Search News Results

CSTD 2015-2016 Inter-Sessional Panel: Smart Cities and Infrastructure and Foresight for Digital Development

Opening statement by Taffere Tesfachew, Acting Director, Division on Technology and Logistics; Director, Division on Africa, Least Developed Countries and Special Programmes, UNCTAD, at the CSTD 2015-2016 Inter-Sessional Panel

It gives me a great pleasure to welcome you – on behalf of UNCTAD – to the CSTD Inter-Sessional Panel meeting to discuss – among others – two important and timely issues: “Smart Cities and Infrastructure” and “Foresight for Digital Development”. This Inter-Sessional Panel is timely because it comes at a critical juncture in the international development discourse – and a time of transition from the Millennium Development Goals (MDGs) to the much broader 2030 Agenda for Sustainable Development and the much more ambitious Sustainable Development Goals (SDGs). A succession of international Conferences and agreements during 2015 has created a new global development agenda. In September, world leaders adopted a comprehensive and ambitious 2030 Agenda for Sustainable Development at the United Nations Sustainable Development Summit, committing themselves and the international community to ending poverty in all its forms and dimensions. In July, they adopted the Addis Ababa Action Agenda, which complements and supports the means of implementation for the 2030 Agenda. In December 2015, at the 21st Conference of the Parties to the United Nations Framework Convention on Climate Change, they agreed, with similar ambition, to limit global warming to 2°C and pursue efforts to limit it to 1.5°C.

The outcomes of all these agreements have – both direct and indirect – implications for many of the issues that the CSTD will be addressing in the coming years, including in the coming three days here in Budapest. When viewed from a broader perspective, collectively the outcomes are the result of a culmination of a half century of profound changes in the world economic order which have at times supported, and at times hindered, the efforts of developing countries to achieve a more prosperous and dignified life for their populations. Sustainable and inclusive development remains a challenge for many countries and communities; and meeting this challenge will require integrating the economic, social, technological and environmental dimensions of sustainable development, nationally and globally, and creating an enabling environment for inclusive and sustainable development.

In an increasingly more complex and inter-dependent world, Science, Technology and Innovation (STI) are key drivers of the inclusive and sustainable development to which the 2030 Agenda aspires. As a UN Commission – responsible for articulating the nexus between STI and development and as a subsidiary body of the ECOSOC with its universal membership – the CSTD has a critical role to play in defining and supporting the science and technology-related actions which flow from recent global agreements. This is a momentous responsibility – but also in line with the overall mandates and Terms of Reference of the CSTD, which was established to provide the ECOSOC and General Assembly with policy advice on the implications of Science and Technology for sustainable development. Above all, the CSTD could serve as a multilateral forum for sharing experiences and best practices in the application of STI for achieving the SDGs. There is no doubt that STI is inextricably linked to the outcome of the 2030 Agenda for sustainable development and the successful conclusion of the SDGs. In this respect, I wish to highlight four points:

First, practically all major international agreements completed in last year or so have recognized the critical role of STI in the development process – and this is reflected in their action plans and the policy measures proposed. For example, goal 17 of the SDGs identifies technology as one of the important means of implementing and achieving the SDGs by 2030. Similarly, the Financing for Development Conference in Addis Ababa in July 2015 and its outcome – the Addis Ababa Action Agenda (AAAA) – have singled out technology for special emphasis in the new Global Development Partnership for advancing the universal development goals. In fact, the first outcome from the Addis Ababa Conference to be implemented was related to technology. I am referring – of course – to the establishment of the United Nations Interagency Task Team on STI for the SDGs and the launching of the Technology Facilitation Mechanism (TFM). How the TFM will function and its role vis-à-vis the CSTD may require further discussion. Nevertheless, its establishment signals the recognition by the international community of the critical role of technology in achieving the new and more ambitious and universal development goals. In the same vein, the recently adopted Paris Agreement on Climate Change has also underlined the centrality of STI in the mitigation and adaptation efforts.

My second point is to highlight that – regardless of the official declaration of the importance of STI – given the diverse, multidimensional, ambitious and absolute nature of the SDGs – it will be practically impossible to achieve all these goals successfully by 2030 without the development and appropriate application of STI. With the vision of “no one must be left behind”, the 2030 Agenda has raised the bar and demands unprecedented actions and efforts. It is clear that in the new global development agenda, islands of prosperity surrounded by poverty, injustice, climate change and environmental degradation are viewed as neither sustainable nor acceptable. It is no longer enough to reduce poverty by half – as envisaged by MDGs – we must now eradicate it totally and everywhere – while ensuring availability of water and sanitation for all, ensuring access to affordable and reliable energy for all, reducing inequality within and among countries, making cities and human settlements inclusive, resilient and sustainable, and so on. For many developing countries, such ambitious goals will be practically impossible to achieve in 15 years without effective and widespread application of technology and innovative ideas. From recent experience, we know already – that new technologies and innovations can transform economies and improve the living standards of many people within a short period. For example – information and communication technologies have had major macro- and micro-level impacts in many low-income economies, especially with increasing application of mobile phones and the internet to find solutions to the challenges facing the poor and marginalized communities. Other technologies, such as synthetic biology and recent advances in gene editing technology equally hold promises for addressing key challenges in developing countries, such as food security, improvement of agricultural productivity and health care. The development of renewable energy technology is another area where poor countries will be able to develop adaptation and mitigation strategies for climate change while, at the same time, decoupling production from negative environmental impacts. These are only a few examples, but as many of you know, the achievement and sustainability of many of the goals in the next fifteen years will not happen without active – in some cases – extensive application of technologies.

The third point concerns the issue of “inclusiveness”, which is a one of the critical criteria of achieving the SDGs along with “sustainability”. The point is – in implementing the Goals – it is equally important to ensure that the “inclusiveness” principle also applies to the dissemination and application of technologies and new innovative ideas to improve productivity and promote social development. This, in effect, means that efforts must be made to apply STI in an ‘inclusive’ manner and ensuring that existing technological gaps do not leave some countries and communities behind. The two major topics addressed in this Inter-Sessional Panel namely “Smart Cities and Infrastructure” and “Foresight for Digital Development” provide excellent examples of the types of new technologies and innovations that are indispensable for advancing the sustainable development objective but difficult to access for poor economies where resources are limited, although urbanization in these countries is taking place at a very fast and unsustainable pace and production is dominated by informal activities and low-pay and low-productivity jobs. As you will see in the course of the next three days, smart technologies can contribute to the achievement of goal 11 by making human settlements in urban areas safe, comfortable, resilient and sustainable. A good example, as shown in the draft background paper, is the deployment of smart water meters in Mumbai, India, which are helping to control water supply remotely and reduce portable water waste by as much as 50%.

However, harnessing STI for SDGs requires an enabling environment, in particular the skills, basic infrastructure (both soft and hard), appropriate policies to facilitate technology transfer, a conducive regulatory framework and a domestic productive capacity, which is essential if technology transfer and diffusion is to take place through linkages. The role of CSTD will be critical in articulating the policy measures and actions that developing countries, especially the least developed among them, need to take in order to facilitate technology transfer and the application of STI aimed at meeting the SDGs.

Finally, the trade-off between the benefits and risks of applying STI for achieving SDGs must be assessed carefully. The potential risks of intensifying the technological divide between communities and countries if the development and application STI is not applied judiciously and the potential dangers of creating dependency on technologies that are incompatible to local production capability and resource endowment need to be factored in policy actions that promote STI for implementing SDGs. All these are issues that the CSTD is mandated to address and share its findings and policy recommendations to member States through the General Assembly. Inter-Sessional meetings among experts – such as this one – provide opportunities to address how STI could be made an effective tool to meet the universal goals that all member states of the United Nations agreed to achieve by 2030. As a final note, I wish to reassure you that UNCTAD – as a secretariat of the CSTD – will continue to provide – both the substantive and logistical support – that the Commission requires to discharge its responsibility and become an effective forum for addressing new and emerging issues in the area of STI and its contribution to the collective and global vision of inclusive and sustainable development. I look forward to the discussions in the coming three days.

