Search News Results

Deepening our commercial engagement with Africa

In July, President Obama visited Africa and shared an important message at the Global Entrepreneurship Summit in Nairobi and at the African Union in Addis Ababa. He said “As Africa changes, I’ve called on the world to change its approach to Africa. So many Africans have told me, we don’t want just aid, we want trade that fuels progress. We don’t want patrons, we want partners who help us build our own capacity to grow. We don’t want the indignity of dependence, we want to make our own choices and determine our own future.”

Today, the citizens in countries across sub-Saharan Africa are certainly making their own choices and determining their own futures, represented by the fact that the economies in this region are among the fastest growing in the world. And when it comes to the U.S.-Africa commercial relationship, more than any at other time in history, these countries are not dependent. They are equal stakeholders in our business and trade relationships.

The U.S. and Africa today stand as engines of mutual economic growth and prosperity. African exports of non-petroleum goods since 2009 have doubled, creating and sustaining more than a million jobs in Africa. The U.S. was also a leading driver behind the region achieving a record in foreign direct investment of roughly $80 billion last year.

As the head of the International Trade Administration, an agency whose mandate is to create opportunities for U.S. businesses by promoting international trade and attracting foreign direct investment, I fully understand how African businesses are creating such opportunities. On the U.S. side, goods exports to Africa have increased by nearly 60 percent since 2009, and these exports support 250,000 American jobs.

But today, the total amount of American trade with every country on the African continent is roughly equal to our trade relationship with the single country of Brazil. There is enormous potential for us to do so much more. By deepening our commercial engagement in Africa, we can generate even greater growth and prosperity for Africans and Americans.

Trade Winds - Africa will help ensure that our partnerships continue to deepen and expand. It is the largest-ever U.S. government-sponsored trade mission to Africa, involving approximately 108 U.S. companies. In addition to a business development forum and trade mission in South Africa, Trade Winds will stop in seven other sub-Saharan African countries – Angola, Ethiopia, Ghana, Kenya, Mozambique, Nigeria, and Tanzania. The forum participants will include local and American market experts, Fortune 500 companies, small businesses, and government decision-makers. Our Commercial Service officers and State Department colleagues will organize business networking events with leading industry and government officials at the forum, and matchmaking meetings with potential partners at the trade mission stops. And when it is over, not only will we have conducted the largest trade mission to the African continent in American history, I hope that we will see new trade deals that will benefit the economies of countries on both sides of the Atlantic.

Trade Winds - Africa is a critical element of our Doing Business in Africa (DBIA) Campaign. DBIA was launched as an unprecedented whole-of-U.S. government effort to deepen commercial engagement between the U.S. and African countries. Under DBIA, U.S. companies have announced new deals worth more than $14 billion; the Secretary of Commerce has established the President’s Advisory Council on Doing Business in Africa, a federal advisory committee comprised of business leaders that advise the President through the Secretary of Commerce on strengthening commercial engagement between the United States and Africa; and the President has announced the Power Africa campaign, which will work to add 30,000 new megawatts of electricity generation capacity to this part of the world.

Trade Winds - Africa and DBIA reflect the United States’ commitment to further advancing our commercial engagement with Africa. And, perhaps more importantly, they reflect our understanding that deepening our commercial engagement secures our mutual commercial interests. Also importantly, our commercial partnership is essential to the interests of maintaining the international order.

As former president of the World Bank Robert Zoellick once said, “responsible stakeholders recognize that the international system sustains their peaceful prosperity, so they work to sustain that system.” Trade and investment, open markets, and strong institutions have been the core elements of that international system: from Europe, to the Asia-Pacific region, to Latin America. And these are the core elements behind the political and economic development we are seeing and will continue to see in Africa today. Just as with the U.S.-Africa commercial relationship, more than at any other time, Africa is a mutual stakeholder in the international order as well.

As we embark on this historic trade mission, it is important to recognize what Trade Winds - Africa, as well as our larger commercial partnership, represents. That the relationship between the United States and African countries is more mutually beneficial, prosperous, and consequential than it has ever been before. And the trajectory is only pointing upward.

Stefan M. Selig serves as President Obama’s Under Secretary of Commerce for International Trade at the U.S. Department of Commerce.

Related News

How to boost sustainable investment for a post-2015 development agenda

What kind of international effort might be required to facilitate sustainable investment?

The global challenges of poverty, sustainable growth, and climate change are being tackled with renewed vigour through a post-2015 development agenda and accompanying sustainable development goals. This will see many countries embark on the design of national development strategies for 2030. Nations are also currently announcing their national climate action plans as part of an effort to ink a deal in December on a post-2020 multilateral climate regime. On the trade side, while uncertainty remains around the Doha Round trade talks, the WTO Trade Facilitation Agreement (TFA) is expected to enter into force sooner rather than later. The outcome document from the Third International Conference on Financing for Development (FfD3) held in Addis Ababa, Ethiopia from 13-16 July, meanwhile, strengthened international commitments and guidelines around development finance. Investment is common to all these processes that will, one way or the other, update the global development vision and in turn increase demands for quantitatively more investment that is also qualitatively more sustainable.

Shifting investment perspectives

Seen from some angles, investment remains a contentious multilateral issue, with divisions over the future of the international investment regime, rising numbers of disputes and criticism of their settlement, and close scrutiny of corporate contracts by media and civil society. Perspectives on foreign direct investment (FDI) have nonetheless evolved greatly over the years, for example, moving from closure to openness or from positive to negative lists. A few facts help to illustrate countries’ current broader openness to FDI. According to the UN Conference on Trade and Development (UNCTAD), some 80 percent of regulatory changes from 2000-2013 involved liberalisation or promotion, while the number of international investment agreements rose to 3268 by the end of 2014.

FDI demand stems from larger search for investment, not just for current growth, but also for sustaining future growth. Major demographic and energy transitions will require significant investments in education, energy, and infrastructure to mitigate and adapt to the threat of climate change. These needs outstrip the ability to finance investments through public expenditure, even in developed countries, and FDI is also a critical mechanism to help spread technological innovation across the globe.

The links between trade and investment more generally have equally become clearer over the years. Firms increasingly locate specific activities wherever it is best for them to maintain or increase their international competitiveness, helping to boost FDI, and giving rise to the concept of global value chains. FDI and trade are necessary complements for an integrated international production system that can act as an engine of growth.[1] Investment can, moreover, help to boost trade. The WTO TFA promises to reduce transaction costs at the country level by 10 to 15 percent. Reduced trading costs improves a country’s locational advantages that attract efficiency-seeking FDI. If FDI is not forthcoming, then the advantages of trade facilitation are less compelling. Alternatively, potential benefits to a host country would multiply if trade facilitation proceeds jointly with investment facilitation to attract FDI, and promote linkages with domestic enterprises and SMEs active in segments of arm’s length trade.

Bridging the sustainable investment gap

When accounting for all infrastructure needs ranging from water to telecommunications, the gap in global investment is at least US$1 trillion per year. An estimated US$5-7 trillion worth of annual investments, meanwhile, may be required to achieve the SDGs. Can this gap be bridged and needs met? From investor perspective the answer is affirmative, it is a matter of policy, not money. Answering the call of the post-2015 development agenda will require innovative partnerships incentivising private investment in social infrastructure. Global financial markets have abundant funds, including for niche activities such as impact investment, microfinance, and green investment. Civil society and the private sector already play an active role in areas such as education, health, extractive sector, and garments. For example, following the 1992 Rio Earth Summit, world industry associations began preparing responsibility guidelines.

