Search News Results

Africa CEO Forum 2014: African Business leaders gather in Geneva

The AFRICA CEO FORUM 2014, one of the most important gathering of African business leaders taking place in Geneva from 17 to 19 March, has been officially opened.

Organised by Groupe Jeune Afrique in partnership with the African Development Bank(ADB), the second AFRICA CEO FORUM welcomed “680 participants, speakers and journalists from more than 38 countries”.

This level of participation is already a measure of the success of this year’s AFRICA CEO FORUM, whose mission is to bring together economic actors from French and English speaking Africa to strengthen regional ties, promote public-private sector dialogue with the goal of building an environment conducive to new business development. It further stimulates African entrepreneurship, innovation and creativity.

The opening ceremony, chaired by Donald Kaberuka, president of the African Development Bank and Amir Ben Yahmed, Managing Director of the Groupe Jeune Afrique and Chair of the AFRICA CEO FORUM, recalled the primary purpose of this major event.

“The year 2013 was marked by a new 16% progress of foreign direct investments. The IMF is forecasting a global growth of 6.5% for 2014. I have lost count of the number of Africa CEOs who are now part of the international rankings of the economic press.

However, we cannot ignore the fact that most of the emerging countries which were considered only a few months ago as the engines of the world economy are today transforming into weak links. So when we elaborated the programme of this second edition of the AFRICA CEO FORUM we intended to take hindsight and reflect together on the ways of accelerating the transformation of our continent”, recalled Amir Ben Yahmed.

A first day of rich an substantive discussions

The first day of the AFRICA CEO FORUM, comprising one plenary session and two knowledge sessions devoted to key topics such as the competitiveness of African companies and the issue of local transformation of the continent’s natural resources, was enriched by the contributions of several high-profile speakers from Africa and the rest of the world.

For Moulay Hafid ELALAMY, Minister of Industry, Trade, Investment and Digital Economy: “We have a current competitiveness and it will persist only if Africa continues to wake up”

“This issue of competitiveness is critical if we want to continue and attract foreign investments and develop human capital, promote employment and thus, further develop this middle class and the local market implied for the CEOs” noted Amir Ben Yahmed.

“When there is discussion around the African economy, there are so many different views. The reality is that they all reflect a certain reality. One thing is certain though, and on this there is a broad consensus. People agree on the imperative of Africa moving up the regional and global value chains, and providing all the services associated with that… We are here to figure out how to take Africa to the next stage. From ‘hopeless’, to ‘rising’, to ‘hopeful’. The African Development Bank is proud to be your partner in this journey. Together we will take Africa to the next level”, added Donald Kaberuka.

Thanks to its rich and substantive programme, composed of high-level sessions and one-to-one business meetings, the AFRICA CEO FORUM 2014 has become the place to be for all those driving the continent’s growth.

About the Africa CEO Forum

Developed in partnership with the African Development Bank, the AFRICA CEO FORUM is an event organised by Groupe Jeune Afrique, publisher of Jeune Afrique and The Africa Report, and by Rainbow Unlimited, a company specialising in the organisation of business promotion events and manager of the Swiss-African Business Circle (SABC).

Related News

Why should the SADC EPA allow export taxes?

Negotiations on the SADC EPA are close to completion, but to finalize the deal limitations on export taxes should be abandoned. An acrimonious battle on the issue will impose more costs than allowing export taxes.

On 1 October 2014, the ten-year negotiations on free trade agreements between the European Union and groups from Africa, the Caribbean and the Pacific (ACP) will come to an end. It remains uncertain if all parties will have completed their Economic Partnership Agreement, or EPA. But on that day in October, regardless of the state of the deal, the EU will put an end to the difficult and at times acrimonious negotiations. The stakes remain high. The EPAs are meant to replace the long-standing Cotonou agreement, which gave ACP countries duty-free access to the wealthy European market. This access provided a competitive edge that will disappear if no agreement is reached. In SADC, Botswana, Namibia and Swaziland would lose duty free access to the profitable EU market; while South Africa and Angola, Mozambique and Lesotho would maintain access under the Trade Development and Cooperation Agreement (TDCA) and Everything But Arms agreements respectively.

Thankfully, the negotiations on a Southern African Development Community (SADC) EPA are close to completion, but a range of the most difficult issues have been left until last, and must now be overcome. Five remaining issues have consistently stood in the way of the completion of a deal. They are export taxes, the Most Favoured Nation (MFN) clause, agricultural safeguards, rules of origin, and regional integration. Each barrier remains important, but export taxes are particularly divisive. A change of mindset on the issue and a removal of requirements on export taxes would be a welcome step towards completing a workable EPA.

Fairness vs. policy space

Exports taxes are, as the name suggests, duties placed on exports. Export taxes are usually applied to commodities, in an attempt to divert supply of the good away from the export market and into the domestic market, thus driving the price up internationally and down locally. While they have sometimes been used to generate government revenue or improve food security, the primary use of export tariffs is to encourage local processing and beneficiation of basic goods. The EU insists on a ban on all export taxes for South Africa and Angola, and a ban on export taxes for other SADC EPA countries in all but a few extreme cases.

The EU sees export taxes as fundamentally unfair. Export taxes can drive up prices, harming the importer – in this case the EU – while relatively wealthy countries like South Africa benefit at their expense. The EU sees Africa as a vital strategic source of basic commodities, and is concerned about anything that can interrupt their supply of cheap raw materials. African countries see export taxes as a means to move up the value chain, and to break the colonial relationship in which they sell unprocessed goods to the rich world, and then buy back processed goods, making a loss in the process. They see the development of domestic processing as way to industrialize, creating jobs and moving the continent up the value chain. Both positions are legitimate, but there is nevertheless a clear avenue for resolution on export taxes.

The SADC EPA should allow export taxes

Simply put, the EU should abandon its objection to export taxes, for three reasons.

First, export taxes are highly unlikely to create large harms for the EU market. Export taxes impose costs on both the exporter and the importer. Exporters (African firms) have to pay an additional tax to export their goods. Importers (the EU) face extra costs because exporters raise prices to account for the tax. Crucially, the mechanism by which the EU would suffer is thus rising prices. But prices for the commodities the EU cares about are set on the world market. Unless a country has a huge proportion of the global market for that commodity, they will not have the requisite market power to change global prices significantly. In most cases, African countries do not have the necessary market power to effect global prices. This means that overwhelmingly it is local firms who will bear the cost of export taxes, because they will have to accept both the tax and fixed world prices. Given this cost, there is a natural disincentive against the use of export taxes, and they will almost certainly be used sparingly, and only in cases in which they can do so much good that this harm is offset.

Secondly, banning export taxes is an intrusion on the sovereign decision-making of African states. Yes, export taxes are complicated and many opposing voices need to be considered. But these voices should be heard in the context of a domestic political process that is accountable and balanced. Europe insists on similar sovereignty for the industrial support it provides under the Common Agricultural Policy, and it is hypocritical to ignore these demands in the case of Africa. Domestic policymaking processes will make better decisions and will more closely reflect the views of those exporters who are most effected by the costs of export taxes.

Finally, export taxes have become an incredibly poisonous issue. They are seen as representing Europe’s attempt to maintain old colonial value chains, and of ignoring the development interests of the continent. The idea that shoving these conditions down the throat of African states will exacerbate Europe’s resource security is misguided. Even if Europe succeeds in banning export taxes, this victory will come at a further loss of ground in the battle for the hearts and minds of African states. Europe has already fallen behind the likes of China in tapping into Africa’s natural wealth for precisely this reason. Ultimately, a strained relationship will cost Europe more than the use of export taxes will ever provide.

