly. There are a fair amount of measures for smaller traders but not enough incentives for the larger, more formalised sectors to move their trade across formally.

One of the key opportunities for the EAC is increasing revenue given the low commodity prices that we are facing and in diversifying economies and infrastructure, “the benefits there are enormous,” said Warren.

With recent initiatives to strengthen regional trade in East Africa neighbouring countries, Warren said these regimes should simplify things like less complex documentation, and goods less than 2000 dollars should not be taxed.

Ngomeli reinforced that saying, “There are very good incentives, Ghana is waiting for us. There are tax incentives, there’s no visa to go to Ghana, their goods are the same price as in Kenya.”

Related News

tralac’s Daily News selection: 8 October 2015

The selection: Thursday, 8 October

Pascal Lamy, José María Figueres, Oby Ezekwesili : ‘A fish called development’ (Policy Innovations)

When political leaders meet at the 10th WTO Ministerial Conference in Nairobi in December, they will have an opportunity to move toward meeting one of that goal's most important targets: prohibition of subsidies that contribute to overfishing and illegal, unreported, and unregulated fishing by no later than 2020. This is not a new ambition; it has been on the WTO’s agenda for many years, and it has been included in other international sustainable development declarations. But, even today, countries spend $30bn a year on fisheries subsidies, 60% of which directly encourages unsustainable, destructive, or even illegal practices. The resulting market distortion is a major factor behind the chronic mismanagement of the world's fisheries, which the World Bank calculates to have cost the global economy $83bn in 2012.

Charles Onyango-Obbo: 'WTO meet heads to Nairobi: It could be Africa’s moment of glory...or disaster' (The Citizen)

So come December, the world will be watching Nairobi. If the WTO meeting ends in chaos and with no deals, you can expect to read about “in the end, it was impossible to reach to reach agreement in Africa’s sweltering heat”.

Roberto Azevêdo welcomes G-20 Ministers’ support for significant Nairobi outcome (WTO)

Remarks by Roberto Azevêdo to G20 Trade Ministers meeting (WTO)

Dubai Chamber study explores untapped Islamic economy potential of the African market (Dubai Chamber)

Launched in association with the Economist Intelligence Unit, the highlights pointed to the growing demand in Kenya, Ethiopia and South Africa markets for Islamic finance products and banking instruments in asset management and takaful sectors. It further revealed that the African region needs somewhere near $98bn a year to fund its infrastructure needs. Sukuk lends itself well to Africa’s infrastructure gap, it said. The study will be fully published during the Africa Global Business Forum in Dubai next month.

Kenya to host first East Africa Islamic Finance Summit

WIPO African ministerial should embrace a pro-competitive and pro-development IP vision (ICTSD)

An African ministerial meeting, organised by the World Intellectual Property Organization (WIPO) and the Japan Patent Office (JPO), to be held in Senegal next November 3-5 should embrace a balanced and development-oriented approach to intellectual property. Such an approach ought to take into account the needs, priorities and socio-economic circumstances of African countries as well as the most recent empirical evidence on the dynamics of intellectual property and innovation on the continent. [The authors: Ahmed Abdel-Latif , Dick Kawooya, Chidi Oguamanam]

Concluding, today: Trade Policy and Sustainable Development Forum (UNCTAD)

The United Nations Conference on Trade and Development will organize its Trade Policy and Sustainable Development Forum for developing countries, particularly for African countries, from 6 to 8 October 2015. It will bring together senior trade and development policymakers, trade negotiators, experts, academia and other stakeholders to examine the role of trade policy in reaping developmental benefits from trade and improving the welfare for the population in the post-2015 development context.

Mauritius eyes maritime projects, Africa links to boost growth (Reuters)

Mauritius has a deal with a Chinese firm to develop a $113m fishing port and is working with investors on plans to become a maritime hub for Africa, part of its bid to accelerate growth, the island nation's finance minister said on Thursday. Such [BOTT] deals usually leave a project in private hands for 20 or more years before it is transferred back to the state. The minister said the term of this plan had yet to be finalised. The quay and related facilities, worth 4 billion rupees ($113 million), would handle up to 20 vessels at a time on completion in 2018, he said. A Mauritian official said the developer was China's LHF Marine Development Ltd.

Fuad Cassim: 'State and private sector must shift attitudes to spur growth' (Business Day)

In conclusion, some lessons can be drawn from the Indian experience, despite the different context. The primary reason for choosing India as a comparative experience is because of the distrust that existed between the private sector and the government. A similar situation prevails in South Africa.

Driving SA's industrial development agenda: call for papers (ERAN, dti)

This highlights a need to assess how existing policy instruments and incentives (and their application) currently contribute to the creation of an enabling environment in support of the objectives of increased productive capacity and inclusive growth. This includes fiscal incentives, preferential procurement and localisation, technical regulations, technology transfer, Rand D support, skills development, trade, investment and market development support. ERAN is therefore hosting a conference entitled Driving South Africa’s Industrialisation Agenda to explore some of these issues and draw practical lessons on improving the economic landscape in South Africa. ERAN is structured around four key thematic working areas, which determine the key focus areas for the conference:

Economic policy low on agenda at ANC council (Business Day)

Zimbabwe: Regional currencies depreciation exposes local industries (The Herald)

Zimbabwe's manufacturers say the continued depreciation of regional currencies is worrying as it further exposes local industries to the threat of cheap imports. Dairibord Holdings chief executive officer Mr Anthony Mandiwanza said the loss of value of the South African rand and the Zambian kwacha against major currencies, particularly the United States Dollar, makes local producers uncompetitive. Zimbabwe’s use of the US dollar pushes up operating costs which feed into the pricing structures of goods produced locally. This makes products manufactured in the region cheaper and makes Zimbabwe the destination for producers from neighbouring countries.

Zim to face international creditors (Financial Gazette)

An International Monetary Fund official has said Zimbabwe’s debt situation will be tabled before creditors at a side meeting of the IMF/World Bank annual meetings to be held in Peru from Friday. Christian Beddies, IMF resident representative in Zimbabwe, told the Financial Gazette’s Companies & Markets: “All of Zimbabwe’s creditors, multilateral and bilateral, have been invited to the (side) meeting”.

Tension rising over depleting Kariba waters (Financial Gazette)

Angola creates Customs Risk Management Centre (MacauHub)

The government of Angola will create a Customs Risk Management Centre to share information between agencies involved in trade with foreign countries, the Minister of Trade said in Luanda. Minister Rosa Pacavira, who was speaking at a seminar on trade facilitation, said the aim of creating the Risk Management Centre was to ensure intelligent risk management when imports arrive in Angola. The creation of the Centre is part of a programme for ratification of the Trade Facilitation Agreement, of the World Trade Organization, which calls for elimination of physical inspections of shipments that include goods that pose no risk and have no tax burden.

