Search News Results

DP World launches infrastructure report at Africa Global Business Forum

Infrastructure development to lead foreign investment says DP World Chairman

A five point plan to help tackle Africa’s infrastructure gap is among the findings of a new DP World report to be unveiled at the Africa Global Business Forum this week.

Public private partnerships, domestic bond financing, monitoring the life cycle of infrastructure by maintaining and upgrading existing stock, enhancing trade integration and improved trade facilitation are key point raised in the study “Africa at the Crossroads: Bridging The Infrastructure Gap”, produced in association with the Economist Intelligence Unit.

Over the past decade, investment in African infrastructure has risen sharply and some notable projects have been completed, but despite the impressive flow of projects and policy reforms, the continent’s infrastructure development has failed to keep up with the average annual GDP growth of 5%. The development of “soft” infrastructure, such as the legal and regulatory frameworks that enable physical infrastructure to be built and maintained, has also fallen short of requirements.

The report traces the continent’s strong economic growth in recent years and highlights how infrastructure development has not kept pace, placing an increasing strain on existing infrastructure assets.

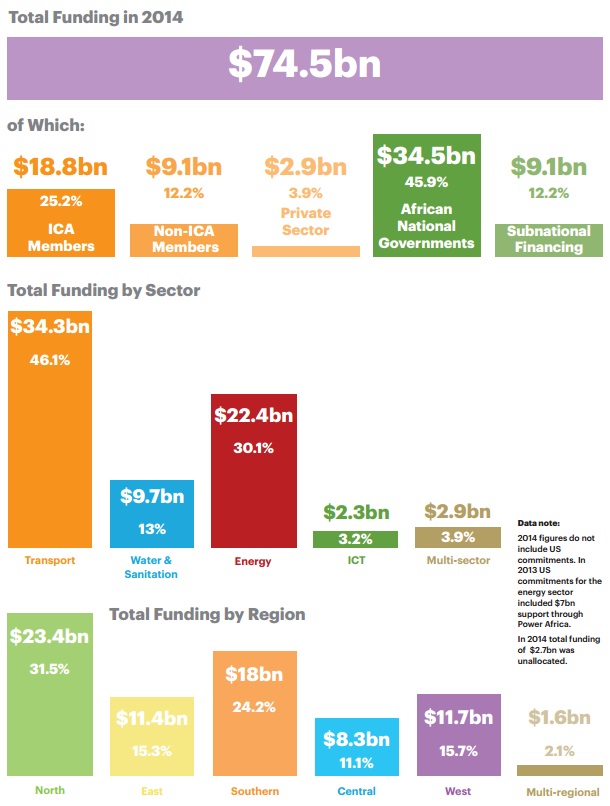

To overcome infrastructure deficits on the continent, as much as $93bn will be required annually (approx 10% of African GDP), with only half of that amount currently available the report explains.

Speaking on behalf of DP World, chairman H.E Sultan Ahmed bin Sulayem said; “African countries need a solid foundation on which to place the building blocks of their economies. Both soft and hard infrastructure is needed, which will determine how quickly physical assets are built and how quickly trade develops.

“Our ports in Africa have shown us how the region has enjoyed strong growth over the last 10 years, leading to rising incomes, falling poverty and a step toward economic diversification. However, all this has also placed an increasing strain on existing inland and marine infrastructure. If Africa’s countries and regions were better connected, market sizes would increase and encourage greater foreign investment.”

Yet while Sub-Saharan Africa currently spends around $6.8bn per year on paving roads, this figure needs to be closer to $10bn.

H.E Bin Sulayem stressed the significance of the Public-Private Partnerships (PPP) model, explaining how several African governments have already started to design policies to accelerate infrastructure projects.

Referring to report findings, he added: “PPP’s are an increasingly popular model to fund projects and the regulatory frameworks supporting them are improving. In addition, resource-rich countries are using their commodities as leverage to obtain infrastructure investment. Today, a growing number of the new natural resource contracts that African governments had out have an ‘infrastructure industrialisation’ component – requiring the company in question to invest in new infrastructure.”

DP World has long advocated the power of partnership, having agreements with governments in all six of its ports in five African countries. Africa is a key market in DP world’s network, where it employs over 5,000 people and has established strong community ties, while creating jobs and opportunities for local businesses.

The report also finds that to address the soft infrastructure gap, better internal trade integration is key. One solution to encourage intra-African trade would be to create a pan-Africa free trade agreement, which has already been proposed.

The paper concludes that growth in Africa brings new challenges and current evidence suggests that the African continent is moving at a rate with which its infrastructure cannot keep up. There are encouraging signs of world-class infrastructure delivery on the continent, like South Africa’s Gautrain rapid rail transit system and Kenya’s new railway connecting Nairobi with Mombasa.

Other high impact projects underway could also be game-changers if they can overcome operational challenges. A notable example is the Inga Dam in the Democratic Republic of Congo.

Meanwhile, a range of policies from regional free trade agreements to improved PPP frameworks across a large number of countries are starting to happen, which suggests that the enabling environments for infrastructure development is improving. If momentum can be maintained and accelerated then it could help the continent overcome its critical deficits and seize the economic transformation that now lies within its grasp.

Related News

Modi resets India’s Africa strategy

Apart from boosting trade and investment ties, the idea is to present a united front at multilateral forums such as WTO

Four changes or incipient trends were noteworthy at the third India-Africa Forum Summit last month. These spell out the contours of the engagement that India will pursue with the African continent, its constituent countries, and regional organisations, as well as the government’s desire for a course correction in the traditional trajectory of the India-Africa relationship.

In the first change, a departure from the approach of previous Indian governments, the October event dispensed with the practice of following the Banjul formula, under which only a few African countries participated in the summit.

This time, the government invited all 54 African countries to New Delhi, and among those who came were 40 heads of state. While the shift in policy could be ascribed to this government’s predilection for spectacular optics, it is also true that the multilateral summit gave India an opportunity to engage with each country.

Prime Minister Narendra Modi and External Affairs Minister Sushma Swaraj held numerous bilateral discussions with individual leaders and representatives.

Multilateral negotiations

This extensive bilateral exercise is tied to a second new policy stance – Modi’s push to forge a united front with African nations for a common, but differentiated, negotiating framework in multilateral institutions. In his inaugural speech at the summit, Modi said: “…our global institutions reflect the circumstances of the century that we left behind, not the one we are in today… That is why India and Africa must speak in one voice for reforms of the United Nations, including its Security Council.”

Beyond this, PM Modi has sought African support on two other critical multilateral fronts – climate change negotiations and trade talks. For the first, Modi wants to create a club: “I also invite you to join an alliance of solar-rich countries that I have proposed to launch in Paris on November 30 at the time of the COP-21 meeting.”

A combined front such as this will be necessary when negotiating with rich countries for resources to shift to clean energy technologies because, “the excess of [a] few cannot become the burden of many.”

Modi also wants to align African countries to India’s concerns with the global trading regime. This becomes important given the forthcoming World Trade Organisation (WTO) ministerial in Nairobi in December, where developing countries are likely to make a last-ditch effort to save the Doha Development Round.

The threat comes from developed nations, specifically the US, which in October has signed the Trans Pacific Partnership with 11 other nations and is lobbying to bury the development round.

Modi said as much in his inaugural speech: “India and Africa seek also a global trading regime that serves our development goals and improves our trade prospects. We must ensure that the Doha Development Agenda of 2001 is not closed without achieving these fundamental objectives. We should also achieve a permanent solution on public stockholding for food security and special safeguard mechanism in agriculture for the developing countries.”

India’s desire to construct a common bargaining platform is probably driven by the embarrassment of July 2014, when it was isolated while blocking the Trade Facilitation Agreement at WTO’s General Council meeting. India’s other attempts to get developing countries on board – to provide Duty Free Tariff Preference (DTFP) to least developed countries on 98 per cent of its tariff lines, including in services – have also produced mixed results, prompting the government to now fast-track the entire scheme.