For governments, despite development fatigue and budgetary constraints, many states are open to partnering with the private sector. The rationale for such cooperation is enlightened self-interest, in other words, leveraging donor assistance to enlist private resources to support recipient countries in implementing shared commitments on trade and sustainable development. Governments are, however, expected to lead the process. National policies in many cases can provide the critical enabling environment for investment. Potentially, all investment is sustainable, but depends on discovering and putting in place the appropriate policy and institutional frameworks.

What needs to be done?

Regulation and promotion are the basic policy levers to enhance investment. While most countries have liberalised laws governing entry, treatment, and exit of FDI, these are often inadequate, and where regulatory support infrastructure exists, clarification or improved coordination among different levels of government may still be needed. In many countries, the overall regulatory environment can be made more transparent, and the costs of doing business lowered. However, in the global competition for FDI, it is also important that investment should advance larger development objectives. Governments frequently offer generous fiscal incentives that do not induce specific development activities. Regulatory exceptions should avoid the sacrifice of long-term objectives for short-term gains. But policy experience in incentivising private investment in sustainable development activities is as yet nascent. Demonstration projects, pioneering partnerships involving multiple stakeholders, and institutional capacity in the public sector receptive to positive engagement with the private sector are needed. Many of these suggestions might be helped by an international support programme for sustainable investment facilitation.

Contours of sustainable investment facilitation

Such a programme would focus on the “nuts and bolts” of encouraging the flow of sustainable FDI to developing countries. Moreover, many developing countries and particularly the world’s poorest nations, do not possess the capacity to compete successfully in the world market for FDI and therefore require particular assistance to meet substantial investment needs. The programme would complement various efforts to facilitate trade, in particular, through the WTO led Aid-for-Trade Initiative and the recently adopted WTO Trade Facilitation Agreement. In a world increasingly dominated by global value chains, the latter address the trade side of the equation, while an international support programme for sustainable investment facilitation would address the investment side. Analogous to WTO efforts, a sustainable investment support programme would be entirely technical focusing on a range of practical actions to encourage the flow of sustainable investment to developing countries, with the aim of fostering their economic growth and development. These undertakings would in turn need the support of official development assistance, especially for least developed countries, to strengthen the basic economic determinants of FDI.

Defining sustainability characteristics of international investments is challenging. An international or non-governmental organisation could establish a multi-stakeholder working group to prepare an indicative list of FDI sustainability characteristics to use as guidance by governments seeking to attract sustainable FDI. This could include, for example, carbon dioxide-neutral foreign affiliates. This identification would also be helpful for governments wanting to encourage sustainable domestic investment. UNCTAD’s Investment Policy Framework for Sustainable Development and the OECD Guidelines for Multinational Enterprises or newly launched Policy Guidance for Investment could provide inspiration in this respect. Defining sustainable FDI is also increasingly required for investor-state disputes. The same applies to international investment agreements as these increasingly make reference to sustainable development.[2] The working group could, in addition, identify mechanisms to encourage the flow of sustainable investment that go beyond those used to attract FDI in general. At the national level, special incentives could be one of the tools used by governments for this purpose. At the international level, the working group could examine among other things, lessons learned from established bodies such as the Clean Development Mechanism and the Clean Technology Fund.

The sustainable investment support programme could address a range of subjects starting, for example, with transparency. Host countries could commit to making information easily available to foreign investors on practices directly bearing on incoming FDI, beginning with issues relating to the establishment of businesses, including existing limitations and incentives, investment opportunities, and project development. Governments could also provide an opportunity for comments from stakeholders when changing the regulatory framework affecting FDI, or when introducing new laws and regulations, while retaining ultimate decision-making power.

Transparency is also important regarding the support offered to outward investors by their home countries.These could commit – through a designated focal point – to making information available to their foreign investors on the measures they have in place both to support and restrict outgoing FDI. Supportive home country measures include information services, financial and fiscal incentives, and political risk insurance. Some of these measures are particularly important for small and medium sized enterprises (SMEs). Multinational enterprises, in turn, could make information available on their corporate social responsibility programmes and any instruments they observe in the area of international investment.

On the national institutional side, investment promotion agencies could be the focal points for matters related to a sustainable investment support programme, possibly interacting and coordinating with the national committees on trade facilitation to be established under the TFA. The function of such agencies in attracting sustainable FDI and increasing its benefits for the sustainable development of host countries could be recognised and undertaken within the framework of a country’s long-term development strategy. Investment promotion agencies could also play a role in the development of investment risk-minimising mechanisms needed to attract investment, or in the prevention and management of conflicts between investors and host countries. Regular interactions between host country authorities and foreign or domestic investors would help.

Finally, as in the Aid-for-Trade Initiative and the TFA, donor countries could provide assistance and support for capacity building to developing countries in the implementation of various elements of a sustainable investment support programme starting with an assessment of their needs and the identification of sources of international assistance. Support could focus on strengthening the capacity of investment promotion agencies as country focal points for the sustainable investment support programme.

Practical steps moving forward

There are several ways in which this idea could be moved forward. One option is to extend the Aid-for-Trade Initiative to cover investment as well, recognising the close interrelationship between investment and trade, and in tune with other trade international frameworks such as the WTO’s General Agreement on Trade in Services (GATS). Transactions falling under the latter’s Mode 3 – “commercial presence” – account for nearly two-thirds of the world’s FDI stock. The initial emphasis could be on investment in services and focus on key sectors for promoting sustainable development. Relevant initiatives, however, might require a broader interpretation of the current Aid-for-Trade mandate. This approach could also benefit from the OECD’s Creditor Reporting System that monitors where aid goes and what purpose it serves. The matter could equally be taken up by the Global Review on Aid-for-Trade, to examine its feasibility. Alternatively the current Aid-for-Trade Initiative could be complemented with a separate Aid-for-Investment Initiative but, given the tight interrelationships between trade and investment, this would be a second-best solution.

Another more ambitious and medium-term option is to expand the TFA to cover sustainable investment. This could be done through an interpretation or amending the Agreement as agreed by member states. A subsidiary body of the Committee on Trade Facilitation could provide the platform to consult on any matters related to the operation of what would effectively be a sustainable investment module within the Trade Facilitation Agreement. It is, however, as yet still uncertain when the required two-thirds majority of the WTO membership will have ratified the TFA or how the accompanying Trade Facilitation Agreement Facility will function in its quest to act as a financing facility to support developing countries unable to access funds from other agencies. Member states would also presumably wish to gather some experience with the operation of the TFA before expanding it.

A third, ambitious option might be for WTO members to launch a “Sustainable Investment Facilitation Understanding” focusing entirely on ways to encourage the flow of sustainable FDI to developing countries, inspired by and complementing the TFA, to be undertaken after the completion of the Doha Round. Work could equally begin in another international organisation with experience in international investment matters, for example in UNCTAD, the OECD, or the World Bank. A group of leading outward FDI countries could also launch such an initiative, for example, through the G20. The objectives of a support programme for sustainable investment facilitation can also be reached if its elements were to be incorporated in international investment agreements. Some of these agreements contain commitments by treaty partners to consult on the promotion of investment flows between them. But few contain binding commitments. Such approaches, while helpful, are nevertheless necessarily more piece-meal.

Meeting the future

The issues mentioned for possible inclusion in an international support programme for sustainable investment facilitation, as well as the options outlined on how such a programme could be put in place, are illustrative and all need to be seen against the background of the importance of economic FDI determinants. If these determinants are unfavourable, and investments are not commercially viable, even the best support programme is likely to have negligible effect. Concomitant productive capacity building is therefore critical. The key premise is the urgency of creating more favourable conditions for sustainable FDI flows to meet the investment needs of the future. As governments and the private sector increasingly share this view they will hopefully muster the political will and find the appropriate venue to put an international support programme for sustainable investment facilitation in place.