Conclusion

The SADC EPA will only make a meaningful contribution if it can succeed outside the negotiating room, when it is placed in the hands of the domestic regulators who must put it into practice. Successful implementation will only be possible if those politicians and civil servants believe the deal is beneficial. Strategic concessions on issues like export taxes hold the key to building the necessary political will to give life to the deal, and to strengthen the vital EU-Africa partnership.

Christopher Wood is a researcher in the Economic Diplomacy Programme at the South African Institute of International Affairs.

This article is published under Bridges Africa, Volume 3 - Number 2, by the ICTSD.

Related News

Time to modernise trade rules for digital era

In the past, nations with the best ships and ports were able to establish global trade leadership and the growth that came along with it. Today, global trade has gone digital.

In the digital economy software-enabled products and services such as cloud computing and data analytics are the key drivers of growth and competitiveness.

In fact, the world now invests more than $3.7 trillion (R40 trillion) on information and communications technologies a year.

In South Africa, we spend $26 billion a year and the total for the Middle East/Africa region is $228bn. However, to maximise our return on that investment, it is important for policymakers to eliminate barriers that could inhibit the continued expansion of digital trade.

It is clear that software-driven technology is transforming every sector of the global economy. For example, thanks to unprecedented processing power and vast data storage capabilities, banks can detect and prevent fraud by analysing large numbers of transactions; doctors are now able to study historical trends in medical records to find more effective treatments; and manufacturers can pinpoint the sources of delays in global supply chains.

Against the backdrop of this kind of innovation, any country that wants to compete in today’s international marketplace must have a comprehensive digital agenda at the core of its growth and development strategy.

In addition to domestic initiatives such as investment in education and skills training, or development of information technology infrastructure, policymakers can succeed in laying the groundwork for broad-based growth in the digital age if they focus on three big priorities.

First, any bilateral or multilateral trade agreement needs to facilitate the growth of innovative services such as cloud computing. As part of this, there should be clear rules that allow information to move securely across borders and prevent governments from mandating where servers must be located except in very specific situations.

Second, to promote innovation and foreign investment, continued intellectual property protection is vital and the use of voluntary, market-led technology standards – instead of country-specific criteria that force firms to jump through different technical hoops every time they enter a new local market – should be encouraged.

Third, all governments should ensure there are level playing fields for all competitors so customers have access to the best products and services the world has to offer.

At the same time, disclosures about government surveillance programmes in the US and other countries have sparked a renewed focus on data protection and personal privacy. Those concerns are worthy of debate and careful reform. But it is critically important not to conflate separate issues: We can’t let national security concerns derail digital trade.

There is precedent for navigating periods of change such as this in the global trade arena.

Policymakers stood at a similar inflection point in the 1980s when they recognised the keys to growth in the coming decades would be intellectual property, services and foreign direct investment.

With foresight and hard work, they updated trade rules in the Uruguay Round of multilateral negotiations to ensure commitments were in place to provide a check against protectionist impulses.

Now, as governments pursue robust growth agendas for the digital economy, it is critical we modernise trade rules again.

Marius Haman is the chairman of BSA: The Software Alliance (South Africa)

Related News

Agriculture cornerstone of Southern Africa’s economy

Although southern Africa’s growth has been driven by minerals and other natural resources, agriculture offers the greatest potential for transforming the Southern Africa’s economy.

Speaking at the official opening of the 20th Session of the Intergovernmnetal Committee of Experts (ICE) in Livingstone, Zambia, Secretary to the Treasury, Fredson Yamba, representing Minister for Finance, Republic of Zambia, Alexander Chikwanda said that agriculture remains one of the most important source of revenues and foreign exchange earnings for governments in the region contributing an average of 30 percent gross domestic product and about 70 percent of employment in Southern Africa.

“Southern Africa boasts massive arable land water resources suitable for large scale crop and livestock production with great potential for fish farming region, but remains underutilized due to low value addition along the agricultural value chain” he said.

Yamba said that the region should optimize and develop agriculture to transform the region’s economy to address rising poverty and growing inequality. “It is imperative that we boast our efforts to entrench inclusive growth and not merely marvel at high gross domestic products growth rates in our countries” he said.

Knowledge and technical capacity

Meanwhile, United Nations Economic Commission for Africa (ECA) Southern Africa Office, Director Said Adejumobi, said Africa needs knowledge and technical capacity.

He said that Africa would have to invest more in cutting edge knowledge and research, especially in science and technology and technical capacity in order to fully harness our natural resources.

Adejumobi said that the challenge was how to make natural resources work for us in stimulating industrialization, facilitating sustained economic growth and development and promoting social transformation.

“Knowledge and technical capacity are the major differentiating factors amongst nations in a knowledge driven World. This is what will make the difference for us in the next five decades as to whether Africa will remain producers of primary products or join the league of industrialized nations.” He said.

He added that natural resources are national assets that should be used for the interests of all citizens expressing concern on economic inequality which has assumed a global problem. Southern Africa has one of the highest rates of economic inequalities in the World.

“Inequality has economic and social consequences. It deepens poverty, affects the quality of life, and denies the majority of the people the fruits of economic progress. It may also create social tension, if not taken care of, over time. As such, our economic growth must not only be inclusive but address the challenges of economic inequality.”

Adejumobi added that the story about Africa Rising was real and visible, but the content and quality is what needs interrogation.

The two day high level meeting jointly organized by ECA and the Government of Zambia has brought together close to 100 delegates including representation from 12 member States and experts in natural resources, industry, academia, civil society and other international organisation. Also present COMESA, SADC, AU and other cooperating partners.

The ICE was preceded by a two day Adhoc Group Expert Meeting (AEGM) from 10-11March under the same theme ‘Making Natural Resources Work for Inclusive Growth and Sustainable Development’. The meeting will among others discuss and review outcome recommendations from the AEGM.

Related News

Nigeria giving SA a run for its money

On March 31 Nigeria is going to shoot past South Africa to become the largest economy in Africa, says Peter Fabricius.

GDP – Gross Domestic Product – has always seemed to be one of the most objective measures of a country, like population size or land area. Turns out that it’s not. There isn’t, after all, a gynormous till somewhere at the Reserve Bank that automatically rings up every single commercial transaction in the country to total the nation’s GDP.

It is instead based on certain assumptions, not least how much weight the gnomes who calculate such things assign to different sectors of the economy.

That’s why Nigeria is going to shoot past South Africa to become the largest economy in Africa on March 31. Nigeria is rebasing its calculation of GDP, from the current base of 1990 to 2010.

That means, essentially, that GDP will give greater weight to new sectors of the Nigerian economy that have become more important since 1990 such as telecoms, IT, Nollywood and the rest of the entertainment industry.

Nigeria’s nominal GDP is now about $305 billion and South Africa’s about $350 billion. Rebasing will boost Nigeria’s GDP by 40 to 60 percent, according to Bismarck Rewane, MD of Nigeria’s Financial Derivatives Company, speaking at a seminar on the subject at the Gordon Institute of Business Science this month.

That means Nigeria’s GDP will immediately expand to somewhere between $427 billion and $488 billion, leaving South Africa a distant second.

What will that mean for both countries?

Rewane thought it would be mostly good for Nigeria, lowering its debt and fiscal deficit ratios and boosting investment.

On the downside, it would widen inequality and by lifting Nigeria from an officially low-income to a middle-income country, would reduce the amount of foreign development aid it received.

And for South Africa?

Well, clearly it will lose its coveted bragging rights as Africa’s largest economy. That will be particularly galling to some in the government and elsewhere who regard Nigeria as a rival.