Government laments trade imbalance between Zambia, South Africa (The Post)

Commerce minister Margaret Mwanakatwe says Zambia needs to increase its exports to South Africa in order to reduce the negative trade imbalance between the two countries. And South African High Commissioner to Zambia Sikose Mji has observed that trade and investment are the most dynamic aspects in regional integration efforts.

Textile manufacturing becomes costly in Zambia (YNFX)

With continuous depreciation of Zambian currency, textile makers are finding it too costly to import raw materials in Zambia as it would increase the cost of production, said Ajit Desai, managing director of Kariba Textiles. The blankets are manufactured by using materials like acrylic yarn and fibre, which are not produced in the local market thereby making it costly to manufacture blankets in Zambia, he said.

Rwanda to host world's first 'drone airport' (New Times)

The government has moved to set up a regulatory framework for remotely piloted aircraft, popularly referred to as ‘drones,’ following investor interest to establish the world’s first drone airport (drone port) in the country beginning next year. Last month, Norman Foster, a renowned British architect, expressed interest by his firm, Foster + Partners, alongside business partners to build the world’s first drone port in the country to facilitate transport of urgent medical supplies and electronic parts to remote parts of the region using drones. In their proposal, the investors said, beginning next year, they intend to begin construction of three drone ports, which will take about four years to complete.

JK: Kenyan projects in Tanzania now worth $1685m (IPPMedia)

“For us in Tanzania, Kenya is not a competitor but a strategic partner. Kenya ranks fifth in the Top Ten list of countries with the largest investments in Tanzania. Kenya comes after only United Kingdom, United States, China and India. Actually, in that Top Ten List, there are only two African countries namely Kenya and South Africa, on which Kenya is the leader. Kenya’s investments in Tanzania account for 518 projects with the total value of USD1,685.47m and have created about 55,762 jobs.”

Broadening the sources of growth in Africa: the role of investment (UNCTAD)

A new UNCTAD Policy Brief argues that enhancing the contribution of investment to the growth and development process in Africa will require three complementary policy measures: boosting the level and rate of investment; improving the productivity of new and existing investment; and ensuring that investment goes to strategic sectors deemed crucial for economic transformation and the realization of national development goals.

Study on gender and inclusive growth: EOI (AfDB)

Under the supervision of the Special Envoy on Gender, the incumbent is expected to perform, inter alia, the following duties: Conduct the study on Gender and Inclusive Growth using evidence from a sample of African countries and will provide evidence to inform the design of future AfDB policy dialogue and development assistance to RMCs aimed at enhancing growth that leaves no one behind.

Global Monitoring Report 2015/2016: development goals in an era of demographic change (World Bank)

According to the Global Monitoring Report 2015/2016: Development Goals in an Era of Demographic Change, released in Peru at the start of the Annual Meetings of the World Bank and the IMF, the world is undergoing a major population shift that will reshape economic development for decades and, while posing challenges, offers a path to ending extreme poverty and shared prosperity if the right evidence-based policies are put in place nationally and internationally.

Donor support to local private sector development: concept paper and methodology for research (OECD)

Current activities also include a peer learning exercise on donors working with and through the private sector. As part of the deliverables for the DAC’s Programme of Work and Budget 5.1.3.3.1, this paper presents a proposal on examining donor support for local private sector development, a topic that has drawn significant attention in numerous DAC discussions. [Prepared for the OECD's Advisory Group on Investment and Development, 14-15 October 2015] [Companion analysis: Private sector engagement and development - deepening private sector engagement in aid for trade (Chapter 7 in Aid for Trade at a Glance 2015)]

How fiscal policy can tame the commodities roller coaster (IMF)

Slump hits Kenya’s private sector on weak shilling (Business Daily)

Namibians urged to invest in Congo (The Namibian)

Kenya-Russia to strengthen trade ties (The Citizen)

Turkish business delegation in Namibia to explore opportunities (StarAfrica)

Environmental crimes change face of Sub-Saharan Africa (Bloomberg)

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome. Richard Humphries (Email: This email address is being protected from spambots. You need JavaScript enabled to view it.; Twitter: @richardhumphri1)

Related News

World undergoing major population shift with far-reaching implications for migration, poverty, development: WB/IMF Report

As migrants and refugees from Africa and the Middle East continue to arrive in Europe in unprecedented numbers, a new World Bank/IMF report says that large-scale migration from poor countries to richer regions of the world will be a permanent feature of the global economy for decades to come as a result of major population shifts in countries.

According to the Global Monitoring Report 2015/2016: Development Goals in an Era of Democratic Change, released in Peru at the start of the Annual Meetings of the World Bank and the IMF, the world is undergoing a major population shift that will reshape economic development for decades and, while posing challenges, offers a path to ending extreme poverty and shared prosperity if the right evidence-based policies are put in place nationally and internationally.

The share of global population that is working age has peaked at 66 percent and is now on the decline. World population growth is expected to slow to 1 percent from more than 2 percent in the 1960s. The share of the elderly is anticipated to almost double to 16 percent by 2050, while the global count of children is stabilizing at 2 billion.

The direction and pace of this global demographic transition varies dramatically from country to country, with differing implications depending on where a nation stands on the spectrum of aging and economic development. Regardless of this diversity, countries at all stages of development can harness demographic transition as a tremendous development opportunity, the report says.

“With the right set of policies, this era of demographic change can be an engine of economic growth,” said World Bank Group President Jim Yong Kim. “If countries with aging populations can create a path for refugees and migrants to participate in the economy, everyone benefits, Most of the evidence suggests that migrants will work hard and contribute more in taxes than they consume in social services.”

More than 90 percent of global poverty is concentrated in lower-income countries with young, fast-growing populations that can expect to see their working-age populations grow significantly. At the same time, more than three-quarters of global growth is generated in higher-income countries with much-lower fertility rates, fewer people of working age, and rising numbers of the elderly.

“The demographic developments analyzed in the report will pose fundamental challenges for policy-makers across the world in the years ahead,” said IMF Managing Director Christine Lagarde. “Whether it be the implications of steadily aging populations, the actions needed to benefit from a demographic dividend, the handling of migration flows – these issues will be at the center of national policy debates and of the international dialogue on how best to cooperate in handling these pressures.”

At country level, governments with young populations can maximize the benefits of demography by investing in health and education to maximize the skills and future job prospects of their youth. Those countries with aging populations should consolidate their economic gains by boosting productivity and strengthening social safety nets and other welfare systems to protect the elderly. At the global level, freer cross-border flows of trade, investment, and people can help manage demographic imbalances.