More details on the ideas outlined in this article can be found in a longer research piece published by the E15Initiative: An International Support Programme for Sustainable Investment Facilitation, July 2015. Implemented jointly by ICTSD and the World Economic Forum, the E15Initiative convenes world-class experts and institutions to generate strategic analysis and recommendations for government, business, and civil society geared towards strengthening the global trade and investment system.

Karl P. Sauvant is a Resident Senior Fellow, Columbia Center on Sustainable Investment (CCS). Sauvant is also the Theme Leader of the E15Initiative Expert Group on Investment Policy. Khalil Hamdani is a Visiting Professor, Lahore School of Economics, Pakistan.

This article is published under BioRes, Volume 9 - Number 7, by the ICTSD.

[1] Sauvant, Karl P. The International Investment Law and Policy Regime: Challenges and Options. E15Initiative. Geneva: International Centre for Trade and Sustainable Development (ICTSD) and World Economic Forum.

[2] Gordon, Kathryn, Pohl, Joachim and Bouchard, Marie. Investment Treaty Law, Sustainable Development and Responsible Business Conduct: A Fact-finding Survey. OECD. 2014.

Related News

AfDB unveils “New Deal for Energy in Africa”

A blue print to get rid of Africa’s energy poverty by 2025

The African Development Bank Group (AfDB) unveiled its landmark initiative to solve Africa’s huge energy deficit by 2025 at a High Level Stakeholder Consultative Meeting attended by business and political leaders at its headquarters in Abidjan on 17 September 2015.

The “New Deal for Energy in Africa,” which charts the way for a transformative partnership on energy focuses on mobilizing support and funding for the initiative from five key areas.

Firstly, the AfDB would significantly expand its support towards energy in Africa; development partners would also be obliged to scale up on-going efforts while countries must also expand their share of financing going into the energy sector and at the same time demonstrate stronger political will to ensure success of the Deal. Development partners would also be required to work together and coordinate their efforts to drive critical policy and regulatory reforms of the energy sector to improve incentives for accelerated investments.

“A lot of financing will be needed. Together, we must close the $55 billion financing gap for energy in sub-Saharan Africa. And we must raise our level of commitment to meet the $22 billion needed to support universal access to energy in the region,” AfDB President Akinwumi Adesina underscored in a speech unveiling the Deal.

Adesina also illustrated how domestic resource mobilization would play a crucial role by leveraging on just 10% of the continent’s tax revenues estimated at US$ 500 billion per year; how ending the over $60 billion annual illicit financial flows out of Africa can help; how developed countries meeting the 0.7% commitment for Gross National Income for development assistance which can generate more than $178 billion can also help to scale up energy development in Africa.

“The New Energy Deal for Africa will push for the establishment of a Bottom-of the Pyramid Energy Financing Facility for Africa. This should support some 700 million people to afford clean cooking energy stoves. The cost is well within our reach to provide, for it will take only $4.2 billion to solve the problem. We can and must solve their problem – and do so quickly,” the AfDB President said.

He called for the development of major regional energy projects such as the Inga dam in the Democratic Republic of Congo.

Quoting an African proverb, Adesina said Africa must go far and solve its energy challenge by 2025. He added: “And for that we must move together. This is why at the Bank we have proposed the formation of the Transformative Partnership on Energy in Africa. Under this, we will pull together to drive the needed reforms in Africa’s energy sector to achieve the universal access to energy by 2025. Success lies just ahead of us!”

Also speaking at the gathering, Nigerian Banker and Co-chair of the African Energy Leaders Group, Tony Elumelu, said that the private sector can play a crucial role in the development of Africa’s energy sector, if provided with the required enabling environment.

He said that given the situation in which some 600 million people lack energy in Africa, it would be necessary for Africa to explore all good sources of energy to meet the huge deficit, adding that the AfDB was in the best position to bring businesses, governments and international organisations together to make the deal a success.

For his part, former United Nations Secretary General, Kofi Annan, in a video message, commended the initiative, noting that Africa’s leaders had no choice but to urgently bridge the energy gap.

The Vice Prime Minister of the Democratic Republic of Congo, Thomas Luhaka and Cote D’Ivoire’s Prime Minister, Daniel Kablan Duncan commended AfDB President Adesina for putting together such as ambition initiative barely two weeks after his investiture. They pledged to mobilise the necessary political support required to ensure that Africa gets rid of its “energy poverty” by 2025.

» Speech by AfDB President Akinwumi A. Adesina at the High-level Consultative Stakeholder Meeting on the New Deal on Energy for Africa

Related News

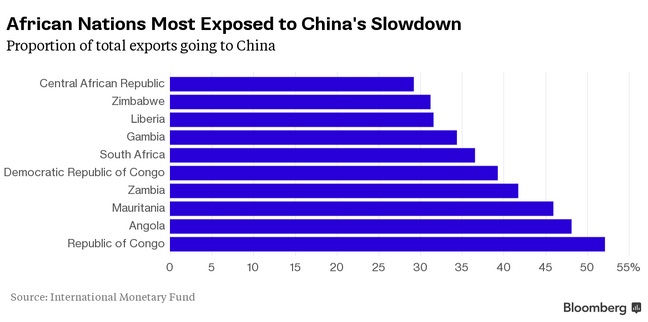

These are the African nations most exposed to China’s slump

China’s slowdown is rippling across Africa and these three nations are the most exposed, relying on demand from the Asian economy for almost half their exports: Republic of Congo, Angola and Mauritania.

Oil accounts for the bulk of Angola’s and Congo’s exports, damaging their prospects after crude prices plunged 55 percent since the beginning of June last year to below $50 a barrel. The price of iron ore, which makes up more than 40 percent of Mauritania’s exports, has dropped by almost a third in the past year. The three nations each shipped more than 45 percent of their exports in 2014 to China, data from the International Monetary Fund shows.

“For countries like Angola, which basically only has one commodity, there is a huge knock when prices fall and less oil is being exported to China,” Christie Viljoen, an economist at NKC African Economics, said by phone from Paarl, outside Cape Town. “It’s a case of when things are good, it’s really good, but when it turns bad, it’s really bad.”

Angola, Africa’s second-largest oil producer after Nigeria, has been forced to devalue its currency twice since June and has slashed its budget by a quarter following a slump in revenue. Congo’s fiscal deficit almost doubled to 8.5 percent of gross domestic product in 2014 from the previous year and in May Finance Minister Gilbert Ondongo cut $500 million of spending from the 2015 budget to bring it down to $4.5 billion.

Reliance on a single commodity and exposure to one country for the bulk of exports is a double-whammy. China’s slowdown means weaker currencies and higher import prices for these African nations, which in turn feeds into more pressure on their exchange rates and a run down of central bank reserves, said Viljoen.

Domino Effect

“If you are at the top of the list in terms of dependence on China and your economy is not well diversified, there are a bunch of negative things which can fall like dominoes,” he said.

Angola’s kwanza has dropped 24 percent against the dollar this year and was trading at 135.86 on the interbank market as of 6 p.m. on Thursday in Luanda, the capital.

While South Africa is the continent’s single biggest exporter to China – with shipments totaling $45 billion in 2014 – its exports are more diversified and destined to a wider range of countries. China buys 37 percent of South Africa’s goods, followed by the European Union at 20 percent.

Commodities such as gold, platinum and iron ore still make up the bulk of exports at just over half, though vehicle shipments have grown in importance to reach 13 percent of the total, according to data from the South African Revenue Service.

Related News

Exporters should look to sub-Sahara Africa

Angola is a case in point: in the five years to 2013, trade with Ireland was up 782%

The steady flow of migrants from Africa to Europe this year has painted a bleak picture of life on the continent.

