Search News Results

“UNDP deeply involved in visionary agenda for sustainable development” – UN Development Chief

The new Sustainable Development Goals (SDGs) will guide global development for a generation after they are formally adopted by Heads of States and Governments at the end of this month, the UN Development Programme’s (UNDP) Administrator Helen Clark told the Organization’s governing body on 1 September at UN Headquarters.

The SDGs are “a strong, ambitious, and visionary set of commitments, with poverty eradication identified as the most urgent task within the broader agenda for sustainable development,” Helen Clark said, addressing the UNDP Executive Board, which is holding its current session from 30 August - 4 September.

“UNDP is deeply involved in all processes around the SDG roll out,” she added, and “we are bringing our extensive programming experience to bear in supporting countries to develop their national SDG efforts.”

All 193 UN Member States are expected to adopt the SDGs here at the Sustainable Development Summit being held 25-27 September. The SDGs are a global call to action to end poverty, protect the planet and ensure that all human beings enjoy peace and prosperity, leaving no one behind. In addition, an agreement on climate change is expected at the Paris Climate Change Conference, or COP21, this December.

Helen Clark illustrated the urgency of this ambitious vision by pointing to several ongoing crises around the world. Whether it be the response after the earthquake in Nepal, the ongoing conflict in Syria, the flooding in Myanmar, the critical electoral process underway in Haiti, or the Ebola outbreak in West Africa, the need for development to be resilience-based and sustainable is constant and paramount. To fill this need, UNDP focuses on building a knowledge-driven, innovative and open institution that supports developing countries with high quality policy advice, and effective and efficient operations.

“We look forward to the Board’s ongoing support at this time of many crises requiring our response, and of new global agendas requiring our support for implementation,” Helen Clark concluded.

The UNDP Executive Board is made up of representatives from 36 countries around the world, serving on a rotating basis. Through its Bureau, consisting of representatives from five regional groups, the Board oversees and supports the activities of UNDP, the UN Office for Project Services (UNOPS) and the UN Population Fund (UNFPA), ensuring that these organizations remain responsive to the evolving needs of programme countries.

Helen Clark: Statement to the Second Regular Session of the UNDP Executive Board*

I am delighted to welcome you to the Second Regular Session of the United Nations Development Programme (UNDP) Executive Board. Since we met in June at the Annual Session of the Executive Board:

-

the final “Millennium Development Goals (MDG) report”, issued by the United Nations Secretary-General, has been released. This is an important milestone as we near the end of the MDG era;

-

the Third International Conference on Financing for Development in Addis Ababa reached consensus on a new framework for development financing; and

-

here in New York, negotiations on the post-2015 sustainable development agenda concluded successfully. We very much look forward to leaders from around the world gathering here later this month to adopt the new global agenda for sustainable development.

In my statement today, I will comment further on these developments and on:

-

the support UNDP will give to implementation of the new global agreements negotiated this year;

-

the UN development system reform agenda; and

-

our ongoing work on transparency and accountability.

The Executive Board’s agenda this week has a dedicated session on funding – including an important dialogue on how UNDP is adapting to the new development finance landscape, and the importance of predictable, flexible, and quality funding. I will also comment briefly on these issues.

The global agendas being determined this year

On 2 August, UN Member States concluded their negotiations on the post-2015 agenda for sustainable development – “Transforming our World: the 2030 Agenda for Sustainable Development”. The agreed text is a strong, ambitious, and visionary set of commitments, with poverty eradication identified as the most urgent task within the broader agenda for sustainable development. After the new agenda is formally adopted by Heads of States and Government at the end of this month, it will guide global development for a generation.

UNDP can support, and is already supporting, countries in three different ways, through the MAPS approach:

-

Mainstreaming

-

Acceleration

-

Policy Support

This sees us:

-

providing support to governments to reflect the new global agenda in national development plans and policies. This work is already underway in many countries at national request;

-

supporting countries to accelerate progress on SDG targets. In this we will make use of our extensive experience over the past five years with the MDG Acceleration Framework; and

-

making the UN’s policy expertise on sustainable development and governance available to governments at all stages of implementation.

Collectively, all partners can support communication of the new agenda, strengthening partnerships for implementation, and filling in the gaps in available data for monitoring and review. As Co-Chair of the UNDG Sustainable Development Working Group, UNDP will lead the preparation of Guidelines for National SDG Reports which are relevant and appropriate for the countries in which we work.

UNDP is deeply involved in all processes around the SDG roll out. The guidance and tools being developed will be shared as they become available. As well, we are bringing our extensive programming experience to bear in supporting countries to develop their national SDG efforts. There is a briefing session on this on the Board agenda for Thursday.

Financing for development

Financing needs for implementation of the new global development agenda and national development agendas are great. The Addis Ababa Action Agenda, agreed in July, has updated the financing for development framework; set important priorities for development investment – including in social protection, jobs creation, nutrition, and agriculture; and agreed on new global technology and infrastructure financing mechanisms.

The agenda from Addis Ababa highlights the critical need for continued Official Development Assistance, and for its more strategic use to build national capacities for domestic resource mobilization. From inclusive and sustainable growth will flow tax revenue for development spending. Investments in capacities of governments will support tax collection, budget allocation to development priorities, and implementation of policies and plans. Effective governance also builds investor confidence and helps stem illicit financial flows.

On capacity building for domestic resource mobilization, UNDP and OECD have launched a partnership to provide “Tax Inspectors Without Borders”. It will place international tax audit experts alongside national tax authorities, to help build their capacity to assess and collect the tax which should be being paid to them by international companies. The experts will be drawn from North and South.

Looking ahead, we need to ensure that all countries, and in particular the poorest and most vulnerable, are able to access the range of financing opportunities which is available. UNDP is already supporting national partners, especially in LDCs and SIDS, to ensure that diverse financing streams can complement and reinforce each other – for example by implementing Development Finance Assessments, first in seven countries of the Asia Pacific, and now also beginning in Africa. This work maps the complex resource flows, and designs integrated national financing frameworks which will support an actionable agenda on SDGs. It is particularly important to find synergies between development and environment finance. Greater synergies between humanitarian and development finance would help too.

Looking ahead to COP21

Countries now have nine negotiating days left until the Paris Climate Change Conference – COP21 – where the aim is to adopt a new, global agreement on climate change. Agreement in Paris has the potential to stop catastrophic and irreversible climate change – but we are not yet seeing the level of ambition required, as the UN Secretary-General and many others are pointing out. This must change in the interests of all peoples and countries and in particular of the poorest and most vulnerable.

The stakes are high. UNDP will continue to support the “Road to Paris” through sharing expertise and experiences from our $1.3 billion portfolio of climate change mitigation and adaptation projects in over 140 countries; strengthening capacities of negotiators from LDCs and SIDS; and partnering with the COP Presidencies from Peru and France. In addition, we have hosted seven regional dialogues on the technical elements of Intended Nationally-Determined Contributions (INDCs), and are organizing three more in Morocco, Uganda and Samoa. We have also developed the first guidance note to support countries as they make important choices on their INDCs – now distributed among experts, government officials and institutions in 150 countries.

Climate action is definitely needed from governments, but the role of the private sector is also indispensable. Policy and regulatory settings are important – UNDP is supporting countries to amend these to create environments conducive to private sector investment in renewable energy and other areas of adaptation and/or mitigation.

An example – in South Africa and Uruguay, UNDP has been helping to lower barriers to private sector investments in the wind-energy sector. These interventions created new jobs; supported economic growth; diversified energy sources; and contributed to Nationally Appropriate Mitigation Actions (NAMAs).

UNDP is one of twenty organisations approved for accreditation by the Green Climate Fund. We have been working with a number of countries to support preparation of projects for the GCF to consider in its first funding allocation round later this year.