Countries can earn a first demographic dividend when a workforce grows as a share of a nation’s population, providing a powerful acceleration to growth. As changes in age structure expand production and resources, a second dividend is possible as savings build up and investment rises.

Although low-income countries can expect to see the largest growth in their working age populations, many of these countries are held back by conflict and fragility, putting these gains at risk. Sub-Saharan Africa’s high fertility and population growth will make the region home to an increasing share of the world’s children and working-age population in decades ahead, the report says.

“As heartbreaking images of families desperately fleeing conflict remind us, many migrants leave home due to conflict, instability and shrinking economic opportunities at home,” said Kaushik Basu, Senior Vice President and Chief Economist at the World Bank. “While refugees are moving to rich countries what is often overlooked is that the flows into middle and low income countries are vastly greater. Creating economic opportunities for countries with growing proportions of youth will contribute to economic stability and development and will help countries lower fertility rates, which contributes to stronger growth.”

Countries that are lagging in development and have high fertility rates are classified as pre-dividend, such as Niger. They would benefit from improving health care and education, facilitating lower fertility rates and accelerating the transition to a greater share of their populations that are working age, the report says.

Early-dividend countries that have already seen a drop in fertility but that still have young populations, such as Ethiopia, could benefit from speeding up job creation. An expanding workforce is linked to growth: an increase of 1 percentage point in the working age population can translate to a rise in the GDP per capita of as much as 2 percentage points, the report says.

In late-dividend countries where the share of the working age population is declining, such as Brazil, economic dynamism is at risk of fading. There, governments should encourage savings for productive investment, female participation in the workforce, and strengthening of social welfare systems. Post-dividend countries such as Japan, which are characterized by declining workforces and rising numbers of elderly, would do well to complete health care and pension reforms and take further steps to raise workforce participation and productivity, the report says.

“To leverage demographic change within countries, the centers of global poverty need to facilitate the demographic transition to slower population growth and accelerate job creation to absorb the swelling working-age population,” said Philip Schellekens, the report’s lead author. “The engines of global growth need to address demographic headwinds and adapt institutions and policies to aging. In today’s interconnected world, effective policies will also arbitrage demographic change across countries. Freer flows of capital, trade and – especially – labor present tremendous opportunity to turn this era of intense demographic change into one of sustained development progress.”

In a separate section, the report details the decline of those living in global poverty, which is reclassified as living on $1.90 or less a day, to a forecast of 9.6 percent of the world’s population in 2015, a projected 200 million fewer people living in extreme poverty than in 2012.

The report notes that world economic growth in 2015 is set to disappoint, down to 3.1 percent, from 3.4 percent in 2014, on the basis of slower growth in many emerging market economies. Growth is expected to pick up to 3.6 percent in 2016, helped by strengthening recoveries in major advanced economies – led by the United States – and some turnaround from weak situations in several emerging market and developing economies.

“The global economic environment is increasingly uncertain, with growth prospects having again been marked down – feeding concerns about a more fundamental slowdown in the trend growth rate in many countries,”said Seán Nolan, Deputy Director in the IMF’s Strategy, Policy, and Review Department. “Supply-side reforms to revitalize productivity growth are essential, with the key actions required varying with country circumstances.”

The Global Monitoring Report analyzes the policies and institutions needed to make progress in achieving global development goals. Produced jointly with the IMF, these reports benchmark progress and present analytical work on issues that will impact global development. For a detailed discussion on updated poverty data, shared prosperity, and policy agendas, see “Ending Extreme Poverty and Sharing Prosperity: Progress and Policies”, World Bank Policy Research Note 15/03.

Related News

Broadening the sources of growth in Africa: The role of investment

A new UNCTAD Policy Brief argues that enhancing the contribution of investment to the growth and development process in Africa will require three complementary policy measures: boosting the level and rate of investment; improving the productivity of new and existing investment; and ensuring that investment goes to strategic sectors deemed crucial for economic transformation and the realization of national develop-ment goals.

Achieving the African Union’s vision of an integrated, prosperous and peaceful Africa that can serve as a pole of global growth in the twenty-first century requires broadening the sources of growth on the continent to lay the foundation for sustained growth and poverty reduction.

For this to happen, however, it is necessary to enhance the contribution of investment to the growth process. This can be done by boosting the level and rate of investment, improving its productivity and ensuring that it goes to strategic sectors of the economy. Further, the international community has a key role to play – that of complementing the efforts of national Governments.

This policy brief outlines some of the key messages and recommendations of the UNCTAD Economic Development in Africa Report 2014: Catalysing Investment for Transformative Growth in Africa.

Investment and diversification of the sources of growth

Broadening the sources of growth in Africa will require enhancing the contribution of investment to the growth process on both the demand and supply sides of the economy. On the demand side this is necessary to obtain a more balanced role for consumption and investment in the growth process; on the supply side it is needed to foster transformative growth because investment has been identified as one of the main drivers of structural transformation. In this paper, “investment” refers to total investment in the economy, which includes public and private investment.

Private investment in turn consists of investment by local and foreign investors. The focus on total investment is important because all components of investment matter for growth and development. Government policy should therefore be geared toward exploiting the complementarities among the various components, rather than promoting one component at the expense of another. Crucially, how can African countries catalyse investment for transformative growth and development?

Key points:

-

Concerted actions are needed at the national and international levels to stimulate investment in Africa.

-

It is necessary to enhance the contribution of investment to the growth process on both the demand and supply sides of the economy.

-

Government policy should be geared toward exploiting the complementarities between local and foreign investment.

Related News

How fiscal policy can tame the commodities roller coaster

Resource-rich economies face enormous challenges to manage volatile and unpredictable commodity prices. In its latest Fiscal Monitor, the IMF examines how countries can tax and spend wisely so that their oil, gas and metals support strong and stable economic development.

Fiscal policy can either calm or magnify the effects of volatile commodity prices on the domestic economy. In many countries, large swings in commodity prices have resulted in large fluctuations in public expenditures and, in turn, exacerbated economic volatility.

The right reforms can make a difference. “Improved fiscal frameworks and policies can help ensure that natural resources are truly a blessing for resource-rich countries,” said Vítor Gaspar, Director of the IMF’s Fiscal Affairs Department.

So how can countries tame the commodities roller coaster? The report outlines how more stable expenditures can give a smoother ride, how well-planned public investment can help a steady economic climb, and how fiscal frameworks can lay the track for the long-term future.

