Search News Results

The dark side of globalization: Fighting illicit trade to safeguard integrity across economies, markets, and supply chains

Illicit Trade: fighting money laundering in international trade

Remarks by David M. Luna, Senior Director for National Security and Diplomacy Anti-Crime Programs, Bureau of International Narcotics and Law Enforcement Affairs, at a Working Session at the WTO Public Forum 2015 in Geneva

Good morning.

It is an honor to participate at this year’s Public Forum (“Trade Works”) under the auspices and leadership of the World Trade Organization (WTO). I would also like to thank the Government of Colombia for hosting our panel discussion this morning on how illicit trafficking globally harms international trade.

But first, I would like to congratulate the WTO for celebrating its 20th anniversary in 2015 and for its commitment over the years in helping to build and strengthen the rules-based global trading system. I very much agree that global trade has helped to boost growth markets, lift people out of poverty, increase access to goods and medicines, and in many ways, helped to promote “cultures of integrity” across economies, markets, and supply chains.

In that regard, I also want to congratulate the WTO and its members for the historic accomplishment of concluding the Trade Facilitation Agreement. And, like others have already done, I would urge all WTO Members to ratify the TFA as soon as possible. One of the reasons the TFA is so important is its recognition of the critical importance of risk management, of prioritizing and facilitating the flow of legitimate trade – the vast majority of trade. This has the critical effect of helping to focus scarce customs resources on detecting and stopping illicit trade. In a globalized world, where criminals are well-networked and organized, we should be too. Ensuring that we have the tools to counter such activities is more important than ever.

As Moises Naim underscored in his well-known book Illicit, “Global criminal activities are transforming the international system, upending the rules, creating new players, and reconfiguring power in international politics and economics.”

In too many places around the world, including in developing countries, criminals have built great empires on dirty money and laundered funds to infiltrate and corrupt government institutions. In this shadowy, illegal economy traffickers and narcotics kingpins act as CEOs and venture capitalists while they build their empires of destruction, jeopardizing public health, emaciating communities’ human capital, eroding our collective security, and destabilizing fragile governments.

Just to give you a snapshot of the breadth and scale of these illicit markets, various international organizations estimate the illegal economy accounts for 8 to 15 percent of world GDP, and in many developing countries, it may account for higher percentages in their economies. The WTO estimates that the value of counterfeit and pirated goods alone is equivalent to some 7% of the world’s merchandise.

This darker side of global trade is thriving with hundreds of billions of dollars in illicit commerce that includes trafficking in narcotics, persons, endangered wildlife, illegally-logged timber, counterfeit consumer goods and medications, hazardous and toxic waste, stolen antiquities and art, illicitly-traded cigarettes, and other illicitly-traded goods and commodities.

Simply put, illicit trade is an obstacle to shared prosperity, by breeding corruption and siphoning capital and human resources away from productive economic activity.

As societies grapple with insecurity and instability, illicit trafficking and corruption further decay any remaining sustainable pillars for development when governments cannot afford to provide vital public security and law enforcement because revenue streams from legitimate commerce are being siphoned away by corrupt officials, smugglers, and criminals.

Countries are also losing their human capital and economic potential when young men, women, and children are kidnapped, trafficked, exploited, or even murdered by a web of criminality and corruption.

Thus, the societal harms and impacts posed by illicit trafficking are very real.

Corruption helps to fuel this and enriches not only those bad actors and illicit networks behind today’s illegal economy but also enables corrupt police, customs, judicial, and other security officials who protect criminals and allow them to carry out their illicit trade.

I would also note that corruption contributes to slower growth, reduced foreign investment, and lower profits.

The OECD Task Force on Charting Illicit Trade, which I chair, is working on advancing international public-private partnerships and regional dialogues that help inform communities on the harms and impact of illicit trade. In joining this week’s Public Forum discussion in Geneva, I firmly believe that when the OECD, WTO, APEC, ASEAN, the United Nations, Interpol, leadings NGOs, and many other partners join forces, we can make a significant difference through collective action. Together, we can help impacted communities to combat the dark side of global trade and related corruption and money laundering.

We must continue to strengthen cross-border cooperation to tackle illicit trade and increasingly inter-connected global challenges, and help communities to fully seize the benefits of open trade to achieve great sustainable development and security. Of course, such cooperation should not impede the rules of the global trading system, but rather be consistent with them.

Pursuant to the questions posed to this panel, and in terms of pragmatic ideas and ways that we can devise strategies to confront these menaces. Coordinating international expertise in the quantification and mapping of illicit markets is a first step. This will enable a fuller understanding of the connections between different forms of trafficking. Concurrently, we need to support the experts in their analyses public policies that successfully increase economic and societal resilience to this threat. Then, we need to isolate elements of successful polices that can be disseminated to share with and emulated by other communities.

Moreover, to mitigate this global risk, public and private sector decision makers need a firmer grasp on the magnitude and nature of its impacts on economic activities, and a clearer understanding of the conditions that enable it. This can help to inform effective policy strategies and operational partnerships between the public and private sectors. The OECD TF-CIT will soon release a state-of-play report on the some of the global scale and impacts of illicit trade.

Additionally, in 2015-2016, the activity of the TF-CIT will continue to focus on:

-

Mapping the economic activities of transnational criminal networks, by gathering data on volume and flow of illegal trades and agreeing to common methodological approaches;

-

Examining the conditions and policies that encourage or inhibit different sectors of illegal trade, whether at the level of production, transit, or consumption;

-

Developing visualization tools to help public and private sector decision makers better target prevention and mitigation efforts in strategic markets; and embarking on campaigns to educate communities not to “buy into organized crime,” taking the profits away from criminals and protecting the public’s health and safety; and

-

Partner across borders through our regional dialogues including those that have taken place in Mexico, Thailand, and the Philippines, and meetings that we are keen to have in the Middle East, Europe, and Southeast Asia. We are partnering with INTERPOL, World Customs Organization (WCO), UNODC, International Chamber of Commerce (ICC), APEC, ASEAN, European Union, and many others.

Truly, the illegal economy poses an existential threat when it begins to create criminalized markets and captured states, which launches a downward, entropic spiral towards greater insecurity and instability.

The United States will continue to enhance international cooperation with key partners to combat the lethal nexus of organized crime, illicit trade, corruption, and money-laundering, and to protect communities from the violence, harm, and exploitation wrought by transnational threat networks. We will do this by enhancing our efforts to: break their corruptive power; attack their financial underpinnings; follow the money and strip them of their illicit wealth; and severe their access to the financial system.

At a time when global risks are growing and converging, the international community must come together and build our own “network of networks” to better understand the current and future turbulences of our world, and to coordinate responses and action.

Global trade, foreign investment, and economic development do create wealth and prosperity and finance economic freedoms around the world.

We must be vigilant, however, to secure these gains of globalization. Efforts to combat illicit activity should not create new barriers to legitimate trade. We must continue to shut down the illegal economy and criminalized markets, put criminal entrepreneurs and illicit networks out of business, and facilitate legitimate trade and enhance integrity across economies, markets, and supply chains.

That is why the WTO Trade Facilitation Agreement is so important. The TFA contains provisions for expediting the movement, release and clearance of goods, including goods in transit. It also sets out measures for effective cooperation between customs and other appropriate authorities on trade facilitation and customs compliance issues. It further contains provisions for technical assistance and capacity building in this area.

Beyond ratifying and implementing the TFA, countries should look to adopt international standards, best practices, and norms on criminalization, including those contained in the Financial Action Task Force (FATF) recommendations to combat money laundering and terrorist financing, and the UN Conventions against Transnational Organized Crime (UNTOC) and against Corruption (UNCAC) to reduce barriers to trade. As noted earlier, because criminals re-invest their illicit profits into other forms of organized crime and in the real economy, combating money laundering, and tracking and confiscating illicit funds are critical.

In closing, illicit trade harms the global trading system that the WTO and its members have worked so tirelessly to build.

If we do not work together, we will collectively destroy our chances of achieving a sustainable future for our children and grandchildren, lifting even more people out of poverty, and helping communities create a better world.

If we do, we can advance trade security as a powerful instrument to more smartly achieve these noble goals.

Thank you.

Related News

Reforms of International Investment Agreements should promote sustainable development goals

Speakers at the UNCTAD 62nd Trade and Development Board said that international investment agreements must preserve States’ abilities to adopt policies that support the SDGs. A better balance between the rights and obligations of investors and host States are needed, as are improved arbitration mechanisms.

Consensus among policymakers is that the international investment regime needs reform, asserted UNCTAD Secretary-General Mukhisa Kituyi during a roundtable discussion on 16 September 2015. The questions that remain, he explained, concern the extent of the reform and how best to implement it.

The discussion brought together representatives of governments, international organizations, academia and civil society. All agreed with Dr. Kituyi on the urgent need for reform, especially in light of the new global development agenda. Concerning the “what” and the “how” of reform, while different approaches have been adopted, the speakers concurred on the need to strike a better balance between the rights and responsibilities of foreign investors and host countries and to seek improved procedures, including alternative mechanisms to settle investment-related disputes.