The third outcome is a public acknowledgement of the partial success in implementing India’s marquee development cooperation programmes – concessional lines of credit (LoCs), grants, and capacity building through the Indian Technical and Economic Cooperation Programme as well as the Pan Africa E-Network – and the need to improve the current processes.

Wider engagement

Modi announced enhanced allocations for the programme – $10 billion under concessional LOCs (double the $5 billion announced at the 2011 summit), $600 million of grants, and 50,000 scholarships in India – but also admitted that, “There are times when we have not done as well as you have wanted us to. There have been occasions when we have not been as attentive as we should be. There are commitments we have not fulfilled as quickly as we should have.”

The problem with LOCs is well documented including a widening gap between sanctions and disbursements. In a pre-summit media briefing in New Delhi on October 17, Secretary (West) in the Ministry of External Affairs, Navtej Singh Sarna, gave an update on LOCs: of the $7.4 billion on offer so far, $6.8 billion has been approved and $3.5 billion disbursed. In effect, disbursals are only 51.47 per cent of sanctions.

Both India and recipient African countries are responsible for the low disbursal rate. In India, a multi-tiered and multi-agency framework for sanctioning and disbursing these loans creates delays. Additionally, a non-transparent process causes distortions.

Exim Bank, which finally disburses the loans, has complained to the Prime Minister’s Office about malpractices. On the African side, capacity gaps in drawing up detailed project reports, essential for the Indian side to conduct a proper appraisal, cause delays.

The India-Africa Framework for Strategic Cooperation has promised to introduce a “regular formal monitoring mechanism” to review implementation of projects.

Addressing gaps

The fourth change was the absence of an announcement of trade targets. This was probably necessitated because India-Africa two-way trade has fallen short of the $90 billion 2015 target. But such ambitious targets tend to overshadow otherwise admirable progress in trade relations. In fact, trade between India and Africa has been remarkable.

According to government data, two-way trade touched $72 billion during 2014-15, which is a vast improvement over the $4.5 billion of 1996-97. But interlocutors still need to address some persistent gaps.

One, there is little data in the public domain about the development and progress of projects, especially those under the LOC umbrella or under other initiatives. For instance, there is no report card on the promise to help build 100 institutions that India made during the second India-Africa Forum Summit in Addis Ababa in 2011.

Two, with similar and competing summits being hosted by China, Japan, Turkey, and the US, India should work on upgrading the status of its India-Africa Summit by including sub-fora on labour representatives, think tanks, civil society, academia, and women’s rights groups, in addition to the existing India-Africa Business Forum.

The writer is a journalist and senior geo-economics fellow with Mumbai-based Gateway House

Related News

UNCTAD briefs UN delegates on Policy Framework and WIR 2015

Mr. James Zhan, Director of UNCTAD’s Investment and Enterprise, and team leader of the World Investment Report, briefed New York delegates about the UNCTAD Investment Policy Framework for Sustainable Development and the Roadmap for the Reform of the International Investment Agreements Regime on 12 November 2015.

Presenting the latest trends in flows and policies, he pointed to the importance of foreign investment in closing the financing gap for achieving the 2030 Agenda for Sustainable Development, estimated by UNCTAD to range from $3.3 trillion to $4.5 trillion per year in developing countries alone. Mobilizing investment and ensuring that it contributes to sustainable development is a priority for all countries.

UNCTAD’s Investment Policy Framework has been developed to assist Member States and the international investment-development community in devising strategies and policies to attract and benefit from investment in sustainable development. The Framework has been updated with Member States and other experts to better align investment to the demands of the Agenda 2030 for Sustainable Development.

As acknowledged in the Addis Ababa Action Agenda, the pursuit of the 2030 Sustainable Development Agenda will also require a reform of the international investment agreements (IIA) regime (which currently consists of over 3,300 treaties). UNCTAD’s 2015 World Investment Report: Reforming International Investment Governance offers a menu of options for the reform of the IIA regime, together with a roadmap to guide policymakers at the national, bilateral, regional and multilateral levels. It also proposes a set of principles and guidelines to ensure coherence between international tax and investment policies.

H.E. Mr. Virachai Plasai, Ambassador and Permanent Representative of Thailand to the United Nations, elaborated on his country’s revision of its investment policy. He emphasized that Thailand has used UNCTAD’s Policy Framework extensively, both in terms of enhancing the sustainable development dimension of the countries' inward and outward flows, and its regime of international investment agreements. He noted that investment is a cross-cutting issue that touches on all of the 2030 Sustainable Development Goals, but that this issue is absent from the General Assembly’s agenda.

Ms. Adriana Vargas Saldarriaga, Director, Foreign Investment, Services and Intellectual Property, in the Colombian Ministry of Commerce, Industry and Tourism, explained the revisions to her country’s investment policies and treaties which were based entirely on UNCTAD’s Policy Framework. Referring to the seminal nature of UNCTAD’s Framework, she elaborated on key treaty aspects that were inspired by the Framework, and the country’s new investment promotion strategy that was based on pursuing the sustainable development dimension of investment in line with UNCTAD’s approach.

Mr. Wamkele Mene, Director, Investment and International Law, in the Department of Trade and Industry of South Africa, elaborated on his country’s new investment policy, which was largely shaped by the Framework. He stressed his country’s role in the development of the UNCTAD’s Framework, which had been launched by H.E. Rob Davies, Minister of Trade and Industry, South Africa. Explaining the background to the new South African approach to IIAs, he reiterated his country’s support for the UNCTAD reform path for IIAs, to provide for a better balance between the rights and obligations of investing companies and to ensure agreements do not run afoul of national laws.

Mr. Joerg Weber, Head of UNCTAD’s Investment Policies Branch, added that foreign investment matters for all of the 2030 Sustainable Development Goals, and that for some countries the contribution of foreign investment is key. He stressed UNCTAD’s role in helping Member States in this regard, pointing to various UNCTAD technical assistance products and programmes. He also noted that the issue of investment has been taken up by all international high-level forums, including the ASEAN Summit, the European Parliament and the G20, but not as of yet by the General Assembly and its Second Committee.

Ms. Chantal Line Carpentier, Chief, UNCTAD New York Office thanked all present and invited them to browse UNCTAD Tool Box that includes all the capacity building tools that UNCTAD offers Member States to assist them in putting in place the policies, regulations, and institutional frameworks and in mobilizing the resources needed to fulfil the ambitions of Agenda 2030 for Sustainable Development.

Related News

Recovery in cross-border mergers and acquisitions

Cross-border merger and acquisition (M&A) activity increased significantly in the first half of 2015, but may be slowing down in the second half of the year, the latest UNCTAD Global Investment Trends Monitor reports.

The UNCTAD Global Investment Trends Monitor analyses the most recent trends in cross-border mergers and acquisitions (M&As) and assesses their prospects for 2015. It covers trends in developed, developing and transition economies.

A lull in South-South mega deals dampens cross-border M&A activity in developing and transition economies

The value of cross-border M&A activity, both in terms of purchases and sales, fell in developing and transition economies in the first half of 2015. Net purchases by MNEs from these economies fell 34%, compared with the same period of the previous year, to US$72 billion. The majority of this decline was due to a sharp reduction in the value of acquisitions in other developing and transition economies.

Developing Asia, which was the world’s largest investing region in 2014, registered the sharpest decline in net purchases in 2015. Nevertheless there was brisk activity by MNEs from a number of countries, including Singapore. Large deals included the purchase by a Singapore-based investor group of IndCor Properties Inc (United States) for $8.1 billion and United Fiber System Ltd’s (Singapore) acquisition of a 67% stake in Golden Energy Mines Tbk PT (Indonesia) for US$2.3 billion.