However, a report to be published today by British bank Barclays outlines the significant potential that exists for Irish exporters in sub-Sahara Africa.

The Barclays Africa Trade Index, which measures the opportunity and openness of 31 of sub-Saharan economies, reveals that trade between Ireland and Africa grew by more than 43 per cent to about €1.44 billion over five years to the end of 2013. This was supported by Africa’s expanding middle class, associated spending power and demand for high-end goods.

South Africa remains the biggest market for Irish companies at €500 million, albeit that trade with the country has reduced in recent years.

Nigeria has closed the gap at the top, with trade reaching €450 million in 2013.

Kenya ranks third in the Barclays study for market openness and opportunity, although the level of trade is small at €36 million.

Rob Roughan, head of global corporates at Barclays Bank Ireland, said emerging markets in Africa should not be overlooked. “Major African economies such as South Africa, Kenya, Ghana and Nigeria have been the primary focus of Irish companies to date, but with increased competition, businesses need to diversify their trade and investment markets to broaden their horizons and compete more effectively.

“By 2020 the five ‘sleeping giant’ economies of Ethiopia, DR Congo, Mozambique, Ghana and Tanzania that we have identified in our index will represent a population of 325 million people, comparable with the US, and experiencing rates of economic growth that were once the preserve of India and China.

“Household spending for these countries is set to nearly double, so companies that establish themselves in these markets now will be positioned to reap the awards of rapid growth by 2020.”

Angola as a case in point. In the five years to 2013, trade with Ireland increased 782 per cent to €175 million.

What you waiting for?

UK-Africa trade corridor to be fuelled by Sub-Saharan ‘sleeping giants’

South Africa tops the inaugural Barclays Africa Trade Index: Openness and opportunity, followed by Nigeria and Kenya. Nigeria offers the greatest trade opportunity for UK businesses, largely due to its population of close to 180m, but Nigeria’s relative level of openness need to be addressed in order to challenge South Africa’s position.

The Index, which measures the opportunity and openness of 31 of sub-Saharan Africa’s leading economies, also identifies a group of ‘sleeping giants’ which, after experiencing significant economic upheaval, are playing catch up and growing at a rapid pace. The ‘sleeping giants’; Ethiopia, DR Congo, Mozambique, Ghana and Tanzania, are expected to provide UK businesses with the opportunity to increase exports three-fold, from US$1.2bn to $3.6bn, over the next five years as economic development continues and consumer spending increases.

With a combined population of around 270m, and average annual GDP growth of 7.3% over the past five years, these five countries represent a significant opportunity for UK exporters in the coming years.

The growth potential for the UK and other international producers across sub-Saharan Africa is considerable, with total consumer spending in the Sub-Saharan Africa economies reaching around US$1trn (£630bn) in 2014. It is expected to grow by a Compound Annual Growth Rate of around 4-5% over the next 5-10 years.

The Index reveals that 80% of UK exports to sub-Saharan Africa are currently going to South Africa together with Nigeria, Botswana, Angola, Kenya, Ghana and Senegal.

Over the past decade, sub-Saharan Africa has experienced a marked shift in trade flows from traditional partners in Europe, North America and the Middle East to faster growing Asian countries. The region received 19% of its imported goods from Asia in 2004 but this rose to 32% by 2013, largely driven by increased trade with China.

Commenting on the Index findings, John Winter, Chief Executive Officer, Corporate Banking, Barclays said: “Major African economies, such as South Africa, Nigeria and Kenya have been the primary focus of UK companies to date but with increased competition, especially from Asia, businesses need to diversify their trade and investment markets to broaden their horizons and compete more effectively.

He added, “By 2020, the five ‘sleeping giants’ that we have highlighted in our Report, will represent a population of circa 325m, comparable with the US and experiencing rates of economic growth that were once the preserve of India and China. Based on recent growth rates, household spending for these countries is set to nearly double, reaching over US$1,000 a year by 2020. Brands that start to establish themselves today will be well positioned for rapid growth by 2020.”

Regional Connectivity

Kenya is cementing its position as a key hub for East African trade and as a gateway to the wider sub-Saharan African market. Increasingly open borders, along with improving transport links, help the country to rank third in the overall Index. Neighbouring countries, including Tanzania (5th in the Index) and Ethiopia (6th), also benefit from strong regional co-operation and accessibility to key transport and communications infrastructure in the region.

To aid cross border movement, a number of countries have started to adopt one-stop border posts (OSBPs) – a single customs check run jointly by neighbouring countries. East Africa has been an early adopter with seven operational or in development OSBPs in Tanzania, six in Uganda and Kenya, five in Rwanda, and three in Burundi. This is supplemented by significant investment in road infrastructure, including the Ethiopia to Djibouti Corridor; the trade corridor running from the Tanzanian port of Dar es Salaam and the Nacala corridor linking the DR Congo, Zambia and Malawi to the port of Nacala in Mozambique.

Historically, air connections across Africa have been extremely patchy, evident in the air transport sub-categories of the Index. Only six countries* score above 5 on a scale of 1 (weak) to 10 (strong) in terms of international air connectivity and seven countries** score above 5 on regional air connectivity. However, a growing number of connections are transforming the air connectivity of key markets. Ethiopia, for example, now has links to 33 African destinations and Kenya has 35, both well ahead of South Africa’s 26.

Commenting on the state of regional integration across sub-Saharan Africa, Alan Winters, Professor of Economics at the University of Sussex explains: “Regional integration only makes sense up to a point. The important thing is the size of the market; ten years ago the sum total of the sub-Saharan African economies, other than South Africa, was equivalent in GDP terms to Belgium. If Africa develops into a very dynamic market, as it may well do, everyone will want to have a part of it.”

John Winter concludes: “Sub-Saharan Africa has become a much more open and attractive opportunity for international trade and investment over the past decade, reflected by a sharp increase in trade and investment flows across the region. There are significant opportunities for UK business, although it is essential that UK firms continue to tailor their products and services to the diverse range of local needs, establish strong working relationships with local partners and align business plans with local development and integration objectives.”

* South Africa, Ethiopia, Mauritius, Kenya, Angola and Nigeria

** Kenya, Ethiopia, South Africa, Tanzania, Nigeria, Cote d’Ivoire and Senegal

About the Barclays Africa Trade Index

The Barclays Africa Trade Index compares and ranks 31 Sub-Saharan African countries based on their attractiveness for cross-border trade. The countries are the largest in the region in terms of GDP and population. The index is designed to help existing and potential importers understand both the opportunities and challenges to trading in the region.

It comprises 41 individual indicators grouped into two major categories – Opportunity and Openness – and divided between six focused categories: Demographics, Market size & Growth, Trade & Investment Flows, Tariff Policy, Border Administration and Transport & Communications.

The categories are designed to be comparable and were formed through a bespoke scoring method to convert raw data – such as FDI flows into a comparable score of 1-10. Indicators in the “Opportunity” category were scored relative to the best-in-class, resulting in larger markets such as Nigeria and South Africa scoring highly. In the “Openness” category, countries were scored relative to an idealised target – such as 100% participation rates for mobile telecoms or a 0% tariff policy, in this way smaller countries such as the Mauritius scored highly – showing their relative openness to trade. The two categories were then combined to produce an overall score out of 100.

Related News

Countries urged to submit climate action plans ahead of UN conference in Paris

Secretary-General Ban Ki-moon is eager to get countries to submit as soon as possible their action plans that will form the basis of the new universal climate change agreement to be adopted in December in Paris, a senior United Nations official dealing with the issue said.

Janos Pasztor, Assistant Secretary-General on Climate Change, told a press conference at United Nations Headquarters that, to date, 62 out of 194 parties to the UN Framework Convention on Climate Change (UNFCCC) have submitted their Intended Nationally Determined Contribution (INDC).