Achieving the Sustainable Development Goals (SDGs) will require a surge in international investment, including private investment. This is because, according to UNCTAD estimates, an annual investment gap of US$ 2.5 trillion exists in key sectors in developing countries. But for private investment to support the SDGs, the discussion pointed out, international investment agreements (IIAs) must not limit governments’ right to regulate in areas related to the goals, such as environmental protection and public health. International Investment Agreements must go beyond simply promoting investment, they must foster sustainable development.

James Zhan, Director of UNCTAD’s Division on Investment and Enterprise, explained that in addressing the challenges as highlighted by Secretary-General Dr. Kituyi, UNCTAD has formulated the Investment Policy Framework for Sustainable Development to guide a new generation of investment policy making, and an Action Menu for reforming the existing investment treaty regime, which consists of nearly 3,300 international investment agreements (IIAs). These policy tool kits are now used by policy makers and treaty negotiators worldwide.

The extensive scope of the provisions is accompanied by an arbitration system that lacks transparency and legitimacy, according to several speakers.

Nathalie Bernasconi-Osterwalder, from the International Institute for Sustainable Development, called for the creation of an institutional mechanism at the regional or multilateral levels that would be detached from any one specific investment treaty. More importantly, she explained, it should allow for the participation of a wider array of affected or interested stakeholders and deal with issues raised by affected persons or communities.

The speakers commended UNCTAD for the 2015 World Investment Report, which, they said, offers an action menu for implementing investment reform, providing tools and options for countries to use to find their own way and approach for reform. They concluded by saying that they expect UNCTAD to continue to play a leadership role in this ongoing debate.

Related News

20 years on, negotiators reflect on breakthrough talks on intellectual property and trade

WTO Director-General Roberto Azevêdo launched a new publication entitled “The Making of the TRIPS Agreement: Personal Insights from the Uruguay Round Negotiations” on Day 2 of the Public Forum on 1 October 2015.

He highlighted that the WTO’s TRIPS (trade-related aspects of intellectual property rights) Agreement introduced substantive and comprehensive disciplines on IP rights into the multilateral trading system and that it has impacted deeply on national IP regimes around the world – with the most significant changes experienced in developing economies.

“The Making of the TRIPS Agreement”, co-edited by Jayashree Watal and Antony Taubman, presents for the first time the diverse personal accounts of the negotiators of this unique trade agreement. Their rich contributions illustrate how different policy perspectives and trade interests were accommodated in the final text, and map the shifting alliances that transcended conventional boundaries between developed and developing countries, with a close look at issues such as copyright for software, patents on medicines and the appropriate scope of protection of geographical indications.

In launching the publication, DG Azevêdo said:

“This book is not just one for IP specialists; and it is not meant to be a book about the law of TRIPS. Instead, by describing the practical process of the making of the Agreement, and by explaining the working methods and negotiating techniques that were developed – or often improvised – it offers real insights.

“I think these insights are valid even today for those who wish to learn how such a potentially divisive subject could be negotiated to a successful conclusion. It therefore offers a rare insider’s account of the craft of international negotiations.

“The insights in this volume are not only of deep historic interest – they will also serve as an inspiration for success in future negotiations in other such complex and sensitive areas.”

His full speech is available here.

In the book, the contributors share their views on how intellectual property fitted into the overall Uruguay Round, the political and economic considerations driving TRIPS negotiations, the role of non-state actors, the sources of the substantive and procedural standards that were built into the TRIPS Agreement, and future issues in the area of intellectual property.

In probing how negotiations led to an enduring agreement that has served as a framework for policymaking in many countries, the contributions offer lessons for current and future negotiators. The contributors highlight the enabling effect of a clear negotiating agenda, and underscore the important, but distinct, roles of the Chair, of the Secretariat and above all, of the negotiators themselves.

Speaking at the launch, Antony Taubman said that “TRIPS has been proven to be an unexpectedly resilient and effective framework for balanced, good governance in the IP domain. The negotiations have shown us the benefits of taking an intellectually curious and inclusive approach to learning about technical issues under negotiation – an approach that is all the more valuable today as we seek together to learn from diverse experience working with TRIPS in over 130 jurisdictions”.

Jayashree Watal added: “The book makes no claim to present the authentic negotiating history of the TRIPS agreement, nor a guide to interpretation of its provisions. It merely presents as its title says – personal insights – from those who were involved in the negotiations.”

Related News

TTIP and beyond: EU trade policy in the 21st century

Trade Commissioner Cecilia Malmström spoke on the future of Trade policy at New York’s Columbia University on 25 September. She called for a trade policy based on economic effectiveness and broader responsibility. Agreements like TTIP should address today’s economic issues, like services and digital trade. They also need to respect values like a high level regulatory protection and sustainable development.

I’m delighted to join you today.

Columbia Law School and the School of International and Public Affairs are both top class departments at a global level. So I’m looking forward to our discussion.

But I hope you’ll indulge me for a few moments so I can give you a sense of some of the issues we are dealing with in EU trade policy.

The title of this event is, “TTIP and Beyond: EU Trade Policy in the 21st Century.”

It gives a pretty accurate picture of my work at the moment.

Because in the public debate in the European Union today, trade policy is almost synonymous with the Transatlantic Trade and Investment Partnership.

And that’s understandable. But of course TTIP is in fact just a part – the biggest part but a part nonetheless – of our wider efforts on trade.

We are using a full range of trade policy tools to boost our economy and help us adapt to a changing world. We are working on more than 20 agreements with more than 60 countries across the Americas, Asia and Africa.

So I’d like to also give you a flavour of the “Beyond” part our trade agenda as well.

And I’d like to do that by looking at trade policy’s two biggest challenges: effectiveness and responsibility.

By effectiveness I mean that trade policy needs to work. To do that we must adapt to economic realities.

Trade is no longer just about finished products. Through global value chains, trade and investment have become part of the production process itself.

Some experts do argue that the growth of these chains has slowed in recent years. That may be cyclical or it may be permanent. It’s too soon to say.

But either way the linkages that have been forged in recent years require us to adapt. If we want to be competitive we have facilitate this value chain trade.

Trade policy also needs to take account of changes in the nature of cross-border flows. In the past, goods were far and away the most significant component. They are still vital.

-

But we now also need to look at services – from transport, to finance, to technical support.

-

We need to address investment.

-

We need to address the rise of the digital economy, which means data flows also need to be part of the equation.

-

We need to deal with the fact that people often now need to cross borders in order for trade to happen.

-

And trade policy also needs to adapt in order to broaden the base of companies that take advantage of trade agreements. 30% of European exports are by small and medium sized enterprises or SMEs. But it’s still true that most SMEs don’t export. We have room for improvement.

What are we doing about these facts?

The best way to facilitate value chain trade is multilateral trade liberalisation through the World Trade Organisation. It caters for the fact that inputs may cross multiple borders multiple times:

-

The EU is working hard with the US and others to deliver a result at the Nairobi Ministerial Conference at the end of the year.

-

We are also making progress on a range of targeted negotiations with groups of WTO members on issues like information technology equipment, services and green goods.

-

And we know we need to start thinking about what happens after the Doha Round is finished as well.

But we also need to keep multilateralism in mind when we negotiate our bilateral and regional free trade agreements.

TTIP is a particularly good example. It covers around 40% of the global economy already.

It is also important because it is ambitious.

Our aim is an advanced set of rules on issues like state-owned enterprises, localisation requirements, raw materials and energy. We are also trying to break new ground in international regulatory cooperation – in general and for 9 specific sectors including pharmaceuticals, cars and cosmetics.

The results of these efforts could serve as models for future global solutions to these issues. So through the bilateral we are preparing the ground for future multilateral work.

Moreover, an ambitious TTIP outcome on issues like services, digital trade and mobility, would help set precedents for tackling these issues in a way that fits with today’s economic realities. And TTIP will be the first agreement where the EU negotiates dedicated provisions to help SMEs benefit as much as possible.

TTIP should be our most ambitious agreement but in all the EU’s free trade agreements we seek to be as ambitious as possible – to make sure they are adapted today’s realities – and that they work. Our agreement with Korea has helped EU exports rise by more than 50% since it entered into force. Our 3 recent deals with Canada and Vietnam are also ground-breaking in different ways. That’s how we mean to go on.

We also need to think collectively about how bilateral agreements relate to each other. One example of where we’ve done this in is Latin America. We’ve had an agreement in place with Colombia and Peru for several years. And last year we reached a political deal with Ecuador that would allow it to accede to that agreement. That’s something we may wish to look at for other agreements as well, including, potentially, TTIP.

The second theme I want to talk about is responsibility.

Trade will always be fundamentally an economic policy. But it is not an island. The choices we make about trade must reflect our values.

This is not just an abstract wish. Over the last two years the public debate around trade policy has intensified – and not just in Europe. Much of the concern is essentially a call to greater responsibility.