A smoother ride: preserving economic stability

The experience of recent decades shows that many countries find it difficult to manage volatility around commodities. Their public expenditure tends to significantly accelerate during price upswings and fall during downswings. This is how fiscal policy can play a major role in transmitting commodity price volatility to the domestic economy. Macroeconomic instability, in turn, hampers sustainable growth.

The latest commodity price cycle illustrates the point. Many countries saw a massive increase in budget revenues during the 2003-08 revenue windfall, exceeding 200 percent of 2002 GDP in some cases, which financed enormous increases to expenditures. There are cases in which the size of the budget more than tripled. In contrast, other countries did build large fiscal buffers during the years of high commodity prices.

With the latest sharp fall in commodity prices, most countries will have to cut expenditures, in some cases by large amounts. However, those with fiscal buffers will be able to apply the brakes at a more gradual pace and cushion the impact on the economy.

A steady climb: promoting economic development

Designing an appropriate long-term strategy to manage natural resources is a complex task. If the wealth is simply consumed, the country will become poorer as the natural resources are depleted. Well-designed strategies promote economic development by investing, for example, in infrastructure. Investment in people is as important, namely by achieving strong health and education outcomes. These decisions are complicated due to the need to manage the high uncertainty of resource prices and commodities reserves.

Indeed, many resource-rich countries used a significant share of the recent windfall to boost capital spending, as well as expenditures on health and education. For example, public investment grew by more than 15 percent a year (at constant prices) in 2000-08.

Good policies are needed to ensuring that large increases in public investment and social spending deliver strong growth dividends. Namely, scaling up of public investment needs to be done at a pace that allows space for private investment and takes into account supply bottlenecks. Countries should build financial buffers to avoid costly “stop-go” cycles. Furthermore the pace of public investment should be consistent with the country’s institutional capacity, to ensure projects are wisely selected and efficiently implemented. The same holds for health and education. It is of paramount importance that social spending is effective and efficient.

Laying the tracks: fiscal frameworks

The Fiscal Monitor stresses the importance of developing a comprehensive fiscal framework to better manage public finances amid high uncertainty. It outlines four key main areas:

-

First, set an appropriate long-term fiscal target to guide fiscal policy. This is especially important given that oil, gas and metals are non-renewable. It also calls for long-term stabilization savings to weather the large and persistent shocks.

-

Second, intensify efforts to widen the revenue base and avoid an overdependence of government revenue on the resource sector.

-

Third, make public spending more efficient. Resource-rich countries are likely to face long periods of lower fiscal revenues. Better management of public investment and expenditure can help ensure that government spending plans are efficient and are likely to yield important growth dividends. There is also room to further reduce energy subsidies.

-

Finally, the Fiscal Monitor highlights the importance of developing strong institutions. Experience suggests that improvements, for example to governance and quality government services, are essential to use natural resources in a way that will support long-term growth.

Related News

UNEP Executive Director welcomes illegal wildlife trade provisions in TPP

The Trans-Pacific Partnership (TPP) trade deal contains unprecedented provisions to combat illegal wildlife trade.

UN Environment Programme Executive Director Achim Steiner released the following statement following the conclusion of negotiations on the Trans-Pacific Partnership (TPP) trade deal.

The TPP contains unprecedented provisions to combat illegal wildlife trade, including requirements for the 12 countries involved to protect wildlife covered under the Convention on International Trade in Endangered Species of Wild Fauna and Flora (CITES) from illegal trade, and to take action to protect any wildlife that has been taken illegally from any country.

“The inclusion of wildlife protections in the TPP are an important move to help conserve biodiversity.

“In agreeing to fulfill their obligations under CITES, combat wildlife taken illegally from any country, and take further action to protect wildlife at risk in their own jurisdictions, TPP member states are taking important action to combat the illegal wildlife trade.

“These agreements on wildlife and on other environmental dimensions will need be followed up with concrete domestic legislation and regulation to ensure this accord results in effective implementation. UNEP will continue to support countries in this endeavour.

“Time will tell whether these provisions will engender significant benefits to the world's wildlife and environment.”

Related News

Mauritius eyes maritime projects, Africa links to boost growth

Mauritius has a deal with a Chinese firm to develop a $113 million fishing port and is working with investors on plans to become a maritime hub for Africa, part of its bid to accelerate growth, the island nation’s finance minister said on Thursday.

Mauritius has revised down growth forecasts for 2015 from 4.1 percent to 3.6 percent, a level Seetanah Lutchmeenaraidoo told Reuters was not enough to meet a target of lifting the Indian Ocean country from its middle income status.

Mauritius aims for 5.7 percent growth in fiscal 2016/2017 and rising to 8 percent “within the next five years”, he said.

But he said private investment had to drive the expansion as there was no room for the government to borrow, given a commitment to cut public debt to 50 percent of gross domestic product by 2018. It stood at 56 percent in June.

“We cannot borrow or give a sovereign guarantee,” he said in an interview, adding reducing debt levels needed “huge growth”.

To deliver that, Mauritius was attracting new investors in shipping and other maritime projects to make the Indian Ocean island a hub for Africa, adding impetus to an economy that now relies on sugar cane farming, tourism and financial services.

Mauritius has a deal with a Chinese firm to start building a fishing port next year on a build-operate-transfer (BOT) basis, he said. Such deals usually leave a project in private hands for 20 or more years before it is transferred back to the state. The minister said the term of this plan had yet to be finalised.

The quay and related facilities, worth 4 billion rupees ($113 million), would handle up to 20 vessels at a time on completion in 2018, he said. A Mauritian official said the developer was China‘s LHF Marine Development Ltd.

Lutchmeenaraidoo said Mauritius had received applications to establish a shipping fuel bunkering facility, including from Horizon Energy Group from the United Arab Emirates.

Dubai-based DP World, one of the world’s biggest port operators, will submit a business plan in November to run a trade transhipment port to serve Africa, he said. A memorandum of understanding was expected to be signed in January.

“We are moving out from being a small port in the Indian Ocean to become the most important maritime hub in this region,” Lutchmeenaraidoo said, and projects would follow the BOT principle.

In a further Africa initiative, he said a Mauritius-based “special purpose vehicle” was being set up to channel investment into projects in Ghana, such as sugar cane production involving Mauritius firm Omnicane, a poultry project and technology park.

Projects using this vehicle would enjoy benefits such as exemptions from value added tax (VAT) and customs duties, he said, adding Barclays was assisting with the plan.

“This special purpose vehicle will be duplicated in other countries,” Lutchmeenaraidoo said, citing interest from Ivory Coast, Senegal, Zambia, Uganda and Mozambique.