Thank you for your attention.

A selection of documents/presentations from the meeting is available below.

Related News

tralac’s Daily News selection

The selection: Thursday, 14 January 2016

Two commentaries on US trade policy, by Ambassador Michael Froman:

Since President Obama took office, the United States has brought 20 enforcement actions at the World Trade Organization, winning every one that has been brought to closure. Last year, the United States saw victories in a wide range of trade enforcement cases that benefit American industries, including high-tech steel producers, farmers, rare earth manufacturers, and other exporters, while launching cases and dispute settlement consultations to protect American manufacturers and exporters.

I’d like to focus on what yet another group has said about TPP. This is a group that you might not normally associate with trade policy, but it’s a group whose advice we often turn to when the stakes couldn’t be higher. Our national security and foreign policy experts - U.S. Secretaries of Defense and State, National Security Advisors, Generals, Admirals, and others - are all saying that TPP is a strategic imperative. They recognize that trade agreements, first and foremost, must stand on their economic merits. They appreciate that the foundation of US national security is a strong economy and that by driving growth and keeping America competitive, TPP will strengthen that foundation. But they also appreciate that TPP is strategic in the broader sense of the word. TPP is the economic centre piece of our rebalancing to Asia and a concrete manifestation of America’s ability to show global leadership. Right now, this critical region is in flux.

Released today: 2016 World Development Report - Digital Dividends (World Bank)

Digital technologies can promote inclusion, efficiency, and innovation. More than forty percent of adults in East Africa pay their utility bills using a mobile phone. There are eight million entrepreneurs in China - one-third of them women - who use an e-commerce platform to sell goods nationally and export to 120 countries. India has provided unique digital identification to nearly one billion people in five years, and increased access and reduced corruption in public services. And in public health services, simple SMS messages have proven effective in reminding people living with HIV to take their lifesaving drugs. To deliver fully on the development promise of a new digital age, the World Bank suggests two main actions: closing the digital divide by making the internet universal, affordable, open, and safe; and strengthening regulations that ensure competition among business, adapting workers’ skills to the demands of the new economy, and fostering accountable institutions - measures which the report calls analog complements to digital investments.

Forthcoming event: African Data Consensus and the implementation roadmap, role of NSOs (UNECA)

Expected outcomes: a common understanding (position) on the concept of data revolution and what it means for Africa; a consensus on the role of NSOs in its implementation; an action plan for implementing the Data Revolution in Africa based on the principles set in the African Data Consensus, SHaSA and the African Charter on Statistics and, an opportunity to prepare for the United Nations Statistical Commission in March 2016. [Addis Ababa, 20-22 January]

The ‘International trade and economic globalisation statistics’ session for forthcoming UN Statistical Commission (8-11 March): Report of the Secretary-General on international trade and economic globalization statistics, Report of the Inter Agency Task Force on international trade statistics

From global SDGs to country policymaking (World Bank)

To kick-start needed country-level analysis, the World Bank recently issued the volume 'Trajectories for Sustainable Development Goals: framework and country applications', co-authored by the authors of this blog. This framework, which is simple and transparent, may be used to analyze the likely progress in SDGs and their determinants, and to discuss policy and financing options to accelerate progress. In the volume, selected parts of the framework and indicators are applied to 10 countries – Ethiopia, Jamaica, Kyrgyzstan, Liberia, Nigeria, Pakistan, Peru, Philippines, Senegal and Uganda – a group that is diverse in terms of initial conditions and future prospects.

Kenya: Yuan clearing house to boost Sino-Africa trade (Shanghai Daily)

State-owned National Bank of Kenya said its Chinese yuan clearing house which was launched in Nairobi last year will help to boost Sino-Kenya trade. NBK's Managing Director Munir Ahmed told Xinhua in Nairobi that the clearing house will make it easier for Kenyan businessmen to access the Chinese currency. The Chinese Embassy in Nairobi estimates that there are over 200 companies operating in Kenya, a factor which influenced the Central Bank of Kenya to include the yuan as a reserve currency given the growing trade between Kenya and China.

Related: China's imports from Africa shrank nearly 40% in 2015: it could get really painful for these 10 countries (M&G), China’s imports from Africa plummet in 2015 (The Zimbabwean), China GDP guide: how the data is sliced and what's new this time (Bloomberg)

The road ahead for EAC regional competition regime (CUTS Africa)

The report highlights: the status of the competition related policy environment in the EAC Partner States; the areas, which need close scrutiny by the national competition authorities; the provisions of the EAC competition law and how it can be used to deal with such anti-competitive practices. The report further identifies the challenges facing the implementation of the EAC Competition Policy and Law at both the national and regional-level, respectively, and proposes recommendations that can be deployed to mitigate these challenges in ensuring that we have well-functioning competitive markets in the EAC region.

Great Lakes region: private sector investment conference (SADC)

Following the Peace, Security and Cooperation Framework Agreement, signed by 13 countries of the region, the overall objective of the Great Lakes Private Sector Investment Conference (Kinshasa, 24-25 February) is to mobilize investments for the transformation of the region, catalyze regional projects that significantly increase employment, improve productivity, and expand the connection of the region to value markets, including intra-regional trade, and to promote shared prosperity across countries while yielding significant returns on investments. The specific objectives are to:

Egypt to host African investment forum (GNN Liberia)

Next month (20-21 February) Egypt will host 'Africa 2016', the first international business and investment forum of its kind. This is an Africa to Africa investment forum aimed at strengthening business ties within Africa, both at a business and presidential level. The Forum will be opened by the President of Egypt, H.E. Abdel Fateh El-Sisi, and a number of African Heads of State are also expected at the forum.

Botswana: Annual review of the Pula basket of currencies (Botswana Government)

Following the annual review of the Pula basket in 2015, and in pursuant to Section 21 of the Bank of Botswana Act, His Excellency the President has approved the Honourable Minister of Finance and Development Planning's recommendation to: maintain the Pula basket weights at 50% South African rand and 50% SDR and change the rate of crawl from zero to an upward crawl of 0.38% per annum, effective 1st January, 2016.

Future of SA not all doom and gloom (Business Day)

SA faces many of the same global challenges as other developing markets — including lower commodity prices and the risk of rising interest rates — but has reason to be upbeat, says global intelligence consultancy, the Oxford Business group. In its SA report for 2016, the group says the future for inclusive growth in the continent’s most sophisticated economy is still seen as "encouraging" compared with other Brics nations Brazil, Russia, and China — but excluding India — and big emerging market Turkey. According to the report, SA needs to diversify its exports beyond the European Union and China, especially into the rest of Africa. [Read the Oxford Business Group 'South Africa 2016' report online]

Related: South Africa to expand international market access: minister (Xinhua), State should ‘intervene decisively’ to lift economic growth, Radebe says (Business Day), Daniel Mminele, Deputy Governor of the SA Reserve Bank: speech to the European Economics & Financial Centre

November traffic demand (IATA)

African airlines experienced their fifth consecutive month of positive traffic growth in November, posting a 12.2% rise compared to November 2014. However, the trend for the year-to-date so far remains weak, with growth of just 1.3% reflecting adverse economic developments in parts of the continent, including in Nigeria, which is highly reliant on oil revenues. Over the past few months, exports from Africa have held up better than they did earlier in 2015, and this could be helping boost international air travel on the region’s carriers. Capacity rose 9.8% and load factor rose 1.5 percentage points to 65.1%.

Egypt's Suez Canal saw more ships, less US-dollar revenues in 2015 (Ahram)

Despite seeing an increase in traffic, Egypt’s Suez Canal saw a drop in revenues in 2015, registering $5.17bn compared to $5.46bn in the previous year. Last year, the canal, which links the Mediterranean and the Red Sea, saw the passage of 17,483 ships compared to 17,148 in 2014, the statement added.