The value of net M&As carried out by MNEs from Latin America and the Caribbean fell sharply (-90%) in the first half of 2015. Their divestments rose to US$8.3 billion, largely as a result of Oi SA’s (Brazil) sales of its Portuguese assets to Altice SA (Luxembourg) for US$7.2 billion. African MNEs registered a similar decline, but the level of their sales was not sufficient to push them to net divestment. A slowdown in large deals carried out by the region’s MNEs contributed to the decline in net value.

MNEs from transition economies have slowed their purchases in 2015. Net purchases by MNEs from the Russian Federation fell 24% to US$866 million in the first six months of the year. These firms have been impacted by the rapid decline in commodity prices, in particular of crude oil, and reduced access to international financial markets.

Key finding of this issue:

-

Cross-border merger and acquisition (M&A) activity increased significantly in the first half of 2015, but may be slowing down in the second half of the year. The value of cross-border M&A purchases, which is an indicator of outward FDI flows, rose to US$441 billion, a 136% increase over the same period of 2014.

-

Multinational enterprises (MNEs) from developed countries were the principal drivers of the global cross-border M&A trend. European MNEs, after a number of years of high divestment levels, registered a sharp rise in the value of acquisitions in 2015.

-

Cross-border M&As carried out by MNEs from North America continued to grow strongly (up more than 100%). Acquisitions by Canadian MNEs reached their highest half-year level. Tax inversions accounted for half of outbound deals by value from the United States, although they represented a small share (10%) of global cross-border M&A purchases.

-

After emerging as the largest investing region in the world for the first time in 2014, cross-border M&As by firms from developing Asia registered a decline this year (-27%). Activity by MNEs from Latin America and the Caribbean, as well as from Africa also decreased, reflecting the consequences of depreciating domestic currencies and falling commodity prices.

-

The growth of cross-border M&As purchases is projected to slow in the second half of 2015, but the full year value will be well above that of 2014, based on the first ten months of the year. While economic, financial, and structural trends support this forecast, potential downside factors could limit the scale and length of this current wave of cross-border M&As going forward.

Related News

tralac’s Daily News selection: 17 November 2015

The selection: Tuesday, 17 November

Starting today in Dubai: Third Africa Global Business Forum. Twitter updates: @AGBForum

Nigeria’s National Assembly Dialogue on Economy, Security and Development concludes today: access the presentations

The Fourth Congress of African Economists continues: opening speech by Anthony Mothae Maruping

Today: a briefing by SA's trade minister on the Promotion and Protection of Investment Bill

South Africa and US agree on terms for US poultry imports (Reuters)

South Africa has signed an agreement with the United States to resume import of 65,000 tonnes of chicken each year, which had become bogged down over health concerns, the government said on Tuesday. “We are on track to resolving the outstanding issues related to beef and pork. The chicken protocol shows we are moving in the right direction,” South Africa’s Department of Trade and Industry spokesman Sidwell Medupe told Reuters, adding that outstanding issues will be finalised by Dec. 31.

Pakistan to challenge South Africa’s decision in WTO (The News)

According to official announcement made here on Monday, the Ministry of Commerce decided to challenge South African decision to impose preliminary anti-dumping duty (PD) on the import of Pakistani cement in the WTO. During May this year, South Africa imposed various rates of PD on Pakistani cement exports ranging from 15%-68% anti-dumping duty on the import of Pakistani cement. South African government considered that these imports were causing injury to the local cement industry. Pakistan, however considers that these measures by the South African government are inconsistent with several provisions of the various WTO agreement. Pakistan’s Permanent Representative to the WTO Dr. Tauqir Shah has written a letter to his South African counterpart in Geneva for formal consultations. Any dispute at the WTO begins with a request for consultations and the dispute has a minimum of two stages. First is the consultations stage without involvement of WTO secretariat which involves a combination of politico-legal-economic claims. Second is the panel stage, with the involvement of WTO secretariat and is purely based upon legal and economic claims.

South Africa: Citrus industry earns a more favourable EU stance on black spot scare (Business Day)

South Africa, Turkey to boost bilateral trade (Journal of Turkish Weekly)

ECOWAS, IGAD updates:

Stringent border rules impede ECOWAS trade protocols (The Graphic)

Ghana's finance minister, Mr Seth Terkper, has stated that the failure of the Trade Liberalisation Scheme of the Economic Community of West African States to achieve its objectives of economic integration was due to the stringent cross-border barriers of member countries. In his presentation of the 2016 budget statement to Parliament on November 13, the finance minister called for the removal of trade bottlenecks that were impeding the implementation of the ECOWAS trade protocols. “While some progress has been made in reducing tariffs, they have not been fully eliminated. Progress towards removing non-tariff barriers such as seasonal import and export bans has been slower. The failure to implement the instruments on the ECOWAS Trade Liberalisation Scheme is affecting economic growth in the sub-region”, he said. [2016 Budget Statement and Economic Policy of the Government of Ghana]

ECOWAS, Development Partners annual coordinating meeting concludes today

EU urges ECOWAS nations to comply with common tariff (StarAfrica)

ECOWAS electricity regulators, operators meet today in Accra (VibeGhana)

IGAD summit in Juba delayed to next week (Sudan Tribune)

IGAD, UN convene peace and security dialogue

IGAD’s regional assessment and mapping of radicalization and violent extremism

Malabo meeting to scale up regional agricultural trade and value chains (IPPMedia)

According to NEPAD, the topics to be addressed during the conference are: a progress report on regional agricultural trade and the performance of the strategic value chains and the regional regulatory and policy framework - moving towards greater coherence in trade and agricultural policies in Central Africa. Finally, the conference recommendations will have to be incorporated into the framework of the PRIASAN action plan, as will the arrangements for the governance system of the Regional Council for Agriculture, Food and Nutrition in Central Africa (CRAAN).

Kenya’s Daily Nation is posting a series of articles on the coffee sector: Coffee's share of exports falls five-fold over 30 years, How coffee farmers lose millions at the hands of millers, How groups of coffee farmers overcame cartel, The case for a commodities exchange to lock out rogue traders and cartels

COMESA member states study Sudan’s Bt-cotton fields

Twelve officials and seven journalists drawn from Malawi, Egypt, Ethiopia, Kenya, Swaziland, Zambia and Zimbabwe participated in the visit. It covered biotechnology and bio-safety Research Centre, ginneries, seed processing units and several Bt-cotton farms along the Blue Nile River. Sudan is the only state in COMESA to have commercialized the Bt-cotton technology (since 2012) with over 100,000 acres currently under cultivation and 97% of the farmers now growing the variety.

G20 Summit resources: G20 Leaders’ Communiqué, Antalya Action Plan, the 22 Agreed Documents can be accessed from here

WTO, OECD, IMF at G2O: DG Azevêdo urges G20 leaders to strengthen global trading system, G20 leaders endorse OECD measures to crackdown on tax evasion, Lagarde urges full implementation of G20 agenda

PIDA Week calls for scaling-up project preparation to unlock infrastructure financing (AfDB)

Delegates attending the consultative Week for PIDA, taking place at the headquarters of the African Development Bank in Abidjan from November 13-17, heard that the most binding constraint to unlocking infrastructure financing in Africa was lack of properly prepared projects, which in turn is due to lack of adequate capacity to prepare large projects.

Carlos Lopes: 'Tunisia’s economic future is in Africa' (UNECA)

Unfortunately, Tunisia is not particularly well integrated with the rest of the continent. In terms of its share of African exports in relation to GDP, it ranks 29th in the continent. In terms of investment, while it has one of the best regulatory environments in Africa (4th in terms of starting and operating a local business), Tunisia ranks only 28th in terms of attractiveness for foreign investment. Accordingly, when we look at regional value chains, Tunisia ranks 21st in terms of its share of the total exports of intermediate goods within Africa. A study that ECA has just conducted with UNIDO assesses the impact of various strategic trade agreements on exports for Tunisia and North Africa.