Some fear that South Africa might also lose its position as Africa’s – unofficial – representative at international organisations like the G20 and Brics.

The consensus at the seminar, however, seemed to be that, if anything, Nigeria might become Africa’s second representative in those clubs, which would be a good thing.

In any case, the G20 and Brics would probably be reluctant to kick South Africa out.

Likewise, if the UN Security Council is ever expanded and two new permanent seats are created for Africa – as Africa wants – there should be no problem. If Africa gets only one seat, Nigeria’s chances of winning it will presumably now be improved.

Economically the impact on South Africa is harder to assess. Rewane suggested that when Nigeria became number one, “South Africa’s anaemic economy and faltering currency may appear less appealing” to investors.

However, Annabel Bishop of Investec Bank and Yvette Babb of Standard Bank did not forsee any great economic impact on South Africa.

Both pointed out the advantages that South Africa would continue to enjoy as the main gateway to Africa, including superior infrastructure, institutions, and financial systems and a vastly bigger capital market of about $1 trillion compared to Nigeria’s $100 billion.

A Nigerian in the audience objected that his country was being painted almost as a failed state, ignoring its high education standards and the dynamism of its entrepreneurs.

By contrast South Africa had been “almost a banana republic” last year as strikes had crippled the economy.

Babb insisted she was merely presenting a nuanced picture and that Nigeria would have to improve institutions and infrastructure if it was really to boom.

Ade Ayeyemi, a Nigerian who heads Citibank’s sub-Saharan operations from Joburg, had the second-last word, saying it was a quibble whether Nigeria or South Africa was the biggest.

“We’re all pygmies in Africa. We need to join forces to make Africa as a whole more attractive.”

The last word came from Lyal White of the Gordon Institute of Business Science who proposed that being overtaken by Nigeria would be good for South Africa, jolting it out of its complacency and spurring it on to greater things.

Peter Fabricius is Independent Newspapers’ foreign editor.

Related News

African connections

Twenty years after joining COMESA, Egypt is still not making the best use of the opportunities the bloc offers, reports Samia Fakhri

With a market of nearly 400 million people, total annual exports of $110 billion, and total annual imports of $100 billion, the Common Market for Eastern and Southern Africa (COMESA) is Africa’s largest regional economic bloc.

However, Egyptian businessmen attending COMESA meetings this year and held recently in Kinshasa in the Democratic Republic of Congo have been worried that the freeze on Cairo’s membership in the African Union (AU) will damage its business prospects in the region and that the country is not making best advantage of its membership of the bloc.

Amany Asfour, the first woman and the first Egyptian to head the COMESA Business Council, told Al-Ahram Weekly that the freeze on AU membership was not hampering Egypt’s ties with COMESA members.

Any misconceptions about Egypt in Africa, she said, were a by-product of European media prejudice and could be corrected by appropriate action.

Over the next two months Egypt will be staging marketing campaigns in Kenya, Uganda, Ethiopia, Tanzania, and Sudan to introduce Egyptian products to these countries.

The campaigns will include exchanges of visits by Egyptian and African business people, and the focus will be on medium, small, and micro projects on the continent. Egyptian companies are also interested in taking part in infrastructure, agriculture, and mining ventures in Africa, Asfour said.

Egypt will also play host to the Second COMESA Tourism Conference in the second half of 2014, an event that will bring together hoteliers, restaurateurs, travel agents, and industry specialists from various eastern and southern African countries.

“Our presence in COMESA hasn’t been fully utilised. Until recently, Egypt exported nearly $2.5 billion to the COMESA countries, including $1 billion to Libya and Sudan last year,” Asfour remarked.

Many experts hope to see an improvement in the shipping and transport infrastructure of the continent. Poor roads, underdeveloped transport systems, and the lack of proper insurance and credit arrangements have all been cited as impediments to intra-regional trade.

Since her appointment as head of the COMESA Business Council, Asfour has been trying to promote a project connecting Sudan, Ethiopia, Kenya, and Uganda by road. The project, once completed, is expected to give a considerable boost to inter-African trade.

One of the areas in which Egypt can promote its ties with COMESA is manufacturing.

“Egypt has a lot of potential for COMESA, especially in industry. Most COMESA countries suffer from a shortage of manufactured products, and their markets have plenty of room for Egyptian industries,” Asfour said.

Egypt is also interested in importing agricultural products and minerals from COMESA members. Currently, Egypt imports tea from Kenya, coffee and meat from Ethiopia, and copper from Zambia.

Tensions between Egypt and Ethiopia over the latter’s Renaissance Dam have not marred Egyptian relations with COMESA members, but the issue needs to be addressed, according to Asfour.

“The Ethiopian public needs to understand that Egypt doesn’t wish to impede Ethiopia’s development,” she said, adding that stronger ties between business and civil society could help clear the atmosphere between Egypt and Ethiopia.

Nasser Bayan, chairman of the Egyptian-Libyan Society for Investors and Businessmen, agreed that Egypt had yet to utilise the full potential of its COMESA connections.

Explaining some of the problems involved in transport, Bayan noted that “to bring merchandise to Zambia, I have to go first to South Africa and then to Zambia. The same problem exists if I want to go to Kenya. This is the problem of doing business in the African market.”

Not only is it hard to reach land-locked African nations with poor roads and inadequate landing and storage capacity, even the banking and insurance sectors also have their problems.

“There is always a problem with financial transfers. African countries, unlike in Europe and America, don’t order merchandise in advance, but expect to buy stuff that is already in stock. So to do business with them, you have to make the products and store them in Africa and then wait for the customers to come calling,” according to Bayan.

Hussein Mahran, a member of the Egyptian Council for Economic Affairs, said that “if we look at COMESA’s imports, we notice that its member countries import much of their needs from across the world, although the same products could be better supplied by Egypt.”

Mahran said that Egypt could supply high-quality kitchenware, shoes, textiles, and aluminum products cheaper than the countries currently exporting to COMESA members.

Intra-regional trade in Africa stands at 4.2 per cent of Egypt’s trade at present. “Our goal is to bring this figure to eight per cent,” he said.

To invest in COMESA, Egypt can also use credit from the African Development Bank, something that Chinese and European companies are already doing.

Mohamed Dawoud, director of the Commercial Representation Agency, said he had been pleased with the manner in which trade between Egypt and COMESA had grown over the past ten years.

“Egypt had a trade deficit with COMESA in 2003. But this has turned into a surplus since 2004. In 2008, our exports to COMESA reached $1.5 billion, then exceeded $2 billion in 2010. In 1998, Egypt exported only $45 million to these countries,” he said.

Related News

Chained value

The growth of multicountry manufacturing is changing how the world’s income and growth are generated

The 787 Dreamliner, the latest aircraft produced by Boeing, is a well-known American product, assembled in Washington state and sold worldwide – more than 80 percent of orders come from outside the United States.

Not only are Dreamliners bought by the world, they are made in the world. Many of their parts and components are manufactured outside the United States, among them the center fuselage by Alenia (Italy); the flight deck seats by Ipeco (United Kingdom); the tires by Bridgestone (Japan); the landing gear by Messier-Bugatti-Dowty (France); and the cargo doors by Saab (Sweden).

Airplanes are just one example of multicountry manufacturing. More and more final products – such as automobiles, cell phones, and medical devices – are produced in one country using inputs from many others, partly as a result of fewer trade barriers and technology-led declines in transportation and communication costs over the past 20 years. This development, what we call the growth of global value chains, is changing how world income and growth are generated. At the same time, the nature of competition has been affected. Are countries competing over the goods produced or over the labor and capital that go into production? Changes in the nature of competition are, in turn, changing the formulation of trade and other policies that are targeted to improve competitiveness. In this article we review how the growth of global value chains has affected income and growth, measures of competitiveness, and trade policies.