More bad news for ocean trade (Business Standard)

The Baltic Dry Index (BDI) slid to a level of 402 on Wednesday, a new low, and this might stop much of trade across the Indian Ocean and Asia-Pacific market, say observers. There could be a strong aversion, for instance, to long-term deals. The BDI is an economic indicator issued daily by the London-based Baltic Exchange.

Swaziland/Mozambique port: update (Club of Mozambique)

The proposed $2.14 billion Swaziland/Mozambique port earmarked to be constructed at Mlawula in north-eastern Swaziland, is in its initial stages of construction, local media report here Wednesday. The project aimed at creating jobs for 10,000 people has started despite the fact that Swaziland has not yet received approval from the Mozambican government for the construction of a 26 kilometre canal that will connect the Mozambican sea to Mlawula (at 15 to 20 hectares of land).

UN forum on ethics for development (UN News Centre)

The universal inclusiveness of the 2030 Agenda for Sustainable Development is an ethical imperative, UN Deputy Secretary-General Jan Eliasson told a forum for UN Member States today on ethics for development. “Fundamental principles that underpin the new goals are interdependence, universality and solidarity. They should be implemented by all segments of all societies, working together. No-one must be left behind. People who are hardest to reach should be given priority,” he said.

Currency manipulation – was the Metical overvalued? (SPEED)

Egypt: Western Union transfers from Egypt to China curbed amid dollar shortage (Reuters)

Nigeria: CBN forex policy responsible for declining production, says manufacturer (ThisDay)

Obinna Chima: 'IMF's prescriptions and Nigeria's challenges' (ThisDay)

Offshore West Africa confirms partnership with UK Trade & Investment (ThisDay)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

Digital technologies: Huge development potential remains out of sight for the four billion who lack internet access

While Digital Technologies Have Spread Fast Worldwide, Their Digital Dividends Have Not

A new World Bank report says that while the internet, mobile phones and other digital technologies are spreading rapidly throughout the developing world, the anticipated digital dividends of higher growth, more jobs, and better public services have fallen short of expectations, and 60 percent of the world’s population remains excluded from the ever-expanding digital economy.

According to the new ‘World Development Report 2016: Digital Dividends,’ authored by Co-Directors, Deepak Mishra and Uwe Deichmann and team, the benefits of rapid digital expansion have been skewed towards the wealthy, skilled, and influential around the world, who are better positioned to take advantage of the new technologies. In addition, though the number of internet users worldwide has more than tripled since 2005, four billion people still lack access to the internet.

“Digital technologies are transforming the worlds of business, work, and government,” said Jim Yong Kim, President of the World Bank Group. “We must continue to connect everyone and leave no one behind because the cost of lost opportunities is enormous. But for digital dividends to be widely shared among all parts of society, countries also need to improve their business climate, invest in people’s education and health, and promote good governance.”

Although there are many individual success stories, the effect of technology on global productivity, expansion of opportunity for the poor and middle class, and the spread of accountable governance has so far been less than expected. Digital technologies are spreading rapidly, but digital dividends – growth, jobs and services – have lagged behind.

“The digital revolution is transforming the world, aiding information flows, and facilitating the rise of developing nations that are able to take advantage of these new opportunities,” said Kaushik Basu, World Bank Chief Economist. “It is an amazing transformation that today 40 percent of the world’s population is connected by the internet. While these achievements are to be celebrated, this is also occasion to be mindful that we do not create a new underclass. With nearly 20 percent of the world’s population unable to read and write, the spread of digital technologies alone is unlikely to spell the end of the global knowledge divide.”

Digital technologies can promote inclusion, efficiency, and innovation. More than forty percent of adults in East Africa pay their utility bills using a mobile phone. There are eight million entrepreneurs in China – one-third of them women – who use an e-commerce platform to sell goods nationally and export to 120 countries. India has provided unique digital identification to nearly one billion people in five years, and increased access and reduced corruption in public services. And in public health services, simple SMS messages have proven effective in reminding people living with HIV to take their lifesaving drugs.

To deliver fully on the development promise of a new digital age, the World Bank suggests two main actions: closing the digital divide by making the internet universal, affordable, open, and safe; and strengthening regulations that ensure competition among business, adapting workers’ skills to the demands of the new economy, and fostering accountable institutions – measures which the report calls analog complements to digital investments.

Digital development strategies need to be much broader than information and communication technology (ICT) strategies. To reap the greatest benefits, countries must create the right environment for technology: regulations that facilitate competition and market entry, skills that enable workers to leverage the digital economy, and institutions that are accountable to people. Digital technologies can, in turn, accelerate the pace of development.

Investing in basic infrastructure, reducing the cost of doing business, lower trade barriers, facilitating entry of start-ups, strengthening competition authorities, and facilitating competition across digital platforms are some of the measures suggested in the World Development Report that can make businesses more productive and innovative. In addition, while basic literacy remains essential for children, teaching advanced cognitive and critical thinking skills and foundational training in advanced, technical ICT systems will be key as the internet spreads. Teaching technical skills early and exposing children to technology promotes ICT literacy and influences career choices.

Digital technologies can transform our economies, societies and public institutions, but these changes are neither assured nor automatic, cautions the report. Countries that are investing in both digital technology and its analog complements will reap significant dividends, while others are likely to fall behind. Technology without a strong foundation risks creating divergent economic fortunes, higher inequality and an intrusive state.

Over the last decade, the World Bank Group has invested a total US$12.6 billion in ICTs.

Related News

South Africa to expand international market access: minister

The South African government is committed to intensifying efforts to expand international market access for its agricultural commodities, Minister of Agriculture Forestry and Fisheries Senzeni Zokwana said Thursday.

The minister was speaking at a meeting in Pretoria with industry stakeholders affected by trade related to exports of poultry, beef and pork meat from the United States to South Africa.

Zokwana convened the meeting to brief the affected agricultural industry stakeholders on the outcomes of the recent intensive negotiations around South Africa's eligibility to the Africa Growth and Opportunity Act (AGOA).

The minister said the objective of the meeting was to ensure that all affected stakeholders were of the same understanding in respect to the recent negotiations between South Africa and the U.S. on key areas related to the importation of poultry, beef and pork from the U.S. to South Africa, their outcomes and the proclamation made by U.S. President Barack Obama.

The White House issued a presidential proclamation on Monday that South Africa's trade benefits on agricultural goods under the AGOA will be suspended if American poultry is not allowed into South Africa by March 15.

Zokwana stressed the importance of maintaining a close partnership between his ministry and its stakeholders not only during this time but as the norm.

The minister committed his department to ensuring that they will again work tirelessly to make sure that the deadline is met.

SA Minister of Trade and Industry Rob Davies announced on January 7 that his government had concluded negotiations with the U.S. on the final barriers to the import of American poultry into South Africa.

But now the U.S. government says it is testing the system to make sure the meat will be available on store shelves in South Africa.

The office of the U.S. trade representative says if the remaining benchmark – the entry of U.S. poultry into South Africa under the agreed-upon conditions – is met before March 15, Obama will be able to consider a revocation of the proclamation before suspension takes effect.

Under the deal reached with the U.S. last week, South Africa will import 65, 000 tonnes of U.S. poultry a year.

With regard to pork, South Africa has agreed to permit the unrestricted importation of the shoulder cuts after the U.S. agreed to apply mitigation measures. South Africa has also agreed to import beef from the U.S..

In return, South African agricultural products will continue to enjoy trade preferences for quota and duty-free entry into the U.S.

The March 15 deadline is the second placed on South Africa by the U.S.. In November last year, Obama set December 31 as the deadline for South Africa to conclude the negotiations on opening its markets to poultry, pork and beef from the U.S. or face the risk of losing AGOA benefits.