He said the plan went beyond the “purely fiscal” double taxation avoidance agreements Mauritius has with African states.

Related News

tralac’s Daily News selection: 7 October 2015

The selection: Wednesday, 7 October

The TPP deal gets done: what does it mean for developing countries? (CGD)

From information available so far, it looks like there were improvements in some areas of interest for developing countries. But I still have concerns in the three areas I wrote about in July. I’ll need to see the details before I can assess the outcomes there. And my biggest concern about the TPP, TTIP, and other regional agreements remains how they affect the World Trade Organization. Most developing countries are outside these big trade deals and will have no way to protect themselves in trade if the multilateral system fades into irrelevance.

Finally, how will the deal impact the multilateral system? Will a successful TPP negotiation spur countries on the outside to increase their efforts to bring things back to the WTO? Or will it encourage US negotiators to turn away from the WTO and focus on the Transatlantic Trade and Investment Partnership? We should get an indication of that when WTO ministers meet in Nairobi in December and, unfortunately, I’m not optimistic. [The author: Kimberly Elliott]

Sean Doherty: 'Has the TPP deal finally brought trade up to date?'

G20-OECD Global Forum on International Investment: summary report

G20 urges reforms for global trade growth

The great global trade slowdown (LiveMint)

The latest trade statistics from around the world do not make for happy reading. Economists at the World Trade Organization have recently cut their forecast of global trade in 2015 by 50 basis points, to 2.8%. Trade volumes are falling in many countries such as China. The Indian trade numbers too have been weak. The immediate news on the trade front should not be a surprise for most people who follow economic trends. But there could be more structural damage as well that is not captured in the headlines. [The author, Niranjan Rajadhyaksha, is executive editor of Mint]

US trade deficit widens as exports sag, imports from China surge (Reuters)

The data released on Tuesday by the Commerce Department illustrates the U.S. economy's vulnerabilities to a strong dollar and weak demand in foreign markets, which could impose further caution on the Federal Reserve's plans to hike interest rates. The trade deficit swelled by 15.6% to $48.3bn in August, according to data that is adjusted for seasonal factors.

The world economy is awash with liquidity and the cost of debt has never been so low – still many developing countries struggle to obtain sources of international finance for long-term productive investment. UNCTAD’s Trade and Development Report, 20151 argues that dedicated government action is needed to correct this shortfall if ambitious development goals are to be achieved. This task cannot be entrusted entirely to financial markets. Instead, specialized public institutions and mechanisms designed specifically for this purpose will be crucial. [Downloads, data]

Global action plan launched against MNCs avoiding tax (OECD)

Inclusive Global Value Chains: policy options in trade and complementary areas for GVC integration by small and medium enterprises and low-income developing countries (OECD/WB)

Jobs, wages and the Latin American slowdown (World Bank)

In the report, Jobs, Wages and the Latin American Slowdown, the World Bank´s Office of the Chief Economist for Latin America and the Caribbean points out that the expectation is that the region will see 0% growth for 2015 with a slight improvement to 1% in 2016, although uncertainty around that projection is high. That would be the fifth year in a row the region has underperformed initial expectations, a sign that new factors, mainly internal, are prolonging the effects of worsening external conditions, particularly the sharp deceleration in China and fall of commodity prices.

From Cape to Cairo? The potential of the Tripartite Free Trade Area (SAIIA)

The three main countries involved in this project – Egypt, Kenya and South Africa – have a considerable regional trade complementarity. The de facto regional trade of these three countries is also high but concentrated in sub-regions of the TFTA. The regional trade complementarity of Ethiopia, another potentially major player, is much lower, as is its regional trade intensity. The authors moreover analyse similarity in regional exports to shed light on the competition that markets face and resulting disincentives for the TFTA. [The authors: Sören Scholvin, Jöran Wrana]

South African trade policy: key cabinet decisions (GCIS)

Cabinet approved the Guidelines of Good Business Practice for South African Companies Operating in Africa. These guidelines are a voluntary set of principles consistent with laws and internationally recognized standards that promote responsible business conduct on the African continent. They provide a guiding framework for South African companies to promote sustainable economic development in Africa. They also encourage South African companies to align their involvement and practices with government’s integration and development objectives in Africa and to build mutual confidence, trust and benefit for the companies and the societies in which they operate.

Cabinet approved the ratification of the Annex on the Institutionalization of the Southern African Customs Union Summit. The summit, which comprises Heads of State or Government of each member state, will provide political and strategic direction to SACU. All SACU member states need to sign the agreement so that the summit can become the highest decision making institution of the SACU. [Background: tralac's SACU Roundtable]

Resolve disputes - Mwanakatwe tells SA (ZNBC)

Commerce Minister Margaret Mwanakatwe is optimistic that Zambia and South Africa will resolve disputes regarding the export of organic products into South Africa. Mrs Mwanakatwe says this will mitigate trade imbalances between the two countries. Mrs Mwanakatwe says the move will allow the Zambian honey to easily penetrate the South African market.The Minister was speaking when she opened the 2015 Zambia-South Africa Trade and Investment Forum in Lusaka.

Security bill spat: SA-US relations at risk (IOL)

South Africa is in danger of being sidelined for project funding by the International Monetary Fund and the World Bank as the US lobbies to scrap the controversial Private Security Industry Regulation Amendment Bill. Yesterday, the US trade mission threatened to withdraw its support for South Africa’s funding applications for infrastructure development projects if certain clauses in the bill were not reviewed, and once more placed the Africa Growth and Opportunity Act on the back foot. Heidi Ramsay, the deputy spokeswoman for the US embassy in Pretoria, said the US’s concerns were that the requirement would force US security firms to sell off their ownership at what would likely end up being fire-sale prices, which could effectively result in an uncompensated expropriation. [Security law to cost SA R133bn (Business Report)]

Botswana moves to eliminate trade barriers (Mmegi)

Local exporters and importers now have a ‘one-stop shop’ where they can receive crucial information on laws, regulations and quality standard requirements for conducting cross-border trade. Through a National Enquiry Point, which was launched in Gaborone this week, the Botswana Bureau of Standards will offer the services. The NEP is a requirement of the WTO under the Technical Barriers to Trade agreement.

Services sector anchors Botswana's 2nd quarter economic growth (Mmegi)

Uganda: Substandard imports decrease by 30% - government (Daily Monitor)

Substandard and counterfeit imports have reduced by 30% over the last two years, the minister of Trade has disclosed. According to Ms Amelia Kyambadde, the reduction is as a result of the enforcement of a government policy subjecting sensitive imports to quality test before being shipped here. Speaking last week at the 6th annual Ministry of Trade Sector Review Conference, Ms Kyambadde said the reduction that the sector has seen since 2013, also tells a story of what a stronger resolve can yield. In the sector review meeting, the executive director of Uganda National Bureau of Standards, Mr Ben Manyindo, said by close of the year, substandard and counterfeit imports would have reduced by 50%. And by end of 2016 it would have gone down by 65%.