Trade in the spotlight at Commonwealth summit (CommSec)

International trade will be one of the prominent issues on the agenda when Commonwealth leaders meet in Malta between 27 and 29 November, as countries seek ways to respond to urgent global challenges. Under the theme ‘The Commonwealth – Adding Global Value’, heads of government will gather at the biennial summit to address international priorities including climate change, migration and violent extremism. The Commonwealth Business Forum, taking place in the run-up to the summit, will serve as a platform for countries to showcase investment opportunities and improve trade. During the Forum, the Commonwealth will launch its new trade report, which provides an in-depth analysis of trade issues relevant to the Commonwealth.

Migration, refugees and internally displaced persons: STC convenes in Addis (AU)

The overall objective of the first session of the STC on Migration, Refugees and Displaced Persons is to consider and adopt its Rules of Procedure, consider and adopt Common African Position on Humanitarian effectiveness to submitted to the World Humanitarian Summit, due to hold in Istanbul, Turkey in May 2016 and the African Humanitarian Policy Framework and the Disaster Management Guidelines.

Migration and the Global Development Agenda (World Bank)

As the first event (9 Dec) after the finalization of the SDGs, this conference will bring together major stakeholders on migration and development to highlight the latest thinking on how to maximize the benefits and minimize the risks associated with migration for host, origin and transit countries as well as for the migrants and their families

Rwanda’s border communities urged to optimise integration benefits (New Times)

Kenya-Egypt trade exchange hit $474m in 2014 - minister (Zawya)

Ethiopia: UN warns of deepening food insecurity (UN News Centre)

El Niño on track to be among worst ever, but world better prepared for fallout – WMO

South-South cooperation on climate change: Beijing conference speech by Ibrahim Thiaw (UNEP)

Africa has the world’s fastest-growing labor force but needs jobs growth to catch up (Quartz)

Should we continue to use the term “developing world”? (World Bank Blogs)

India: October trade data shows frailty of economic recovery, Merchandise exports contract for 11th month

Brazil keen to further strengthen trade ties with India (Economic Times)

USDA secretary to lead trade mission to Africa (Crop Protection News)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome. Richard Humphries (Email: This email address is being protected from spambots. You need JavaScript enabled to view it.; Twitter: @richardhumphri1)

Related News

South Africa and U.S. agree on terms for U.S. poultry imports

Earlier this month the US threatened to suspend trade benefits for South African farm products.

South Africa has signed an agreement with the United States to resume import of 65,000 tonnes of chicken each year, which had become bogged down over health concerns, the government said on Tuesday.

The veterinary trade protocol comes after the U.S. threatened to suspend trade benefits for South African farm products earlier this month, in retaliation against the clamp down on poultry imports.

South Africa has been concerned that an outbreak of avian flu in the United States which killed nearly 50 million birds could pose animal and human health risks to Africa’s most advanced economy.

“We are on track to resolving the outstanding issues related to beef and pork. The chicken protocol shows we are moving in the right direction,” South Africa’s Department of Trade and Industry spokesman Sidwell Medupe told Reuters, adding that outstanding issues will be finalised by Dec. 31.

The pact the two countries signed is part of the African Growth and Opportunity Act (AGOA), a U.S. programme designed to help African exporters.

The agreement would see the United States emerge as one of the top poultry exporters to South Africa.

South Africa imposes “anti-dumping” duties of above 100 percent on certain chicken products, and industry groups said removing those import barriers opened a market which had been closed for the last 15 years.

South Africa-United States sign Poultry Veterinary Trade Protocol

The “Protocol for Poultry Meat and Day-Old Chicks” has been signed by South African and US Veterinarians on Friday, the 13th of November, 2015.

After several months of technical discussions by the South African and US Veterinary experts a Poultry HPAI Trade Protocol has been finalised.

The United States and South African Veterinary authorities have been negotiating a Poultry HPAI Trade Protocol in the event of any new outbreaks of Avian Flu (HPAI) in the United States to secure the continued exports of poultry from those areas in the US that are NOT AFFECTED by Avian Flu. Almost 20 US States experienced outbreaks of Avian Flu this year.

Negotiating an appropriate trade protocol and health certificate that both secures market access for the US and also ensures safety for animal and human health was a challenging task for the Veterinarians from both the United States and South Africa.

This agreement signals another significant milestone in the process of securing AGOA for South African exporters into the US market.

South Africa’s Message on its AGOA eligibility remains:

-

AGOA has contributed significantly towards building a mutually beneficial partnership between the USA and South Africa.

-

South Africa is a vital part of the regional integration and development process underway in Africa and removing South Africa from AGOA would substantially diminish the significance of AGOA for sub-Saharan Africa and the United States.

-

The breakthrough made at the June 6-7th meeting in Paris on the poultry issue and the progress made on the SPS issues related to poultry, beef and pork offer significant opportunities for the US and South Africa to increase their trade in Agriculture.

-

South Africa is a relatively open economy and trade and investment relations between South Africa and the United States have continued to grow and deepen during the period under AGOA

-

Bilateral mechanisms, such as TIFA, have provided an excellent forum for the resolution of trade and investment concerns.

-

South Africa meets all the eligibility criteria to remain a beneficiary of AGOA for the next 10 years.

Background

Since August 2014 South Africa had campaigned successfully for AGOA to be renewed for all sub-Saharan African Countries.

South Africa’s campaign in Washington to also be included in the extended AGOA was successful.

President Obama signed the AGOA Extension & Enhancement Act (AEEA) of 2015 into law on June 29.

However, the US lobbies insisted that some issues of interest to them such as poultry, pork and beef needed to be resolved by South Africa to allow SA to be eligible South Africa remains on track to finalise outstanding issues by 31 December!

While the US out-of-cyle review held on the 7th of August in Washington had raised a number of concerns of US lobby groups, the USTR confirmed the main issues to be resolved in exchange for South Africa’s participation in AGOA were the three “meats”: poultry, beef and pork.

SA’s Veterinary experts have had several bilateral engagements since the Paris 4th and 5th June meeting including in Paris, Baltimore and via Video Conference on the 27th July, 14th of September, 9th of October, 15th of October, and 6th of November, to resolve the technical SPS issues of mutual concern, to facilitate the imports of these three meats from the US to SA.

The 65 000 ton quota will be open by 31st December 2015.

South Africa’s International Trade and Administration Commission has published the Anti-Dumping draft Rebate Regulations on Friday, the 30th of October, 2015 for comment.

The Regulations will be finalized by the end of November by ITAC and the quota for US bone-in-chicken pieces (chicken legs) will be created by SARS before the end of December 2015.

Issued jointly by the dti and Department of Agriculture, Forestry and Fisheries

Related News

Committee on Regional Cooperation and Integration (CRCI): Enhancing Productive Integration for Africa’s Structural Transformation

Regional Cooperation Committee meeting to discuss improvements to Africa’s productive integration and Continental Free Trade Area

Despite growth during the past decade and relatively good performance, African economies lack industrialisation and integration. Academic evidence from the Economic Commission for Africa (ECA), the African Development Bank (AfDB) and the African Union Commission (AUC) shows this recent growth has had no impact on the underlying structural design of these economies and to diversify its economies, the continent must reverse its dependence on merchandise exports dominated by raw and unprocessed commodities.

The ninth session of the Economic Commission for Africa Committee on Regional Cooperation and Integration (CRCI) will therefore convene in Addis Ababa from 7 to 9 December 2015 to discuss means of promoting and accelerating productive integration through trade and market integration; economic diversification; competitiveness; infrastructure; regional and continental value chains development; and the financing and investments needed to meet implement these policies.