The two sides allowed negotiations to continue for some more days to resolve outstanding technical issues, particularly highly pathogenic avian influenza and salmonella.

South African had blocked chicken imports from the U.S. because of outbreaks of avian flu in parts of the U.S. and because of concerns about salmonella infection. It has also been citing concerns about diseases in pork and beef to block imports of those products.

SA exported 176 million U.S. dollars worth of agricultural products to the U.S. last year, mainly citrus and wine. South Africa's total exportss amount to 70 billion rand (4.5 billion U.S. dollars) and of these, 25 million rand (about 1.6 billion dollars) are to the U.S. market.

SA has allowed virtually no U.S. chicken, pork or beef imports into the local market for several years, partly through anti-dumping duties and partly through health restrictions.

Last June officials from both sides agreed partly to lift the anti-dumping duties on U.S. chicken imports, to allow a quota of 65,000 tons a year to be imported. This would be subject to several conditions being met. But virtually chicken imports were not allowed into the SA market because of outbreaks of avian flu in parts of the U.S. and because of concerns about salmonella infection.

Although the U.S. renewed the AGOA for another decade last July, Washington said South Africa's participation in AGOA had to undergo out-of-cycle review.

The AGOA, a legislation that was approved by the U.S. Congress in May 2000, is to assist the economies of Sub-Saharan Africa and to improve economic relations between the U.S. and the region. The act provides trade preferences for quota and duty-free entry into the U.S. for certain goods, under certain conditions.

Related News

As oil crashed, renewables attracted record $329 billion

The slump in oil prices that’s brought upheaval and cost-cutting to the traditional energy industry spared renewables such as solar and wind, which raked in a record $329.3 billion of investment last year.

The 4 percent increase in clean energy technology spending from 2014 reflected tumbling prices for photovoltaics and wind turbines as well as a few big financings for offshore wind farms on the drawing board for years, according to research from Bloomberg New Energy Finance released on Thursday.

“These figures are a stunning riposte to all those who expected clean energy investment to stall on falling oil and gas prices,” said Michael Liebreich, founder of the London-based research arm of Bloomberg LP. “They highlight the improving cost-competitiveness of solar and wind power.”

While oil companies such as Exxon Mobil Corp. and Royal Dutch Shell Plc eliminate jobs and curb capital spending to cope with prices that have fallen two-thirds in 18 months, renewables are enjoying a renaissance underpinned by rules designed to curb fossil-fuel emissions damaging the atmosphere.

Fears that low oil prices will continue into 2016 have knocked confidence among oil companies, delaying $380 billion worth of investment in upstream projects, according to analysis by industry consultant Wood Mackenzie Ltd. on Jan. 12. Companies are "going into survival mode" this year with more projects delayed and budgets cut, said Angus Rodger, one of the report’s authors.

Brent crude oil has traded near $30 a barrel this month, down from more than $110 in 2014 as exporters led by Saudi Arabia battled for market share. Coal and natural gas prices have followed, already pushing a handful of producers into bankruptcy. While BNEF has said lower prices may hurt funding for efficiency projects and the spread of electric cars, the main clean energy technologies enjoyed record installations in 2015.

Another “strong year” is in store for renewables in 2016, said Angus McCrone, chief editor at BNEF, stopping short of saying another record will be reached. Balancing that is a potential slip in funding for yieldcos, which drew higher investment in 2015, and a clouded outlook for offshore wind in its biggest market.

“There is a lot of uncertainty on how strong U.K. support for offshore wind is going to be,” McCrone said. “It is conditional on costs coming down, and I think that will happen, but it’s hard to say how many will be supported."

China remained the biggest market for renewables, increasing investment 17 percent to $110.5 billion. That’s almost double the $56 billion invested in the U.S., which was second in the BNEF rankings. The strength of the dollar helped boost the value of investment.

In India, funding for clean energy rose 23 percent to $10.9 billion, and new markets including Mexico, Chile and South Africa attracted tens of billions of dollars. Brazil bucked the trend with a 10 percent drop to $7.5 billion.

“Wind and solar power are now being adopted in many developing countries as a natural and substantial part of the generation mix,” Liebreich said. “They can be produced more cheaply than often high wholesale power prices. They reduce a country’s exposure to expected fossil fuel prices. And above all, they can be built very quickly to meet unfulfilled demand for electricity.”

New wind and solar power accounted for about half of all new generation last year. Around 64 gigawatts of new wind power and 57 gigawatts of new photovoltaics was added, representing an increase of 30 percent from to 2014.

Investment was driven mainly by large-scale projects, including a number of major offshore wind farms. The U.K.’s 580 megawatt Race Bank offshore wind farm was the largest project financed last year, attracting $2.9 billion, followed closely by the $2.3 billion Galloper offshore wind farm, also in the U.K.

U.K. Record

As a result, the U.K. was by far Europe’s strongest market, despite Prime Minister David Cameron’s effort to roll back incentives for the industry. Renewables investment in the U.K. rose 24 percent to a record $23.4 billion from 2014, according to BNEF.

The U.K.’s rooftop solar power market grew to $1.8 billion, putting the U.K. in fourth place for investment in solar installations smaller than one megawatt, behind Japan, the U.S. and China.

Globally, rooftop solar installations like the ones championed by SolarCity Corp. were another big winner, reaping a 12 percent increase to $67.4 billion.

Europe recorded its weakest year since 2006, in part because of slower activity in Germany after the government cut subsidies and revealed plans for a new auctioning system in 2017. Investment in the continent’s biggest economy fell by 42 percent to $10.6 billion. The continent as a whole suffered an 18 percent drop to $58.5 billion.

Clean energy defies fossil fuel price crash to attract record $329bn global investment in 2015

2015 was also the highest ever for installation of renewable power capacity, with 64GW of wind and 57GW of solar PV commissioned during the year, an increase of nearly 30% over 2014.

Clean energy investment surged in China, Africa, the US, Latin America and India in 2015, driving the world total to its highest ever figure, of $328.9bn, up 4% from 2014’s revised $315.9bn and beating the previous record, set in 2011 by 3%.

The latest figures from Bloomberg New Energy Finance show dollar investment globally growing in 2015 to nearly six times its 2004 total and a new record of one third of a trillion dollars (see chart), despite four influences that might have been expected to restrain it.

These were: further declines in the cost of solar photovoltaics, meaning that more capacity could be installed for the same price; the strength of the US currency, reducing the dollar value of non-dollar investment; the continued weakness of the European economy, formerly the powerhouse of renewable energy investment; and perhaps most significantly, the plunge in fossil fuel commodity prices.

Over the 18 months to the end of 2015, the price of Brent crude plunged 67% from $112.36 to $37.28 per barrel, international steam coal delivered to the north west Europe hub dropped 35% from $73.70 to $47.60 per tonne. Natural gas in the US fell 48% on the Henry Hub index from $4.42 to $2.31 per million British Thermal Units.

Source: Bloomberg New Energy Finance

Michael Liebreich, chairman of the advisory board at Bloomberg New Energy Finance, said: “These figures are a stunning riposte to all those who expected clean energy investment to stall on falling oil and gas prices. They highlight the improving cost-competitiveness of solar and wind power, driven in part by the move by many countries to reverse-auction new capacity rather than providing advantageous tariffs, a shift that has put producers under continuing price pressure.

“Wind and solar power are now being adopted in many developing countries as a natural and substantial part of the generation mix: they can be produced more cheaply than often high wholesale power prices; they reduce a country’s exposure to expected future fossil fuel prices; and above all they can be built very quickly to meet unfulfilled demand for electricity. And it is very hard to see these trends going backwards, in the light of December’s Paris Climate Agreement.”