Remarkable growth

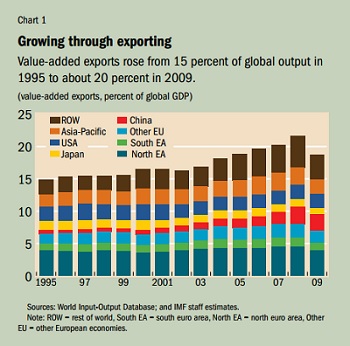

The growth of trade relative to total output in the past two decades has been remarkable – a reflection in large part of the number of times intermediate products cross borders. The world export-to-output ratio rose from 20 percent in 1995 to 25 percent during 1995-2009 (in 2008, the ratio was as high as 30 percent, before falling during the global financial crisis). The change is even more impressive for some countries – such as China, where the ratio rose from 23 to 39 percent, and the northern euro area countries, where it went from 30 to 40 percent.

The growth in gross exports relative to output to some extent reflects more intensive use of global value chains: more intermediate inputs move from one country to another as part of the manufacturing process. To produce just one more Dreamliner, for example, requires more imports – cargo doors from Sweden, tires from Japan, landing gear from France, and myriad other components from foreign suppliers. Assessing the growth and income effects of value chains, however, requires looking at more than just gross exports. The value of a country’s exports (for example, a Dreamliner sold by the United States) can be very different from the value the country adds to its exports. The so-called value-added exports in this case represent the labor and capital income generated in the United States to export the Dreamliner.

A critical question is whether the growth of global value chains is generating wealth in the countries that make up the chain. The short answer is yes, but at different speeds within and across different economies. Most countries and all regions have increased their contribution to world output through exports. But for some this growth has been faster than for others. Globally, value-added exports increased from 15 percent of world GDP in 1995 to about 20 percent in 2009 (see Chart 1). Over time, both labor and capital income have increased, although capital income has grown faster as value-added exports have become more capital intensive.

A critical question is whether the growth of global value chains is generating wealth in the countries that make up the chain. The short answer is yes, but at different speeds within and across different economies. Most countries and all regions have increased their contribution to world output through exports. But for some this growth has been faster than for others. Globally, value-added exports increased from 15 percent of world GDP in 1995 to about 20 percent in 2009 (see Chart 1). Over time, both labor and capital income have increased, although capital income has grown faster as value-added exports have become more capital intensive.

Growth isn’t just about manufacturing: income in global value chains is generated increasingly by exporting services, many of which are susceptible to offshoring or outsourcing. Income generated by exporting financial, communication, business, and other services directly, or indirectly as part of manufactured goods exports, increased from 6 percent of world output in 1995 to almost 9 percent in 2008.

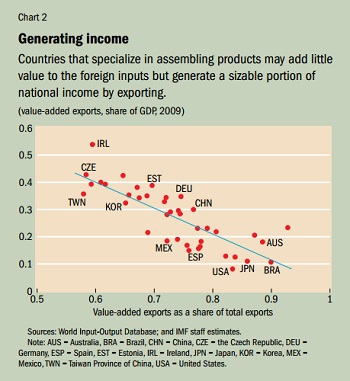

The increase in value-added exports results from a number of factors, but participation in global value chains appears to play an important role. Consider countries that specialize in the assembly stage. They import expensive core inputs, add relatively little value to those inputs, and export goods whose added value is largely foreign. These countries’ ratios of value-added exports to gross exports tend to be lower. But even though they take on low-value-added assembly tasks, their exports still generate a substantial portion of their  income – that is, they have a high ratio of value-added exports to GDP (see Chart 2). These are also the economies that have been growing relatively fast since the mid-1990s, which suggests that there are important learning effects and other kinds of positive spillovers on the rest of the economy that come from anchoring a country to global value chains. For example, local firms in countries that specialize in assembly may indirectly benefit from exposure to new technology used by foreign firms or the improved business environment associated with foreign investment.

income – that is, they have a high ratio of value-added exports to GDP (see Chart 2). These are also the economies that have been growing relatively fast since the mid-1990s, which suggests that there are important learning effects and other kinds of positive spillovers on the rest of the economy that come from anchoring a country to global value chains. For example, local firms in countries that specialize in assembly may indirectly benefit from exposure to new technology used by foreign firms or the improved business environment associated with foreign investment.

Changing competitiveness

Since December 2012, when Shinzo Abe became prime minister of Japan, the Japanese currency, the yen, has lost about 20 percent of its value against the euro and the dollar, which could affect Japan’s Asian trading partners in two ways. It could mean that their exports are competing with much cheaper Japanese products. But the lower yen could also reduce the cost of the intermediate inputs they buy from Japan. Which effect predominates depends on how much a trading partner directly competes with Japanese products and how important Japanese imports are in products these countries produce as part of global value chains.

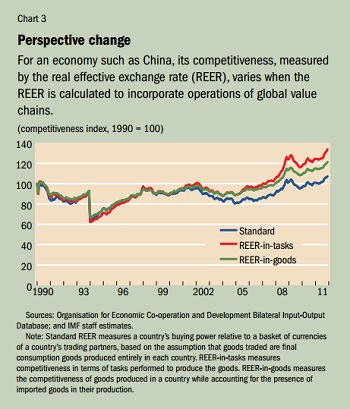

Economists’ standard approach to measuring a country’s price competitiveness is to calculate its real effective exchange rate, which essentially measures the buying power of a currency relative to a basket of currencies of its trading partners. This measure, though, is based on the assumption that goods traded are final consumption goods only and that goods are produced entirely in each country. In a world with value chains, this assumption is obviously incorrect. In recent years, two approaches have emerged to incorporate the international fragmentation of production into measuring the real effective exchange rate. Both provide useful new insights but with a slightly different focus.

One approach (Bems and Johnson, 2012) is to construct an index that measures competitiveness in terms of tasks performed to produce goods rather than the goods themselves. Such an index is better suited for measuring the competitiveness of a country’s factors of production (that is, labor and capital). A second approach (Bayoumi, Saito, and Turunen, 2013) measures the competitiveness of the goods produced in a country while accounting for the presence of imported inputs in their production. This index is better suited for measuring the competitiveness of goods shipped out of a country.

Empirical differences between the standard real effective exchange rate and the new indices incorporating global value chain operations are significant. For example, China had an additional 14 to 27 percent cumulative appreciation in its real effective exchange rate during 1990-2011 relative to the standard measurement (see Chart 3). In other words, China is less competitive than a standard real exchange rate calculation would suggest, mainly because the new measures better capture the rapid increase in the cost of wages and other factors in China (relative to its trading partners) during this period. The amount of additional appreciation varies depending on whether competitiveness is measured in terms of tasks or goods.

Empirical differences between the standard real effective exchange rate and the new indices incorporating global value chain operations are significant. For example, China had an additional 14 to 27 percent cumulative appreciation in its real effective exchange rate during 1990-2011 relative to the standard measurement (see Chart 3). In other words, China is less competitive than a standard real exchange rate calculation would suggest, mainly because the new measures better capture the rapid increase in the cost of wages and other factors in China (relative to its trading partners) during this period. The amount of additional appreciation varies depending on whether competitiveness is measured in terms of tasks or goods.