Kenya: Current account deficit hits Sh151bn on imports surge (Business Daily)

The gap between Kenya’s imports and exports widened by 62% in the second quarter of the year, contributing to the pressure on the local currency. The country’s exports value slumped to Sh133.5 billion between April and June from Sh141 billion for the same period last year while imports grew to Sh379.9 billion from Sh371.5 billion, KNBS data shows. The expanded import bill and reduced exports pushed Kenya’s balance of trade to a deficit of Sh246.3 billion compared to a Sh230.5 billion deficit reported in the second quarter last year. However, the current account deficit was kept low because of the positive balance on the services account and remittances.

Dar-Kenya trade scales EA high (Daily News)

Trade between Kenya and Tanzania has continued to grow, accounting for 80 to 90 per cent of trade in the East African Community, President Jakaya Kikwete has said. Addressing the Kenya’s National Assembly in the capital, Nairobi, President Kikwete said the growth in trade between the two countries demonstrated how much the two countries’ contribution is critical to the greater EAC integration agenda.

Kenya-Tanzania Business Forum: Uhuru Kenyatta's speech (Business Daily)

France’s milk firm eyes East Africa (Daily Nation)

Improve ease of doing business in Tanzania (The Citizen)

EALA plenary commences in Nairobi, Pan-African Parliament: opening of the 1st Ordinary Session

Women traders in Africa’s Great Lakes (World Bank Blogs)

The Great Lakes Trade Facilitation Project (GLTFP) is groundbreaking in many ways: it is the first large-scale World Bank operation focusing on small-scale trade in a conflict area; it moves beyond a traditional focus on trade in goods, also targeting cross-border trade in services; and it is a collaborative effort across WBG’s Global Practices, including the Trade & Competitiveness and the Governance GP, designed with critical support from the Fragility, Conflict and Violence Group. [The authors: Cecile Fruman, Carmine Soprano]

Serial offenders - industries prone to endemic collusion: contributions from South Africa, Brazil (OECD)

State-business relations as drivers of economic performance (UNU-WIDER)

The empirical study of state-business relations in developing countries has emerged only recently, with notable contributions starting in the mid-1990s, developing further in the 2000s and gaining more general acceptance in the 2010s. The evidence suggests that effective SBRs can matter for economic performance. The case studies suggest that SBRs can be effective (Mauritius) but also ineffective (Malawi). [The authors: Alberto Lemma, Dirk Willem te Velde]

International agencies and experts meet to update classification of non-tariff measures (UNCTAD)

Leading organizations and experts in trade and non-tariff measures (NTMs) met in Geneva on 28-29 September, to plan an update to the International Classification of NTMs - policy measures other than ordinary customs tariffs that nevertheless restrict free trade. The following objectives were achieved:

Towards a new partnership between the EU and the ACP countries after 2020: public consultation

It is important to take stock of the current Partnership Agreement, to explore the extent to which it remains valid for the future and offers a platform to advance joint interests. A thorough review is needed of the assumptions, on which the partnership is based, of its scope, instruments and ways of working. The outcomes will form a major component of the analysis and as such contribute to set out policy proposals for the future relationship. Reference documents:

Zambia constitutes team to tackle job losses in mining industry (Coastweek)

South Africa: State of Renewable Energy report (GCIS)

WTO agrees membership terms for Liberia

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome. Richard Humphries (Email: This email address is being protected from spambots. You need JavaScript enabled to view it.; Twitter: @richardhumphri1)

Related News

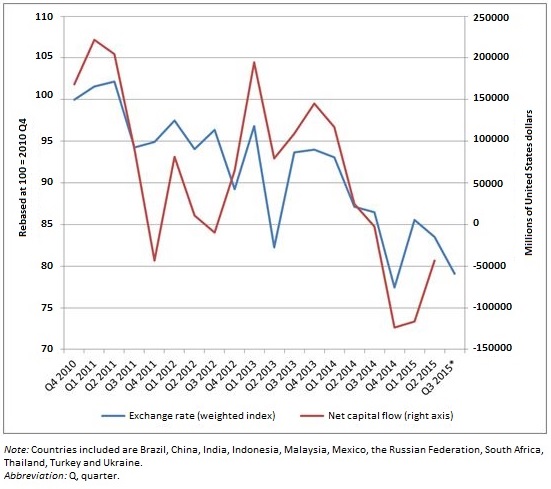

As volatile financial markets create rumblings in developing countries, UNCTAD report calls for fresh policy thinking

For most developing economies, integration into global financial markets has up to now had only weak linkages to their long-term development goals, the UNCTAD Trade and Development Report, 2015 says. Coupled with increasingly large and volatile capital flows that have expanded vulnerabilities to external shocks, the effectiveness of the policy tools designed to manage growth and development is also being limited.

Since the early 2000s, private capital inflows to developing and transition economies have accelerated substantially. External inflows to these countries, as a proportion of gross national income, increased from 2.8 per cent in 2002 to 5 per cent in 2013, after reaching two historical records of 6.6 per cent in 2007 and 6.2 per cent in 2010. Worries of a sudden or substantial exit of inflows began with the economic slowdown and have become more pronounced with the increased volatility of recent months. The close ties between capital flows and key economic prices also increase the danger of a downward deflationary spiral (see figure).

Particularly after the crisis of 2008, those capital flows owed as much to policy decisions in advanced economies as to improved fundamentals in recipient countries. Prior to the crisis, borrowing and asset appreciation drove consumption booms and private investment bubbles in some major economies, and net exports in others. After the inevitable collapse that followed, developed country policies of quantitative easing, together with fiscal austerity, have largely continued this pattern of generating excess liquidity in the private sector.

In mid-2015, global financial markets were spooked by recessions in Brazil, the Russian Federation and South Africa and by signs of economic weakening in China. Global investors, already anticipating a hike in interest rates in the United States of America and a continuing fall in commodity prices, moved briskly to exit emerging economy equity and bond markets.

“Managing the persistent volatility of financial short-term flows requires an internationally coordinated policy response,” UNCTAD Secretary-General Mukhisa Kituyi said, not merely a financial correction with few serious consequences for the real economy. “With developing countries contributing over 60 per cent of global growth since 2011, the knock-on effects of recent emerging market difficulties could be widely felt.”