UNDP is planning a ministerial-level event to take place in late February next year, which will be a key occasion to mark both the fiftieth anniversary of UNDP’s founding and the beginning of the SDG era. The event will showcase UNDP’s fifty year journey of promoting sustainable development by supporting the transformation of countries and societies. It will enable us to recognize the substantial long-term collaboration and investments of our partners, and to provide a detailed briefing on UNDP’s approach to and package of support for SDG implementation at country level. A “hold the date” letter is going out now.

* Read the full statement here.

Related News

‘Agrocorridors’ to boost food security

Farming projects along lines of transportation are being promoted as opportunities to attract investment and increase food security.

At a recent event in Nairobi, early-stage venture backer Village Capital brought to a close its programme by inviting a number of startups in the agribusiness space to present their solutions for assisting smallholder farmers.

This saw the likes of Ghana’s Farmerline, which expands access to information to farmers, Rwanda’s Atikus Insurance, an initiative that extends access to credit via reimagined risk solutions, and Mifugo Trade, an online livestock marketing platform, pitching to investors for much-needed financing to scale their businesses.

And in Africa, agriculture is big business.

Across much of the continent, according to the World Bank, agriculture’s contribution to GDP is more than 20%, while in some countries, such as Ethiopia or the Central African Republic, it is higher than the 40-50% mark. Yet farmers, overwhelmingly based in rural areas, traditionally lack access to required networks and finance, with only 1% of commercial loans going to smallholder farmers. This relative underdevelopment of a vital sector, according to UN Food and Agriculture Organisation (FAO) agribusiness economist Eva Gálvez Nogales, is due to a lack of collaboration between various stakeholders, including government and investors.

Nogales is an open proponent of economic “agrocorridors”, which she believes can serve as a strategic tool to bring private capital and large-scale investment to agricultural projects in Africa. This, she believes, will benefit smallholder farmers and boost food security.

Agrocorridors are development programmes that foster agriculture along lines of transportation such as highways, railroads, ports or canals. They integrate investments, policy frameworks and local institutions.

Nogales’ report on the subject for the FAO, ‘Making economic corridors work for the agricultural sector’, highlights a couple of global success stories with agrocorridors, notably the Poverty Reduction and Alleviation Project in Peru, which began in 1998.

The novel approach relied on “star connector firms” that were able to quickly expand commercial networks along 13 corridors in the country, with the result being a “flowering” of overlooked market opportunities. Peru is now the world’s third-largest exporter of artichokes, produced through outgrower contracts and processed in several corridors. The government continued the approach after the bilateral agency responsible for it had departed, and it has been duplicated in a number of sister programmes. In Africa, thus far, the benefits of such agricultural corridors remain mostly overlooked, though Mozambique and Tanzania have started programmes aimed at implementing them. Nogales says implementation is hard work as it requires all stakeholders to rally around an agenda.

“It is a very recent development,” she says. “What has been going on for the last two decades is more transportation corridors linking ports to different cities and production areas to areas of consumption.

“The natural next level in terms of corridor evolution would be trade corridors, but that hasn’t been promoted in Africa for the time being. But for the last two years there has been this movement towards agrocorridors.”

Peru may have seen success with agrocorridors, but there is no “one size fits all” approach, with the FAO report saying effective corridors need to be geared to the competitive advantages of a country rather than “conceived as a miracle method to make a desert bloom”. Nogales says they “should be developed in areas where there is already economic density and untapped growth potential that can be maximised”.

“The idea is not to just invent everything from scratch but to build on what is already going on in terms of transportation and different initiatives,” she says. Collaboration and awareness of mutual benefits are key. Agrocorridors, in principle, give policymakers a framework with which they can assist both consumers and farmers; farmers are provided with better access to markets and credit, and investors are offered supply opportunities to link up with those producers.

“It is about increasing market access and doing that in a way that benefits farmers the most,” says Nogales, adding, “The main challenge for agrocorridors is how to upscale good initiatives that are already taking place but making them wider and attracting other startups, businesses and foreign agribusinesses to follow the examples that are already in place.”

The government’s role in this is crucial, with the development of agrocorridors requiring incentives and the provision of a better investment setup through aspects such as reduced transaction costs.

“The main duty of government is to provide an enabling environment,” says Nogales. “Investments are happening with or without the government’s intervention, but the benefit of agrocorridors for governments is that they can massage and influence investments so they are beneficial for farmers and certain communities.”

Deepening roots

Connectivity, competitiveness and the sense of community are the primary aspect of successful corridors, with stakeholders coming together to identify “soft” targets and harmonise approaches in order to avoid disputes that emerge in the wake of “hard” infrastructure investments. Agriculture as a sector could arguably benefit, but advocates say there are also possible advantages in terms of food security and the environment.

“Corridors can in fact allow for better management of environment risks and practices such as unsuitable monocropping,” says Eugenia Serova, director of the FAO’s Rural Infrastructure and Agro-Industries Division. “The key is for inclusive coordination of stakeholder interests both in the planning and execution phase.”

Extension of this collaboration across borders, increasingly happening within other sectors in various regions of Africa, can only increase the impact of economic agrocorridors. Such an approach has already been tried in Southeast Asia, with the Greater Mekong Subregion corridor programme bringing together Cambodia, Vietnam, Thailand, Laos, Myanmar and some Chinese provinces. Though still in its early stages, there are already improved bridges and customs procedures at border towns and contract farming is beginning to span national frontiers.

Nogales sees this expansion of corridor schemes as potentially beneficial to Africa in the long term too, noting that countries have been hindered by relatively small markets and trade with neighbouring countries. Increasing intra-regional integration could be important for economic growth, but if market opportunities are to be deepened, partnerships and collaboration between government and private sector players may be required both within individual African countries and beyond.

Related News

tralac’s Daily News selection: 2 September 2015

The selection: Tuesday, 2 September

Inaugural speech: Dr Akinwumi A. Adesina (AfDB)

Five priorities will shape our work at the Bank under my Presidency as we advance the implementation of the Bank’s Ten Year Strategy: Light up and Power Africa. Feed Africa. Integrate Africa. Industrialize Africa. Improve quality of life for the people of Africa. Our Bank staff, processes and systems will be shaped to deliver on these critical imperatives. We will become sharply focused on measuring the results of our lending operations on the lives of people. No longer will we judge ourselves simply based on the size of our lending portfolio but on the strength of Africa’s growth and development and the quality of improvements in the lives of the African people. We will be more than a lending institution. We will build a highly competitive, world-class knowledge-driven Bank, to provide top-notch policy and advisory services to countries and the private sector. We will become a true development institution with measurable impacts on the lives of Africans.

African Caucus 2015: Luanda Declaration

We, the African Governors of the IMF and WBG, discussed ways and means through which the Bretton Woods Institutions to support our efforts to: (i) address the challenges of financing for sustainable development; (ii) combating tax evasion and eliminate illicit financial flows; (iii) invest in processing and economic diversification; (iv) finance transformational projects and regional infrastructure; and (v) strengthen the voice and representation of Africa at BWI. [Downloads include: UNECA presentation on economic transformation and diversification in Africa, OECD presentation on illicit financial flows]

Beyond a middle income Africa (ReSAKKS)

The strategic choices facing African countries are important and complex, in light of the major developments occurring across the continent. These developments present both challenges and opportunities and include rapid urbanization, a growing middle class, the rapid rise in the young population entering the labour force, the effects of climate change, and the increased volatility of global food and energy prices. In this context, the 2014 Annual Trends and Outlook Report chapters examine both current and future trends that are likely to shape the trajectory of African economies and the factors driving Africa’s recent growth performance.