Looking at the figures in detail, the biggest piece of the $328.9bn invested in clean energy in 2015 was asset finance of utility-scale projects such as wind farms, solar parks, biomass and waste-to-energy plants and small hydro-electric schemes. This totalled $199bn in 2015, up 6% on the previous year.[1]

The biggest projects financed last year included a string of large offshore wind arrays in the North Sea and off the coast of China. These included the UK’s 580MW Race Bank and 336MW Galloper, with estimated costs of $2.9bn and $2.3bn respectively, Germany’s 402MW Veja Mate, at $2.1bn, and China’s Longyuan Haian Jiangjiasha and Datang & Jiangsu Binhai, each of 300MW and $850m.

The biggest financing in onshore wind was of the 1.6GW Nafin Mexico portfolio, for an estimated $2.2bn. For solar PV, it was the Silver State South project, at 294MW and about $744m, and for solar thermal or CSP, it was the NOORo portfolio in Morocco, at 350MW and around $1.8bn. The largest biomass project funded was the 330MW Klabin Ortiguera plant in Brazil, at about $921m, and the largest geothermal one was Guris Efeler in Turkey, at 170MW and an estimated $717m.

After asset finance, the next largest piece of clean energy investment was spending on rooftop and other small-scale solar projects. This totaled $67.4bn in 2015, up 12% on the previous year, with Japan by far the biggest market, followed by the US and China.

Preliminary indications are that, thanks to this utility-scale and small-scale activity, both wind and solar PV saw around 30% more capacity installed worldwide in 2015 than in 2014. The wind total for last year is likely to end up at around 64GW, with that for solar just behind at about 57GW. This combined total of 121GW will have made up around half of the net capacity added in all generation technologies (fossil fuel, nuclear and renewable) globally in 2015.

Public market investment in clean energy companies was $14.4bn last year, down 27% from 2014 but in line with the 10-year average. Top deals included a $750m secondary share issue by electric car maker Tesla Motors, and a $688m initial public offering by TerraForm Global, a US-based ‘yieldco’ owning renewable energy projects in emerging markets.

Venture capital and private equity investors pumped $5.6bn into specialist clean energy firms in 2015, up 17% on the 2014 total but still far below the $12.2bn peak of 2008. The biggest VC/PE deal of last year was $500m for Chinese electric vehicle company NextEV.

There was $20bn of asset finance in clean energy technologies such as smart grid and utility-scale battery storage, representing an 11% rise on 2014, the latest in an unbroken series of annual increases over the past nine years. The final category of clean energy investment, government and corporate research and development spending, totaled $28.3bn in 2015, up just 1%. This figure provides a benchmark for any surge in spending in the wake of announcements at COP21 in Paris by consortia of governments and private investors, led by Bill Gates and Mark Zuckerberg.

National trends

China was again by far the largest investor in clean energy in 2015, increasing its dominance with a 17% increase to $110.5bn, as its government spurred on wind and solar development to meet electricity demand, limit reliance on polluting coal-fired power stations and create international champions.

Second was the US, which invested $56bn, up 8% on the previous year and the strongest figure since the era of the ‘green stimulus’ policies in 2011. Money-raising by quoted ‘yieldcos’, plus solid growth in investment in new solar and wind projects, supported the US total.

Europe again saw lower investment in 2015, at $58.5bn, down 18% on 2014 and its weakest figure since 2006. The UK was by far the strongest market, with investment up 24% to $23.4bn. Germany invested $10.6bn, down 42% on a move to less generous support for solar and, in wind, uncertainty about how a new auction system will work from 2017. France saw an even bigger fall in investment, of 53% to $2.9bn.

Brazil’s clean energy investment slipped 10% to $7.5bn in 2015, while India’s gained 23% to $10.9bn, the highest since 2011 but a far cry for the figures needed to implement the Modi government’s ambitious plans. Japan saw investment rise 3% to $43.6bn, on the back of a continuing PV boom. In Canada, clean energy investment fell 43% to $4.1bn, while in Australia, it edged up 16% to $2.9bn.

A number of “new markets” together committed tens of billions of dollars to clean energy last year. These include Mexico ($4.2bn, up 114%), Chile ($3.5bn, up 157%), South Africa ($4.5bn, up 329%) and Morocco ($2bn, up from almost zero in 2014).

Africa and the Middle East are two regions with big potential for clean energy, given their growing populations, plentiful solar and wind resources and, in many African countries, low rates of electricity access. In 2015, these regions combined saw investment of $13.4bn, up 54% on the previous year.

[1] Large hydro-electric projects of more than 50MW are not included in this asset finance figure or in total clean energy investment. However, BNEF’s estimate is that $43bn of large hydro projects reached “final investment decision” worldwide in 2015.

Note: Following minor revisions to prior year totals to reflect additional deal information, Bloomberg New Energy Finance’s historical series for global clean energy investment is: $61.9bn in 2004, $88bn in 2005, $128.3bn in 2006, $174.9bn in 2007, $205.6bn in 2008, $207.3bn in 2009, $273.7bn in 2010, $318.3bn in 2011, $297bn in 2012, $271.9bn in 2013, $315.9bn in 2014 and $328.9bn in 2015.

Related News

China’s imports from Africa plummet in 2015

China’s imports from Africa fell nearly 40 percent last year, officials said Wednesday, as low commodity prices and slowing growth in the Asian giant hit trade.

Imports from the continent fell to 440 billion yuan, some 38 percent lower than in 2014, China’s Customs administration said.

Natural resources from Africa such as iron ore and oil have helped fuel China’s economic boom, and it became the continent’s largest trade partner in 2009, giving it growing diplomatic influence.

But growth in the world’s second-largest economy has slowed to its lowest since the aftermath of the global financial crisis, punishing world prices for commodities – the bedrock of African exports.

Economists say Chinese growth is becoming less dependent on heavy industry, further hitting demand for raw materials.

However, Chinese exports to Africa rose by about 4 percent to reach 670 billion yuan, officials said.

Oil exporters are expected to be hit especially hard. China said its imports from Nigeria slumped more than 50 percent by value last year.

Beijing said in November its direct investment in Africa dropped “more than 40 percent” to about $1.2 billion in the first six months of the year.

China’s President Xi Jinping announced $60 billion of assistance and loans for Africa last month, signalling ongoing commitment to the continent despite the investment drop.

Related News

From global SDGs to country policymaking

What should countries do to accelerate progress on the UN Sustainable Development Goals (SDG) agenda?

The agenda, adopted by the world’s leaders in September is very comprehensive: its 17 goals and 169 targets cover economic, social, and environmental dimensions of development. It is also very ambitious: the general spirit of the targets under each goal is that everyone should benefit in full from the fruits of development across all areas (be it electricity, health, or education) and that, accordingly, no one should be left behind. Inspired by these ambitions, individual countries now face the tough challenge of translating this agenda into feasible (but still ambitious) development plans and identifying policies that reflect their initial conditions and priorities.

To kickstart needed country-level analysis, the World Bank recently issued the volume Trajectories for Sustainable Development Goals: Framework and Country Applications, coauthored by the authors of this blog.[1] This framework, which is simple and transparent, may be used to analyze the likely progress in SDGs and their determinants, and to discuss policy and financing options to accelerate progress. In the volume, selected parts of the framework and indicators are applied to 10 countries – Ethiopia, Jamaica, Kyrgyzstan, Liberia, Nigeria, Pakistan, Peru, Philippines, Senegal and Uganda – a group that is diverse in terms of initial conditions and future prospects.

The analysis is done from a cross-country perspective, with the outcomes for each country assessed relative to what is typical for countries at the same capacity level, proxied by income per capita. It offers a practical starting point for a discussion of how policies and financing should be designed to speed up development outcomes. The framework achieves this by:

-

benchmarking recent outcomes for SDG target indicators and the factors (including policies) that influence them – how well is a country doing compared to other countries at similar levels of per-capita incomes?