Global value chains involve more than just the relationship between a buyer and seller of final goods – just as the purchase of a Dreamliner involves not only the United States and the buying country but all economies that participate in the Dreamliner value chain. Changes in exchange rates between countries that are integrated in a value chain may therefore be more important and more complex than indicated by standard real effective exchange rate measures. The new indices are a step toward uncovering the complexities in value chain relationships – although more work and more data are needed to make them a tool for day-to-day policy analysis.

Blurred boundaries

Although global trade talks under the auspices of the World Trade Organization (WTO), the so-called Doha Round, have stalled, a number of substantial free trade agreements are being negotiated that are not global but involve many large economies and cover a significant amount of global trade. For example, in 2013, the United States and the European Union began negotiating what they call the Transatlantic Trade and Investment Partnership (TTIP). Another important free trade pact under negotiation is the 13-nation Trans-Pacific Partnership (TPP). The growth of value chains – which has increased the complexity of international commerce and blurred the boundaries between trade and domestic policy – requires the kind of new trade rules that are often negotiated within these trade agreements.

Supply chains mix the flow of goods, investment, services, technology, and people across borders. Baldwin (2011) calls this jumble “supply-chain trade.” Supply-chain trade differs markedly from traditional trade in final goods. In supply-chain trade, firms must set up production facilities in many countries and connect those factories – moving personnel, capital, and technology among many locations.

For policymakers, there are two challenges. First, domestic policies are a more important barrier to international trade than in the past. For example, weak protection of intellectual property and investment rights hurts global value chains because moving production to another country (offshoring) increases the international exposure of a firm’s knowledge and capital. Second, the rise of global value chains creates new forms of international policy spillovers because governments’ policy choices that affect the domestic component of the international production chain also affect the full value of the chain. These challenges create a demand for international policy agreement. But the content of these agreements is no longer about keeping the temptation of self-destructive tariff wars under control, but about ensuring that policies that regulate the different parts of the value chain of complex goods like the Dreamliner are coherent across countries.

The new rules and disciplines underpinning the rise of supply-chain trade have been and continue to be written, primarily (but not only) in newly negotiated free trade agreements. These agreements often include legally enforceable provisions that go beyond the commitments negotiated under the WTO (WTO, 2011). In a survey of 96 free trade agreements covering 90 percent of world trade, the WTO found that the core rules introduced in these agreements govern competition policy, intellectual property rights, investment, and movement of capital. For instance, 73 percent of agreements in the survey contain obligations on competition policy outside the current WTO mandate. While a number of factors are behind the new wave of free trade agreements – including geopolitical considerations and the difficulties in the multilateral negotiations under the WTO – the need to provide governance to supply-chain trade is an important driver.

This relationship between free trade agreements and global value chains has overall economic consequences that are often overlooked in the policy debate:

-

The pattern of trade agreements will influence the future geography of value chains, forcing latecomers to adopt rules negotiated by others. This may create a risk of regulatory fragmentation of the multilateral trading system and impair further development of value chains. Finding ways to “multilateralize” free trade agreements is an important objective.

-

The new wave of trade agreements will magnify the transmission of policy and economic shocks between members and reduce their transmission between members and nonmembers. That is because firms that engage in cross-border production are inevitably more vulnerable to unexpected events – earthquakes, for example – that disrupt the provision of customized inputs.

-

Economic models that estimate the effects of trade agreements generally focus on the consequences of removing high tariffs in protected sectors. However, mega free trade agreements, such as the TTIP and the TTP, are mostly about nontariff measures, many of which relate to cross-border production decisions that have a direct impact on growth. As a result, the effects of these agreements on economic welfare may be substantially different from those suggested in the current policy debate.

Economic consequences

In the past 20 years, the rise of global value chains has changed the nature of international trade with implications on, among others, the generation of income, measures of competitiveness, and trade policymaking. The message is simple: recent developments in the area of trade have significant macroeconomic consequences, including on economic growth, countries’ competitiveness, and the transmission of shocks.

Our research points to three broad conclusions. Global value chains are generating wealth, but at different speeds within and across countries. They are also affecting the notion of competitiveness, making it more important to capture how firms produce across multiple borders. Finally, global value chains magnify interdependence across countries and, hence, the need for policy cooperation.

Michele Ruta is a Senior Economist in the IMF’s Strategy, Policy, and Review Department and Mika Saito is a Senior Economist in the IMF’s African Department.

This article is based on the 2013 IMF Policy Paper “Trade Interconnectedness: The World with Global Value Chains” and appears in Finance & Development, March 2014, Vol. 51, No. 1.

Related News

Azevêdo reports “excellent start” on efforts to put Doha Round back on track

Director-General Roberto Azevêdo reported to the General Council on 14 March 2014 that the chairs of the negotiating groups have completed the first round of consultations on Doha Round issues that might be taken forward. He said: “I have heard a lot of good feedback – and I think there is much which we can build on constructively. But, nevertheless, there remains a lot to do.”

Report by the Chairman of the Trade Negotiations Committee

This is going to be brief report, for two reasons in particular.

Firstly, because the Chairs of the Negotiating Groups will be issuing full written reports of their consultations at the end of this meeting which you will have time to read and consider – I think this will be more productive than me reading them out here.

And secondly, because I am planning to convene a meeting of the TNC on 7 April, which will provide an opportunity for a more detailed discussion on each of the negotiating areas. So I will not spend too much time on these discussions now.

Mr Chairman, since the Ninth Session of the Ministerial Conference in Bali, the TNC has held one informal meeting on 6 February 2014.

My statement at the meeting has been issued in document JOB/TNC/37, and I would request that it be included in the records of this meeting.

Since that meeting I have been listening to members here in Geneva and talking to the Chairs of Negotiating Groups – who have of course been conducting their own consultations.

I have also seized the opportunity, whenever I am visiting capitals around the world, to further our work and bring greater focus to our forward planning.

When we met here in February we discussed our next steps after Bali. And I highlighted the two priorities for our work in 2014:

The first priority is to deliver on the blood, sweat and tears that we put into the Bali Package by implementing the decisions and agreements that we reached there.

I know that this work is incredibly important for all members in demonstrating that not only can we reach negotiated outcomes, but we can also implement them – bringing real benefits to the people we are here to serve.

The second priority is to prepare a clearly defined work program to conclude the Doha Development Agenda – and we must do so by the end of this year.

At the TNC in February I asked the Chairs of the Negotiating Groups to start a dialogue with members on issues that we may be able to take forward – using a set of very simple parameters to guide the discussions.

A broad range of views were expressed at that meeting in February. Overall I felt that the tone was very positive – and I didn’t hear any member say that they were not ready to engage on the basis that I had outlined.

So we have done what we said – we have proceeded on this basis.

I met with the Chairs of the Negotiating Groups yesterday and they confirmed that they have held an initial round of consultations with members.

As I mentioned, the Chairs’ full written reports of their discussions will be made available at the end of this meeting – and I encourage you to study them in detail in the coming days.

I will give just a brief summary of progress in each of the respective areas.

It seems that some factors were common among some of the Groups.

For example in Agriculture, Market Access and Services, it came across strongly that our approach should be balanced across all three issues – and that all three should tackled together, simultaneously

There was also a clear emphasis on the parameters during the discussions – particularly on the importance of development, and on ensuring that we focus on outcomes that are doable.

Now, let’s look at each area in turn – starting with the Special Session of the Committee on Agriculture.

The Chair’s consultations so far have highlighted a range of views:

-

Most Members acknowledged the need for a balanced approach among the three key pillars of agriculture in the areas of market access, domestic support and export competition. Among the three pillars Export Competition is recognised as an important priority for a large group of Members.

-

Many Members highlighted the importance they attached to the draft modalities, while other members have placed less emphasis on this.