The Secretary-General is “eager” to get all countries to submit their climate action plans, Mr. Pasztor said, adding “the earlier we get them the better.”

According to the UNFCCC, the Paris agreement will come into effect in 2020, empowering all countries to act to prevent average global temperatures rising above 2 degrees Celsius and to reap the many opportunities that arise from a necessary global transformation to clean and sustainable development.

Mr. Pasztor described as “remarkable” the submissions that have been put forward so far, drawing attention to the fact the plans are based on what countries are prepared to do in response to climate change. Countries have agreed that there will be no back-tracking in these national climate plans, meaning that the level of ambition to reduce emissions will increase over time.

He added that the Secretary-General hopes the visit to the UN by Pope Francis during next week’s General Assembly session devoted to adopting a new global development agenda will bolster support for action on climate change.

The UN expects 154 Heads of State or Government and 30 ministers for the Sustainable Development Summit, which will be held from 25 to 27 September.

On Wednesday, Mr. Ban voiced his concerns at a press conference that not enough is being done to keep temperature rise under the 2-degree Celsius threshold and urged world leaders “to raise ambition – and then match ambition with action.”

Against the backdrop of unprecedented population movements confronting the world today and in response to a question about whether climate change was a cause that forced people to be on the move, Mr. Pasztor said that there is “increasing evidence” that climate change is a factor.

“Climate change is a threat multiplier,” he said, adding that if there are already conditions that are prompting people to be on the move, the effects of climate change are making them worse.

“The facts are clear on the ground,” said Mr. Pasztor.

He also noted that there is “no silver bullet in reducing emissions,” and advocated for investing in substantive research for new technologies in the long-term battle against climate change.

“We are in this game for a long time,” he said.

Regional Dialogue on Transport Industry kicks-off

Stakeholders in the transport and logistics service industry converged in Nairobi for a two-day regional dialogue on the economic and competitiveness challenges facing the sector in the region.

The dialogue which was opened by Principal Secretary in the Ministry of Transport and Infrastructure, Kenya, Eng. John Mosonik was organized by the COMESA Business Council (CBC) and brought together transporters, shippers, port authorities, freight forwarders, customs and clearing agencies among others.

COMESA Secretary General Mr Sindiso Ngwenya told the delegates that some stubborn issues existed in the transport sector which have slowed the deepening of regional integration and made it difficult for goods to flow easily across the region.

“There is limited awareness on customs and trade facilitation instruments, vehicle overload controls at weigh bridges and different load systems that are applied in the regional states,” Mr Ngwenya said.

He cited other handicaps as customs interconnectivity issues which resulted in intermittent network and electronic system downtimes, slow speed of systems, multiple documentation and process requirements and port inefficiencies.

To address these challenges, he said COMESA had developed various trade facilitation instruments that include the COMESA Yellow Card which is a third party motor vehicle insurance scheme, the Regional Customs Bond to replace the multiple national bonds required in each country of transit, the Carrier License, Harmonized Axle Loads and the Virtual Trade Facilitation System.

These instruments, Mr Ngwenya said are aimed at ensuring reduction of time loss across borders, efficiency in auto-tracking of cargo, revenue collection and opportunities for corruption along the corridors.

“Transport and logistics lie at the center of trade and regional integration. It is when imports and exports can reach their destination without delay at the most affordable cost that the competitiveness of industries increases at both global and regional level,” Mr. Ngwenya said.

He described the dialogue as an opportunity to provide solutions to the long standing challenges associated with transport, logistics and the movement of cargo in the region and Africa as a whole.

In his address, Eng Mosonik outlined the investments that the Kenya government had made in development of transport infrastructure given the country’s strategic location as a getaway to other parts of the region.

These include the construction of the second container terminal at the Port of Mombasa whose first phase is expected to be completed by 2016. Others are the standard gauge railway linking the port to the hinterland economies of eastern and central Africa and a state of the art Greenfield terminal at the Jomo Kenyatta International Airport with capacity to handle 12.5 million passengers.

The Chairperson of the COMESA Business Council Dr Amany Asfour called for continuous dialogue, engagement and consultation between the private sector and governments to resolve the challenges in the transport and logistics sector.

Related News

tralac’s Daily News selection: 17 September 2015

The selection: Thursday, 17 September

Evolving banking trends in Sub-Saharan Africa: key features and challenges (IMF)

This paper discusses key stylized facts and trends of banking development in SSA, looking at a variety of dimensions such as size, depth, soundness, and efficiency. It also assess the rapid expansion of pan-African banking groups, which have overtaken the role of the European and U.S. banks that had traditionally dominated banking activities in SSA, creating significant cross-border networks and becoming the largest participants in new syndicates and large bilateral loans to finance infrastructure development. [Download]

New Unified Insolvency Act can help African SMEs improve access to finance (World Bank)

With support from the World Bank Group, 17 African countries, members of the Organization for the Harmonization of Business Law in Africa, adopted a Unified Insolvency Act last week in Côte d’Ivoire. This new law replaces the previous 1998 law which was widely believed to be lacking key features of a modern insolvency regime, particularly as regards reorganization proceedings and the treatment of creditors.

IFC in Africa: Year in Review, Fiscal 2015

SADC food and livelihoods insecurity: VAC 2015 results (Humanitarian Response)

The SADC summary of the 2015/16 regional food security and vulnerability situation based on the results of the 2015 NVACs vulnerability assessments: given the hazards faced, the number of food insecure people in the countries providing data increased by 13% (13.4 million this year compared to 10.3 million for last year) which was an above average year. The exceptions were Mozambique and Swaziland where numbers continued to decrease. In comparison to last year major increases in food insecure population are noted in Malawi, Namibia, Zambia and Zimbabwe. [Download]

South Africa: Agricultural Policy Action Plan (Agbiz)

Extract (Trade, agribusiness development and support): On the international front, the changing global environment and increasing standards on food safety excludes smaller farmers to play a critical role in international market access. Over and above this is the cost to access foreign markets. Stringent sanitary and phyto-sanitary, private standards, labelling and other technical requirements have gone beyond compliance capacity of many smallholders. Lack of market access could constraint growth and the targeted jobs that the sector intend to create. Strategic interventions are required to integrate smallholder and struggling smaller commercial farms to participate in the mainstream economy and take advantage of both domestic agro-food chains and international markets. [Download]

South Africa promotes expensive wines to boost exports (Bloomberg)

US, South Africa find common ground in bid to resolve poultry row (Bridges/ICTSD)

Kenya unveils blueprint to revive industrial and manufacturing sector (KBC)

The decade-long plan, aptly christened Kenya’s Industrial Transformation Programme (KITP), looks beyond import-substitution and export-led policy regime to develop its industries, stimulating Kenya’s ambitions as Africa’s next industrial power. Anchored on a five-point strategy, prioritizing leveraging Kenya’s comparative advantages, the plan aims at growing the manufacturing sector to levels above 15% of GDP from a static 11% over the past decade. According to Cabinet Secretary Industrialization and Enterprise Development Adan Mohamed, Kenya has identified 10 opportunities within the key strategies that will increase manufacturing sector jobs to 435,000 additional jobs in the next 5 years (+150% compared to today) and add Kshs. 200-300billion to the GDP.