Policy makers in democratic systems have to listen to that debate, understand it and respond to it.

Here again TTIP is at the forefront, not least because – in Europe at least – it is the most controversial.

I see this debate as an opportunity to look hard at some of our approaches and update them where needed.

One issue is about the way we negotiate. When trade deals cover issues like regulation on safety, health and the environment, people need to trust that we are not lowering standards.

If we want their trust we need to be more open. That’s why the EU now publishes our TTIP negotiating proposals on these issues. And why we are now assessing whether to apply this to other negotiations as well.

Responsibility is also about substance. For example, investment protection is one of the most intense issues in the TTIP debate in Europe.

There is considerable concern about the possibility for investors to take cases against governments.

The Commission listened to the debate in civil society and among national and European political representatives. We have – just last week – published our proposals for a new system.

We believe it keeps what is good about investment protection – it reduces risk and therefore encourages job-creating investment.

But it also makes clear that governments can make policy in the public interest.

And it turns an arbitration system that needed reform into a transparent courts system that citizens can trust.

This new approach – once agreed within the EU – will also serve as the basis for our investment deals in the future. So here again we have a result from TTIP that has wider impacts.

There is a second strand to the public debate on responsibility in trade – less linked to TTIP but no less important. And that’s the fact that consumers today are more concerned about the social and environmental footprint of the products they buy from abroad.

That is good news, as far as I’m concerned. Trade – like any other international policy – should help put our principles into practice. That goes for development of poor countries, human rights, labour rights and protecting the environment.

Trade policy makers around the world have increasingly come to this view in recent decades. The EU has also played its part:

-

We offer advanced preference schemes for developing countries and free access for the products of least developed countries.

-

We have also concluded a series of Economic Partnership Agreements with developing countries in Africa, the Caribbean and Pacific.

-

Along with our Member States, we are the most significant provider of the Aid for Trade that helps countries take advantage of these opportunities.

-

And the sustainable development rules of our free trade agreements encourage countries to respect the core conventions of the International Labour Organisation and the key international conventions.

I believe we need to do more.

-

For example, we should have ambitious provisions on labour and the environment in TTIP…

-

We should give more support to fair and ethical trade schemes…

-

And we can do more to promote responsible supply chain management by companies.

The Commission will be talking about these and other issues in a new trade strategy document released very soon.

I hope this gives you an overview about the issues facing trade policymakers.

Resolving them will require hard work and political will from Europe and our partners around the world.

It will also need creative thinking, not only from within government but also the academic community.

So, no pressure but I hope to hear some of those from you today! Thank you.

Related News

tralac’s Daily News selection: 1 October 2015

The selection: Thursday, 1 October

Entering uncharted waters: El Niño and the threat to food security (Oxfam)

Millions of poor people in Southern Africa, Asia and Central America face hunger and poverty this year and next because of droughts and erratic rains as global temperatures reach new records, and because of the onset of a powerful El Niño – the climate phenomenon that develops in the tropical Pacific and brings extreme weather to several regions of the world. The combination of record warmth one year followed by an El Niño the next is unique and the climatic implications are uncertain. If 2016 follows a similar pattern, we are entering uncharted waters.

Perhaps the greatest problems may occur in Southern Africa. The annual rains across Southern Africa are notoriously fickle and in addition, borderline El Niño conditions were prevalent by late last year. The rains that fell from October/November 2014 through to February 2015 were very erratic, starting a month or more late, and then from mid-December through January 2015, they were extraordinarily heavy and brought unusually extensive flooding to southern Malawi and northwest Mozambique. Zimbabwe suffered particularly poor rains. [The author: John Magrath]

Can intra-regional trade act as a global shock absorber in Africa? (Africa at LSE)

Several important issues remain for future research. First is gaining a better understanding of the relationship between regional integration and intra-regional trade and how to strengthen multilateral trade ties. Our results should not be interpreted as support for regional integration via preferential regional trade agreements at the expense of multilateral trade. Second, we have focused on the transmission of shocks from the advanced economies to Africa, leaving the impact of shocks in emerging markets on Africa to further investigation. Finally, future research could examine channels through which intra-regional trade facilitates diversification and integration of African RECs into global value chains. [The authors: Zuzana Brixiová, Qingwei Meng, Mthuli Ncube]

Informal trade flows in the EAC (Global Trade Review)

Speaking at GTR’s East Africa Trade & Commodity Finance Conference, Ecobank’s head of group research, Edward George, surmised that informal trade represents 30 to 40% of the EAC’s trade flows, affecting the competitiveness of the region’s formal traders. In this excerpt from his presentation, he questions who and what is driving this illicit activity and what hopes East Africa has for the future of trade.

Unlocking the trade potential of a continent on the move (Africa Outlook)

With a potential slowdown in China refocusing attention on SSA’s future growth and trading partners, Barclays has studied trade openness and market opportunity across SSA to provide a comparative perspective on the opportunities ahead. The research demonstrates: [The author, John Winter, is Barclays’ Corporate Banking CEO]

Business and the Sustainable Development Goals (Business Fights Poverty)

South Africa: August 2015 merchandise trade statistics (SARS)

The R9.95bn deficit for August 2015 is due to exports of R87.63bn and imports of R97.58bn. Exports decreased from July 2015 to August 2015 by R5.45bn (5.9%) and imports increased from July 2015 to August 2015 by R3.38bn (3.6%). The cumulative deficit for 2015 is R36.27bn compared to R69.94bn in 2014. Africa trade surplus: R15 330 million – this is a 6.9% decrease in comparison to the R16 464 million surplus recorded in July 2015. Trade statistics with the BLNS for August 2015 recorded a trade surplus of R9.12 billion.

US-South Africa trade dispute risks $1.7bn of exports (Bloomberg)

“South Africa needs to take concrete steps towards eliminating barriers to US trade and investment, a key criterion to be eligible for AGOA trade benefits,” Trevor Kincaid, a spokesman for the office of the U.S. Trade Representative in Washington, said in an e-mailed response to questions on Wednesday. “Ultimately, South Africa’s AGOA eligibility is in South Africa’s hands.”

Congressmen bewail SA’s trade ‘barriers’ (Business Day)

New AGOA apparel quota cap for 2015-2016 announced (AGOA.info)

DTI to lead an outward selling and investment mission to Zambia (Cape Business News)

The Department of Trade and Industry will lead a delegation of 38 business people to participate on an Outward Selling and Investment Mission to Zambia. The mission will take place from 6-8 October 2015 in Lusaka, Zambia. “Trade between South Africa and Zambia has increased from over R15bn in 2011 to more than R28bn in 2014. South Africa is Zambia’s main trading partner in the Southern African Development Community region, whilst Zambia is South Africa’s fourth trading partner,” says Davies.

Zimbabwe: Dairy producers want duty on inputs scrapped (NewsDay)

Dairy producers have called on government to scrap import duties on inputs which are not locally available to ensure that prices of final products are competitive in the region. Dendairy director Daryl Archibald told a delegation from the Office of the President and Cabinet (OPC) which toured the company’s Kwekwe plant on Tuesday that Zimbabwe’s milk products were failing to compete locally because of the heavy duty imposed by the Zimbabwe Revenue Authority on inputs such as packaging and other machinery imported by dairy companies. “If the government wants us to just produce for the local market it’s fine, but if we have to go into exports, we ask that they do not charge any duty on any product that is not available locally because even duty of 5% would make us lose the market to South Africa in the region,” he said.

Formalisation of informal economy (NewsDay)

Malawi to implement new visa regime from October 1st (StarAfrica)

Malawi through its Immigration Department will start implementing its new visa regime from 1st October whereby all foreign nationals will require to pay visas fees ranging from $50 to $100 to enter the Southern African country. Minister of Home Affairs and Internal Security, Jean Kalirani told reporters in the capital Lilongwe on Tuesday that the new regime is required from nationals of all countries except Southern African Development Community (SADC) countries except Angola, Common Market for Eastern and Southern Africa (COMESA) countries, diplomats and government officials. “Nationals from all countries that do not require Malawian nationals to pay visa fees when travelling to such nations will not pay to enter Malawi,” she added.