-

Ensuring that further discussions are assisted by appropriate updated data and information on member policies was highlighted by some Members.

-

The need to ensure a coherent approach to the work within the Regular Committee on Agriculture to implement Bali outcomes and the ongoing work in the Special Session was also mentioned.

Let me turn now to the Negotiating Group on Market Access.

In relation to “what went wrong?”, several factors were cited. These include negotiating approaches, the different expectations among Members regarding the NAMA outcome and the different perceptions about the balance in the current modalities text.

As to “what should be done?”, several questions were discussed including whether or not to continue where Members left off, the possibility of updating the technical negotiating base and whether to discuss in a more generic manner the question of what is doable in this area.

Some delegations express their views on the latest draft modalities, but, as I understand it, no common position was reached.

The Group’s discussions will need to continue in order to establish how Members can contribute to a meaningful result on market access.

The Chair has offered some personal conclusions and suggestions at the end of his report, as you will see.

Let’s move now to the Special Session of the Council for Trade in Services.

There was broad convergence that, in addition to balance across the three market access pillars, there would also need to be balance within the services agenda itself. And such an outcome would require the exploration of new approaches.

Many said that, with any outcome in services, the development dimension of the round will need to be fully reflected.

The need to avoid previous mistakes was also seen as crucial. Some wished to avoid the sequencing of DDA negotiations, which in their view had placed services at a disadvantage – while others stressed that progress in services must be contingent on progress elsewhere.

While further deliberations are needed, it was widely accepted that an appropriate level of ambition in services would have to be commensurate with those in agriculture and NAMA.

Regarding the plurilateral negotiations on services, which are taking place outside the WTO – some saw these as complementary to the WTO negotiations and emphasized the potential for cross-fertilization between the two tracks. Others took the view that such initiatives could undermine the multilateral process.

On the Negotiating Group on Rules, most members agreed that there needs to be serious horizontal reflection as to the overall scope and level of ambition of post-Bali activity – and that this should be the basis for determining whether any or all of the Rules issues will be included in the next phase of our work.

A substantial number of delegations were open to including Rules in the work program, but considered that this could only be addressed once clarity has been achieved on the level of ambition for the three “core issues”.

In contrast, a few delegations considered that Rules itself constitutes a “core issue”, and that outcomes on at least certain Rules issues will be essential.

Next is the Special Session of the Council for TRIPS. Based on the interim Chair’s consultations earlier this week, it seems that negotiations on a register for wine and spirit geographical indications would depend on the relationship of this work to other TRIPS issues and the wider Doha Round.

In addition, some Members have expressed interest in recommencing the consultation process on TRIPS implementation issues. We need to look into this further.

Moving on, let’s turn now to the Special Session of the Committee on Trade & Environment.

As this is his last meeting as chair of the Negotiating Group, Ambassador Selim Kuneralp will give his own personal update to Members when the Chairman of General Council opens the floor in a few moments.

So I will just say I understand that in these discussions members have reiterated the view that environmental negotiations remain an important element of the overall Doha mandate – and continue to be high on delegations’ political agendas.

Turning now to the Special Session of the Committee on Trade & Development.

The Chair has encouraged Members to review the three areas of outstanding work, specifically the remaining Agreement Specific Proposals – including the Cancún-28.

The indications are that delegations recognise the centrality of development in our post-Bali work and have an open mind on the possible elements in the development pillar of the post-Bali work program. Some Members observed that this work program will inevitably influence the contours of the work program on S&D.

The Chair reports that there is a sense of preparedness for serious engagement among the Members – and an acceptance of the need for creative approaches. However, for this to happen, Members will need a clear road map with tangible substance. A clear articulation of concerns and interests will help us to move towards a successful outcome in the work of the Special Session.

Finally, let’s look at the Special Session of the DSB.

Work has continued on the basis of the “horizontal process” launched in June last year, which is geared towards identifying achievable outcomes across the board. In three areas – namely: remand, post-retaliation and third party rights – some elements were presented as possible bases for solutions. This effort was very well received and will set the tone for further work.

Further progress now requires willingness to be flexible across-the-board to develop achievable outcomes that reflect the interests of all participants.

That concludes the round-up from the negotiating groups.

I would like to thank all the Chairs for their work. And in doing so, I would like to pay particular tribute to the outgoing chairs:

-

Ambassador Selim Kuneralp of Turkey.

-

Ambassador Fook Seng Kwok of Singapore, who unfortunately cannot be here today.

-

Ambassador Fernando de Mateo of Mexico.

-

And Ambassador Alfredo Suescum of Panama.

Thank you all for your contribution. I know that everyone in this room – and outside this room – has greatly appreciated your efforts.

I have also been considering how best to ensure that we advance LDC issues. These were key in Bali – and will only take on greater significance as our work progresses.

Following consultation with the LDC Group, I have asked Ambassador Steffen Smidt to continue as the Facilitator for LDC issues this year.

I am pleased to say that Ambassador Smidt has agreed to this request, and I would like to thank the Danish Government for allowing him to do so.

I think this is a very welcome development – and I trust members will extend to Ambassador Smidt the same support and co-operation that you gave him last year. So thank you Steffan.

In closing, Mr Chairman, I think we have made an excellent start.

I have heard a lot of good feedback – and I think there is much which we can build on constructively.

But, nevertheless, there remains a lot to do.

On the basis of the Chairs’ reports, and of my own conversations, I would like to instruct the Chairs to continue their work – and continue this process of consultation. And I will do the same.

We will all need to reflect on what we have heard today – and then to consider our next steps.

The first quarter of 2014 is almost behind us. In the space of just nine months we must complete this work. It is essential that all members are fully engaged in these consultations.

As I said at the TNC in February: 2014 should be a defining year for the WTO – not just as the year that we implement our first negotiated outcomes, but also as the year that we put the Doha Round firmly back on track.

So let’s continue the work we’re in – and let’s redouble our efforts.

This is of course an ongoing conversation. As I have said, I will convene a meeting of the TNC on 7 April to report on further progress and provide for a fuller debate among members on the way forward.

Of course you are free to take the floor now, but I would suggest that we wait for this TNC meeting in a few weeks’ time as we will then be in a better position to have a more thorough and meaningful discussion.

Thank you Mr Chairman – that concludes my report.

Related News

Boosting industrial devt through Free Trade Zones

Revamping ailing economies presents huge challenges of industrialisation. Development of Free Trade Zones remains an attractive option, writes George Okojie.

Proliferation of Free Trade Zones (FTZs) in the country is part of renewed commitment towards realising the importance of an industrial economy in creating jobs and improving standard of living of the people. Thus, Brazil, Russia, India and China known as (BRIC) nations took cover in the platform provided in FTZs as a buffer to economic meltdown particularly in the wake of the most recent financial and economic crisis.

Amid the core of the growth attributed to emerging markets, maximum opportunities offered by the FTZs ameliorated the negative effects of the economic downturn of 2007-2009 leaving the BRIC nations to grow at the rates of seven per cent to 13 per cent.

Free Trade Zones Operations In Nigeria

FTZs establishment in Nigeria dates back to 1991. It was an industrial initiative embraced by economic pundits at that time to diversify nation’s export activity that had been dominated by the hydrocarbon sector. Available statistics showed that by 2011, there were nine operational zones; 10 under construction; and three in the planning stages.

Although Zones could be managed by public or private entities or a combination of both under supervision of the Authority, the governing legislation resides with the Nigeria Export Processing Zones Act (NEPZA) and the Oil and Gas Export Free Zone Act (OGEFZA). The FTZs idea has continued to blossom because Nigeria has a number of strength on which to build including the relatively large market. Exploring the FTZs initiative to boost its economic prosperity, the Lagos State Government established the Lekki Free Trade Zone.