Extract (Agro-processing): More than half of Kenya’s exports are related to agriculture, including tea, horticulture (i.e., cut flowers, fruits and vegetables) and coffee. We will continue to increase these exports and have identified additional opportunities in agro-processing that build on our vast agricultural potential. ƒ Tea is a staple of Kenya’s exports, worth USD 1 billion annually. However, 97% of tea is exported in bulk form. Kenya can attract a 50 to 100% price premium by promoting “Made in Kenya” brands internationally, attracting USD 200 million in value addition, and create 10,000 jobs.ƒ

Only 16% of all exported agricultural output in Kenya is processed; the rest is exported in raw form. By contrast, Tanzania processes 27%, Uganda 34% and Ivory Coast 32%. We can double the amount of our processed agricultural exports to boost agriculture, create an additional 110,000 jobs and earn USD 600 million. Eastern Africa annually imports USD 3.8 billion in raw and processed commodities such as wheat, palm oil and rice for local consumption. The majority of these imports come from outside of the region. We can take advantage of the strategic location of the Port of Mombasa into our priority sectors to set up a “food hub” where we import raw commodities in bulk and process and export consumer goods to serve the growing regional market. This could earn Kenya an additional USD 300 million in GDP and create 60,000 jobs. [Download]

Poorly managed concessioning of the container terminal could harm port (Daily Nation)

Prominent Nairobi lawyer Fred Ngatia has moved to the High Court to demand that tender evaluation documents relating to the controversial privatisation of Mombasa’s newly-built second container terminal be made public. The battle for the lucrative contract is surely going to be a cause célèbre. Indications are that we could end up with a protracted court tussle likely to drag on for a long time. With the new container terminal, Mombasa will be able to reposition itself as the reference port of the Indian Ocean and consolidate its leadership over Djibouti, Dar es Salaam, and Maputo. We should, therefore, select the very best to run it. [The author: Jaindi Kisero]

Two new papers, by Isabelle Ramdoo, on extractive sector policy issues: Resource-based industrialisation in Africa: optimising linkages and value chains in the extractives sector (ecdpm), Unpacking local content requirements in the extractive sector: what implications for the global trade and investment frameworks? (E15 Initiative)

Malawi extractive sector update: Mines Bill to be tabled in October parliament sitting (Mining in Malawi)

One foot on the ground, one foot in the air: Ethiopia’s delivery on an ambitious development agenda (Development Progress)

This case study looks at the progress achieved in material well-being, education and employment, where Ethiopia has shown particularly strong performance over the past 10 to 15 years. However this transformation is far from complete and a number of challenges remain, not least the depth and breadth of chronic poverty. A number of key lessons for the Sustainable Development Goals can be drawn from Ethiopia's experience:

South Africa: Constitution protects foreign investors’ rights (Business Day)

The Department of Trade and Industry defended its Promotion and Protection Investment Bill on Wednesday despite a slew of submissions claiming the bill was investor unfriendly. In his response to the submissions, Department of Trade and Industry director-general Lionel October said SA had an ambitious development agenda, which required new policies and regulations while ensuring it remained open to foreign investment. "SA is the favourite destination for foreign direct investment in Africa by a long way and we want to put to rest the notion that there is less protection under the bill," Mr October said.

South African businesses hoard cash in indictment of economy (Bloomberg)

Tanzania: State promises investor-friendly climate (Daily News)

Trade Hub hosts SADC TIFI thematic group cluster meeting

MTN warns against removing African tax incentive (Business Day)

Republic of Congo: 2015 Article IV Consultation (IMF)

The Republic of Congo has been hit hard by the oil price shock. Fiscal and current account balances deteriorated in 2014 reflecting increased government spending and lower oil prices. Corrective measures are now being taken. Private sector activity is held back by infrastructure gaps, a difficult business climate, and a shallow financial system. Growth and spending have yet to translate into significant reductions in poverty and progress in this area lags peers. Persistent inequality could be a source of instability.

Africa without limits (Times Live)

City bosses across Africa want national governments to ban visa requirements and allow people to move freely between the various countries. Jean-Pierre Elong Mbassi, secretary-general of the United Cities and Local Governments of Africa, said the time for keeping colonial borders had lapsed. Speaking in Sandton yesterday, Mbassi said Africa had to facilitate the movement of people to realise development and intra-continental trade it so desperately needed.

Mozambique updates: Funding development in the districts (SPEED Program), Government wants alternative north south road (Club of Mozambique), Metical devaluates almost 40% against the dollar (Club of Mozambique)

'India, Africa looking at deeper political, economic engagement' (SME Times)

Navtej Sarna, Secretary (West) in the Ministry of External Affairs, also said that India and Africa have a "collaborative partnership", which distinguishes it from the ties between Africa and other nations. Addressing the inaugural session of'National Consultation on India-Africa Partnership: Priorities and Prospects', Sarna said that India and Africa are looking at "a very tangible political and economic engagement, which keeps in view several facts", including that together both comprise one-third of the world population. He said India is only seven years old in its partnership with Africa in the IAFS format, which began in 2008, while Japan, the EU and China have two decades old partnership with the continent.

Mapping the world’s winners and losers from China trade (Foreign Policy)

UNU-WIDER 30th Anniversary conference started today: 'Mapping the future of development economics'

The growth-employment-poverty nexus in Latin America in the 2000s: Brazil country study (UNU-WIDER)

AU gets $70m to fight insurgencies (ThisDay)

C20: new civil society policy paper on tax justice (Tax Justice Network)

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome. Richard Humphries (Email: This email address is being protected from spambots. You need JavaScript enabled to view it.; Twitter: @richardhumphri1)

Related News

South Africa publishes Agricultural Policy Action Plan (APAP) 2015-2019

Agriculture, forestry and fisheries (AFF) are widely recognised as sectors with significant job creation potential and with strategic links to beneficiation opportunities. However, although between 1994 and 2012 the real contribution of AFF to GDP increased by 29%, over the same period employment declined in both primary production and agro-processing by about 30% to 40%. This combination of slow-to-modest growth and declining employment, continues a longer-term trend evident since at least the 1970s.

The challenges facing AFF are numerous: rising input costs, an uneven international trade environment, lack of developmental infrastructure (rail, harbour, electricity), and a rapidly evolving policy and production environment. At the same time, transformation of the AFF sectors has been slow and tentative.

While there have been a variety of sector strategies established in the past, and while some progress has been made, there is recognition of a need to sharpen our analysis of what accounts for sluggish growth and job losses in AFF, and what is required to reverse this trend. At the same time, it is recognised that while the Agriculture, forestry and fisheries sectors play various strategic roles in respect of food security, agrarian transformation and rural development, and in supporting industrial development, it is also the case that AFF is under-funded: according to National Treasury’s estimates of consolidated government budgets and expenditure (‘functional classification’), the share of public money going to agriculture, forestry and fisheries has been at around 1,7% over the past four years, and is expected to decline to 1,6% over the next two. The OECD recognises South Africa’s agriculture sector as among the least supported in the world: South Africa’s Producer Support Estimate is currently 3,2%, versus 4,6% for Brazil, 7,1% for the US, and 18,6% for the OECD. Of particular concern is the lack of attention to R&D: according to the 2009/10 R&D survey conducted by HSRC on behalf of the Department of Science and Technology (the most recent survey for which the results are available), agriculture accounted for only 6,9% of South Africa’s total R&D spend. This state of affairs can in part be explained by the absence of a compelling, widely-supported strategy and implementation plan.

A detailed analysis of the various challenges is given in the Integrated Growth and Development Policy for Agriculture, Forestry and Fisheries, or ‘IGDP’. Based on this analysis, the IGDP also outlines appropriate responses. The Agricultural Policy Action Plan (APAP) seeks to translate the high-level responses offered in the IGDP into tangible, concrete steps. However, this first iteration of APAP is not offered as a fully comprehensive plan; rather, based on the model of the Industrial Policy Action Plan (‘IPAP’), it identifies an ambitious but manageable number of focused actions, in anticipation of future APAP iterations that will take the process further. APAP is planned over a five-year period and will be updated on an annual basis. Aligning itself with the New Growth Path (NGP), the National Development Plan (NDP) and Industrial Policy Action Plan (IPAP), APAP seeks to assist in the achievement of Outcome 4, Decent Employment through Inclusive Growth, and that of Outcome 7, Comprehensive Rural Development and Food Security.