Falling import demand, lower commodity prices push down trade growth prospects (WTO)

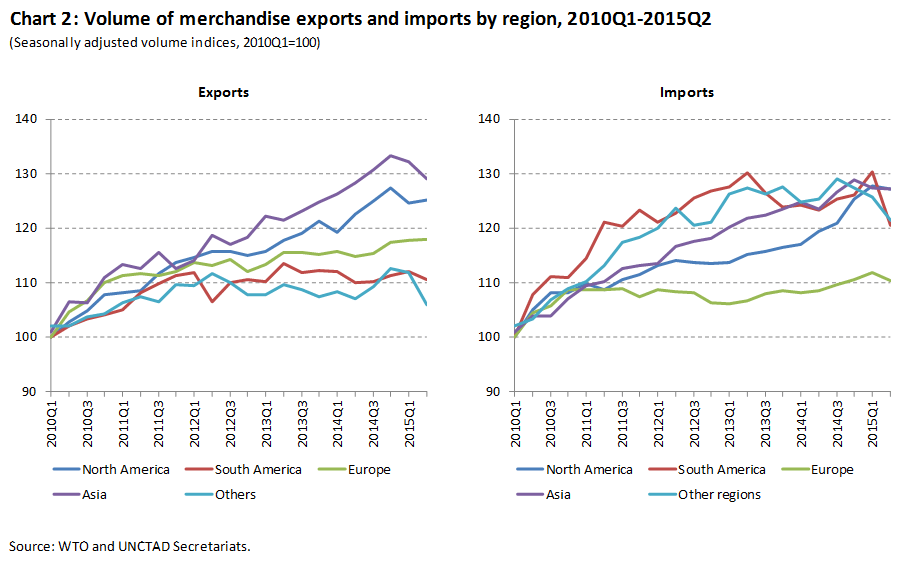

WTO economists have lowered their forecast for world trade growth in 2015 to 2.8%, from the 3.3% forecast made in April, and reduced their estimate for 2016 to 3.9% from 4.0%. These revisions reflect a number of factors that weighed on the global economy in the first half of 2015, including falling import demand in China, Brazil and other emerging economies; falling prices for oil and other primary commodities; and significant exchange rate fluctuations. Trade growth remains uneven across countries and regions as illustrated by Chart 2, which shows WTO merchandise trade volume indices by geographical region.

More collaboration is needed to ensure the benefits of trade are enjoyed by all, panellists agreed at the plenary debates of the WTO’s 2015 Public Forum on 30 September. The need for multilateral cooperation among governments was highlighted in the opening plenary debate while the importance of public-private sector dialogue was underlined in the afternoon debate on making trade work for business. [The Forum www]

WTO accessions and trade multilateralism: case studies and lessons from the WTO at Twenty (WTO)

Ethiopia: IMF concludes 2015 Article IV Consultation (IMF)

Noting a softening of export activity, Directors recommended more decisive action to strengthen the business climate and enhance external competitiveness. Greater exchange rate flexibility, less burdensome regulation, and easier private sector access to credit and foreign exchange would be steps in the right direction. Opening some strategic sectors to foreign investment could also improve the provision of critical services.

Bullish Ethiopia and Djibouti agree on $1.55Bn pipeline; Kenya’s LAPSSET has reason to worry (M&G Africa)

Germany commits 37 million Euros to support regional integration in East Africa (EAC)

Delivering on the promise: Leveraging natural resources to accelerate human development in Africa (AfDB/Gates Foundation)

In the light of these challenges, this report makes three fresh contributions on how to leverage oil, gas, and mineral resources to accelerate human development progress in Africa. First, it provides a broad estimate of the possible magnitude and timing of potential new extractives revenues in Ghana, Liberia, Mozambique, Sierra Leone, Tanzania, and Uganda – six countries that have recently discovered significant oil, gas, or mineral resources. Second, it presents a practical policy framework for helping governments to better link their revenue management decisions to their human development agendas. Third, it highlights ways to leverage extractives companies’ direct spending, including procurement and employment throughout the lifecycle of extractives projects, to ensure businesses and individuals are ready to harness the benefits. [Download]

This research was inspired by a major conclusion of the 2013 African Economic Outlook on natural resources and structural transformation. The Outlook’s cross-country analysis stated that, while dependence on natural resources poses serious challenges, natural resource abundance is associated with positive outcomes such as long-term growth. By analysing the correlations among export diversification patterns of unprocessed, semi-processed and finished goods, this paper indicates that broadening the array of exported unprocessed commodities is a good predictor of higher manufacturing diversification. And, it is sometimes a first step towards industrialisation for many poor countries. This important conclusion makes a compelling case for inviting more low-income countries to join the OECD Development Centre’s ongoing Policy Dialogue on Natural Resources.

ALSF catalysing Uganda’s extractive resource sector (AfDB), Tanzania: New database launched for openness in gas, oil sector (The Citizen), Commodity exporters facing the difficult aftermath of the boom (IMF)

UN Office for Coordination of Humanitarian Affairs migration debate (UN News Centre)

As the world confronts the biggest refugee and migration crisis since the Second World War, Secretary-General Ban Ki-moon convened a high-level meeting on the issue and outlined eight guiding principles to improve preparedness.

Malaysia ramping up in Africa (Institute of Southeast Asian Studies)

Apart from South Africa, major trade partners for the export of Malaysia goods in 2014 included Kenya at $737m, Angola at $585m and Nigeria at $389m. The largest trade partners for the import of Africa goods, on the other hand, are concentrated in West Africa, with the highest ranking being Cote d’Ivoire at $355m, Ghana at $346m and Algeria at $310m

Dubai Chamber reviews investment potential of East African markets (CPI Financial)

WTO issues panel report on Argentinian financial, tax and forex measures affecting trade

Overview of INDCs submitted by 31 August 2015 (OECD)

AECF: African youths pivotal to agric business (Vanguard)

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome. Richard Humphries (Email: This email address is being protected from spambots. You need JavaScript enabled to view it.; Twitter: @richardhumphri1)

Related News

South Africa Merchandise Trade Statistics for August 2015

The South African Revenue Service (SARS) has released trade statistics for August 2015 that recorded a trade deficit of R9.95 billion. This figure includes trade data with Botswana, Lesotho, Namibia and Swaziland (BLNS).

Including trade data with Botswana, Lesotho, Namibia and Swaziland (BLNS)

The R9.95 billion deficit for August 2015 is due to exports of R87.63 billion and imports of R97.58 billion. Exports decreased from July 2015 to August 2015 by R5.45 billion (5.9%) and imports increased from July 2015 to August 2015 by R3.38 billion (3.6%).

The cumulative deficit for 2015 is R36.27 billion compared to R69.94 billion in 2014.

The month of July 2015 trade balance was revised downwards by R0.72 billion from the previous month’s preliminary deficit of R0.40 billion to a revised deficit of R1.11 billion.

Trade highlights by category

The month-on-month export movements:

| R’ million | ||

| Section: | Including BLNS: | |

| Mineral Products | - R4 205 | - 20.1% |

| Base Metals | - R2 464 | - 20.0% |

| Precious Metals & Stones | + R1 120 | + 7.3% |

| Vehicle & Transport Equipment | + R 382 | + 3.4% |

| Wood and articles thereof | + R 176 | + 41.2% |

The month-on-month import movements:

| R’ million | ||

| Section: | Including BLNS: | |

| Vehicle & Transport Equipment | + R2 027 | + 22.1% |

| Mineral Products | + R1 758 | + 12.1% |

| Chemical Products | + R1 248 | + 12.4% |

| Equipment Components | - R 743 | - 9.4% |

| Base Metals | - R 681 | - 12.8% |

Trade highlights by world zone

The world zone results from July 2015 to August 2015 are given below.

Africa:

Exports: R26 195 million – this is a decrease of R 0.28 million from July 2015

Imports: R10 865 million – this is an increase of R1 106 million from July 2015

Trade surplus: R15 330 million – This is a 6.9% decrease in comparison to the R16 464 million surplus recorded in July 2015.

America:

Exports: R8 015 million – this is a decrease of R1 099 million from July 2015

Imports: R10 947 million – this is an increase of R 941 million from July 2015

Trade deficit: R2 932 million – This is an increase in comparison to the R 892 million deficit recorded in July 2015.

Asia:

Exports: R24 773 million – this is a decrease of R3 111 million from July 2015

Imports: R43 883 million – this is an increase of R1 599 million from July 2015

Trade deficit: R19 110 million – This is a 32.7% increase in comparison to the R14 399 million deficit recorded in July 2015.

Europe:

Exports: R21 371 million – this is a decrease of R 720 million from July 2015

Imports: R30 502 million – this is a decrease of R 332 million from July 2015

Trade deficit: R9 131 million – This is a 4.4% increase in comparison to the R8 743 million deficit recorded in July 2015.

Oceania:

Exports: R1 164 million – this is a decrease of R 162 million from July 2015

Imports: R1 300 million – this is an increase of R 203 million from July 2015

Trade deficit: R 135 million – This is a deterioration compared to the R 229 million surplus recorded in July 2015.

Excluding trade data with Botswana, Lesotho, Namibia and Swaziland (BLNS)

The trade data excluding BLNS for August 2015 recorded a trade deficit of R19.07 billion. The deficit is as a result of exports of R75.93 billion and imports of R95.00 billion. Exports decreased from July 2015 to August 2015 by R5.83 billion (7.1%) and imports increased from July 2015 to August 2015 by R3.31 billion (3.6%).

The cumulative deficit for 2015 is R105.59 billion compared to R135.91 billion in 2014.