The industrial cluster development started in May 2006 when the Chinese consortium in the name of CCECC-Beyond International Investment & Development Co., Ltd (CCECC-Beyond), now China Africa Lekki Investment Ltd (CALIL) as the majority shareholder, entered into a joint venture with the Lagos State government and the Nigerian partner “Lekki Worldwide Investment Ltd.” to establish the Lekki Free Zone Development Company (LFZDC FZC) in Lagos, Nigeria.

The initiative was authorised by both the Nigerian federal government and the Lagos State government as the sole and legally competent entity to develop, operate and manage the Lekki Free Zone project. Lekki Free Zone Development Company FZC (LFZDC) was registered in October 2006 under the NEPZA Acts and embarked on the Phase I Development of the zone.

One-stop Business Hub

As an emerging international market, the Lagos State government knew that the initiatives come with transfer of technology from the trans-national corporations (TNCs) and minimise capital flight, just as it would make the state a one-stop global business haven. It was designed to have a refinery, an international airport, seaport and high grade residential quarters, among other features that make free trade zones thick.

To realise its objectives, construction work has commenced at the development of Lekki Seaport located within the free trade zone. According to Lagos State Governor, Mr Babatunde Fashola, “Lekki Free Trade Zone is beginning to take shape. The Master Plan is being realised, investors are trouping in. Tank farms and major refineries are springing up to service the demands of the country and make room for export.

“The refineries create a major selling point and release of the opportunities that lie ahead in this zone, create opportunities for the local people and the potentials for Lagos and the Nigerian economy”. Fashola stressed that the speedy completion of the project is subject to availability of funds, while soliciting for the cooperation of the investors to ensure that the overall objective is achieved.

He said, “I cannot tell you the date when that port will be finished but work has started at the port and the contractor is on site. There are still a few issues in terms of getting funding and commitment from the private sector because clearly both the management and the private sector own the zone. They are not government-owned but government has an enabling role to play in the regulation of the Zones”, he said.

The governor said plans are on to effectively drive the zone on water transportation system considering that it is bonded on the side of Atlantic and lagoon. “This zone is located on a peninsula. That is why we are considering the need to transport our goods on the water. We have put the cart before the horse. This is peninsula that sits so strategically that it has access to its own transportation which is water transportation.

“That was why we have decided to fast track the plan of accessing the zone and evacuation of cargo by using the lagoon. This lagoon goes as far as Ondo State. Most logs come into the state through water. I do not know any country where the haulage of its industrial cargo are transported by road. “It is not sustainable. The roads will not last. The water ways would be our immediate and short term focus. And before the end of the year, we would ensure the possibility of water transportation in the zone”.

He said the design for the construction of airport on the zone is also ready, adding that soonest the bid will be sent to the public for investors who want to build to indicate interest. According to him, the state was strategically positioned, citing the advantage of population and proximity to Europe, Middle East and South America, all of which the development of the airport would benefit.

He said the management would source private capital to develop Lekki International Airport, noting that the airport would be of international standard according to the plan already approved. “We have shortlisted bid for people who want to build the airport, for me my responsibility is that you want an airport through which you can run your business but I don’t have the money to build it but I can provide the land which is what we have done. It will be an airport that would drive business at all point like we have seen all over the world.”

He assured that the state government remained truly committed to providing infrastructure needed to make Lekki Free Trade Zone (LFTZ) functional as soon as possible. The Governor advised local manufacturers especially agro-based sector and investors to tap into the Lekki Free Trade Zone initiative phased into four quadrants, on a land mass of about 16,500 hectares.

FTZs As Job, Poverty Alleviation Solution

Giving credence to the fact that creating jobs and income is one of the foremost reasons for the establishment of FTZs, president of the Dangote Group of Companies, Alhaji Aliko Dangote said the Lekki Free Trade Zone would be the biggest of such zones in the African continent. The business mogul said, “By bringing this here, I can assure you that this is going to be the biggest free trade zone in the African continent and I know that the people will begin to show their appreciation”.

Expressing confidence that the Zone holds enormous economic benefits for Lagos State and the country, Dangote declared, “For instance, there is no way we can put down over $9 billion of our money here without making sure that the zone is going to work”, adding that his Group was going to work at a very high speed. Dangote assured that the communities stand to benefit enormously as over 8,000 engineers would be trained while jobs would be created for youths of the communities.

Challenges In Actualisation of Projects

For the Commissioner for Commerce and Industry, Mrs Sola Oworu, establishing a refinery in the zone has opened up enormous economic opportunities not only for Lagos but for Nigeria, adding that only about 35 per cent of the goods to be produced in the zone would be consumed in Lagos while the rest would be exported.

To accelerate development of the LFTZ, Lagos State government and the NNPC in collaboration with a consortium of Chinese investors known as China State had before now sealed a deal for the establishment of the refinery which capacity is put at 300,000 barrels of crude oil per day under a public private partnership (PPP) arrangement within the Lekki Free Trade Zone (LFTZ).

On completion it will in addition to the above crude output, produce 500,000 metric tons of liquefied petroleum gas (LPG) per annum and hopefully trigger the formal switch of domestic household fuel in Lagos and environs from firewood, charcoal and kerosene, to LPG if properly harnessed.

LEADERSHIP Sunday gathered that the proposed date for realisation of the $8 billion Greenfield refinery project may not be possible due to the challenges posed by national policies and frequent changes in the top management of the Nigerian National Petroleum Corporation (NNPC) by the federal government. Also said to be posing a challenge to the early take-off of the refinery is the continued delay in passing the controversial Petroleum Industry Bill (PIB) which is expected to redefine the operations of the oil industry in the country.

International investors that have showed strong interest in the project LEADERSHIP Sunday learnt are watching to see what becomes of the PIB which is now politicised and even polarising the national assembly. The investors in Lekki Free Zone as the state’s new business hub in the making have not been enjoying good relationship with the people of Idasho community in the Lekki area.

So many stakeholders before the last peace accord brokered with the community leaders had appealed to them to allow investors whose aim is to set up businesses at the Zone to commence the process of building industries that would provide employment for the people. They noted that there is no way an investor who has been driven away and has his equipments damaged can create or provide jobs.

The state governor specifically said, “The people in Idasho have not been receptive and have driven investors from the site, they have damaged investors’ equipments yet they want work. If the investor cannot build his factory, how does he create work? If there are issues with government, let us sit down and continue to engage. Let development start in the zone. That is the only way to prosperity”.

Imperative of Incentives In Free Trade Zones

To encourage investment in the zone, the state Commissioner for Energy and Mineral Resources, Engr Taofiq Tijani, said the state government will liaise with other arms of government to offer a number of policies and incentives such as complete tax holidays from all Federal, State and Local government taxes, rates, customs duties and levies to all investors patronising the Lekki Free Trade.

The waiver, according to him, will cover import and export licences, duty-free capital goods, consumer goods, machinery, equipment and furniture, duty-free, tax free import of raw materials and components for goods destined for re-export or permission to sell 100 per cent of manufactured, assembled or imported goods into the domestic market.

He said the present administration led by Mr Babatunde Fashola will continue to provide a thriving environment with exponential potentials to attract both local and foreign direct investment in the area of manufacturing, real estate, tourism, oil and gas. It is the belief of many economic pundits that if the potentials inherent in Free Trade Zones are fully tapped, the nation would experience rapid economic growth.

Related News

Science, ICT critical to Africa’s future – Kagame

The importance of science, technology, research and innovation in shaping the socio-economic transformation of nations cannot be overstated, President Paul Kagame has said.