The chapters examine the drivers behind the recent growth recovery, the nature and patterns of structural transformation among African economies, past strategies and future outlook for industrialization, the changes occurring in agrifood systems, and the role of major infrastructure sectors in the continent’s past and future growth. They also analyze major global- and continental-level trends that may shape future growth across the continent and affect the region’s integration into global value chains. [Downloads include: Africa in the global agricultural economy in 2030 and 2050, Megatrends and the future of African economies, Renewing industrialization strategies in Africa]

IORA: Enhancing Blue Economy cooperation for sustainable development

The First IORA Ministerial Blue Economy Conference aims to act as an ideal platform to bring together Member States and Dialogue Partners of the Indian Ocean Rim Association to promote Blue Economy in the Indian Ocean region. The conference will focus on four priority areas namely: fisheries and aquaculture, renewable ocean energy, seaports and shipping, seabed exploration and minerals.

Why India must be the leading player in the Indian Ocean region (Economic Times)

Australia must dive into the blue economy of marine resources (The Australian)

Research on Blue Economy gains momentum as Australia and Seychelles' ocean-oriented research institute forges partnerships (Seychelles News Agency)

East African Manufacturing Business Summit: follow it live

Africa welcomes Japan's quality infrastructure model (UNECA)

Infrastructure Africa Business Forum: update (TimesLive)

CEMAC: Transport-transit facilitation (World Bank)

The project's development objectives are to enhance regional trade and integration and sub-regional cooperation between CEMAC and ECCAS member states, and specifically provide the landlocked countries Central African Republic (CAR) and Chad with a better access to the Port of Douala through: (i) assistance to the strengthening of the CEMAC Customs Union; and (ii) improvement of the logistics chain, including road and rail infrastructure to the Port of Douala's hinterland. At a higher level, the project will contribute to the shared growth objectives of the CEMAC countries'PRSPs, by ensuring that the Customs Union is effectively implemented and by improving trade facilitation in the region. It will also support the broader goal of increasing the regional integration of CEMAC member states by improving its core rail and road infrastructure. Furthermore, NEPAD has selected CEMAC as one of the target institutions for Central Africa, and these corridors as the main transport infrastructure to be supported in this sub region.

South African and Lesotho transport ministers meet in Pretoria (The New Age)

The meeting discussed the resuscitation of the Committee of Transport Officials; the process of the uprading of the roads that leads to the borders between South Africa and Lesotho, especially the N8 (under SANRAL), Monantsa (under Free State province) and the Sani pass (under KwaZulu Natal province); the process of the installation of eNatis in Lesotho; the Cross Border Transport issue, particularly the border taxi operators conflict between South Africa and Lesotho and the signing of the Memorandum of Understanding on transport-related matters between the two counties.

Namibia feels the pinch of China’s economic woes (New Era)

“We are definitely impacted by the situation in China because their demand is slowing, but the volumes of trade between us is relatively small, hence so far there is no indication that [bilateral] trade is slowing,” Schlettwein said yesterday. He said there remains space to increase trade because of the recent agreement between the two countries that allows Namibia to export its beef to China. “The volumes of dimension stones and minerals are relatively small, and they are tied into long-term contracts, so I do not think we have a big issue,” he said. “I think if we mitigate it [market crash] early enough we will manage it,” said Schlettwein.

Is 2015 the beginning of the end for Africa’s China-led boom? (Reuters, MoneyWeb)

China-South Africa Economic Forum: update (Global Post)

"You have to transfer skills development and training to the locals. Localize supply chain to value chain. Look at the architecture beneficiation platform for value chain and come to work with us. If you do these you will be successful in this country," dti's Yunus Hoosen, Head for Investment Promotion, said.

Joint China-South Africa arbitration centre set up to resolve commercial disputes (Out-Law)

A new arbitration centre will open in Johannesburg specifically to resolve commercial disputes between Chinese and African parties. The China-Africa Joint Arbitration Centre (CAJAC) will be led by Michael Kuper, the current chair of the Arbitration Foundation of South Africa. Kuper told the industry publication that the new centre would be ready to accept cases from October.

China-Africa International Arbitration Centre: speech by Dep Min John Jeffrey (RSA Department of Justice)

Zambia's power woes: all roads lead to Kariba Dam (Daily Maverick)

Experts have warned that without urgent repairs the Kariba Dam risks collapse, unleashing a ‘tsunami’ of water through the Zambezi Valley, reaching the Mozambique border in just eight hours where it would overwhelm the Cahora Bassa wall, in so doing eliminating 40% of the region’s hydro-electric capacity and putting an estimated 3.5-million human lives at risk. Overlooked, perhaps inevitably, amidst the hyperbole of collapse, destruction and loss of life, is the cost of the poor management of the asset, and the water resource, something that can be relatively easily fixed and where the failure to do so is less dramatic but no less costly. [The author: Greg Mills]

African Governance Architecture Platform: consultation (DGTrends)

The Africa Union Department of Political Affairs, as the Secretariat of the African Governance Architecture Platform, is convening a consultation with the African Union Permanent Representative Committee (PRC) on the operationalisation of the African Governance Architecture and the State Reporting processes under the African Charter on Democracy, Elections and Governance (ACDEG). The PRC consultation will be held from 2 – 4 September, 2015 in Arusha, Tanzania.

Mozambique issues new deadline for completion of Sena rail line rehabilitation (Club of Mozambique)

11th SADC CSO Forum calls for inclusion of citizens in regional decision making (Southern African Trust)

Festus Nghifenwa: 'Regional cooperation on banking regulation – why is it needed?' (New Era)

Durban Marukutira: The wicked side of a dollarised economy (NewsDay)

Carlos Lopes: 'African Migrants - payback time?' (UNECA)

South Korea exports plunge 14.7%, the biggest fall in 6 years (Financial Times)

US-China economic relations: the propeller needs oil (CSIS)

Christine Lagarde, in Indonesia: 'The future of Asian finance', ‘Unleashing Indonesia’s economic potential’

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome. Richard Humphries (Email: This email address is being protected from spambots. You need JavaScript enabled to view it.; Twitter: @richardhumphri1)

Related News

Kenya to lobby WTO for freer trade in services

Kenya will use the December World Trade Organisation’s ministerial conference in Nairobi to push for global liberalisation of trade in services, Foreign Affairs and International Trade Cabinet secretary Amina Mohamed said on Monday.

She said time has come for the 161-member states WTO to lead the process of opening up the services sector, just like it is doing for trade in goods, to ease rising costs especially for developing countries like Kenya.

While there has been a considerable liberalisation in financial intermediation and telecommunications sector, she said, trade barriers remain rife in transport and professional services.

“For example, travelling from here (Nairobi) to London costs twice as much as travelling from London to Washington, while the distance is almost the same,” she said, adding that such barriers are prevalent across the world. “The WTO should lead this process (because) if the standards are set at the WTO-level, everybody else must adhere to that. You cannot go and have a regional treaty that violates the WTO standards or sets higher standards.”

United Nations Conference on Trade and Development secretary general Mukhisa Kituyi said half of Africa’s wealth, as measured by gross domestic product, is now service-driven.

Kituyi called for policies and regulations that support service liberalisation, but emphasised that agriculture should remain part of such negotiations.

“Kenya and Africa must continue insisting that whatever else you do for us in services and other non-agricultural market access, a minimum compromise is required for purposes of fighting rural poverty and, ensure progress is made on agricultural subsidies and support in the developing economies,” he said.

The ministerial conference, held after every two years, is WTO’s top decision making organ.