-

projecting 2030 outcomes for selected indicators (when the association between GNI per capita and an indicators is deemed sufficiently strong) – under current trends and given expected growth, what are likely achievements for SDG indicators by 2030?; and

-

assessing options for accelerated progress – what can a country and its government do to increase fiscal space for the SDG agenda and raise the effectiveness of its policies?

What are the next steps? This cross-country approach is useful to benchmark current achievements, to project likely developments, and as an input into detailed country strategies. Countries need to consider in-depth country-specific knowledge, prioritize and sequence their efforts. As part of this, it is important to strike a balance between steps to support immediate growth accelerations and investments in education and other areas that only can promise payoffs over the long haul.

The cross-country approach limits the analysis to what is available in cross-country databases. While the database underlying the framework contains nearly 300 indicators, many of these are second best options; and data exist only for a minority of the 169 targets that are identified. Hence, our work echoes the urgent need to improve within- and cross-country databases. The UN report A World That Counts: Mobilising the Data Revolution for Sustainable Development provides key recommendations for this urgent call of action.

[1] The work was sponsored by the office of Mahmoud Mohieldin, the World Bank Group President's Special Envoy for Millennium Development Goals.

Related News

Yuan clearing house to boost Sino-Africa trade: official

State-owned National Bank of Kenya (NBK) said its Chinese yuan clearing house which was launched in Nairobi last year will help to boost Sino-Kenya trade.

NBK’s Managing Director Munir Ahmed told Xinhua in Nairobi that the clearing house will make it easier for Kenyan businessmen to access the Chinese currency.

“It is now much more convenient for importers to get Chinese Yuan,” Ahmed said during a ceremony where National Bank and Airtel signed a partnership agreement.

Under the agreement National Bank account holders will be able to access their funds using the Airtel mobile platform.

National Bank is currently one of the banks in Kenya that offers the Chinese currency.

Ahmed said that their service reduces the need for the business community trading with China to use financial intermediaries.

“As a result it reduces the cost of transactions of Sino-Kenya trade,” he said.

Experts say the clearing house could boost trade between the two countries by easing commercial transactions as Kenyan exporters normally have payments processed through a lengthy process that involves physically sending Chinese payment cheques back to the country for clearance and payment.

However, with a clearing house, the cheques could be processed locally through an agreement between the two central banks thus expediting payments and easing the cost trade.

Last year, the Chinese Yuan was included into the International Monetary Fund’s (IMF) basket of currencies that includes the U.S. dollar and the Euro.

One of the key priorities of the National Bank is to tap into the growing demand for the Chinese yuan that is fueled by expanding Chinese presence in Kenya. Ahmed said that China is a global leader in international trade.

“Therefore the easy access of the Chinese Renminbi will also help Kenyans to access the global value chains,” he said.

National Bank Director Business Development Yao Sandra said that there is an expanding Chinese community in Kenya.

“They now find it convenient to access the Chinese yuan while in Kenya,” Yao said.

She said that when Kenya traders land in China, they are now able to conduct business immediately.

National Bank, which is owned partly by the government, plans to take members of its business club to this year’s Canton Trade fair.

Yao said the demand for yuan has especially increased among Kenyans heading to China for business trips and holiday goers.

“Business is brisk and the yuan has brought value to our customers. We are receiving new customers daily and the Chinese Banking Unit has experienced the most significant growth in the bank,” Yao said.

Yao said the volume of transactions has made direct shilling to yuan business deals less expensive and bothersome by-passing the dollar.

“We have sufficient reserves to cater for the influx of customers. The service is also significant to the Chinese nationals who need to deal directly in yuan,” Yao said.

Kenyan traders prefer going through the yuan transaction to settle their obligations because of increased costs and the volatility risks that three currencies expose them to.

The Chinese Embassy in Nairobi estimates that there are over 200 companies operating in Kenya, a factor which influenced the Central Bank of Kenya to include the yuan as a reserve currency given the growing trade between Kenya and China.

More bad news for ocean trade

A fresh plunge on the main global index of the cost of moving major raw materials by sea has potential implications for trade.

The Baltic Dry Index (BDI) slid to a level of 402 on Wednesday, a new low, and this might stop much of trade across the Indian Ocean and Asia-Pacific market, say observers. There could be a strong aversion, for instance, to long-term deals.

The BDI is an economic indicator issued daily by the London-based Baltic Exchange.

“The trade climate is full of insecurity, as charterers are not sure if the price at which they have negotiated is the right low price,” Kiran Kamat, owner of Link Shipping & Management Systems, a leading chartering and shipping company, told Business Standard. “Charterers are unable to take a call, leading to last-minute back out (from deals), even if ship-owners are being flexible.”

The index began falling from early August last year, when China initiated a devaluing of its currency. From a high of 1,222, it has lost two-thirds in five months. Wednesday’s level is a three-decade low; the all-time high of 11,793 was on May 20, 2008. Since then, the index has been volatile, being down for much longer than thought likely.

A charterer might own cargo and employ a broker to find a ship to deliver for a certain price, the freight rate. A charterer might also be a party without a cargo, taking a vessel for a specified period from the owner and then trading the ship to carry cargoes above the hire rate.

“There have been very few inquiries and even of those, most were not firm. Of (every) five inquiries, three have failed,” said a ship owner, on condition of anonymity. “The charterers are fixing rates and then trying to trade the cargo. Freight is low enough but still charterers are not able to sell the cargo.”

The BDI measures a change in transportation cost of raw materials such as metals, ore, coal, grain and fertiliser by sea. The continuous fall since August followed China’s economic data, which set a strong bearish tone for the bulk trade market across the globe. For, China is the world’s largest importer and exporter of several commodities. A slowing in its economy now indicates a grimmer trade climate.

“Interest in fixing freight contracts for a longer period is absolutely absent from the charterers’ side,” said someone from a steel company. “No charterer wants to lock-in freight at a premium to the spot price, as they see little upside over this year. Ship owners might have to consider laying off some of their vessels to stem the slipping freight rates.”

On the India-specific trade scenario, sectoral officials said with coal supply higher in the domestic market, the iron ore export market completely out of the picture due to a long-period ban, and a diminished fertiliser trade, small-size Supramax and large-size Capesize vessels are idle, pushing even the ancillary industries out of a job. The latter caters to Capesize vessels, as these ships need constant maintenance.

“Shipping is a gamble and one cannot say when things will look up. It's all about being optimistic in the business,” say officials in the sector.

Related News

tralac’s Daily News selection

The selection: Wednesday, 13 January 2016

Conference alert: '2016 Conference of Ministers: exploring the synergies between the African and the Global Development Agenda' (UNECA)

The Conference will address the question of how African countries could design and implement effective strategies and policies that will support the promotion and implementation of a common framework for meeting the goals of the Agenda 2030 and 2063. Such strategies should not only focus on promoting high and sustainable long-term growth but also ensure that the benefits of such growth are widely shared in order to reduce poverty and improve the standard of living for all Africans. Furthermore the Ministers will, at the end of their deliberations, offer guidance on mechanisms for the successful execution of a common framework at the national, regional and continental level. [Conference: 27 March - 1 April]

The African Lions: Kenya country case study (UNU-WIDER)

This paper mainly analyses the drivers of economic growth in Kenya and the linkages to the labour market dynamics, with a focus on population growth, its structure, and the prospects of reaping a demographic dividend. This is in recognition that Kenya, as the ninth largest economy in Africa and the fourth largest in sub-Saharan Africa and with a locational advantage, presents some policy lessons and challenges that can boost its capacity for growth and take advantage of its location and the policy environment to drive growth in the region. [The authors: Mwangi S. Kimenyi, Francis M. Mwega, Njuguna S. Ndung'u]

Project details: ‘Understanding the African Lions - growth traps and opportunities in six dominant African economies’ (UNU-WIDER)

Profiled documents prepared for UNDP's Executive Board’s First regular session 2016: Draft country programme documents for Ethiopia 2016-2020, Tanzania 2016-20121