Studies, including the recent ECA Economic Report on Africa (ERA), suggest that to improve intra-African trade, the continent must address its overall weak productive capacities and lack of competitiveness and technological sophistication. The studies cite infrastructure as one of the key impediments to productive integration in Africa. An insufficient infrastructure has adverse effects on supply and value chain linkages, not only in the agriculture sector on which the majority of Africans depend, but also in manufacturing and other sectors of the economy. It also affects growth, the creation of jobs and eventual elimination of widespread poverty.

With infrastructure in place, intra-African trade and regional value chains can effectively facilitate Africa’s industrialization and eventual entry into global value chains, the report suggests.

Themed “Enhancing Productive Integration for Africa’s Structural Transformation”, this ninth session of the Committee will meet to review several documents such as the report on Assessing Regional Integration in Africa VII: Innovation, Competitiveness and Regional Integration (ARIA VII) which recommend that Africa implement innovation-friendly policies if it is to achieve sustained economic growth and transformation.

The ARIA VIII and ECA Economic Report on Africa recommend increasing investments in hard infrastructure, financial services, soft infrastructure and a creation of conducive macroeconomic policies and business environment. Investments in transport, energy, and information and communication technology form a strong basis for a viable and an economic oriented regional integration, the reports argue.

While the eighth session of the Committee focused on concrete policy actions and measures required to enhance progress in trade, regional cooperation and integration, this ninth session will address specific policies such as the Action Plan for Boosting Intra-African Trade, and the envisaged establishment of the Continental Free Trade Area (CFTA) which African Union Assembly of Heads of State and Government wish to launch by 2017.

Since the last session’s discussions, important progress has been made with regard to CFTA. The Heads of State of the tripartite countries launched the Tripartite Free Trade Area, comprising 26 member states of the Common Market for Eastern and Southern Africa, the Southern African Development Community and the East African Community during their recent summit in Egypt in June 2015. The African Union Assembly of Heads of State and Government also launched the negotiations for CFTA during their summit in Johannesburg in June 2015, and reaffirmed their earlier decision to have CFTA established by 2017.

For the CFTA to be more meaningful, it is recommended for African states to transform the structure of their economies through accelerated industrial development and by creating supply and value chain linkages across the continent.

Parallel to the CFTA negotiations is the need to accelerate the progress on economic diversification and structural transformation in Africa, in order to reverse the continent’s dependence on merchandise exports dominated by raw and unprocessed commodities. The structural transformation of the African economies, by means of accelerated industrial development and supply and value chain linkages across the continent, therefore remains a key priority action to make CFTA more meaningful. An operational CFTA buttressed by this structural transformation of the African economies would not only greatly boost intra-African trade, but also it would enhance Africa’s marginalized position in the global trading and economic mainstream.

Deficit infrastructure also has an adverse effect on Africa’s potential to unlock its productive integration and regional value chains capacity as a pathway to economic oriented regional integration. Infrastructure development is vital for regional integration as it facilitates and fosters intraregional trade and the development of regional markets, accelerated growth, and ultimately the creation of jobs and the reduction and eventual elimination of widespread poverty. Furthermore, with infrastructure in place, intra-African trade and regional value chains can effectively facilitate Africa’s industrialization and eventual entry into global value chains.

Productive integration would, therefore, form a strong basis for a viable and an economic oriented regional integration. Productive integration and capacity for effective participation in regional and global value chains requires boosting investments in key strategic sectors, such as hard infrastructure (particularly transport, energy, and information and communication technology) and other enablers such as financial services, soft infrastructure and a conducive macroeconomic policy and business environment.

Against this background, the ninth session will take place at a time of renewed commitment and urgency towards accelerating Africa’s structural transformation and the operationalization of CFTA, as embodied in the African Union’s Agenda 2063, the post-2015 development agenda, and other related developmental action plans. The ninth session will provide a platform for member States to deliberate on this topical and important issue, including ways and means of promoting and accelerating productive integration and its ancillary components of trade and market integration, economic diversification, competitiveness, infrastructure, regional and continental value chains development, and the financing and investments needed to meet these strategic objectives.

In the context of the discussions on the theme, the ninth session will also have the opportunity to receive and review brief parliamentary reports and presentations by the Secretariat on developments taking place in the different areas of the ECA Regional Integration and Trade Division’s work. The reports and presentations will cover the following areas:

-

Development and promotion of regional strategic food and agricultural commodities value chains in Africa. The discussions on this will look at a regional value chain model for the development of agribusiness and agro-industries with the potential for increased participation of small holders in the chain at national level first, then through identification of preferential agroecological zones, recommend regional value chain for economies of scale;

-

The status of food security in Africa. Discussions will be held on the update of the status of food and nutrition security in Africa. The root causes of food insecurity and policy recommendations to enhance capacity and engagement at national, subregional and regional levels will be the mainstay of the discussions;

-

Intra-African trade and the Africa Regional Integration Index. An overall picture of intra-African exports and imports between 1995 and 2013 will be presented and discussed. The session will debate on the composition of the intra-African trade that tends to be dominated primary by commodities, reflecting not only low levels of industrialization but also the low level of transformation in the continent. A joint initiative by the African Development Bank, the African Union Commission and ECA in producing the Africa Regional Integration Index will be presented and discussed during the session. The index project covers regional dimensions of tariff liberalization, trade facilitation, free movement of persons and labour markets, financial integration, macroeconomic policy convergence, social and cultural integration (including gender issues), regional economic community institutional capacity, regional value chains, statistical harmonization and regional infrastructure (including communications, transport and energy);

-

Africa’s international trade. Presentations and discussions will focus on the developments in international trade in 2013 and 2014. The African trade performance and recent trends in merchandise and services, the status of negotiations under the Doha Development Agenda and the Economic Partnership Agreements; and the African Growth and Opportunity Act (AGOA), the Aid for Trade initiative and the increasing importance of South-South cooperation with China and other Asian economies – will all be salient areas for discussions and will conclude with policy recommendations;

-

Infrastructure development in Africa. Discussions in the area of infrastructure, paying particular attention to the transport and energy infrastructure, will be held. The main focus will be to show the current status and gaps of the transport and energy infrastructures, the key priority areas to be discussed, and finally, the current state of play and progress in bridging the requisite infrastructure finance gap;

-

Review of industrial policies and strategies in Africa. The session will discuss the relevant information on the development of industrial capacities to fill observed gaps in the sector; and

-

Review of investment policies and bilateral investment treaties landscape in Africa. Implications for Regional Integration. There will be a dialogue on bilateral investment agreements and how they can help advance Africa’s economic and social transformation.

Participants for this Committee are expected to comprise of senior officials and experts drawn from African ministries in charge of regional integration, trade and industry, infrastructure, agriculture and land policy; Addis Ababa based African Ambassadors and Plenipotentiaries based in Addis Ababa; representatives from the African Union Commission, the regional economic communities, the African Development Bank, and the NEPAD Planning and Coordinating Agency; representatives from the organisations of the United Nations system, the World Bank, and the African Economic Research Consortium (AERC); and development partners as observers.

Established by the ECA Conference of Ministers, the Committee on Regional Cooperation and Integration (CRCI) meets on a biannual basis to review the work undertaken on regional integration and trade such as food security, agriculture, industrialisation, infrastructure and investment in Africa.

Related News

G20 leaders endorse OECD measures to crackdown on tax evasion, reaffirm its role in ensuring strong, sustainable and inclusive growth

The leaders of the world’s 20 largest economies on 16 November 2015 endorsed overhauled global standards to crackdown on tax evasion and recognised the important contribution made by the OECD to help the Turkish presidency in achieving the goal of more inclusive growth.