APAP proposes a number of transversal interventions that complement but also go beyond the specific sectoral interventions identified. Altogether seven transversal interventions – or ‘Key Action Programmes’ (‘KAPs’) – are included, which collectively seek to strengthen the agriculture, forestry and fisheries sectors in diverse ways. One of these is Trade, agribusiness development and support.

Trade, agribusiness development and support

Problem statement

South Africa’s agro-food market landscape has changed in line with changes occurring internationally as a result of globalisation and market reforms. As a result agricultural production portfolio is diversifying and moving towards producing high value products (i.e. fruits, vegetables & animal products) in response to the changing tastes and preferences of the consumer. These changes present opportunities as well as challenges for agriculture in South Africa.

Although consolidation of the market is evident since the 1950s, market liberalisation reforms undertaken by government in the mid-1990s, fast tracked the process in which agriculture grew to the exclusion of the smaller commercial sector, and smallholder producers. Globalised market structures, further characterised by amongst others long chains of transactions between the producers and consumers, poor access to appropriate and timely information, led to many struggling smaller commercial business in the sector, let alone smallholder, being bought out by bigger corporates.

The lack of access to markets both domestic and international has been identified as one of the constraints faced by small-scale operators in the agriculture, forestry and fisheries sectors. Firstly, the entry of large retail supermarket chains into smaller rural towns has largely replaced the role of small-scale farmers as local food producers. Secondly, the procurement requirements of many supermarket chains and agribusinesses are too heavy for the smallholder to comply because of the numerous standards such as food quality and safety. Their access to the market is further constrained by factors such as low volume (with small marketable surplus), poor quality, erratic suppliers, etc. As a result, smallholder farmers cannot benefit from market access opportunities offered by these agro-food chains.

On the international front, the changing global environment and increasing standards on food safety excludes smaller farmers to play a critical role in international market access. Over and above this is the cost to access foreign markets. Stringent sanitary and phytosanitary, private standards, labelling and other technical requirements have gone beyond compliance capacity of many smallholders. Lack of market access could constraint growth and the targeted jobs that the sector intend to create.

Strategic interventions are required to integrate smallholder and struggling smaller commercial farms to participate in the mainstream economy and take advantage of both domestic agro-food chains and international markets.

Aspiration

- To increase market access for agriculture, forestry and fisheries products both domestically and internationally through targeted/product specific interventions. The priority should be given to smallholder farmers through research, capacity building and technical assistance.

Policy levers

- Agriculture, Forestry and Fisheries Trade and Agro-processing strategy

Nature of the intervention

The interventions in this area should be tailored to address both trade and market access opportunities for SMMEs including smallholder farmers. Evidence has shown that smallholder farmers do participate and make a sizeable contribution to the production of high value food commodities, but their links to markets are not strong. DAFF has various programmes to support smallholder farmers, however, some of these interventions have a narrow focus on production with very little or no support directed to activities of market access. On the domestic front, government support and intervention should focus on the creation of smallholder commodity associations, marketing cooperatives, enhance programmes supporting market access information and build on existing production systems and support sectors in which smallholder farmers are involved. Development efforts to resuscitate the smallholder farmer should also be linked with improvements in food safety and development of national food standards and regulations. This could stimulate the smallholder to continue earning income and creating jobs.

Regarding access to international markets, exports orientated programs must be integrated at early stage of production. The specific intervention by government will be to embark to directly assist smallholders by providing training and technological upgrade (in terms of standards for production, quality, packaging and delivery). This will enable smallholder farmers to meet export market requirements. Other interventions in these areas should focus on business networking events, including trade shows, business to business and direct buyer’s engagements. The trade strategy developed by DAFF should further guide the integration of smallholder farmers into global markets.

Related News

Kenya unveils blueprint to revive industrial and manufacturing sector

Kenya has unveiled its first-ever blueprint to revive its manufacturing and industrial exports sector.

The decade-long plan, aptly christened Kenya’s Industrial Transformation Programme (KITP), looks beyond import-substitution and export-led policy regime to develop its industries, stimulating Kenya’s ambitions as Africa’s next industrial power.

Anchored on a five-point strategy, prioritizing leveraging Kenya’s comparative advantages, the plan aims at growing the manufacturing sector to levels above 15% of Gross Domestic Product (GDP) from a static 11% over the past decade.

According to Cabinet Secretary Industrialization and Enterprise Development Adan Mohamed, Kenya has identified 10 opportunities within the key strategies that will increase manufacturing sector jobs to 435,000 additional jobs in the next 5 years (+150% compared to today) and add Kshs. 200-300billion to the GDP.

“As an emerging economy, moving from agriculture based, low income economy to an industrial, middle income economy, it is paramount that the manufacturing share to GDP increases,” said Mohamed.

Under the plan, Kenya will build and innovate on its export engines and continue to support them. “To boost production and exports, Kenya will work to ease regulations on the sale of the exports while looking to attract a 50-100% price premium by marketing tea and coffee as a ‘Made in Kenya’ brand internationally,” said the Cabinet Secretary.

“We also plan to offer incentives for local value addition for multinational companies to consider creating opportunities for SME’s by investing in group packaging,” said the Cabinet Secretary, adding these efforts will attract Kshs 20-24 billion (USD 200-240 million) in value addition and 10,000 jobs.

Kenya is also eyeing on capitalizing on agro-processing’s global market worth Kshs.1,47 trillion (USD 14.7billion), which Mohamed said the Government “is working on attracting investors to develop three to five large integrated value chain ‘Agropolis’ projects with potential to yield Kshs.30 billion (USD 300 million) in GDP and create up to 60,000 jobs.”

Under the plan, Mohamed said the government plans to enforce the ‘Buy Kenyan, Build Kenya’ policy to nip Kenya’s huge Kshs. 82 billion textile and apparel import bill.

Painting a rosy picture of the industry, buoyed by the AGOA extension for another decade, he said Kenya is keen to grow its share of US market from the 0.4%, increasing AGOA exports to Kshs.100 billion in the next 3 years.

“We will be expanding to new geographical markets in textiles and apparel growth, and building an industrial park with a textile cluster in Naivasha to take advantage of natural power sources. Such will help us manufacture enough textiles and apparels to increase our 0.4% pie in the USD 84billion US textiles market,” said Mohamed.

He cited ongoing efforts to build a leather city in Machakos and upgrading the Kariokor leather cluster as key to netting USD 150 to 200 million in GDP and 35,000 to 50,000 new jobs.

Other efforts will include marketing Kenya leather products abroad and securing international sourcing contracts for leather products.

Mohamed said the blueprint commits to work build on capacity of local firms to profit from Kenya’s infrastructure and investments boom. Infrastructure, Residential and Commercial Construction and oil and gas and mining services have witnessed a massive boom with local firms missing out due to scale and expertise.

“Despite the healthy contribution to GDP and employment, only 8% of the 6 trillion regional infrastructure construction market is served by domestic firms. The Government has legislated local content rules such that projects worth Kshs 1 billion are awarded to domestic companies,” said Mohamed.

According to KAM Chief Executive Phyllis Wakiaga, building capacity of Kenya’s local construction companies could yield Kshs.10-20 billion in GDP and create 30,000 jobs from the bludgeoning industry.