Overall, developing country growth is forecast to decline to around 4 per cent in 2015, continuing a slowdown that began in 2011 after what initially seemed to be a robust recovery from the crisis in 2008/09, when annual growth reached 7.8 per cent in 2010. That forecast, though, hangs on robust growth in the Asia region; downside risks could push the figures sharply lower in the final quarter of 2015.

For much of the last decade, many developing countries experienced strong growth and improving current accounts, accumulating considerable external reserve assets as a group. The promise of higher returns for investments in developing countries presented an attractive alternative to the low interest rates on offer in advanced economies for international investors.

These capital inflows, however, generated pressures for exchange rate appreciation. More open capital accounts also meant Governments had to conduct monetary and fiscal policy with an eye to the preferences of international finance. An estimated $2 trillion carry trade in emerging economy markets was “an accident waiting to happen”. A minor currency correction by Chinese authorities seems to have been the straw that broke the camel’s back.

Trade growth is also stalling, with the slowdown in most developing regions in 2014 expected to continue or accelerate this year. Commodity prices fell significantly during 2014 and the first half of 2015, extending their downward trend from peaks in 2011/12. The most dramatic fall was that of crude oil prices, but commodity groups whose demand is more closely linked to global economic activity experienced substantial decreases as well.

The resulting decline in the terms of trade for commodity exporters, coupled with increasing capital outflows, has severely weakened economic prospects for many developing countries, the report notes.

The associated depreciation in emerging market currencies does not, however, hold the promise of a recovery-inducing surge in exports. Instead, lower global prices are likely to result in more deflationary pressures than expanded trade given the ongoing weaknesses in global aggregate demand.

A monetary and fiscal policy mix aimed at better managing private capital flows, in particular those of an unstable or speculative nature, and their macroeconomic effects, would help developing countries to face the challenges and to enhance the gains made overall from integrating into global financial markets, the report argues. Measures at the national level, including the judicious use of capital controls and credit allocation policies, need to be supplemented by global measures that discourage the proliferation of speculative financial flows and provide more substantial mechanisms for credit support and shared reserve funds at the regional level. The recent financial turmoil has added urgency to adopting such measures.

Graph 1: Aggregate net capital flows and exchange rates

Highlights

The Trade and Development Report (TDR) 2015: Making the international financial architecture work for development reviews recent trends in the global economy and focuses on ways to reform the international financial architecture. It warns that with a tepid recovery in developed countries and headwinds in many developing and transition economies, the global crisis is not over, and the risk of a prolonged stagnation persists. The main constraint is insufficient global demand, combined with financial fragility and instability, and growing inequality.

These trends reveal the lack of a well-functioning international monetary and financial system, which should be able to properly regulate international liquidity, avoid large and lasting imbalances and allow for counter-cyclical policies; however, international liquidity and capital movements respond to economic conditions in developed countries rather than to actual needs in developing countries. Furthermore, much of the current regime is in fact driven by large international banks and financial intermediaries whose activities increased much more rapidly than the capacity of any public institution (either national or multilateral) to effectively regulate it. Recent initiatives aiming at better regulation remain too timid and narrow.

This dysfunctional regime can neither prevent boom-and-bust episodes nor recurrent debt crises; and when such crises occur, it leads to asymmetric adjustment that throws most of the burden on debtor countries and exacerbates a pro-cyclical bias. This calls for a mechanism for debt resolution, in particular for sovereign external debt, which minimizes the cost of crisis and shares it fairly among the different actors. Furthermore, inefficiencies and missing elements in the international financial architecture have had negative effects in the provision of long-term finance for development.

Against this background, TDR 2015 identifies some of the critical issues to be addressed in order to establish a more stable and inclusive international monetary and financial system which can support the development challenges over the coming years. It considers existing shortcomings, analyses emerging vulnerabilities and examines proposals and initiatives for reform.

In order to improve global growth and financial stability, and to realize the investment push required to fulfil the new development agenda, the systemic problems of the international financial architecture need to be addressed. Solutions are available, but they require dedicated action by the international community.

The main recommendations of the Report are:

-

To avoid secular stagnation, developed countries need to combine monetary expansion with fiscal expansion and wage growth, and be mindful of the international spillovers that their policies can produce;

-

To make the provision of official international liquidity more stable and predictable, multilateral reform remains the desirable target – in the meantime, developing countries may build on regional and interregional initiatives, set swap arrangements among Central Banks and reduce the need for reserve accumulation;

-

A bolder regulatory agenda is needed. This should include strict separation of retail and investment banking, strong regulation of shadow banking as well as public oversight of credit rating agencies and their progressive substitution by more appropriate mechanisms for risk assessment;

-

Developing countries should not be required to apply prudential rules which have been conceived for countries hosting internationally active banks as they result in credit rationing to sectors and agents that need support from a development perspective;

-

A sovereign debt restructuring mechanism is urgently needed. This could be in the form of contractual improvements or internationally accepted principles to guide sovereign debt restructuring. However, the Report sees the best option in a statutory approach based on a multilateral treaty defining a set of rules for a debt restructuring that restores growth and debt sustainability;

-

Specialized public institutions and mechanisms are crucial for the provision of long-term development finance, in particular development banks. The international community needs to meet its Official Development Assistance commitments and to tune it better to strengthening the productive economy.

Related News

G20-OECD Global Forum on International Investment 2015: International investment policies in the evolving global economy

Report on the Global Forum on International Investment (GFII), 5 October 2015, Istanbul

Ministers and High Officials from more than ten G-20 and non-G20 countries, Heads of International Organizations, business leaders, academics and high-level representatives from labour and civil society participated in the G20-OECD Global Forum on International Investment (GFII).

The Forum took place at a critical juncture for the global economy, with the growth recovery lukewarm, trade and investment at half speed, and the social consequences of the crisis, including high income inequality, weighing down on the economic recovery. Investment – foreign direct investment in particular – still remain well below the levels prevailing before the global crisis, and the backlash of protectionism, including through new forms of ‘murky protectionism,’ is a real threat. These circumstances make it critically important to maintain open markets, and to make trade and investment work better together for the global recovery.

Against this background, the OECD Forum has provided a constructive exchange of views on evolving business realities and what they imply for policy-making, including in the G20 process. The Forum has revealed that the current regime for international investment does not allow to fully meet the challenges brought about by three realities:

-

The scope for open trade and investment regimes, and the need to foster an investment climate that is conducive to development and recognizes new countries and actors in the investment landscape;

-

The fragmentation of the international regime for investment, and the need to improve linkages with trade disciplines in mega-regionals and new-generation regional trade agreements (RTAs);

-

The sharper inter-dependencies between trade, investment and services in global value chains (GVCs), and how these links must be better coordinated in policy-making.