At their Summit in Antalya, Turkey, the G20 leaders committed to the implementation of the Base Erosion and Profit Shifting project (BEPS) which closes gaps that allow corporate profits to “disappear” or to be artificially shifted to low or no tax environments. They called on the OECD to monitor progress and to develop, by early next year, an inclusive framework including the participation of developing economies on equal footing.

The leaders welcomed progress being made to boost transparency and fairness in the global tax system, reaffirming their commitments to implement automatic exchange of information as early as 2017 and by 2018 at the latest.

The G20 called on the OECD, IMF and World Bank to continue to monitor their commitment to boost growth, create jobs and tackle inequality through the National Growth Strategies established at last year’s Brisbane Summit.

The OECD and the ILO have been tasked with assisting countries in monitoring implementation of a new G20 pledge to reduce the share of young people who are most at risk of being permanently excluded from the labour market and from education by 15% by 2025.

Speaking from Antalya, OECD Secretary-General Angel Gurría said: “The comprehensive policy package which has been promoted by Turkey as President of the G20 – including skills, youth employment, job quality and tackling inequalities – represents real progress. The OECD will continue to play its part in helping to build a fairer and more inclusive global economy. ”

In presenting to the Summit their joint assessment of progress made so far in the Growth Strategies, the organisations said action by governments needs to be accelerated. The OECD has also helped develop the G20 Skills Strategy to tackle inequality as well as low productivity. A job quality framework has been produced to promote decent working conditions throughout G20 countries. The two organisations will also continue to monitor progress towards the G20 goal to increase women’s participation in the labour force.

In addition, the OECD is providing the G20 with analysis and policy recommendations to boost investment and stimulate business dynamism, particularly among small and medium-sized enterprises (SMEs).

With weak growth and a slowdown in emerging markets, spurring investment, particularly through private sector involvement, will be crucial. The leaders finalised the country-specific Investment Strategies developed with the OECD. Its analysis indicates that the strategies would contribute to lifting the aggregate investment to GDP ratio by an estimated 1 percentage point by 2018.

The OECD supported the G20’s Turkish presidency’s emphasis on SME development and the participation of poor developing countries in the global economy. It has provided analysis on improving the integration of both small businesses and poor countries into global value chains, drawing up G20/OECD principles on SME financing and G20/OECD Principles of Corporate Governance. Both sets of principles were endorsed by the leaders.

OECD work on migration and climate change informed the debates at the Antalya summit. In order to support green finance and the fight against climate change, the OECD has delivered work on tracking climate finance as well as toolkits for channelling green investment.

Building on its experience analysing migration, the OECD is assessing the economic impact of the recent surge of refugees in Europe.

The Summit, overshadowed by the tragic attacks in Paris, two days before, devoted a special session and issued a separate statement on increasing international cooperation in countering terrorism.

As the Secretary-General of the Paris based Organisation, Mr Gurría said: “The impact of these atrocities is all the more poignant as Paris is literally our home, where we have our headquarters and where I along with the majority of over 2500 OECD staff and representatives of our 34 Member countries and their families live.”

“Our condolences, thoughts and prayers are most particularly with the families of the victims. This is a moment when we will all stand more united than ever in defence of the freedoms our democracies hold dear.”

» G20 Leaders’ Communiqué: Antalya Summit, 15-16 November 2015

Related News

DG Azevêdo urges G20 leaders to strengthen global trading system

Director-General Roberto Azevêdo briefed G20 leaders at their meeting in Antalya, Turkey, on 16 November on preparations for the WTO’s 10th Ministerial Conference in Nairobi next month.

In their communiqué, the leaders gave a strong call for the WTO to deliver in Nairobi and to implement all the elements of the Bali Package, including those on agriculture, development, public stockholding as well as the prompt ratification and implementation of the Trade Facilitation Agreement. However, in the meeting much of the discussion focused on regional and bilateral trade initiatives due, in part, to slow progress in the Doha Round negotiations.

The Director-General said:

“Our analysis of regional trade agreements shows no obvious conflicts with WTO rules – they all have WTO DNA. But a bigger consideration is where regional agreements cover areas that are not currently covered by the WTO. No one would suggest that regional agreements should not venture into these areas, but conversations in the WTO would definitely be more inclusive, coherent and balanced.

“Progress in Nairobi on a number of fronts – including on issues under the Doha Round – would help to strengthen trade at the global level. We are working towards agreement on issues including agricultural export subsidies and similar measures, and a package for the least-developed countries. This would be significant. We have been trying to do away with export subsidies for decades. We also need to support ratification of the Trade Facilitation Agreement and continue to implement all other elements of the Bali Package.

“But what we decide to do after Nairobi is also crucial. We have to find ways of moving the Doha issues forward and keeping the organization operational and responsive to challenges currently faced by members.

“This is particularly important against the backdrop of a persistent slowdown in trade growth, continuing protectionism and unprecedented activity at the regional and bilateral level. We must ensure that the global trading system is as strong as possible in order to boost growth, jobs and development. But for this to happen, the G20 leaders need to work collectively – they must work to find and explore synergies on a range of trade-related issues. We are not doing that now.”

The key section of the official G-20 communiqué reads as follows:

“The WTO is the backbone of the multilateral trading system and should continue to play a central role in promoting economic growth and development. We remain committed to a strong and efficient multilateral trading system and we reiterate our determination to work together to improve its functioning. We are committed to working together for a successful Nairobi Ministerial Meeting that has a balanced set of outcomes, including on the Doha Development Agenda, and provides clear guidance to post-Nairobi work. We will also need to increase our efforts to implement all the elements of the Bali Package, including those on agriculture, development, public stock holding as well as the prompt ratification and implementation of the Trade Facilitation Agreement. We will continue our efforts to ensure that our bilateral, regional and plurilateral trade agreements complement one another, are transparent and inclusive, are consistent with and contribute to a stronger multilateral trade system under WTO rules. We emphasize the important role of trade in global development efforts and will continue to support mechanisms such as aid for trade in developing countries in need of capacity building assistance.”

Related News

Fourth Congress of African Economists: Opening Speech by Anthony Mothae Maruping

Opening Speech by Anthony Mothae Maruping, Commissioner for Economic Affairs, AUC, at the Fourth Congress of African Economists being held from 16-18 November 2015 in Accra, Ghana, under the theme “Industrial Policy and Economic performance”

“Optimal industrial policy for Africa’s transformation”

It is my distinct honour and special privilege to convey warm greetings of Her Excellency the Chairperson of the African Union Commission, Dr. Nkosazana Dlamini Zuma, and on her behalf, may I warmly welcome you, one and all, to the 2015 Edition of the Congress of African Economists under the theme: Industrial Policy and Economic Performance in Africa.

Allow me to express my profound gratitude and appreciation to the Government and people of Ghana for their usual warm welcome and hospitality and for graciously agreeing to host this 2015 Congress of African Economists in this pioneering country. Ghana is the cradle of Pan-Africanism and therefore a suitable location for this Congress.

I first came to Ghana in 1984 to attend the meeting of the Executive Board of the Association of the African Universities (AAU) which has its headquarters here. Those were in the days of Prof Sawyer (then Vice Chancellor) and Prof Benneh (then Pro-Vice Chancellor). Since then I have had the privilege of coming innumerable times. More vividly I remember negotiations on the predecessor to the Busan Commitments regarding Global Partnership for Effective Development Co-operation and later negotiations that resulted with UNCTAD XII in 2008. Not long ago there was a conference addressing inequalities. Only last week, November 10-11, 2015, there was a regional stakeholders workshop seeking to identify effective ways of combating Illicit Financial Flows from Africa, under the baton of H E Former President Thabo Mbeki. Ghana ought to be commended for taking the lead in addressing inequalities and in curbing illicit financial flows and also for being exemplary in good governance and deepening of democracy, among many other contributions.