Trade highlights by category

The month-on-month export movements:

| R’ million | ||

| Section: | Excluding BLNS: | |

| Mineral Products | - R4 131 | - 21.8% |

| Base Metals | - R2 365 | - 20.7% |

| Vehicle & Transport Equipment | + R 434 | + 4.5% |

| Precious Metals & Stones | + R 282 | + 1.9% |

| Wood and articles thereof | + R 189 | + 71.3% |

The month-on-month import movements:

| R’ million | ||

| Section: | Excluding BLNS: | |

| Vehicle & Transport Equipment | + R2 019 | + 22.0% |

| Mineral Products | + R1 760 | + 12.2% |

| Chemical Products | + R1 239 | + 12.9% |

| Equipment Components | - R 743 | - 9.4% |

| Base Metals | - R 677 | - 12.9% |

Trade highlights by world zone

The world zone results from July 2015 to August 2015 are given below.

Africa:

Exports: R14 495 million – this is a decrease of R 405 million from July 2015

Imports: R8 286 million – this is an increase of R1 039 million from July 2015

Trade surplus: R6 209 million – This is an 18.9% decrease in comparison to the R7 654 million surplus recorded in July 2015.

Botswana, Lesotho, Namibia and Swaziland (Only)

Trade statistics with the BLNS for August 2015 recorded a trade surplus of R9.12 billion. The surplus is as a result of exports of R11.70 billion and imports of R2.58 billion. Exports increased from July 2015 to August 2015 by R0.38 billion (3.3%) and imports increased from July 2015 to August 2015 by R0.07 billion (2.7%).

The cumulative surplus for 2015 is R69.32 billion compared to R65.98 billion in 2014.

The month-on-month export movements:

| R’ million | ||

| Section: | BLNS: | |

| Precious Metals & Stones | + R 837 | + 4812.3% |

| Base Metals | - R 99 | - 11.4% |

| Chemical Products | - R 96 | - 9.1% |

| Mineral Products | - R 74 | - 3.8% |

| Vehicle & Transport Equipment | - R 52 | - 3.7% |

The month-on-month import movements:

| R’ million | ||

| Section: | BLNS: | |

| Precious Metals & Stones | + R 60 | + 25.6% |

| Machinery and Electronics | + R 28 | + 10.8% |

| Live Animals | - R 19 | - 5.8% |

| Raw Hides & Leather | - R 14 | - 37.0% |

| Plastics & Rubber | - R 10 | - 25.5% |

Related News

WTO Public Forum: Plenary debates on Day 1 highlight need for collaboration to make trade more inclusive

More collaboration is needed to ensure the benefits of trade are enjoyed by all, panellists agreed at the plenary debates of the WTO’s 2015 Public Forum on 30 September. The need for multilateral cooperation among governments was highlighted in the opening plenary debate while the importance of public-private sector dialogue was underlined in the afternoon debate on making trade work for business.

“Trade works,” Director-General Roberto Azevêdo said in his welcome address, “if it is accompanied by the right policies, if countries are supported to build the capacity they need to compete, and if we have a transparent system of rules which are agreed together and are enforced in a fair, open and cooperative way.”

“We need all of you to make sure the trading system will work for everyone,” Lilianne Ploumen, Minister for Foreign Trade and Development Cooperation of the Netherlands, said in her keynote speech. “I do hope that with our mutual commitments and with combined efforts we can help achieve equal opportunities for all.”

Opening plenary debate

Lerato Mbele, the moderator, opened the debate by noting that while trade indeed works, the benefits are not shared by all in the same way.

Panellists began the discussion by defining inclusivity. Yuejiao Zhang, Appellate Body member, said this meant getting equal access through the WTO’s most favoured nation principle and special and differential treatment for poorer countries.

Anabel Gonzàlez, Senior Director for Trade and Competitiveness Global Practice at the World Bank Group, emphasized the need to include people in rural areas, conflict zones, and the informal sector as well as women.

Susan Schwab, former United States Trade Representative, said consideration must be made for everyone from production to consumption.

Ms. Ploumen said inclusivity meant all players have access to the formal system with formal rules.

DG Azevêdo said inclusivity was important both at a geographical as well as an individual level.

Amina Mohamed, Cabinet Secretary for Foreign Affairs of Kenya, emphasized that developing countries and least-developed countries (LDCs) should be given attention.

The panellists discussed the benefits delivered by trade and the WTO; however, they also noted that benefits are not automatic to all. “This trickle down effect – forget about it. It only happens when we have policies to make sure everyone benefits,” Ms Ploumen said.

The panellists agreed that the prospects were even more worrying considering the current economic uncertainty. “We should be worried. I am concerned about the situation we are in,” Ms Schwab said, adding that trade and trade policy had the potential to be a “force multiplier” to deliver outcomes for women, youth, the environment, and other disadvantaged sectors. DG Azevêdo similarly said that, having exhausted fiscal and monetary policy, governments should explore using trade policy to turn around the slowdown and deliver gains to all.

To move forward, various policy options were discussed. Ms Gonzàlez and Ms Mohamed, for instance, emphasized the importance of domestic policy to improve an economy’s business climate, competitiveness and connectivity to regional and global trade.

On subsidies, Ms Zhang and Ms Mohamed noted the need for special and differential treatment for poorer countries while Ms Ploumen added that some developing economies have grown considerably since subsidies were first being negotiated and that talks need to reflect these changes.

On the environment, there were mixed views on whether stricter standards to address climate change were helping or hindering poorer economies.

Panellists agreed, however, that collaboration among governments on a multilateral level is necessary. “All these perceptions are valid. The good thing is the common thread,” said DG Azevêdo. “We need collaborative efforts.”

Afternoon plenary debate

The afternoon plenary debate focused on the relationship between trade and business, including small and medium enterprises (SMEs) and agribusiness.

DG Azevêdo opened the session by taking stock of what the WTO has accomplished for the business sector through efforts like the Aid for Trade initiative (which assists developing countries and LDCs export), the Trade Facilitation Agreement (which seeks to improve the ease of doing business at the border), the plan to eliminate tariffs on more information technology (IT) products through the expanded Information Technology Agreement and the plurilateral Environmental Goods Agreement in the pipeline.

“In recent years the WTO has shown that it can deliver agreements with real economic impact,” DG Azevêdo said. “Now we need the support of the business community to move ahead once again. The record shows that when we join forces – the private sector and governments in the WTO – we can achieve a great deal,” he said.

Harold McGraw III, chairman of the International Chamber of Commerce, echoed this by noting that the cooperation between governments and businesses is essential. “Government establishes policy but business is the one that executes it. They need to be on both sides of the coin,” he said. Mr McGraw further noted the importance of attracting investment to create growth and jobs as well as the significance of business organizations to help exchange information between government and the private sector.

Roland Auschel, Adidas board member in charge of global sales, discussed the importance of ironing out trade policy. “The reality today is that we’re still held by trade barriers, delays in importation and so on. We aren’t delivering on our consumer promise today,” he said. For Mr Auschel, cost and time are important factors that businesses consider as they integrate more and more into global value chains (GVCs).

Commenting on the GVCs, Gregory Doming, Trade Minister from the Philippines, noted that while integrated assembly lines are valuable for bringing in more businesses into trade, it is also important to consider alternatives for helping micro and small enterprises participate and export directly.

“The mind set has been from the perspective of large enterprises and this locks out micro and small businesses from international trade,” he said. “I’m saying GVCs are very useful but we have to add on to this. We need more pipelines for them to directly export.”

Evelyn Nguleka, President of the World Farmers’ Organization, meanwhile emphasized the importance of trade to farmers and agribusiness. Trading results in the balance of resources, she said. “There are certain areas of the world where there is more of a resource than the other. We need a scenario where it is possible and efficient and everyone can participate.” To accomplish this, however, the playing field needs to be more level in the case for instance of financing for poorer farmers.

At the close of the plenary, the moderator Ms Mbele asked each panellist whether trade works for business. Messrs McGraw, Auschel, Domingo and Ms Nguleka answered in the affirmative. When asked whether the WTO will do all it can to ensure this, DG Azevêdo replied: “Yes, if members let us.”

Related News

Falling import demand, lower commodity prices push down trade growth prospects

WTO economists have lowered their forecast for world trade growth in 2015 to 2.8%, from the 3.3% forecast made in April, and reduced their estimate for 2016 to 3.9% from 4.0%.

These revisions reflect a number of factors that weighed on the global economy in the first half of 2015, including falling import demand in China, Brazil and other emerging economies; falling prices for oil and other primary commodities; and significant exchange rate fluctuations.

Volatility in financial markets, uncertainty over the changing stance of monetary policy in the United States and mixed recent economic data have clouded the outlook for the world economy and trade in the second half of the year and beyond.

If current projections are realised, 2015 will mark the fourth consecutive year in which annual trade growth has fallen below 3 per cent and the fourth year where trade has grown at roughly the same rate as world GDP, rather than twice as fast, as was the case in the 1990s and early 2000s.