Related News

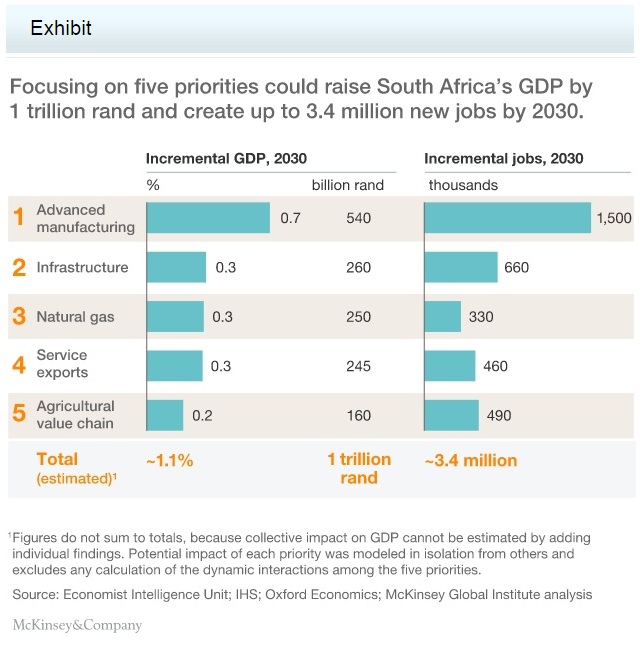

South Africa’s bold priorities for inclusive growth

In the two decades since South Africans worked together to transform their political landscape and usher in a new democracy, the country has made remarkable progress. In particular, GDP has nearly doubled in real terms, lifting millions of people out of poverty and into the middle class and greatly expanding access to services.

Yet since 2008, average annual GDP growth has slowed to just 1.8 percent, while unemployment has stubbornly remained at 25 percent. Given the country’s vibrant public life and dynamic business sector, South Africa has no shortage of ideas, but a tone of pessimism is growing as many worry that the economy is stuck in a low-growth trap.

A new McKinsey Global Institute report, South Africa’s big five: Bold priorities for inclusive growth, recommends reigniting the country’s economic progress by focusing on five opportunities: advanced manufacturing, infrastructure, natural gas, service exports, and the agricultural value chain. If government and businesses prioritize them, these five initiatives alone could by 2030 increase GDP growth by a total of 1.1 percentage points per year, adding 1 trillion rand ($87 billion) to annual GDP and creating 3.4 million new jobs (exhibit).

Here are the “big five” opportunities we’ve identified – and why:

-

Advanced manufacturing. South Africa can draw on its skilled labor to grow into a globally competitive manufacturing hub focused on high-value-added categories such as automotive, industrial machinery and equipment, and chemicals. To realize this opportunity, South African manufacturers will have to pursue new markets and step up innovation and productivity.

-

Infrastructure productivity. While the country is investing heavily in infrastructure, big gaps remain in electricity, water, and sanitation. A true partnership between the public and private sectors could make infrastructure spending up to 40 percent more productive by maximizing the use of existing assets and increasing maintenance, prioritizing projects with greatest impact, and strengthening management practices to streamline delivery.

-

Natural gas. South Africa’s electricity shortage has constrained growth, and, despite new capacity, another shortfall is projected between 2025 and 2030. Natural-gas plants – which are fast to build, entail low capital costs, and have a small carbon footprint – can provide an alternative to diversify the power supply. With the necessary regulatory certainty, we estimate that South Africa could install up to 20 gigawatts of gas-fired base-load power-generation capacity by 2030. Gas can be provided through imports, local shale-gas resources (if proven), or both.

-

Service exports. South Africa has highly developed service industries, yet it currently captures only 2 percent of the rest of sub-Saharan Africa’s market for service imports, which is worth nearly half a trillion rand ($38 billion). With the right investments, service businesses could ramp up exports to the region; and government can help by promoting regional trade deals. In construction, the opportunity ranges from design to construction management to maintenance services. In financial services, promising growth areas include wholesale and retail banking, as well as insurance.

-

Raw and processed agricultural exports. With consumption rising in markets throughout sub-Saharan Africa and Asia, South Africa could triple its agricultural exports by 2030. This could be a key driver of rural growth, benefiting the nearly one in ten South Africans who depend on subsistence or smallholder farming. Capturing this potential will require a bold national agriculture plan to ramp up production, productivity, and agroprocessing.

Successfully delivering on these priorities will move South Africa closer to realizing its long-held vision of a “rainbow nation” characterized by shared prosperity for all. But first, the country will need to embrace some fundamental changes to become more globally competitive; not least, it will have to address a serious skills shortage through a dramatic expansion of vocational training. Tackling such foundational issues will require business and government to come together in a new partnership characterized by shared vision, collaboration, and trust.

Richard Dobbs is a director of the McKinsey Global Institute, where Susan Lund is a partner; David Fine is a director in McKinsey’s Johannesburg office, where Paul Jacobson is a consultant, Acha Lekeis a director, and Nomfanelo Magwentshu and Christine Wu are principals.

Related News

Africa faces five headwinds of concern

With gross domestic product increases of at least fivefold since 2000, Africa’s growth story has been the good news narrative of recent years.

As if little could derail the rise of hitherto uncharted frontier markets like Nigeria, Ethiopia, Angola and Rwanda, economists and related experts have waxed lyrical about almost every business opportunity from infrastructure to consumer to agriculture and financial services.

But recent domestic and international events are precipitating the rise of some stormy headwinds that threaten – at the very least – to provide the exciting growth markets of late with a degree of harsh reality. Here’s a list of the top five issues, which could retard or even set back the advance of the continent.

The China and other syndromes

Africa’s recent rise has coincided with the advance of the Chinese economy and a quest for the supply of commodities that initially attracted Beijing to the continent. Over the last decade, China has become Africa’s single largest trading country (the European Union collectively is still a larger partner) and has forged close economic and political bonds with just about every African state.

Clearly, those countries most exposed to China’s current economic woes may feel the aftershocks. China’s voracious demand for commodities has already contracted. Beijing’s imports from Africa in July were down about 40% from the same month a year ago. A sluggish domestic environment will continue this trend and as China moves more to a consumption-driven economy, expect lower demand for commodities and related raw materials.

And it's not just China – ongoing EU uncertainty, a slowly normalising US interest rate environment and a sharp decline in other developing markets like Brazil and Russia all add to Africa’s uncertainty.

Commodities collapse

Across the board, commodity prices have fallen – and hard. From iron ore to copper to coal, African countries reliant on these exports have begun to feel a contraction. But the real kicker is the price of oil that is still a core export earner for Nigeria, Angola and the Democratic Republic of Congo to name but a few.

Only a year ago, Nigeria and Angola needed oil at over $120 per barrel to balance their respective budgets. With prices now well below half that, national treasuries are slashing their budgets. Cost-cutting is now the order of the day. And, unfortunately, big capital expenditure items like infrastructure may well bear the brunt of financial pruning.

State business interests are also likely to be severely curtailed for a period that could last some time as countries adjust – painfully – to lower state revenues. Already Nigeria’s GDP has almost halved, falling to just 2.3% in the second quarter compared to 3.9% a year ago.

It’s not just oil; the end of the broader commodity super-cycle puts Zambia’s recent advances at risk along with those of Sierra Leone and Liberia.

Currencies crash

With commodities and oil under severe pressure, it comes as no surprise that African currencies have tumbled. The Nigerian naira has slumped 15% over the last year and – unless oil prices rise – may tumble another 10% by the beginning of 2016. The same crisis has befallen South Africa, Kenya, Ghana and Angola whose unit is now 19% weaker against the US dollar.

Crashing currencies have all sorts of negative consequences. Higher rates of borrowing will result in growing budget deficits and possible repayment crises. Ghana has already had to be bailed out by the International Monetary Fund even before the latest bout of global financial flu.

Inflationary pressures on imported goods naturally add strain to a shifting sentiment that may retard global foreign direct investment into the continent after a very bullish decade. And sentiment can be a big driver on equity markets – the Nairobi Stock Exchange has lost almost $1.5bn in value since Januar, confirming a more negative trend.

Middle class can become a floating class

Much has been said about the 330 million plus Africans who have moved up the income ladder over the last decade. However, a large proportion of this ‘middle class’ – about 200 million – live on only $2 to $4 per day. Any broad-based economic decline can push many back into lower categories, thereby upsetting the substantial boom in consumer demand these last few years.

There is a new-found vulnerability to domestic consumption demand as a result of falling GDP rates. These also have the potential to raise political temperatures as austerity-induced budget cuts fuel rising discontent.