At this point let me also like to express gratitude to colleagues and development partners from the international community, and especially the African Capacity Building Foundation (ACBF), for sharing with AUC valuable time and ideas and resources. The Congress of African Economists is an important platform for collaboration and for advancing solutions to the key economic challenges facing the African continent.

Gratitude should be expressed to the economists who have graciously honoured AUC invitation to come and actively participate in this congress.

At this juncture allow me to attempt to give context to the pivotal role of industrialization in the quest for transformative growth. Not so long ago almost every speaker on African economies, with the exception of the few, jumped on to a “bandwagon” chanting: the refrain “six out of ten fastest growing economies globally are in Africa” Analysts put average growth rates at 4%+ seen as rising towards 5%+. The few that did not jump onto this bandwagon were viewed as pariah. Yet Africa has fifty four economies making six only eleven per cent. In addition, given that Africa is still home for over 30 least developed countries and several low middle income countries, all accompanied by rapidly growing populations, growth rates of between 4 and 5 per cent fell short of what would be required to achieve economic transformation sought. Sustained growth rate of at least 7 per cent in real terms remains what is required to achieve sufficiently rapid socio-economic development. Coupled with diversification and inclusivity and equitable distribution of income and wealth, some resilience to external shocks would be attained and Africa would be set on the road towards poverty eradication. That 4-5 per cent growth rate that Africa was supposed to celebrate depended largely on commodities price boom. Many African economies remain commodities based. They thrive during commodities price boom with multinationals engaged in extractive industry repatriating profits. GDP figures then look impressive but very little remains to permeate into the domestic economy. Such economies experience setbacks when commodities prices fall. Hence the need to transform African economies ensuring diversification and value addition. African economies are currently going through a rough patch. Demand for raw materials exports has sharply declined, commodities prices have dropped drastically, drought is adversely affecting agricultural production and hydro-electric power generation, thus exacerbating energy deficit. Unemployment rate is rising and incomes are declining. Poverty is rapidly rising. Tax bases are shrinking. Fiscal deficits are widening. Foreign exchange reserves are dwindling. Domestic borrowing has soared. External borrowing has been complicated by credit rating downgrades. Authorities in most cases are resorting to deep expenditure cuts affecting supply of necessities. There is definitely a dire need for a new strategy for African economies. Business as usual is not an option. Agenda 2063 is that strategic framework.

On September 25th, 2015, the General Assembly (GA) adopted by acclamation Transforming Our World: The 2030 Agenda for Sustainable Development together with its 17 Sustainable Development Goals (SDGs) and 169 targets. Statisticians are busy working on methodologies for quantifying attendant indicators. Africa had contributed substantially to this outcome through her Common African Position on Post 2015 Development Agenda (CAP on P2015 DA). CAP influenced the work of the Open Working Group and subsequent inter-governmental negotiations. Africa also had the fortune of holding the Presidency of GA and of G77 + China. In addition one of the facilitators was African and UN SG Advisor on P2015 DA was African as well. Omens were good for Africa. Industrialisation featured prominently as an essential part of transformative growth in CAP (paragraph 23) and in SDGs as Goal 9.

In 2013 the African Union (AU) decided to activate her new mandate, from that of OAU of pre-occupation with decolonization, to that of AU of economic, social and political development. Work on African Agenda 2063 was commenced. Consultations with a wide array of stakeholders were held. Interactive website was opened. Written inputs from member states were submitted. Regional Economic Communities and 35 member states strategic frameworks studied and factored in. Mega trends were analysed. Contents of the AU Constitutive Act, existing continental frameworks, programmes and resolutions were captured. All the foregoing were compiled, analysed and synthesized to formulate African Agenda 2063, both the conceptual part (Strategic Framework) and the First Ten Year Implementation Plan. Conceptual Framework was adopted by AU Summit in January 2015 while the 1st Ten Year Implementation Plan was adopted in June 2015. Essentially Agenda 2063 calls for transformative economic growth in Africa. It proposes a move away from narrow base commodities based economies to diversified economies with high value addition. As a means to this end Agenda 2063 proposes:

-

Development of infrastructure, hard and soft, and its broad context, as well as energy generation;

-

Boosting quantity and quality of production in the agricultural sector;

-

Investing much more in science, technology and innovation for development (technology development, transfer and diffusion);

-

Increasing investment in human capital with emphasis on health, education and training with special emphasis on technical skills;

-

Accelerated industrialization (which is still considered a leading job creator);

-

Improvement of the services sector in quantity and quality;

-

Expediting integration which creates economies of scale opportunities and facilitate efficient allocation of factors of production);

-

Nurturing African private sector development (considering that it is largely the private sector that engages in extraction, diversification, value addition and distribution and thus create jobs and contributes to tax bases);

-

Raising competitiveness to enable Africa joining sub-regional, regional and international supply chains trough trade;

Agenda 2063 also has twelve fast track programmes and projects. These are:

-

Realizing integrated high speed train network;

-

Developing e-network on the continent;

-

Speeding up implementation of open skies decision of 2002;

-

Hastening the pace in implementing the Grand Inga Dam hydro power project;

-

Silencing the guns by 2020;

-

Devising and applying commodities strategy (this in essence is industrialization as it involves value addition and diversification);

-

Convening periodic high level African stakeholders forum;

-

Accelerating establishment of continental financial institutions;

-

Reaching Continental Free Trade Area (CFTA) by 2017;

-

Devising Africa outer space strategy;

-

Giving impetus to the growth of African Virtual E – University.

Enablers, such as good governance in its broad context, and others have been given due attention as well. Similarly cross-cutting considerations such as gender parity and women empowerment, engagement of youth in economic activity and inclusion of people with disabilities in the work place, have all been duly factored in.

Clearly industrialization that Africa seeks cannot thrive in isolation. There is a definite symbiotic relationship among various development facets. They feed one another. They depend upon one another. A comprehensive approach is, therefore, more likely to succeed.

A tally of the 20 goals of Agenda 2063 and 17 SDGs show clearly that the latter are embedded in the former. Agenda 2063 encapsulates the 17 SDGs. Africa, therefore, by pursuing Agenda 2063 will ipso facto be meeting her global obligations on SDGs.

Ambitious as it may seem Agenda 2063 is doable. Due attention was paid to ensure avoiding pitfalls of the past that led to delays in the implementation of the previous frameworks. What gives greater hope of achieving the goals of Agenda 2063 are the fact that:

-

Bottom up approach has ensured inclusion, participation, ownership and commitment by the public, private and civil society sectors;

-

Basing the framework on firm foundations and commitments including constitutive act, existing continental, regional and national frameworks, initiatives and programmes, resolutions and action plans has ensured coherence, alignment and harmony;

-

Implementation involves public, private and civil society sectors;

-

Implementation is at national, regional and continental levels;

-

20 goals and 41 priorities of the First Ten Year Implementation Plan are clear, enabling results based management and mounting of a credible accountability framework;

-

Risk analysis has been conducted and risk management strategy developed;

-

Requisite implementation capacity has been assessed and strategy for closing the gaps devised;

-

Effective communications strategy has been developed;

-

Domestication process at national and regional levels is ongoing;

-

Means of implementation have been, and is being, given full attention;

Africa hosted the 3rd International Conference on Financing for Development (FfD3). Watered down version titled Addis Ababa Action Agenda (AAAA) was the outcome document adopted. Developing countries would have preferred a more committal Addis Ababa Accord (AAA). In paragraphs 23, 24, and 25, illicit financial flows (IFF) is referred to. The leadership of Africa on this matter is recognized. Africa commenced in 2011 to address this issue through the African Union’s High Level Panel led by H. E. former President Thabo Mbeki. HLP report, based on consultations with a broad spectrum of relevant stakeholders, is comprehensive, meticulous, incisive and courageous. The facts it unearthed, observations it made, analysis conducted, interpretations of results given, synthesis unfolded and conclusions arrived at and recommendations derived, are all profound. It is a credible report. At the instruction of the AU Summit consultations with African stakeholders have already been held to identify modalities of implementing recommendations of the HLP report on combating IFF from Africa. The last was right here in Accra, November 10-11, 2015.