“Trade can act as a catalyst for economic growth. At a time of great uncertainty, increased trade could help reinvigorate the global economy and lift prospects for development and poverty alleviation. WTO members can help to set trade growth on a more robust trajectory by seizing the initiative on a number of fronts, notably by negotiating concrete outcomes by our December Ministerial Conference in Nairobi,” Director-General Roberto Azevêdo said.

Global output is still expanding at a moderate pace but risks to the world economy are increasingly on the downside. These include a sharper-than-expected slowdown in emerging and developing economies, the possibility of destabilizing financial flows from an eventual interest rate rise by the US Federal Reserve, and unanticipated costs associated with the migration crisis in Europe.

At the time of our last forecast in April 2015, world trade and output appeared to be strengthening based on available data through 2014Q4. However, results for the first half of 2015 were below expectations as quarterly growth turned negative, averaging ‑0.7% in Q1 and Q2. Recent trade developments are illustrated in Chart 1, which shows seasonally-adjusted, quarterly merchandise trade indices in volume terms (i.e. adjusted to account for fluctuations in prices and exchange rates) by level of development.[1] Despite the quarterly declines in the first half of 2015, year-on-year growth in trade for the year to date remains positive at 2.3%.

Quarterly export growth of developed economies was essentially flat in the first two quarters of 2015 (-0.2% on average in Q1 and Q2), but those of developing countries were more negative (‑1.9%). The drop in exports was driven by weaker developing countries’ imports (-2.2%) and stagnation in developed countries’ imports (+0.1%).

Trade growth remains uneven across countries and regions as illustrated by Chart 2, which shows WTO merchandise trade volume indices by geographical region. After a long period of stagnation, Europe recorded the fastest year-on-year export growth of any region in Q2 at 2.7%, followed by North America (2.1%), Asia (0.6%), South and Central America (0.4%) and Other Regions (-1.0%, including Africa, the Commonwealth of Independent States and the Middle East). Disparities between regional growth rates was stronger on the import side than on the export side, with positive growth of 6.5% in North America, 3.1% in Asia and 1.6% in Europe, and declines of 2.3% in South and Central America and 3.1% in Other Regions.

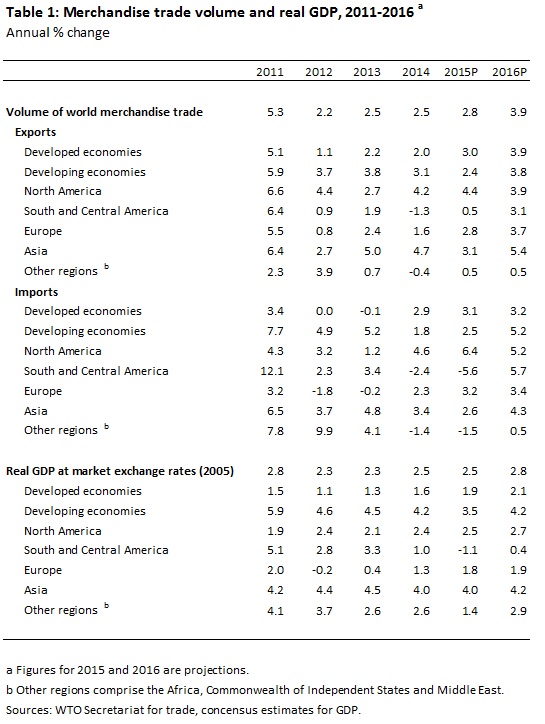

Table 1 shows revised trade projections for 2015 and 2016, which depend on consensus estimates of world real GDP growth at market exchange rates. The WTO now expects world merchandise trade volume as measured by the average of exports and imports to grow 2.8% in 2015 and 3.9% in 2016. On the export side, shipments from developed economies should rise 3.0% this year and 3.9% next year. Developing economies’ exports are expected to grow more slowly at 2.4% in 2015 and 3.8% in 2016. Imports of developed economies should increase at around the same rate in 2015 (3.1%) and in 2016 (3.2%), while those of developing economies pick up from 2.5% this year to 5.2% next year.

The strongest downward revision to the previous export forecast for 2015 was applied to Asia, where our estimate was lowered to 3.1% from 5.0% in April. This is mostly due to falling intra-regional trade as China’s economy has slowed. The downward revision to Asia on the import side was even stronger, from 5.1% to 2.6%, partly due to lower Chinese imports which were down 2.2% year-on-year in Q2 (non-seasonally adjusted data). The product composition of China’s merchandise imports suggests that some of the slowdown may be related to the country’s ongoing transition from investment to consumption led growth. Large year-on-year drops in quantities of imported machinery (-9%) and metals (iron and steel -10%, copper ‑6%) were recorded in customs statistics for August, while strong increases were recorded for agricultural products including cereal grains (+130%) and oilseeds (+33%).

Another noteworthy revision relates to the import forecast for South and Central America in 2015, which was lowered to -5.6% from -0.5% in April. Much of this reduction can be attributed to adverse economic developments in Brazil, which has been simultaneously hit by a fiscal crisis, a financial scandal involving the country’s largest company, and falling export prices. Brazil’s merchandise imports in Q2 were down 13% year-on-year compared to the same period in 2014. A rebound in imports of South and Central America is expected in 2016 as Brazil’s GDP growth stabilizes and its imports start to recover. Other countries in the region should also see imports accelerate as their economies pick up next year. The size of the rebound in 2016 is also partly explained by the fact that future growth will be proceeding from a lower base following the steep decline in 2015.

If the slowdown in emerging markets worsens the revised forecasts in Table 1 could still prove to be overly optimistic. In particular, a slower rebound from recent declines in developing economies’ imports could shave half a percentage point off of global trade growth in 2015.