Keeping markets open and fostering a favourable investment climate for development

Speakers recognized the scope for further elimination of investment barriers, particularly in services, and more broadly the need to promote a good investment climate for development. The OECD Policy Framework for Investment (PFI) was mentioned as useful in this regard. Participants also underscored the need to better identify, monitor, and assess the costs associated with murkier forms of protectionism.

A common thread in these discussions was the widespread recognition that investment needs to deliver for the well-being of people, and foster more inclusive productivity, as well as durable and sustainable forms of growth meeting high standards of responsible business conduct. The OECD Guidelines for Multinational Enterprises allow for a balanced approach meeting society expectations, and participants affirmed that their use should be encouraged, particularly in the process of shaping the post-2015 Development Agenda and achieving the Sustainable Development Goals. They also encouraged continued collaboration between OECD and other international organisations in helping developing countries implement investment reforms.

Promoting a coherent governance for the international investment regime

Despite the importance of international investment as a source of economic growth and employment, there is no overarching set of rules governing this subject matter. The discussions highlighted how the current fragmented governance of FDI contributed to the confusing landscape for governments and businesses. Bilateral and regional arrangements have continued to proliferate over the past decade to fill this void: the international investment regime consists of over 3,000 international investment agreements (IIAs), most of which are bilateral investment treaties (BITs). The growing trend in RTAs signed over the past decade to include comprehensive coverage of investment underlines the importance of developing trade and investment disciplines under a joint framework. Still, participants highlighted that there is more to do to strengthen internal coherence. The Forum welcomed the contribution of the OECD-hosted dialogue on international investment disciplines gathering all G20 members, developing countries, business, civil society and international organisations, on collecting and exchanging best practices.

Participants agreed that new disciplines in emerging in ‘mega-regionals’ and next-generation RTAs have advanced policy thinking and provided partial solutions to pertinent issues; they are improving the links between trade and investment, and a range of related regulatory disciplines. On the other hand, there were also concerns that the co-existence of different blocs may create loopholes, overlaps and contradictions across investment regimes, which can engender costs and distort efficient patterns of investment and trade. On balance, participants agreed that it is necessary to promote dialogue on WTO-plus measures that can provide inspiration on potential good practices for constructing more coherent and comprehensive global rules in the future.

Addressing inter-dependencies between trade and investment

Participants agreed that the sharper inter-dependencies between trade and investment in Global Value Chains may call for strengthened coordination in policy-making. The growing complexity in the trade-investment relationship emerges from the activities of multinational enterprises (MNEs), which account for a large share of world trade. Participants agreed that it was necessary to understand new business strategies of MNEs, including the changing trade and investment relationships between parent companies, subsidiaries and suppliers, including small and medium enterprises. When flows of not just goods (final and inputs), but also services, capital, management personnel, technology, and data cross borders, investors are subject to multiple risks that may be effectively attenuated with coordinated policy efforts. Although RTAs can continue to make strides in addressing some of these issues, the need for a more global and systematic approach was underlined.

Recognizing the importance of services competitiveness in supply chains, participants highlighted that great benefits could be reaped from various types of domestic reforms, particularly in backbone services such as telecoms, transport and logistics. Services are the cornerstone of GVCs, not only as inputs in the production process, but also in connecting different production segments. Manufacturing remains a core activity in GVCs, but is increasingly dependent on efficient services. There is also enormous potential in services value chains that remains untapped due partly to high levels of restrictions. Adequate reforms in key services markets are still not in place. Participants mentioned the OECD Services Trade Restrictiveness Index (STRI) as a key tool for prioritising and sequencing of such reforms, and strengthening the assessments of costs from remaining barriers. Participants also underscored the need to enhance participation of SMEs and LDIC in GVC to build a more inclusive and sustainable world economy. They welcome the report on this topic prepared by the OECD and the WB and encourage them to continue addressing these issues, with the view to develop a comprehensive policy analysis.

The way forward: enhance the dialogue on trade and investment in the G20

Ministers, High Officials and other participants concurred that enhanced G20 involvement in trade and investment matters is critical to address such challenges. There is an opportunity to build evidence, mutual understanding and consensus on the way forward to improve the international regime for trade and investment, the twin engines for reviving the world economy. The design and implementation of better policies and disciplines cannot happen in a vacuum. It will rather proceed from a more informed debate and systematic sharing of good practices. Finally, participants commended global efforts carried out under the outstanding chairmanship of Turkey to improve the policy environment for investment, infrastructure and long-term finance; and called on the OECD together with other international organisations to enhance its contribution on international investment and trade in 2016 under the leadership of China.

Related News

Istanbul G20 Trade Ministers Meeting: Presentation of the OECD-WBG inclusive global value chains report

Presentation of the OECD-World Bank Group report, “Inclusive Global Value Chains: Policy options in trade and complementary areas for GVC integration by small and medium enterprises and low-income developing countries”, on 6 October 2015

Remarks by Angel Gurría, Secretary-General, OECD

Understanding global value chains is crucial to understanding trade and globalisation in today’s highly interconnected world, and to defining the policies that will help countries reap their full benefits in terms of growth and jobs.

I am honoured to be here today to present to you the findings of a new report prepared jointly by the OECD and the World Bank Group. Building on earlier reports that we have prepared under the Mexican, Russian and Australian G20 presidencies, this report goes deep into questions about how to strengthen the participation of small and medium sized enterprises and low-income developing countries in GVCs. I salute the wisdom and the commitment of Turkey in bringing these important issues into the limelight.

The foundation of our GVC analysis is our joint effort with the WTO to develop new trade statistics (TiVA) that identify the value added by each country along the value chain. We have just released a new version of the TiVA database, which extends coverage to 61 countries and 34 sectors. This new data shows that GVCs drive trade today, with 75% of global trade now comprised of intermediate inputs and capital goods and services. In addition, the data reveal that services are much more important in driving trade than we previously thought – over half of total trade is composed of value-added services in OECD countries, and 42% in China. These data reinforce earlier conclusions that imposing protectionist measures on imports is the trade policy equivalent of shooting yourself in the foot, causing costs of production to rise and damaging the competitiveness of exporting firms.

But not all countries, and not all firms, have had the same level of success integrating into GVCs:

-

Although their participation has greatly expanded in the past two decades, low-income developing countries (LIDCs) are still hugely under-represented in GVCs – only about 11% of the total world gross exports in 2011 (up from 6% in 1995). In particular, SMEs in LIDCs tend to be concentrated in the agriculture sector, or remain in the informal economy, and so have particular difficulties.

-