Inability to diversify sufficiently

A common human failing is to enjoy the good times but fail to plan for the bad. Africa’s decade of tremendous growth largely failed to transform a continent still reliant on extraction into a continent of manufacturing.

Africa has 12% of global oil reserves, 40% of gold and 80% of chromium and platinum – but still just 1% of global manufacturing and 2% of world exports. Clearly, this is an unsustainable model given the volatility in the current era. The foundations for job-creation for massive future population increases have not been laid nearly adequately. Africa’s cities need substantial infrastructure capex to be competitive, and face serious lags as budgets shrink.

Finally, the continent still has at least 50% of the world’s remaining arable cropland. But environmental issues and drought also place a strain on a sector that, if harnessed wisely, can make Africa hugely resourceful. Land policy and utilisation needs to be a priority like never before.

So, for the first time in over a decade, Africa looks more vulnerable. This represents a major challenge to the continent’s status quo. But equally, Africa is more equipped to deal with change than never before. Regional integration and trade blocks are stronger than ever. Democratic accountability has improved. Technological advances can provide hitherto unimaginable opportunities. And there are green shoots in new manufacturing industries and ICT start-ups that will be critical in fighting these headwinds.

It’s a testing time for the continent – perhaps the most arduous since the ‘Arise Africa’ theme gained global traction. The coming few years will be the real test. It’s now not just about ever-increasing GDP or FDI statistics; it’s how resilient the management of economies can become in times of strain.

It’s not going to be one-way upward traffic any more and global volatility is likely to extend to this continent too. But then again, that’s just the new normal for us all.

Daniel Silke is director of the Political Futures Consultancy and is a noted keynote speaker and commentator. Views expressed are his own.

Related News

Africa projected to have just one low income country by 2050: ReSAKSS 2014 Annual Trends and Outlook Report

Large infrastructure gaps, climate change, high speed of urbanization, and a youthful and rapidly growing population will influence the future pace of growth

Most African countries that today are considered low income will transition to middle income within 15 years, and all but one will be middle income by 2050, according to the Annual Trends and Outlook Report (ATOR), released on 1 September.

The ATOR, released by the Regional Strategic Analysis and Knowledge Support System (ReSAKSS), a program facilitated by the International Food Policy Research Institute (IFPRI), examines the current and future trends that are likely to shape the trajectory of African economies. As the second-fastest growing region in the world, Africa has enjoyed robust economic growth in recent years. However, that progress has not been enough to make up for the lost decades of economic stagnation that preceded the recent recovery. And secondly, the benefits of this growth have not trickled down to the wider population. Today too many people experience poverty and food scarcity.

“While the recent growth performance is encouraging, African counties still face major challenges in terms of reducing poverty and eliminating hunger and malnutrition,” said Ousmane Badiane, IFPRI Director for Africa. “This report shows that policymakers need to continue to refine policies, improve institutions and increase investments to sustain and accelerate the pace of growth as well as its inclusivity or broadness – and the outcomes of their decisions can be the difference between persistent poverty and future shared prosperity for many of Africa’s most vulnerable populations.”

The report found:

-

Africa south of the Sahara is projected to experience more sustained economic growth in GDP per capita between now and 2030 and 2050.

-

By 2050, climate change will result in a 25% increase in cereal prices compared with a no climate change scenario.

-

Trends that are likely to influence the trajectory of African economies include:

-

more volatile food and energy prices;

-

rapid urbanization, increasing incomes, and the rise of a middle class;

-

rapid increase in a young population entering the labor force;

-

greater climate variability; and

-

agriculture as the largest source of employment.

-

-

African diets are changing in response to rapid urbanization and the rise of a middle class. Fifty percent of Africa's population is projected to live in urban areas by 2020. Processed food now represents a significant share of food purchases, even for the rural poor. Diets have also diversified beyond grains into horticulture, dairy, livestock, fish, and pulses.

-

Structural change in Africa is now contributing to productivity growth. Africa's informal goods and services sector (e.g., home goods and handicraft production, and food staples processing) is emerging steadily, and must play a major role in future growth and industrialization.

-

Industrialization in Africa has been weak, and has contributed little to Africa’s recent growth. A new industrial strategy needs to focus on investing in infrastructure, especially energy, transport, and water supply.

“As envisaged under the African Union Malabo Declaration, transforming African economies will need ensuring that future growth is broad based and inclusive, especially of women and youth, a critical component of the Africa We Want as depicted in the Africa Agenda 2063,” said Her Excellency Tumusiime Rhoda Peace, Commissioner for Rural Economy and Agriculture of the African Union Commission (AUC). ‘‘This is a sure way for wealth to be created and jobs to be generated,” she added.

Related News

Adesina assumes office as 8th President of the African Development Bank Group

“We must light up and power Africa – as a Bank we will launch a new deal on energy for Africa”

Former Nigerian Agriculture Minister Akinwumi Adesina formally assumed office as the 8th elected President of the African Development Bank Group (AfDB) on Tuesday, September 1, 2015. At a ceremony in Abidjan, Côte d’Ivoire, he took the oath of office administered by Zambia’s Finance Minister and Chair of the Board of Governors, Alexander Chikwanda.

“I, Akinwumi Ayodeji Adesina, President of the African Development Bank, solemnly declare and undertake … that I will abide by the provisions of … the … Bank, and discharge my duties … with loyalty, discretion and conscience. So help me God,” he swore, to sustained applause by the large audience.

Adesina said that the AfDB had risen to its present level through the efforts of many great men and women, including members of the Board of Governors, the Board of Directors, the past Presidents of the Bank, and the dedication of its staff over 50 years.

“Future generations will look back on your work with respect and admiration. We have a sacred duty to honour your hard work by building upon the solid foundation that you have created.”

Under his presidency, he said, the Bank will expand opportunities and unlock potentials for countries, women, youth, the private sector – and the continent as a whole – with a view to ushering in a new wave of growth and development shared by all. Growth has to be shared, he said. “The sparkle in the eyes of the fortunate few is drowned by the sense of exclusion by the majority. Hundreds of millions of people are left behind. …. Africa can no longer be content with simply managing poverty. For our future and the future of our children, we must eliminate it.

“We must integrate Africa”, he said. “Grow together, develop together. Our collective destiny is tied to breaking down the barriers separating us.

“We will build stronger partnerships for impact – from the private sector, civil society and academic institutions, multilateral and bilateral development agencies. We will advance Africa’s priorities, as envisaged by the Founding Fathers of the Bank. We will be a strong voice for Africa, positioning and building support for Africa in the global environment,” he emphasised.

“We must light up and power Africa”, he said. “Energy is the engine that powers economies.” He promised that the Bank will launch a New Deal on Energy for Africa. “Africa is blessed with limitless potential for solar, wind, hydropower and geothermal energy resources. We must unlock Africa’s energy potential – both conventional and renewable.”

He also stressed the need to develop the private sector to drive the industrialization of the continent, create employment for the young, empower the rural population and women, and lift millions out of poverty.

Adesina made it clear that “Africa must feed itself,” stating that it was inconceivable that a continent with abundant arable land, water, diverse agro-ecological richness and sunshine should be a net food-importing region. Africa has 65% of all the arable land left in the world, which can help meet the food needs of 9 billion people on the planet by 2050. This is a huge untapped potential, “but Africa cannot eat potential”.

He laid down five priorities that will drive the Bank’s work as it implements its current 2013-2022 Strategy: “Light up and Power Africa. Feed Africa. Integrate Africa. Industrialize Africa. Improve quality of life for the people of Africa.”

“Our Bank staff processes and systems will be shaped to deliver on these critical imperatives. We will become sharply focused on measuring the results of our lending operations on the lives of people. No longer will we judge ourselves simply based on the size of our lending portfolio, but on the strength of Africa’s growth and development and the quality of improvements in the lives of the African people. We will be more than a lending institution. We will build a highly competitive, world-class, knowledge-driven Bank, to provide top-notch policy and advisory services to countries and the private sector. We will become a true development institution with measurable impacts on the lives of Africans,” he said.