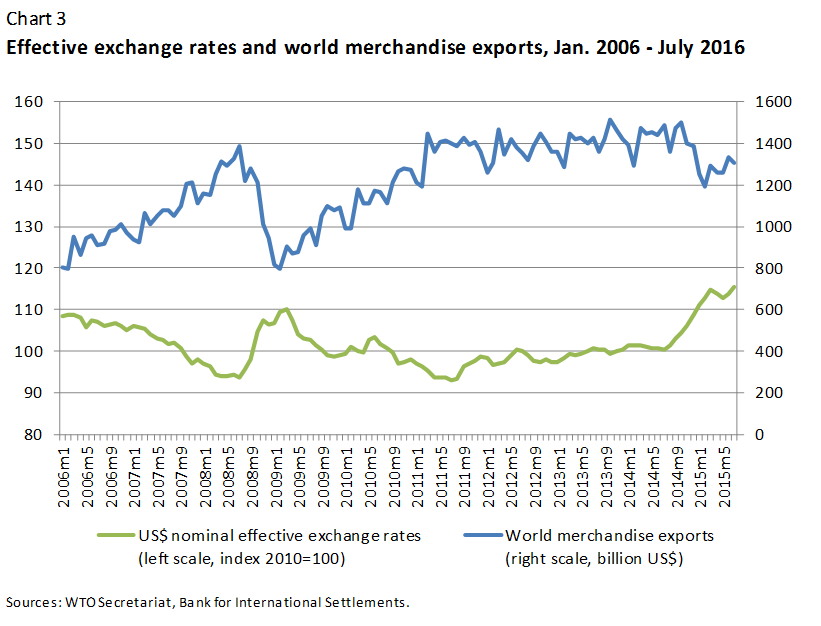

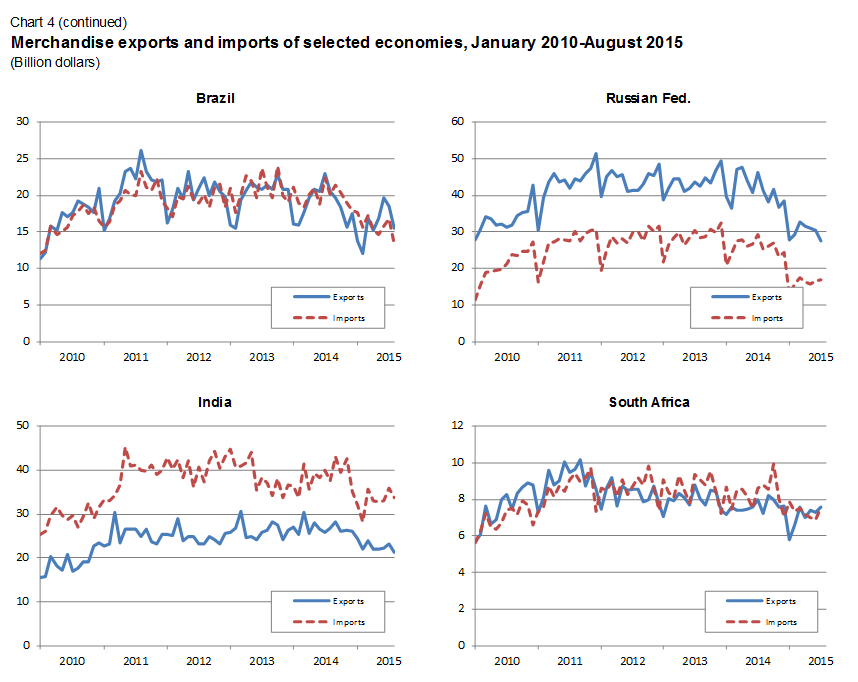

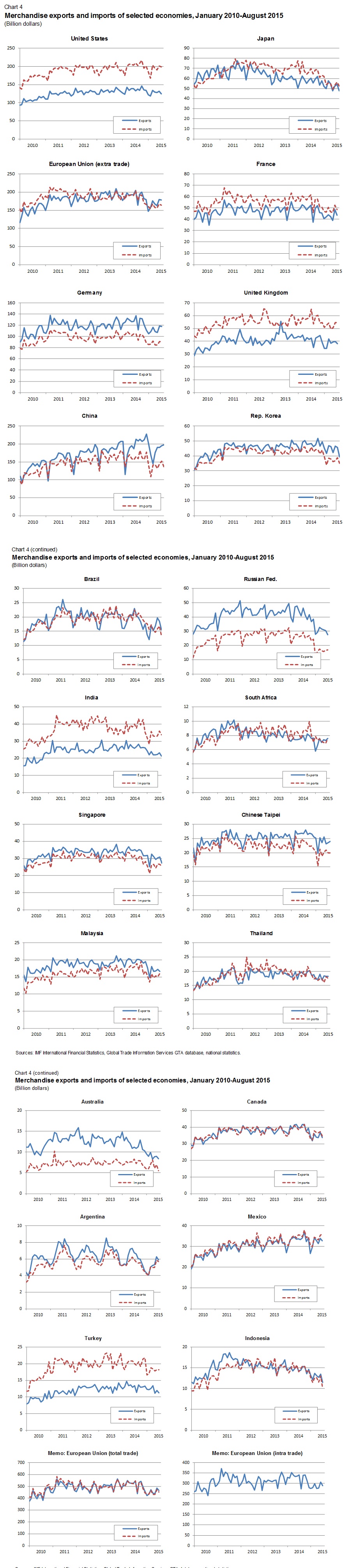

Finally, nominal merchandise trade statistics sometimes provide a better indication of current trade trends than statistics in volume terms since the former are generally timelier. These are illustrated by Charts 3 and 4. However, trade statistics in dollar terms are highly sensitive to fluctuations in prices and exchange rates and should be interpreted with caution.

Trade values in dollar terms have declined in most countries since last year and were down roughly 12% year-on-year in July at the world level. This is partly the result of a strong general appreciation of the US dollar over this period (+15% in nominal effective terms against major currencies according to the Bank for International Settlements). As Chart 3 shows, there is generally an inverse relationship between world trade values in current dollar terms and the value of the US currency. For example, Germany’s exports and imports were both down 14% year on year in dollar terms in July, but they were up 6% in euro terms.

Click here to view Chart 4 in full.

[1] Data are sourced from WTO short-term trade statistics, which can be downloaded here.

Related News

Exchange rates still matter for trade

Exchange rate movements still have sizable effects on exports and imports, according to new research from the International Monetary Fund.

Recent currency movements have been unusually large. The U.S. dollar is up more than 10 percent in real effective terms since mid-2014. The yen is down more than 30 percent since mid-2012 and the euro by more than 10 percent since early 2014. Brazil, China, and India have also seen unusually large changes in their currency values.

Not surprisingly, these movements have kindled a debate on their likely effects on trade. Some predict strong effects on exports and imports, based on conventional economic models. Others argue that the increasing fragmentation of production across different countries – the so-called rise of global value chains – means that exchange rates matter far less than they used to for trade, and may have disconnected altogether.

This is an important debate, says Daniel Leigh, Deputy Division Chief in the Research Department, and lead author of the report. “A disconnect between exchange rates and trade would complicate policymaking. It could weaken a key channel for the transmission of monetary policy, and complicate the reduction of trade imbalances, as in the case of imports exceeding exports, via the adjustment of relative trade prices.”

From exchange rates to trade: lessons from history

Concerns about a disconnect between exchange rates and trade are not new. Back in the 1980s, the U.S. dollar depreciated, and the yen appreciated sharply after the 1985 Plaza Accord, but trade volumes were slow to adjust. Some commentators then suggested a disconnect between exchange rates and trade. But by the early 1990s, U.S. and Japanese trade balances had adjusted, largely in line with the predictions of conventional models.

The question is whether this time is different, or whether the apparent disconnect between exchange rates and trade will once again dissipate.

A new study, for the October 2015 World Economic Outlook, contributes to the debate by taking stock of the relationship between exchange rate movements and exports and imports.

The study examines the experience of both advanced and emerging market and developing economies over the past three decades – a broader sample than is typically examined. It uses both standard trade equations and an analysis of historical cases of large exchange rate movements.

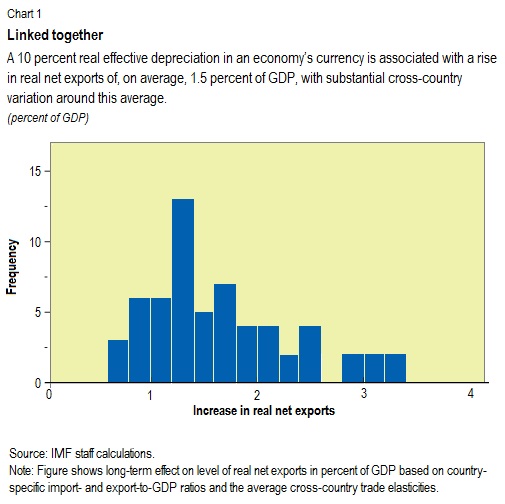

“We find that, on average, a 10 percent real effective exchange rate depreciation comes with a rise in real net exports of 1.5 percent of GDP,” says Leigh, noting that there is substantial variation around this average (Chart 1). “Although it takes some years for the effects to fully materialize, much of the adjustment occurs in the first year,” he says.

Among economies experiencing currency depreciation, the rise in exports tends to be greatest for those with slack in the domestic economy and financial systems operating normally.

Disconnect or stability?

The study also finds little sign of a breakdown in the relationship between exchange rates and exports and imports.

There is some evidence, however, that the rise of global value chains, with different stages of production located across different countries, has weakened the relationship between exchange rates and trade in intermediate products used as inputs into other economies’ exports. This is particularly relevant for economies such as Hungary, Romania, Mexico, and Thailand, which have substantially increased their participation in global value chains.

But this finding needs to be seen in perspective: global-value-chain-related trade has increased only gradually through the decades and appears to have decelerated, and the bulk of global trade still consists of conventional trade.

There is also little sign, at least so far, of a generalized weakening in the relationship between exchange rates and total exports and imports. There is little evidence of disconnect for various country groups, including Asia and Europe, where the process of production fragmentation across countries has been particularly noticeable, as well as for samples of economies used in other recent studies.

Importantly, the rising size of exports and imports in GDP means that even a weaker relation between exchange rates and trade volumes could be consistent with exchange rate mattering more for trade in percent of GDP than before.

A key exception to this pattern of broad stability is Japan, which displays some evidence of disconnect. Export growth has been weaker than expected, despite substantial exchange rate depreciation. However, this weak export growth reflects a number of Japan-specific factors that have partly offset the positive impact of yen depreciation on exports and that do not necessarily apply elsewhere. These include, in particular, the sharp acceleration in production off-shoring since the global financial crisis and the 2011 earthquake, which created uncertainty about energy supply.

Redistributing net exports

These results are important because they mean that recent currency movements are shifting net exports from some economies to others. But this only speaks to the direct effects of exchange rate movements.

Overall changes in exports and imports also reflect shifts in the underlying fundamentals driving exchange rates themselves. These include demand growth at home and in trading partners, and movements in commodity prices.

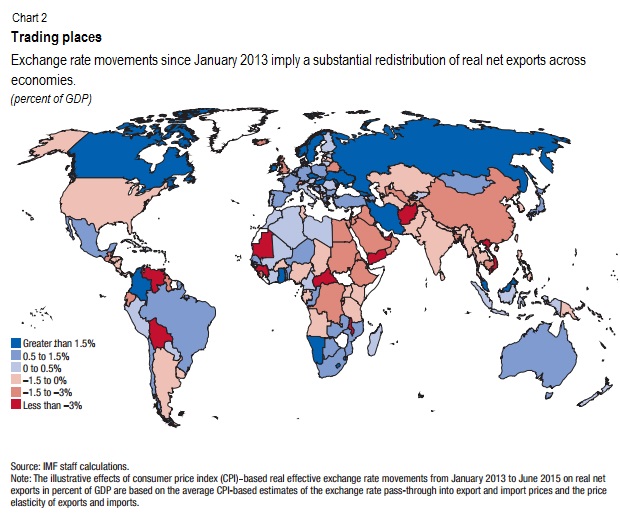

But, in terms of the direct effects, the currency movements since January 2013 point to a shift of real net exports from the United States and economies whose currencies move with the dollar to the euro area, to Japan, and to economies whose currencies move with the euro and the yen (Chart 2).