In sub-Saharan Africa, he said, these “critical enablers” can drastically improve standards of living.

Kagame was speaking in Kigali yesterday at the closure of a two-day forum on higher education for science, technology and innovation.

The forum, which attracted senior government officials and other players from around the continent and beyond, was organised by the World Bank and Government of Rwanda.

Kagame, however, said there was need for the continent to build a critical mass of skills in these areas.

“To unlock this potential, Africa must have well-trained science and technology professionals,” he said.

“I am told only around 25 per cent of tertiary education students in Africa are enrolled in science, engineering and technology. In fast growing countries such as Korea, China, and Taiwan, this figure is close to 50 per cent.”

Kagame recalled that to address the gap, the Connect Africa Summit, held in Kigali in October 2007, recommended to establish five centres of excellence in each sub-region of Africa.

“These centres would support the development of a critical mass of science and technology skills required for the continent’s advancement,” Kagame said, explaining that for Africa to utilise and benefit from global scientific research, it needs scientists who communicate and collaborate with their peers around the world on specific regional and international projects.

He challenged Africa’s higher education sector to play “a unique and important role” in resolving the existing skills gap in Africa.

The Rwanda style

Sharing Rwanda’s experience, the Head of State said over the last two decades, his government has put in place governance and physical infrastructures to develop national science, technology and innovation.

“We know that harnessing their potential and integrating them into Rwanda’s development plans is critical to achieving our national goals”.

He cited the Kigali-based ICT Centre of Excellence, as well as the establishment in the capital of a Carnegie Mellon University campus that operates a master’s degree programme, including at its Kigali campus where it is expected to graduate students this year.

Kagame said these steps gave his government the belief that these seemingly difficult undertakings would deliver intended results.

The President also cited regional collaborative efforts in enhancing science and technology, singling out the partnership among the five East African Community partner states that has resulted in the establishment of the East African Science and Technology Commission, which is based in Rwanda.

“Leveraging opportunities in science and technology contributes to the building of capacity across many sectors, including health, agriculture, trade and industry, infrastructure, environment, and ICT, all of which are key to development,” he said.

“They will help us fight against infectious diseases, increase food production, promote industrialisation, add value to natural resources and arrest degradation of the environment.”

Participants at the conference resolved to strengthen and mobilise resources for building capacity in science and technology in pursuit of Africa’s socio-economic transformation.

Kagame called on the participants and stakeholders to follow up on their commitment, and hailed Brazil, China, India, and Korea for supporting this World Bank and AU-backed effort.

Jessica Alupo, Uganda’s education minister, said they had resolved to adopt a strategic investment in science and technology to accelerate Africa’s development to a knowledge-based society and also harness science and technology job-creation potential.

Related News

The impact of Infant Industry Protection on competition in Namibia

Recent reports have pointed to concerns over increases on consumer prices of basic foodstuffs and commodities, such as poultry, meat and dairy. Some critics have blamed this on the government’s Infant Industry Protection (IIP) policy.

Caution should however be taken when apportioning such blame on infant industry protection. The Minister of Trade and Industry in his recent ministerial speech indicated that the rationale for the adoption of the policy and regulatory measures such as infant industry protection and quantitative restrictions on imports of selected products entering our market are very important instruments to preserve and nurture our economic and industrial growth and in turn accelerate jobs and wealth creation and to equalize wealth distribution by cushioning and creating policy space for existing economic value chains to get off the ground and build the requisite competitive capacity.

Infant Industry protection usually takes three forms, namely that it protects and nurtures local industries such as the imposition of an import duty levy on imported goods, a quantitative restriction on imports, and granting of targeted and performance based incentivized subsidies to stimulate local production and ensure market supply.

Factors affecting basic food prices

It is however undeniable that the prices of basic foods are increasing worldwide. Food prices are expected to rise 3 to 4 percent in 2014 and will continue rising till the year 2018, representing a 12-15% increase over a four year period. There are global factors at play that can have repercussions on food prices. The El Niño drought impact of 2012-2013 withered crops in the fields. As a result, prices for agricultural goods and agro-processing products will tend to rise and since it usually takes several months for these commodities’ prices to translate to the food we buy, most of the price effect of the drought will occur in 2014 as it is happening currently in Namibia.

Higher prices of agricultural inputs will directly affect the cost of meat and any other animal-based product. Also hardest hit will be cereals, baked goods and other grain-based food. The current exchange rate depreciation from around 8-plus to the US Dollar in 2012 to around 10 plus in 2014 will also cause the price of imported food to increase in line with the depreciation impact of the exchange rate. There is therefore cold comfort that Namibians will have to dig deeper into their pockets to meet the rising prices of foodstuffs. According to data and inflation reports by the Namibia Statistics Agency, food price inflation is on an increasing trend and this trend, based on forecast data worldwide, will continue until 2018.

This situation will worsen if the Rand/Namibia dollar depreciates against the currencies of its trading partners, as is the case currently where food imports rise in local currency against foreign prices. The squeeze on many Namibian consumers’ finances will continue for at least the next four years as many experts warn food prices will continue to increase significantly in the world. Rising food prices will result in the annual food bill for the average family tripling over the coming years, heaping further pressure on already overstretched household incomes of the Namibian consumer.

Namibia is not alone!

Namibia is not alone in this since all countries would be affected. The rising food prices are exacerbated by rising global civil and military unrests in countries across Europe and Asia, Ukraine, Turkey, Egypt, Nigeria, Egypt and the Central African Republic. These unrests do cause interrupted supplies and global food shortages along the global distribution chains and cause prices of basic food items to rise. Namibia is a net importer of most of the food we buy from different supermarkets and grocery stores and as a result, rising food prices in global markets will be transmitted into Namibia automatically. In Namibia, food price increases are being driven by rises in key inputs such as maize and wheat, as well as commodities of administered prices such as energy, fuel and water. This implies rising cost structures across the firms involved in the food value chains, prompting them to either seek productive efficiencies and financial viability through assimilations and integrations in terms of mergers and acquisitions.

How does this impact on competition in Namibia?

The Competition Commission as established by the Competition Act, 2003 considers competitive pricing and wider product choices as a form of consumer protection for the Namibian consumer. It is in this regard that it necessitates that the commission informs the consumer on the recent food price increases and that it is not directly attributed to the infant industry protection measures as a policy instrument by the Ministry of Trade and Industry. The commission is considerate of higher price increases, which have an impact on consumer welfare in Namibia. Consumers are informed that the Namibia Competition Commission has announced measures as part of ensured micro-economic stability to monitor prices of selected consumer products to assess their pricing trends in terms of input costs, margins, retail pricing strategies and to inform the Ministry of Trade and Industry as competition advisor on such pricing formations. The constitutional dispensation of Namibia is such that prices are set in the context of the market economy in accordance to demand and supply conditions. The role of the commission is to ensure that consumers are not overcharged for items such as poultry, meat, and dairy products.

Where excessive pricing would be proven in court, the commission would be in a position to penalize businesses and companies that are engaged in predatory pricing i.e. charging so low as to drive other businesses such as SMEs out or excessive pricing i.e. charging so high, way above to make super normal profits at the expense of consumers.

The commission also wants to ensure that members of the public understand their consumer rights, as well as the avenues of recourse available to them and the infant industry protections granted that are in the best interests of industrial development and manufacturing expansion. There is further evidence of higher propensity of mergers in the retail and commercial businesses in Namibia, mainly from South Africa. Such mergers could impact on further consolidation of the food sector, pushing the dominance and monopolisation of certain firms further.