He ended with a call to action: “Let us rededicate ourselves to a greater Africa. An Africa with prosperous, sustainable and inclusive growth – one that is peaceful, secure and united, regionally integrated and globally competitive. A continent filled with hope, opportunities, liberties and freedom, with shared prosperity for all. An Africa that is open to the world, one that Africans are proud to call home.”

Nigeria’s Vice-President, Professor Yemi Osinbajo, spoke on the need to consider other paradigms for Africa development, and to focus on good governance, climate change and the empowerment of women.

Alassane Ouattara, President of the Republic of Côte d’Ivoire, reminded the audience that the African continent currently faces multiple challenges including security, market volatility, and youth unemployment. He said he was convinced that President Adesina would be able to tackle these challenges, given his experience and proven leadership.

Among those who attended the ceremony were Cape Verde’s former President Pedro Pires, Côte d’Ivoire’s Prime Minister Daniel Kablan Duncan, former Nigerian Finance Minister, Ngozi Okonjo-Iweala, as well as a large delegation of governors, legislators and business-people from Nigeria.

Minister Chikwanda had called the occasion “a historic changing of the guard for the African Development Bank, the pride of Africa.”

Related News

Is 2015 the beginning of the end for Africa’s China-led boom?

Africa-focused economists caught off-guard on China weakness.

Disappointing growth in Africa’s two biggest economies has highlighted the role of China in the expansion of recent years, now that China’s own economy is slowing.

Expectations of more than 4% growth in Nigeria, Africa’s largest economy, are probably now too high, and South Africa’s prospects also look in need of revising.

Second-quarter growth for both countries was worse than the most pessimistic forecasts – in South Africa’s case, by the biggest margin in at least half a decade of Reuters polls.

Their slowdown is similar to other emerging market economies in Latin America and Asia, and a sign that China’s appetite for raw materials is now waning.

On Tuesday, the latest purchasing managers’ data showed the weakest growth in 6 1/2 years for small- to mid-sized China manufacturers and the weakest in three years for larger enterprises.

Economists have long been aware that commodity-exporting countries would be troubled by China’s rebalancing to a more consumer-driven economy. They have been warning since the shift began that investors would have to make do with slower growth.

“With growth slowing in Nigeria and collapsing in South Africa, our prediction that 2015 would be Africa’s most difficult year so far this century seems, unfortunately, to be playing out,” said John Ashbourne at Capital Economics.

“The key point is that high oil prices over the past decade may have led both investors and policymakers to ignore the deep structural problems within Nigeria’s economy. Now that prices have fallen, those flaws have been exposed.”

In addition, the Federal Reserve expects inflation to accelerate, making an increase in US interest rates more likely. But many emerging market policymakers say they are ready for a US rate rise, and they are now focused on dealing with a slowing Chinese economy.

FUNDAMENTALS REMAIN INTACT

Two months ago, the Reuters long-term consensus on Nigeria was for 4.4% growth this year. But a drop to 2.35% in the second quarter – from a record high of 8.6% in the fourth quarter of 2010 – puts that at risk.

South Africa, the continent’s second-biggest economy, shrank 1.3% in the second quarter – worse than any of the 21 economists polled by Reuters had predicted. That makes the consensus for 1.9% growth this year, already weak by emerging market standards, look too optimistic.

Razia Khan, Africa research head at Standard Chartered, says in the next decade, the structural drivers of Africa’s growth – rising demographics, greater rates of urbanisation, productivity gains, growth of financial markets, will remain in place.

“However, in the very near future, external headwinds -deteriorating risk appetite and weaker commodity prices – may well take the shine off growth trends,” she said.

The World Bank forecasts GDP growth in sub-Saharan Africa will slow this year to 4.2%, down from an average of 6.4% during 2002 to 2008.

Even after a decade of growth, sub-Saharan Africa’s manufacturing remains weak. Exports from the region more than quadrupled to $457 billion in the decade to 2011, but manufactured goods made up just $58 billion of that.

Africa could have rebalanced its own economies, by shifting from commodity-led growth to inter-regional trade. But neglected infrastructure looks set to keep the continent reliant on commodities.

“Africa remains largely a primary goods exporter. There are growth opportunities to be found in forward-integrating its largely primary industries,” said Rafiq Raji, an economist at macroafricaintelligence.com, a research service based in Lagos.

Related News

DG Azevêdo: “Let’s make Nairobi a success”

In his speech in Costa Rica during his current official visit to Central America, WTO Director General, Roberto Azevêdo, talked about the importance of the early ratification of the Trade Facilitation Agreement and the recent expansion of the Information Technology Agreement as a good inspiration for a successful Nairobi Ministerial Conference in December.

It is a great pleasure to be in Costa Rica. I thank you for your kind invitation.

I am pleased to have the opportunity to meet with you during my first visit to Costa Rica as Director-General of the World Trade Organization. Actually, this is my first time in Costa Rica, full-stop!

And especially so as we celebrate the 20th anniversary of the WTO.

Since its foundation in 1995, the WTO has shown that trade can be an important element in promoting development and growth.

Costa Rica has been an important partner in that mission, as well as an example of the role trade can play in leveraging opportunities and competitiveness.

Costa Rica became a Member of the WTO’s predecessor, the General Agreement on Tariffs and Trade, in 1990. And, in 1995, it became a founding Member of the WTO.

Ever since then you have played a very active role.

I would like to thank Minister Mora and Ambassador Álvaro Cedeño Molinari for their leadership and commitment.

Costa Rica played an important role in the negotiations which led to the Trade Facilitation Agreement, which we are discussing here today. I’ll come back to this in a moment.

Your country also plays a major role in supporting the Organization’s day-to-day work.

For example, since February 2006, Ambassador Ronald Saborío of Costa Rica has chaired the negotiating group which discusses potential reforms to the rules underpinning dispute settlement in the WTO. This is one of the main pillars of the WTO’s work. It is where Members resolve major trade disputes – and so potential reforms of this system are hugely important.

Indeed, as a small country, Costa Rica is known at the WTO for punching above its weight.

This is one of the strengths of the Organization. All Members have a seat at the table, all voices are heard. So it’s up to you how loudly you want to speak – and Costa Rica speaks very loud!

I think there are a number of reasons for this prominent role.

Costa Rica is blessed by its geography. Located between the Caribbean and the Pacific, and connecting the Americas, Costa Rica is extremely well-positioned to trade.

Moreover, despite its relatively small size, Costa Rica has one of the most attractive business climates in Latin America.

The stability of governance and the skills of the workforce combine to make this country very attractive to investors.

And Costa Rica has seen impressive growth in recent years.

Over the last 20 years GDP per capita has tripled.

And I think trade has played an important role as an engine of growth.

Over the same period, since 1995, Costa Rica’s goods exports have also tripled in value.

Now, of course, this is not to sound complacent.

The financial crisis had an impact here, as it did everywhere. And still, economic conditions are not as favourable as they could be.

So the work to promote growth and development continues.

I think that trade will be more important than ever in terms of how we move forward.

So let me say a few words about the role of the WTO in this context.

ROLE OF THE WTO

In the 20 years since the birth of the World Trade Organization, the world has seen huge changes.

New centres of economic growth have emerged. New technologies have proliferated. Communication has been revolutionized. In 1995, less than 0.8% of the world’s population used the internet, while in 2015 it was around 44%.

We live in a world that is more interconnected than ever.

Today globalization is fact of life. So the question is less about whether or not we like globalization – it is more about how we should respond.

Closing markets will increase inefficiencies and costs. More than that, in the long run many jobs will be lost. In the end, protection leads to a downward economic spiral, which then becomes a difficult trend to revert.