“Kenya stands to make 35% of estimated 100 billion mining value at stake annually. The Eastern African Oil and Gas Services market could grow rapidly at around 26% over the next few years to reach USD 3.5 billion by 2020,” said KEPSA’s CEO, Carole Kariuki.

“The National Single Electronic Window System (NSEWS) together with the other administrative reforms will reduce the time taken to comply with payment of taxes, levies, duties and fees as well as facilitate cross border trade across the EAC region. The Single Window System is expected to double East African trade to $33.3 billion by 2016, and enhance transport along the Northern Corridor from the port of Mombasa to Uganda, Rwanda and Burundi,” said Ms. Kariuki.

Also set to be improved are the non-industrial job creating sectors – Information Technology related sectors, Tourism and Wholesale and Retail. The last decade saw a liberalized economic wave driven by a thriving domestic service sector. In the period, telecommunications, wholesale and retail and hotels and restaurants have grown by 12.2%, 8.8% and 7.7% respectively.

“Kenya is keen to develop into an IT service export hub within Africa and a preferred location for business process and IT outsourcing. In tourism, we are positioning our resources to muscle into the Ksh 320 billion conferencing tourism market in Africa,” said Mohamed.

According to KAM CEO, Phyllis Wakiaga the plans commitment to build an enterprise culture with an SME pilot programme dubbed ‘Rising Stars’ Programme is a good step towards supporting SME’s growth.

Further, Mohammed said the government will focus on creating an enabling environment as Kenya seeks to transition to higher-value added manufacturing sectors. With Ease of Doing Business Reforms Agenda in top gear, with new bills signed by H.E the President last week, the stage is set for unprecedented investments. The government will focus on upgrading investment targeting strategies to attract local capital and foreign direct investment.

“We will also create a fund that will allow the Ministry or its agencies to offer attractive co-investment packages to local or foreign investors when they are needed and to support other critical activities in the industrialization programme,” said Mohamed.

Further, industrial parks along major infrastructure corridors including the SGR and LAPSSET Corridor will be created.

Related News

US, South Africa find common ground in bid to resolve poultry row

The US and South Africa have reportedly made progress on the technical health and sanitary discussions related to the imports of poultry, pork, and beef meat from the United States, following a strategic dialogue held this week.

This development comes after growing frustrations from Washington over the alleged lack of implementation of the Paris agreement reached in June, which was meant to pave the way for the re-entry of US chicken imports to the South African market.

Since 2000, imports of certain US chicken products into South Africa had been subject to anti-dumping duties of above 100 percent, which US poultry meat exporters deemed unfair. Under the Paris agreement, South Africa committed to end import duties on US chicken and resume imports, initially at levels of 65,000 tonnes a year.

A separate set of actions was then envisaged in order to resolve the remaining sanitary issues related to poultry, pork, and beef after South Africa raised concerns over an avian influenza outbreak – an infectious viral disease of birds which can sometimes spread to poultry – in 15 US states. This led the former to delay the effective implementation of the agreement.

A policy of “regionalisation”

The South African government welcomed the agreement by US and South African veterinary experts on the meat import issues as a breakthrough, according to the Citizen, an online news platform. On poultry, experts settled on a protocol and health certification allowing for the import of poultry from areas in the US that are not affected by the virus.

A statement issued on Tuesday by South Africa’s Ministry of Trade and Industry confirmed that the two sides aim to finalise the terms and conditions for poultry export certificates by 15 October in order to resume shipments from the US by year’s end.

In a letter addressed to South African President Jacob Zuma last week, US senators Johnny Isakson and Chris Coon requested that Pretoria follow the World Organization for Animal Health (OIE) guidelines and implement a “policy of regionalisation for pathogenic avian influenza,” along with adopting language for export certificates. They specified that without these issues being addressed and in place, US companies would not be in a position to ship any product, regardless of the terms of the Paris agreement.

According to commentators, the common understanding found this week appears to address this issue of “regionalisation,” as South Africa agreed to only to ban poultry imports from specific areas of the US affected by the virus.

Isakson is a Republican from Georgia while Coons is a Democrat from Delaware, both major poultry producing US states. The two senators are also the co-chairmen of the US Senate Chicken Caucus and are members of the Senate Foreign Relations Committee, and have been pressuring the Obama Administration over the past year to block the renewal of the South Africa’s participation in the African Growth and Opportunity Act (AGOA) unless market access for American poultry exports was increased.

The lifting of similar health-related restrictions on US beef and pork were also discussed during this week’s meeting. Both parties reportedly discussed possible South African exports of animal products to the US and exchanged information on the technical requirements to access American markets, reports the Citizen.

One source consulted on this issue indicated that a common ground might have been reached on pork and beef restrictions, but cautioned however that there were still additional issues to be dealt with before a full-fledged solution can be confirmed.

South Africa under pressure

“We look forward to successful implementation of the Paris agreement so the United States and South Africa can at last leave this trade dispute behind,” read the letter co-signed by the US senators to South African President Zuma.

The letter describes two processes that need to be completed by South Africa in order to make the Paris agreement effective. These include the creation of a rebate facility to legally exempt the annual quota amount from anti-dumping duties and the development of rules for allocation and administration of the quota through a transparent legal process.

“We are also disappointed to learn that there has been no progress in addressing South Africa's complete ban on US poultry due to avian influenza,” reads the letter.

The letter also makes specific reference to the review of South Africa’s eligibility under the new version of the African Growth and Opportunity Act (AGOA). In the context of such review, if the US President determines that South Africa does not meet certain requirements, the latter’s eligibility could either be withdrawn, suspended, or limited.

This summer, the US Congress passed legislation to extend duty-free access to the American market for eligible sub-Saharan African countries for another decade through AGOA.

“Congress has made clear that the United States should not allow other countries to enjoy trade benefits under AGOA while actively undermining our trading interests,” said Coons.

At stake are South Africa exports to the US of motor vehicles and citrus valued at US$1.3 billion and US$41 million, respectively.

Related News

IFC expands support for infrastructure, entrepreneurs, and fragile states in Africa in 2015

IFC, a member of the World Bank Group, on 15 September announced that it committed $3.6 billion in new long-term financing and mobilizations in Sub-Saharan Africa during its 2015 fiscal year. IFC’s strategy in Africa aims to help bridge the region’s infrastructure gap, build productive industries, and lead inclusive business approaches through financing for private companies and advice to the private sector and governments. The 2015 financing figure compares with $3.0 billion committed in the previous year.*

Oumar Seydi, IFC Director for Eastern and Southern Africa, said, “IFC’s expanding investments in Africa in 2015 are a reflection of the investment opportunities and our ability to target key sectors critical for African development. IFC supports projects that help nurture entrepreneurs and small businesses and reach projects in Sub-Saharan Africa’s critical sectors, including infrastructure and agribusiness.”

Private sector projects expanding infrastructure through power, transport, and utilities received $1.1 billion in new financing from IFC this fiscal year. Four new public-private partnership mandates were signed, which will help improve healthcare in Mozambique and boost power generation in Ghana, Tanzania and the Democratic Republic of Congo. IFC provided wide-ranging advice to governments and private investors in projects across 30 countries.

IFC committed $246 million in Sub-Saharan Africa’s fragile and conflict affected situations, supporting projects in finance, mining, infrastructure, and smaller businesses. That included more than $80 million in new investment commitments to companies and financial institutions in Guinea, Liberia and Sierra Leone as part of a $450 million, three-year target to step up new investments that respond to Ebola and support economic recovery in countries worst-affected by the epidemic.

IFC invested $1.2 billion, including capital mobilized from partners, in the financial sector in Africa. IFC’s investments in banks and financial institutions helped provide loans to entrepreneurs. Meanwhile, IFC provided more than $500 million to encourage key industries, including agribusiness and healthcare.