On Friday October 23rd, AUC, UNCTAD and UNECA and others persuaded the joint meeting of ECOSOC and 2nd Committee of GA to put IFF issue on the global platform in keeping with paragraphs 23-25 of AAAA, with the view to developing a global framework or at least a roadmap on curbing IFF globally. Africa can do her part but for effectiveness it requires others to play their part as well considering that IFF is a global challenge.

In order to raise required funding for Agenda 2063 and SDGs IFF from Africa must be combatted resolutely and effectively, among many other measures and other sources. Heavy reliance for financing Agenda 2063 will be on Domestic Resource Mobilisation (DRM). Hence the imperative of stopping loss of potential domestic revenues through IFF. Still selective, conditionality laden ODA characterized by often unmet commitments, and the elusive FDI, are expected to be only supplementary.

It is clear from all the foregoing that industrialization is of great importance in order for Africa to achieve her sought after economic and social transformation, especially with regards to the realization of Agenda 2063 in the longer term and the Sustainable Development Goals in the comparatively shorter term. Allow me to elaborate on industrialization.

A year ago, the Conference of Ministers of Economy, Finance, Economic Planning and Development resolved that the need for industrialization is obvious and that Africa must “design a comprehensive industrial development framework that is inclusive and transformative to speed up and deepen value addition of local production, linkages between commodity sector and other sectors”.

Therefore, this Fourth Edition of the Congress of African Economists offers a unique opportunity to develop and discuss issues of critical relevance for designing and implementing optimal policies for inclusive and sustainable industrialization in Africa.

While the Third Congress took a comprehensive approach to industrialization as a catalyst of economic emergence, this year we the agenda has been streamlined to cover specific topics to permit us to delve into greater details of the issues that have the biggest impact on growth and economic performance, and reach where impediments may be inhibiting growth in the region. In order to help deepen the understanding of these complex issues, a broad range of African Economists from the continent and its Diaspora have been invited to share their insights and expertise. The Commission will be in “listening mode”. The hope being to learn from participants about best approaches to tackling these challenges effectively, and about how the Commission can be of assistance towards fostering industrialization and achieving Agenda 2063 goals and priorities.

Industrialization is key for Africa to foster structural transformation and improve standards of living.

Yet, industrialization has remained elusive, with an embryonic manufacturing sector, low productivity and marginal participation in domestic and international markets. In fact industrialization is seen as receding by some analysts. While services have surpassed agriculture and industry as the leading income-generating sectors across Africa, this has not created the quantity and quality of jobs that are sought after which should emerge from manufacturing and labour-intensive production.

This Fourth Edition of the Congress of African Economists, therefore, calls on the continent to refocus its economic development strategies on industrialization, particularly on the means of formulating and implementing effective industrial policies.

In the past, most African countries pursued industrial policy with mixed results. It is now time to acknowledge that appropriate developmental state support is vital to address market failure and spur industrialization and to institutionalize industrial policy in national and regional development strategies at the highest levels of government.

Allow me to share with you four reasons that are viewed as making industrialization central for Africa’s transformation.

First, industrialization is essential to sustain the current Africa’s quest for growth leading towards structural transformation.

As African countries require high and sustained economic growth to make significant progress in reducing poverty, generating employment opportunities for young people and engendering development, industrialization appears to be one of the most important routes for structural transformation.

In that perspective, it should be stressed that no country in the world has achieved rapid and sustained economic growth without structural transformation, generally characterized by the shift of production and labour from lower to higher value and productivity activities and sectors.

A robust and expanding industrial sector, including more manufacturing and resource processing and value addition is crucial for the structural transformation of African economies. In spite of the continent’s huge untapped human resources and natural endowments and more than a decade of growth turnaround, the lack of industrialization has limited Africa’s long-term growth prospects as well as the success of growth on social development. Industrialization would also render African economies more resilient to external shocks.

Second, industrialization must take advantage of best practices and strategic engagement with the private sector.

Our assessment must also check the best practices in terms of industrial and trade policy instruments- such as local content requirements, appropriate monetary policy required for industrialization, the impact of trade partnerships on industrialization and intra-Africa trade.

Building on past achievements and lessons, and taking account of feedback received from consultations with stakeholders during the drafting of Agenda 2063, the AUC proposes a strategic framework for strengthening the role of the private sector in achieving inclusive and sustainable growth. This framework consists of three levels at which the Commission believes it can add value and effectively complement actions by its Member States, RECs and private sector organizations to foster the role of the private sector in inclusive and sustainable industrialization and growth. These three levels are: (i) fostering a business environment conducive to private sector initiatives; (ii) developing productive capacities of the private sector, and; (iii) strengthening private sector engagement for development in Africa.

Industrial policy is unlikely to succeed without conscious efforts to build champions, and without dynamic dialogue and interactions between the government and the private sector at sectoral, country, regional and continental levels.

Third, sustainable and inclusive industrialization must be built on regional integration and efficient economic and social infrastructures.

Sustainable and inclusive industrial development must be accompanied by our integration efforts towards the Continental Free Trade Area (CFTA). In doing so, developing effective regional policies will support industrialization, achieve more equitable growth and reduce the current trends of regional disparities within the continent. AU is taking practical measures to deepen integration, enhance free movements of people, goods and services and removing tariff and non-tariff barriers, as well as harmonizing regulations and policies so as to boost intra-African trade during the next decades. These are articulated in the fast track programmes/projects of the 1st Ten Year Implementation Plan of Agenda 2063.

To achieve Africa’s regional integration agenda and prosperity, infrastructure has been recognized as a fundamental factor. We know that the infrastructure bottlenecks on our continent (especially transport, ports and harbors, energy, irrigation and ICT) are a major challenge to industrialization and intra-Africa trade. At regional level, AU is seeking to address this challenge through PIDA and other infrastructure projects that are critical for industrialization.

At a continental level, discussions have started on developing the High-Speed Train Network Project that will link capitals and major commercial centers. This project will accelerate integration process and intra-African trade and more critically, boost industrialization.

But for the High-Speed Train to facilitate inclusive and sustainable industrialization, energy efficiency to improve economic competitiveness in an environmentally sustainable way is imperative. To avoid vulnerabilities due to energy shortage, countries should adopt efficient technologies associated with higher productivity and reduce negative externalities. Support for the development of the Grand Inga Dam Project and other energy generation projects will contribute to addressing the energy needs of the continent.

Fourth, inclusive and sustainable industrialization must ensure equal opportunities for all the segments of African society.

As the world leaders recently adopted the Post-2015 Development Agenda and SDGs, building inclusive and sustainable industrialization will be of critical importance to addressing the challenges of inclusivity and sustainability of Africa’s growth towards a stable, prosperous and integrated continent as foreseen in Agenda 2063. For the African Union Commission, the moderate progress recorded toward achieving the MDGs underlines the need to give priority to inclusive and sustainable industrialization.

As part of its support to women entrepreneurship and employment through “2015 Year of Women Empowerment and Development Towards Agenda 2063”, the Commission gives particular attention to micro, small and medium-sized industrial enterprises and to creating an enabling environment for women entrepreneurship. Women are under-represented in business communities in Africa. The Commission pushes for gender-sensitive business regulations, and works tirelessly towards addressing the specific training and support needs of women as entrepreneurs and workers to ensure that recent improvements in girls’ education are translated into real economic opportunities for women.