The protectionism of the early 1930s, following the Wall Street Crash, wiped out two thirds of world trade.

We did not repeat that mistake after 2008. Governments did not respond with wholesale trade restrictions. Instead the policy response was mostly very restrained. And this was due largely to the fact that governments knew that they were bound by rules and obligations of the multilateral trading system. Introducing protectionist measures would have had costly consequences – even authorized sanctions under the dispute settlement mechanism.

So we need to value and maintain the trading system to ensure that countries like Costa Rica can compete in a fair, predictable, transparent and rules-based environment.

And we need to ensure that the system can evolve to reflect the realities of today.

We have seen the scope of the Organization increase dramatically over these 20 years. We have welcomed 33 new Members: from China and Russia, to some of the least developed economies.

Our membership will shortly rise to 162 with the accession of Kazakhstan which is expected later this year. And we hope that Liberia will follow soon.

We have also worked hard in providing more transparency.

The WTO has proved very effective as a forum where Members can monitor each other’s practices and regulations to ensure that agreements are being observed.

The regular work of WTO bodies, for instance, enables countries to exchange information, to raise concerns and to suggest new approaches.

When difficult issues arise, the WTO has provided a place for dialogue that very often results in mutually acceptable understandings.

If those understandings don’t materialize, we offer a dispute settlement mechanism that has a solid track-record on the international stage.

In just 20 years we have successfully dealt with almost 500 trade disputes, helping our Members settle their differences in a fair, open and transparent manner.

And the topics that are being handled in the dispute settlement mechanism show that the WTO is in tune with current issues.

Recent disputes touch upon the relationship of trade and renewable energy; policies to discourage tobacco consumption; packaging information for consumers; preservation and management of exhaustible resources; and many other issues.

As jurisprudence develops and new precedents are set, the dispute settlement system has allowed the rulebook to evolve and modernize.

Of course, the system also evolves through negotiating new trade rules. This is often where the most focus is placed in the media, and it is an area where we can deliver much, much more.

Many argue that the difficulties in advancing the Doha Development Agenda show that the Organization has lost its ability to negotiate.

However, while those difficulties are very real, the reality is that Members are negotiating all the time – and delivering.

Just last month we recorded a major negotiating success when a group of WTO Members laid the basis for an expansion of the WTO’s Information Technology Agreement.

Costa Rica is part of this agreement.

This is the first tariff-cutting deal at the WTO in 18 years – and it is a big one! It will eliminate tariffs on over 200 IT products. Trade in those products is valued at over 1.3 trillion dollars each year.

Eliminating tariffs on trade of this magnitude will have a huge impact. It will support lower prices, create jobs, and it will help boost GDP growth around the world. Besides, while the expansion was agreed by a group of Members, its benefits will apply to all.

This success comes quick on the heels of the WTO’s successful Bali negotiations in 2013.

These negotiations led to the “Bali package”, which comprised a set of ten decisions, including:

-

steps on agriculture;

-

measures for LDCs;

-

and, of course, the Trade Facilitation Agreement – the first multilateral agreement since the WTO was created.

Let me say a few words on the significance of this agreement.

It will substantially reduce trade costs, by delivering simpler, more predictable, and streamlined border procedures.

Studies suggest that the full implementation of the Trade Facilitation Agreement could reduce worldwide trade costs by between 12.5% and 17.5%.

It is estimated that it could bring a boost in trade worth up to 1 trillion dollars and create 21 million jobs, 18 million of which would be in developing countries.

Besides its economic significance, the Trade Facilitation Agreement has a number of innovative features, including its novel implementation architecture.

It allows for more flexible implementation by developing countries. It also says that practical help must be provided, where needed, to developing countries.

And we have set up a new initiative – the Trade Facilitation Agreement Facility – to ensure that developing countries get the help they need to develop projects, find partners and access the necessary funds.

Now, two thirds of Members must ratify the agreement before it can enter into force. Some have done so, but we need to increase the pace.

Therefore, I am very pleased to hear that Costa Rica will submit the agreement for legislative approval later today.

That will be an important step to realize the gains that the agreement will bring.

And again it shows your leadership on trade issues. I hope that others in the region will follow this lead and move forward with their ratification processes.

Steps taken to improve trade and integration at the regional level can be very important in boosting trade and in complementing the multilateral system.

Costa Rica itself is part of several ventures of this nature, such as:

-

the Central American Common Market;

-

the Dominican Republic-Central America-United States Free Trade Agreement;

-

as well as numerous bilateral initiatives.

Trade liberalization is contagious, and so regional efforts can serve as an inspiration towards global agreements.

However, it is also important to note that there are many big issues, such as agricultural or fisheries subsidies, which simply cannot be efficiently tackled outside the WTO.

Today the WTO’s system of rules and disciplines covers around 98% of global commerce.

At a time when the global economy is more interconnected than ever, I think it is difficult to imagine a world without the WTO and the multilateral trading system.

CAPACITY BUILDING

But openness by itself is just not enough to promote the widespread, equitable growth that I think we all want to see.

Liberalization must be accompanied by complementary policies that facilitate an enabling environment.

Too often, poor infrastructure and complex border procedures make countries uncompetitive. They can also distance whole segments of the population – especially in rural areas – and Small and Medium Enterprises from the benefits that trade can provide.

To avoid continued marginalization, a range of policies can be effective to improve connectivity, business environments, logistics and trade facilitation.

This is why providing practical support to build capacity is another crucial element of our work at the WTO.

That’s what Aid for Trade is all about. To date, more than 245 billion dollars have been disbursed for official development assistance programmes and projects.

Costa Rica is a recipient of Aid for Trade – and we are seeing the results on the ground.

In 2006 it took on average more than 35 days to export. In 2014 this was just below 15. I’m sure we can do even better.

Implementing the Trade Facilitation Agreement will help to further increase that efficiency, which helps to cut costs and raise competitiveness.

Indeed, trade facilitation was one of the top priorities mentioned by participants of an Aid for Trade survey in Costa Rica.

CONCLUSION

So I am determined that we should keep building on all of this work. And I think that there are two immediate priorities:

-

First – we must move forward and implement the decisions taken in Bali, to ensure that the significant benefits promised are delivered – including the Trade Facilitation Agreement.

-

And second, we must make further progress on the Doha Development Agenda.

With this in mind, much hard work is going on in Geneva.

At the end of the year, we will hold our 10th Ministerial Conference in Nairobi, the first time it has been held in Africa.

During the first semester, progress has been modest. But we have been able to start tough discussions on the main issues, such as agriculture, industrial goods, and services.

And we have had engagement at a level that we haven’t seen for some years.

However, there are still significant gaps to bridge.

If we want to deliver substantive outcomes by Nairobi, we have to redouble our efforts.

Nairobi is our number one focus.

And we will take inspiration from the success of Bali – and the recent breakthrough on the ITA.

May these successes be an inspiration on our road towards Nairobi.

We have a long journey ahead and Costa Rica’s support and active participation in the months to come will be crucial.

So I urge you to stay engaged in every way you can – and keep displaying leadership in Geneva.

Let’s make sure we end this year with real results in Nairobi, and lay the foundations for another successful 20 years.

I would like to thank you once again for this invitation and for your very kind attention.

Thank you.

Related News

tralac’s Daily News selection: 1 September 2015

The selection: Tuesday, 1 September

Donald Kaberuka, AfDB President 2005-2015 (AfDB)

Sovereign wealth funds can ease Africa risks, new AfDB head says (Bloomberg)

Africa rising: the new growth agenda (International Growth Centre)

The IGC has now published 'Africa rising: The new growth agenda', a conference report summarising the lectures, panels, and framework sessions from the 3rd annual Africa Growth Forum. Africa Growth Forum 2015 was attended by 186 delegates, including researchers and policymakers from over 20 different countries and 50 different institutions and ministries. [Downloads available]

Intra-African trade rises as market access between blocs improves (The EastAfrican)

Intra-African trade increased by 50% to $61bn between 2010 and 2013, according to recent data released by the African Development Bank. The rise is attributed to improved market access and a strong growth in re-exports among African countries.