Africa Tourism Monitor 2015: Unlocking Africa’s tourism potential (AfDB)

One of the key findings of the report, as indicated in its introduction, is that the tourism sector in Africa is growing. In 2014, a total of 65.3 million international tourists visited the continent – around 200,000 more than in 2013. Back in 1990, Africa welcomed just 17.4 million visitors from abroad. The sector has therefore quadrupled in size in less than 15 years. According to the World Tourism Organization, Africa’s strong performance in 2014 (up 4%) makes it one of the world’s fastest-growing tourist destinations, second only to Southeast Asia (up 6%). This influx of tourists means more money coming into the continent. Transport infrastructure and services is one of the key constraints limiting growth of the tourism sector. As the report indicates, “Journeys in the African continent are not always seamless”. In fact, it is more difficult – and more expensive – to travel across Africa than to get there from Europe, America or the Middle East. [Download]

Uhuru waives visa fees for children to spur tourism (Business Daily)

Uhuru Kenyatta on Tuesday announced plans to waive visa fees for children under the age of 16 in yet another move aimed at wooing foreign visitors into the country. Kenya currently charges Sh10,200 ($100) for a multiple entry visa and Sh5,100 for single entry tourist visa. The fees apply to all visitors, including children under 16. The official guideline at the Directorate of Immigration and Registration of Persons indicates that all children under 16 require a visa unless they are on the same passport as a parent.

The civil society guide to regional economic communities in Africa (AfriMAP)

As regional integration gains momentum, there is growing interest among civil society and citizens to participate in the processes and programmes of regional economic communities (RECs). The constitutive treaties of RECs provide for citizens’ participation, but the accessibility of REC treaties and protocols remains a challenge. Decision-making remains state-centric despite growing citizen and civil society interest in regional integration. The Civil Society Guide to Regional Economic Communities aims to assist citizens and civil society in engaging with the policies and programmes of three RECs in Africa: EAC, SSADC, ECOWAS. [Download]

Featured infographic, @PatrickMcGee_: Compare RMB and US$ trade reports

China trade volume falls 7.0% in 2015: Customs (Business Times)

China's total trade volume fell 7% year-on-year to 24.59 trillion yuan (around US$3.74 trillion) in 2015, Customs said Wednesday, as slowing growth in the world's second-largest economy and plunging commodity prices took their toll. It was far below the government's target of 6% growth in trade, and the fourth year in a row that external commerce had missed its goal. China's imports slumped 13.2 per cent on the previous year to 10.45 trillion yuan, Customs said, while exports were down 1.8 per cent to 14.14 trillion yuan.

China sees 'many challenges' in 2016 as trade slumps on weak external demand (The Guardian)

South Africa: AGOA deadline stretched to retain US leverage (Business Day)

The US government has adopted a "prudent, risk-averse" approach in extending rather than completely lifting the threatened suspension of SA’s agricultural products under the African Growth and Opportunity Act, the Department of Trade and Industry’s director-general Lionel October says.

Mozambique: Mozal profits quadrupled in 2015 (Zitamar)

Mozal, the aluminium smelting business at Beleluane, Maputo, saw its profits almost quadruple last year to hit $238m according to data released by its majority owner, Australia-based South32.

Zambia Development Agency, China seal economic deal (Daily Mail)

Zambia's dependency on copper processing is set to change following the signing of an economic co-operation agreement that will spearhead value addition to natural resources and agricultural produce. On Monday evening, ZDA director general Patrick Chisanga and deputy director of commerce bureau of Qingdao Chunyu Xianli signed an economic co-operation agreement to provide a platform for strengthening joint ventures among the two countries’ business entities.

Zambia’s cross-border traders on trade sensitisation drive (Daily Mail)

CBTA secretary general Charles Kakoma said the association is keen to ensure that members are educated on the importance of cross- border trade formalities and the incentives that exist. He said in the spirit of promoting dialogue between the various stakeholders, the association intends to establish another trade information desk at the main Common Market for Eastern and Southern Africa trading centre market.

Zimbabwe: Non-essential imports bad for the economy (editorial comment, The Herald)

As a nation we need to tame our appetite for foreign goods. This is in the national interest. It is our economy we are destroying by resorting to needless imports in the name of choice. No amount of foreign direct investment can substitute for prudent use of our foreign reserves. Does it make sense that the country is in dire need of foreign currency to import maize because somebody used the money to import chocolate, second hand clothes or to import a musician to come and sing for one evening and take away $40 000 as payment?

Rwanda’s horticulture exports rise to Rwf4.7b (New Times)

Rwanda’s horticulture industry fetched more than $6.1m (Rwf4.7bnion) in the 11 months to November 2015, an increase from $4.3m realised in the same period in 2014. This was an increase of 41.3%, according to National Agricultural Exports Board report released last week.

Effectiveness of anti-corruption agencies in Kenya, Tanzania and Uganda (AfriMAP)

The study makes recommendations, based on the findings, for stronger, more relevant and effective institutions, which are aligned to the regional and continental frameworks such as the African Union Convention on Preventing and Combating Corruption (AUCPCC), which the three countries have ratified.

Tanzania: Fate of Bagamoyo port clarified (The Citizen)

The government has said the processes for the construction of the Bagamoyo Port will not be halted and will continue. Reacting to reports about the suspension of the construction of the $10 billion port the Ministry of Works, Transport and Communications said in a statement that the construction of the port will start in July this year upon conclusion of financing negotiations with key partners. The government was currently in discussions with China Merchant Holding International and Oman which are expected to be concluded by March, this year.

New report on global migrant trends highlights rising numbers for 2015 (UN)

Presenting the key finding of the latest United Nations survey on international migrant trends, the UN Deputy Secretary-General stressed that the issue of migration is one of the most challenging and important that the Organization is taking on in the new global landscape. “When we get into a period of dealing with the migration and refugee issues, it’s important that we have the facts,” Jan Eliasson told reporters at a press briefing, at UN Headquarters, thanking the UN Department of Economic and Social Affairs (DESA) for producing the latest international migration report. [Downloads available]

The future of ACP-EU relations: a political economy analysis (ECDPM)

Principles and practice in measuring global poverty (World Bank)

Dark clouds over ECOWAS single currency (Graphic)

Kenyan dealers cry foul over influx of cheaper Ugandan cars (Business Daily)

Zimbabwe: Millers set maize import target (The Chronicle)

Uganda approves Islamic banking (The Citizen)

Developing public-private partnerships in Guinea-Bissau: getting the policy framework right (AFDB)

Nigeria: the challenge of job creation (AfDB)

Christine Lagarde: 'The case for a global policy upgrade' (IMF)

CELAC summit to highlight strategies to combat poverty and economic inequalities (Caribbean News)

tralac’s Daily News archive

Catch up on tralac’s daily news selections by following this link ».

SUBSCRIBE

To receive the link to tralac’s Daily News Selection via email, click here to subscribe.

This post has been sourced on behalf of tralac and disseminated to enhance trade policy knowledge and debate. It is distributed to over 300 recipients across Africa and internationally, serving in the AU, RECS, national government trade departments and research and development agencies. Your feedback is most welcome. Any suggestions that our recipients might have of items for inclusion are most welcome.

Related News

Principles and practice in measuring global poverty

Collecting data on global poverty levels helps measure progress towards the goal of eliminating extreme poverty by 2030.

For more than 35 years, the World Bank has estimated the number of people living in extreme poverty by setting a global poverty line and collecting data from households around the world. In 2015, more than 700 million people were estimated to be living on less than US$1.90/day. The same line is used by the World Bank, the United Nations, and many others to track progress towards the elimination of extreme poverty and to hold the international community accountable for achieving progress.

So when a team of World Bank economists set about updating the poverty line earlier this year, they knew they had a daunting task ahead of them. They had to balance the requirements of ensuring methodological rigor, using the best available data, and keeping the goalpost for eliminating extreme poverty securely fixed in place.