“For policymakers, a key implication of these results is that exchange rate adjustments can still help to reduce trade imbalances,” says Leigh. Exchange rate changes also continue to have strong effects on export and import prices, with implications for inflation dynamics and the transmission of monetary policy.

In sum, exchange rates still matter!

The authors of this study are Daniel Leigh (team lead), Weicheng Lian, Marcos Poplawski-Ribeiro, and Viktor Tsyrennikov, with support from Olivia Ma, Rachel Szymanski, and Hong Yang.

Related News

Entering uncharted waters: El Niño and the threat to food security

Millions of poor people in Southern Africa, Asia and Central America face hunger and poverty this year and next because of droughts and erratic rains as global temperatures reach new records, and because of the onset of a powerful El Niño – the climate phenomenon that develops in the tropical Pacific and brings extreme weather to several regions of the world.

Despite record global temperatures in 2014, an El Niño did not appear; nevertheless, in an unusual development, the climate in many parts of the world behaved as if one was occurring and growing seasons were seriously disrupted, mainly by drought. Temperatures have continued to soar this year and now an El Niño has indeed developed. It could be the most powerful since 1997-98, 2 which caused climate chaos and humanitarian disasters in many countries. With the boost of El Niño, unprecedentedly high temperatures are likely to continue into 2016.

Already, Ethiopia is facing a major emergency: 4.5 million people are in need of food aid because of successive poor rains this year. Floods, followed by drought, have cut Malawi’s maize production by more than a quarter; between two and three million people may face a food security crisis by February next year, at the peak of the lean season. In Zimbabwe, drought has reduced the maize harvest by 35 percent, and it is estimated that 1.5 million people will need assistance in early 2016. Farmers across the ‘dry corridor’ of Central America have been hit by drought for two years running, with huge harvest losses. Disruption to maize production in both Southern Africa and Central America is driving a surge in the price of maize on local markets, making it increasingly hard for people living in poverty to afford sufficient food.

Over the next few months the El Niño will attain maximum strength. This will coincide with the coming rains in Southern Africa, due from November onwards. Meteorologists predict a high probability of below-average rains again as a result. A second successive poor rainy season across Southern Africa will bring serious food security problems next year. The next rains in northern Ethiopia from March may also be affected.

El Niño has also already reduced the Asian monsoon over India, and is raising the odds of a prolonged drought in East Asia, coinciding with the planting and early development of the main rice crop in Indonesia; if world prices for rice increase there could be knock-on effects on poor urban consumers in import-dependent West African countries. In Papua New Guinea, 1.8 million people have been affected by drought already and El Niño will make this worse.

Yet meteorologists and international agencies such as the World Food Programme have provided ample warning of El Niño; the regions likely to be affected and the potential effects are understood. Agencies such as Oxfam have been monitoring conditions on the ground, helping communities cope with the current food crises and, increasingly, sounding the alarm that more must be done. Disasters are not inevitable at this point. If governments and agencies take immediate action, as some are doing, then major humanitarian emergencies next year can be averted. Prevention is better than cure.

In the immediate future, increasing climatic disruption, driven by rising temperatures, threatens to increase pressures on the humanitarian system at a time when resources and capacity are under enormous strain. Furthermore, scientists are warning that recent events could signify that big changes may be underway in the Earth’s climate system, 4 driven by rising surface temperatures and changes in major atmospheric and oceanic circulation systems such as those which give rise to El Niño.

Warming seas could double the frequency of the most powerful El Niños, and as global warming creates more and more sea-surface temperature ‘hot spots’ in the world’s oceans, and wind systems change as a result, extreme weather and greater climate disruption may be what a ‘normal’ future looks like if greenhouse gas emissions are not urgently and drastically reduced.

The combination of record warmth one year followed by an El Niño the next is unique and the climatic implications are uncertain. If 2016 follows a similar pattern we are entering uncharted waters.

Just one week after leaders adopted an historic new goal of eradicating hunger by 2030, as part of the package of Sustainable Development Goals, this unfolding crisis shows the scale of threat that climate change poses to its realization. For those leaders, the first test of their commitment will be to strike an agreement at the UN climate talks in Paris this December that delivers for the women, men and children on the frontlines of climate change.

Related News

Commodity exporters facing the difficult aftermath of the boom

With a weak outlook for commodity prices, particularly for energy and metals, growth in commodity-exporting emerging and developing economies could slow further over the next few years, says a new study.

The study, published in the forthcoming 2015 World Economic Outlook, suggests that the recent declines in commodity prices could shave off one percentage point annually from the growth rate of commodity exporters over 2015-17 as compared with 2012-14. In exporters of energy commodities, the drag is estimated to be even larger – about 2¼ percentage points on average.

This slowdown is not just a cyclical phenomenon, the study finds. “It has a structural component as well,” says lead author Oya Celasun, Deputy Division Chief in the Research Department. “Investment, and accordingly, potential output, tend to grow more slowly in exporters during commodity price downswings.”

The decline in potential growth exacerbates the post boom slowdown, Celasun says. “This means that policymakers in commodity-exporting countries must go beyond demand-side measures and tackle structural reforms to improve human capital, increase investment and, ultimately, unleash higher productivity growth.”

Upswings and downswings

Commodity prices are unpredictable and can be very volatile. They can remain high or low for prolonged periods, giving the impression that their levels are permanent, only to exhibit very sudden and large changes.

Recent history is no exception. The first decade of the 2000s saw a persistent surge in commodity prices from record lows in the mid-1990s to record highs by 2011. More recently, however, the prices of commodities have fallen again, some in a dramatic fashion, and are expected to remain weak for some time (Chart 1).

Procyclicality, a common concern

In commodity-exporting economies, output growth, and economic developments more broadly, are unavoidably driven by commodity price cycles. To understand the channels better, the study examines data for more than 40 commodity exporters in emerging and developing economies for the last 50 years. It finds that output and, particularly, investment grow faster during commodity price upswings than in subsequent downswings (Chart 2). Much of this cycle reflects a strong investment response in the commodity-producing sector itself, which spills over into supporting industries such as construction, transportation, and logistics.

But it also reflects other mechanisms. In countries that rely heavily on resource revenues, fiscal policy is often procyclical with respect to the terms of trade. Government spending tends to increase when commodity terms of trade are improving, influencing economic activity more broadly. At the same time, governments, firms, and households in commodity-exporting economies all tend to borrow more easily during commodity booms than during downturns, amplifying the economic cycle set in motion by commodity prices.

Cyclical trends versus structural shifts

The appropriate policy responses depend not only on the extent of the growth slowdown but also whether commodity-price-related fluctuations in output are mostly structural or cyclical in nature. That is, policies would have to be designed differently if commodity price changes affect potential output and not just the cyclical fluctuations around it.

The study finds that both cyclical and structural factors tend to be at play during commodity-price driven fluctuations in output growth. On average, about two-thirds of the decline in output growth in commodity exporters during a commodity price downswing is cyclical, and one-third is structural, reflecting lower potential growth. This means that for commodity exporters that have enjoyed a prolonged surge in commodity prices, the recent slowdown also reflects weaker growth potential, as investment growth collapses.

What to expect going forward

What does the behavior of economic activity during past commodity price cycles imply for the current downswing? While the size and duration of the 2000s commodity boom exceeded its historical average, its reversal could lead to a sharper slowdown now. However, a typical commodity exporter is now better equipped to deal with a downswing than in earlier episodes.

Despite the more pronounced commodity price boom, growth rates over the last decade have been in line with earlier boom episodes and inflation rates have remained more subdued. This suggests that macroeconomic policies were more successful in smoothing the impact of the commodity windfall than in the past, as there was less of a growth boost than one would have expected given the size of the increase.

More specifically, fiscal policy has been less pro-cyclical – allowing for greater savings out of resource revenues – exchange rates have been more flexible, and financial depth has increased relative to the earlier episodes. All these factors were associated with smaller drops in output growth during previous downswings.

In addition, commodity exporters are entering the current downswing with stronger external positions, which can also help mitigate the effect of the commodity price downturn on their economies.

What are policymakers to do

The findings of the study imply that the growth slowdown in the immediate aftermath of a commodity price boom most likely represents a return to a more sustainable level of output. At the same time, slowing investment and economic capacity can lead to lower potential output growth.

Policymakers in commodity exporting countries therefore need to be careful not to overestimate the extent of excess capacity in their economies. A significant deceleration in growth rates is unavoidable for many economies.

Looking beyond the current juncture, the findings suggest that more flexible exchange rates and policy frameworks that avoid excessive pro-cyclical fiscal spending can help policymakers smooth the impact of commodity price swings on their economies.

Where growth is disappointing, policy efforts that focus on structural reforms to foster sustained medium-term growth are likely to be very fruitful. The structural reform priorities vary across countries, but removing infrastructure bottlenecks, improving the business climate, and enhancing the quality of education are common goals across many.