Trade between China and Sub-Saharan Africa: can the reliance on raw materials be reversed? (Bridges Africa, ICTSD)

It appears that trade policy has only little room for manoeuvre. Bilateral tariff elimination will yield only limited gain because China is already one of the most open markets for African countries. China’s average tariffs towards least developed countries in general, and SSA in particular, are already low: between 2005 and 2010, the weighted average tariff fell from 2 to 0.5 percent (average tariff fell from 7.14 to 2.83 percent). Because SSA’s export volume to China is small, the tariff reduction has limited welfare and terms of trade effects. [The authors: Manitra A. Rakotoarisoa, Cheng Fang]

Economic Partnership Agreements: what has Africa gained and what can it lose? (Bridges Africa, ICTSD)

It is therefore timely for ACP policymakers to forge strategic responses, by taking bold steps within their own intra-regional trade agenda, as a way to mitigate the ‘tsunami effect’ of mega trade deals. It may also be appropriate to build strategic alliances with other non-participating countries, in order to take the lead at the WTO to address some of the issues that might affect the global trading system once those mega-trade deals are agreed. [The author: Isabelle Ramdoo]

South Africa: July 2015 merchandise trade statistics (SARS)

The South African Revenue Service has released trade statistics for July 2015 that recorded a trade deficit of R0.40bn. This figure includes trade data with Botswana, Lesotho, Namibia and Swaziland. The R0.40bn deficit for July 2015 is due to exports of R94.21bn and imports of R94.61bn. Exports increased from June 2015 to July 2015 by R4.26bn (4.7%) and imports increased from June 2015 to July 2015 by R10.14bn (12.0%). The cumulative deficit for 2015 is R25.23bn compared to R53.37bn in 2014. [Download]

South Africa’s bold priorities for inclusive growth (McKinsey Global Institute)

A new McKinsey Global Institute report, South Africa’s big five: Bold priorities for inclusive growth, recommends reigniting the country’s economic progress by focusing on five opportunities: advanced manufacturing, infrastructure, natural gas, service exports, and the agricultural value chain. If government and businesses prioritize them, these five initiatives alone could by 2030 increase GDP growth by a total of 1.1 percentage points per year, adding 1 trillion rand ($87 billion) to annual GDP and creating 3.4 million new jobs. [Downloads available]

Pakistan firm fights SA duty (Business Day)

The International Trade Administration Commission, which investigates and sets tariffs on imported products, is facing legal action by a Pakistani cement firm. South Africa’s four largest cement companies have been named as respondents. The Karachi-based firm has filed papers in the High Court in Pretoria contesting the 14.29% provisional antidumping duty imposed in May on its cement exports to the Southern African Customs Union following complaints by local producers. Itac plans to oppose Lucky Cement’s application for the court to set aside its decision.

ArcelorMittal SA steel mills to close as industry crisis bites (Business Day)

Ben Turok: Haggard country is crying out for sagacity (Business Day)

Irvin Jim decries state incoherence (Business Day)

Botswana: Moody's sees a wider budget deficit for Botswana (Mmegi)

Botswana’s projected P4 billion budget deficit for the 2015/16 financial year could turn out to be much larger due to the downturn in the diamond market, credit rating agency, Moody’s says.

Madagascar: systematic country diagnostic (World Bank)

Chapter four discusses the role and challenges of the private sector, the main driver of growth. Chapter five discusses the challenges for achieving higher human capital in a country with a very young population and some of the highest infant stunting and malnourishment rates in the world. Chapter six discusses the faces of poverty, which are predominantly rural, agricultural and informal. A structural transformation has not started in Madagascar and poverty and environment are closely intertwined. The chapter also discusses the challenges to enhancing the management of natural resources and protecting the poor from natural disasters and impacts of climate change. Chapter seven summarizes the challenges and prioritizes the reforms.

Made in Brazil, packed in Kenya: how tariff windows feed Kenya’s sugar cartels (Daily Nation)

Has Uganda been re-exporting into Kenya the sugar it imports duty-free from Brazil? Do the Ugandans really have a sugar surplus as they claim? These two questions are at the heart of the controversy over sugar imports from Uganda, yet if indeed Uganda is re-exporting sugar into Kenya, then what the political opposition should be fighting for is stricter inspection of imports from Uganda for compliance with rules of origin under the East African Customs Union. So far — and despite the polarised debate among the political elite as to whether President Uhuru Kenyatta signed away major concessions on sugar imports during his recent visit to Uganda — there are no indications that the stipulations on rules of origin have been eliminated, or even relaxed, from Uganda sugar imports. [The author: Jaindi Kisero]

John Kamau: 'The fall — and rise — of Tanzania’s Kilombero, and Tom Mboya’s fears over Kenya sugar firms' (Daily Nation)

Wamwangi clashes with privatisation team over sugar mills sale (Business Daily)

Why Kenya should stop the fight (Daily Monitor)

Exit Kenya’s sugar, enter Tanzania rice: Kampala’s new trade war (The EastAfrican)

Tanzania: Mega rail project ‘to start soon’ (The Citizen)

President Jakaya Kikwete will officiate at the ground-breaking ceremony for the much-anticipated standard gauge railway line in the next two weeks, Transport minister Samuel Sitta said yesterday.

Preventing conflict in Central Africa: ECCAS caught between ambitions, challenges and reality (ISS)

The Economic Community of Central African States has a long way to go in preventing regional crises. Many challenges remain in making the infrastructure (especially the Central African Early Warning Mechanism and the Central African Multinational Force) operational and effective, and there is a gap between ambition and reality. These obstacles and challenges include ECCAS’ highly centralised and state-focused structure; a narrow, militaristic approach to security issues; and the wider institutional setting. Matters of responsibility in relation to the African Union also remain unresolved. With regard to the cross-border dimension of security issues and the high number of upcoming elections in the region, ECCAS’ participation in maintaining peace appears crucial.

Remittances from West Africa’s Diaspora: financial and social transfers for regional development (AfDB)

Migrant remittances, namely the money migrants send to their countries of origin from their host countries, are increasingly significant for West Africa. In 2014, the amount sent home totalled US $26 billion (of which US $20.9 billion was sent to Nigeria) and amounted to 3.2% of the region’s GDP. The magnitude of these transfers, which make West Africa the second recipient sub-region on the continent, reflects the size of the West African diaspora, estimated at 9.1 million people in 2011, or 2.6% of the population of the region. As recently highlighted in the 7th edition of the West Africa Monitor Quarterly these financial flows are an opportunity for regional development. [West African Quarterly Monitor]

Nigeria: External reserves rise to $31.43bn (ThisDay)

Nigeria's foreign exchange reserves were $31.43bn on August 27, up by 1.12% from $31.08bn a month earlier, data from the Central Bank of Nigeria showed on Monday. The forex reserves of Africa's top crude exporter were down 20.65% year-on-year from $39.61bn a year ago.

‘Nigeria spends $1.5bn annually on importation of tomato products’ (ThisDay)

Director General and CEO of the Raw Material and Research and Development Council, Dr Husaini Ibrahim, has revealed that Nigeria spends around $1.5 billion annually on tomato products importation from China and other parts of the world. Ibrahim said such imports were unsustainable following the economic downturn befalling the country, and added that the country can reverse the trend with the introduction of improved seeds that yield more in dry season farming.

Tomorrow, in Harare: Stakeholders workshop on draft competition policy for Zimbabwe (UNCTAD)

Kazungula Bridge Project: construction of Zambia One Stop Border Post facilities (AfDB)

Gerard Kambou: Impact of low oil prices on sub-Sahara Africa’s economies and lessons learned (World Bank)