“When the World Bank says that global poverty numbers are going down, we are criticized for showcasing our success. When we say they are up, people accuse us of rigging the numbers so that we can stay in business a little longer,” said Research Director Asli Demirguc-Kunt, “Keeping this goalpost fixed has become even more of an issue recently, since in 2013 the World Bank announced the goal of ending extreme poverty by 2030.”

At a Policy Research Talk last month, Francisco Ferreira, Senior Adviser in the World Bank’s Research Department and a leading member of the team charged with the poverty line update, sought to bring transparency to the update by explaining in detail all of the methodological choices and data constraints the team faced in setting a new poverty line.

The measurement of global poverty trends over time requires establishing a benchmark line that is consistent across countries. Once that line is drawn, it needs to be held constant in real terms as relative prices change – that is: as the prices of goods and services vary differently over time across countries. Between 2008 and 2015 that line was set at $1.25/day in 2005 dollars. But in 2014, the release of new Purchasing Power Parity (PPP) conversion factors for 2011 necessitated the adjustment of the poverty line as expressed in dollars. PPP exchange rates allow for the comparison of the prices of goods and services across countries, even if they are not traded internationally.

Ferreira explained that in approaching their task, the team followed three principles:

-

Use the most accurate set of prices available to compare the standards of living across countries – in this case the recently released 2011 PPPs.

-

Minimize changes to the World Bank’s goalpost for the objective of ending extreme poverty by 2030 – set at $1.25/day at 2005 PPP exchange rates.

-

Anchor decisions on the most relevant price levels: those faced by the world’s poorest people.

In following these principles, the team arrived at a line of $1.90/day in 2011 dollars. This upward revision in the line reflected a shift in relative prices between the U.S. and the world’s poorest countries, with the dollar losing value in PPP terms between the 2005 and 2011 price collection rounds. The revision helped ensure that the new poverty line reflects approximately the same cost for a basket of goods and services as the $1.25 line did in 2005.

“$1.90 appears to be much higher in US dollar terms. In Indian rupees it is not higher. And in Ghanaian cedis it’s not higher,” said Ferreira.

But so much for principles: did the updated poverty line succeed in keeping the goalpost constant in practice? The answer, as Ferreira explained, is a robust “yes”. Estimates of the incidence of global poverty moved only slightly, from 14.5 percent of the world’s population in 2011 using the old line to 14.1 percent using the new line. In addition, a number of alternative approaches to choosing a new line tend to yield figures that are very close to $1.90.

However, Ferreira was quick to caution that much more could be done to enhance the World Bank’s global poverty monitoring work. High on his wish list were a better understanding of what drives periodic changes in PPPs – which would require access to micro-level price data from the International Comparison Project (ICP) – and improved monitoring of key non-income dimensions of well-being, such as health and education.

Discussant Jan Walliser, Vice President for Equitable Growth, Finance, and Institutions, reflected on the value of the global poverty line and the data that it generates. “It’s the only number that is out there… It may not be perfect, but it’s something that we’re expected to provide for the international community. It’s one way of telling people where poverty trends are going across the world, and not just country by country.”

Related News

Classifying countries by income: a new working paper

The World Bank has just released a working paper reviewing the Bank’s classification of countries by income.

As Tariq Khokhar and Umar Serajuddin pointed out in their recent blog about whether we should call countries developing or not, there’s a strong appetite for classifying and ranking countries. Where is the best country to live, according to the OECD? (it depends, but it might be Australia, Norway or Sweden.) Which are making the most social progress, according to the Social Progress Imperative? (Norway and Sweden again.) Where is it easiest to do business, according to the World Bank? (Singapore.) Which countries have highest or lowest human development, according to the United Nations Development Program? (that’s Norway once more, and Niger is lowest.).

Using GNI per capita

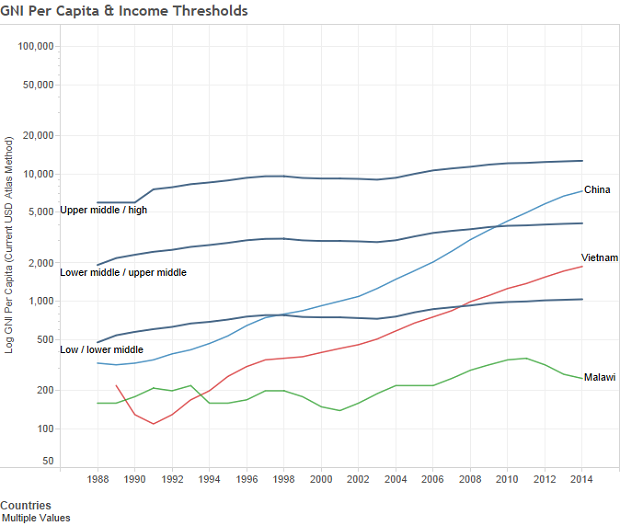

The World Bank has used a specific measure of economic development - gross national income (GNI) per capita – for the purpose of ranking and classifying countries for over 50 years. The first compendium of these statistics was called the World Bank Atlas, published in 1966 – it had just two estimates for each country: its population, and its per capita gross national product in US dollars, both for 1964. Then, the highest reported average income per capita was Kuwait, with $3,290. In second place was the United States, with $3,020, third was Sweden, a fair way behind, with $2,040. The bottom three were Ethiopia, Upper Volta (now Burkina Faso), and Malawi, with GNP per capita estimates of $50, $45 and $40 respectively (GNI used to be called GNP). It probably comes as no surprise that today Norway is top. Malawi is still bottom.

Grouping countries

In 1978, the first World Development Report went a step further. It introduced groupings of “low income” and “middle income” countries, which were those countries that were not industrialized, surplus oil producing, or centrally planned, and had 1976 per capita incomes lower and higher than $250, respectively. In the 1983 WDR, the middle income grouping was split into “lower” and “upper” bands around a cutoff of $1,670, and in 1989 a “high income” threshold of $6,000 was introduced. This system has remained in place since then, by adjusting the thresholds for inflation each year. Over time the terms have become a regular part of the development discourse, and many practitioners even just refer to the shorthand: LICs, MICs, and HICs.

This chart shows the GNI per capita of any country against the three thresholds, using the latest data from World Development Indicators.

Of course, the world has changed since 1989. Back then, well over half of all people on earth lived in countries classified as LICs – two thirds of them in just two countries, India and China. In 2014, some 25 years on, the effect of economic growth has meant that some countries have moved to a higher classification, from LIC to MIC, or from MIC to HIC, and less than 10% of the world lived in 31 LICs in 2014. 70% of those living in extreme poverty now live in MICs, although the extreme poverty rate in LICs is extremely high, at around 50%. So we’ve been taking a closer look at the the income classification. Our working paper was published recently – in it, we’ve attempted to review whether it is still relevant for its original analytical purpose.

The income classification is still useful

Our general finding is that using fixed thresholds that are held constant over time, adjusting only for price inflation, provides an absolute method of assessing change that many still find appealing. Other methods seem to have more limitations. For instance relative thresholds, such as those purely based on rankings (such as quartiles), are attractive but they have the inherent limitation that the target is constantly moving.

GNI per capita also continues to be a reasonable choice for a classifying variable. While clearly not perfect, GNI correlates well with several other indicators commonly used to assess the progress of countries. There is also an important practical advantage of data availability – for the most part, there are enough data, and estimates of both GNI and population size are available in time to update the classification each year.

Both measures are subject to difficult-to-qualify error, especially in countries with weak statistical capacity. This can be a source of volatility in the classification (i.e. sudden changes from one classification to the next), since GNI per capita estimates are occasionally revised when methods or source data improve – a new census is conducted, for example, or GDP estimates are “rebased”. You can see this effect for yourself, by taking a look at our archive database – we’ve selected GNI per capita for three April releases of the WDI six years apart: 2003, 2009, and 2015).