News

Africa’s growth potential – and its ‘Next 10’ biggest cities

Global investors are increasingly taking note of the untapped potential of sub-Saharan Africa, particularly its unparalleled demographic edge. According to a new report by PricewaterhouseCoopers, Africa will be enjoying faster economic growth than any other region – and will have the world’s biggest labour force.

Most major international corporations are already active in at least one of the three largest cities in sub-Saharan Africa – Lagos in Nigeria, Kinshasa in the Democratic Republic of Congo (DRC), and Johannesburg in South Africa.

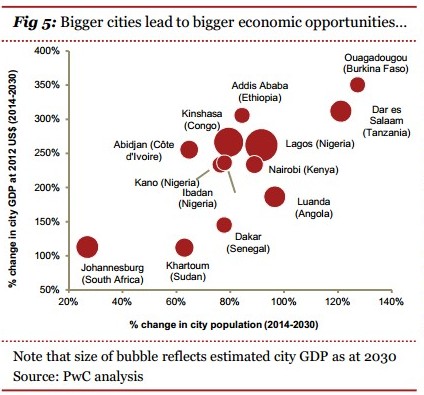

However, PricewaterhouseCoopers (PwC) economists believe investors should also be getting excited about the “Next 10” biggest cities in sub-Saharan Africa, namely Dar es Salaam (Tanzania), Luanda (Angola), Khartoum (Sudan), Abidjan (Côte d’Ivoire), Nairobi (Kenya), Kano and Ibadan (Nigeria), Dakar (Senegal), Ougadougou (Burkina Faso), and Addis Ababa (Ethiopia).

According to PwC’s latest Global Economy Watch report, released on Thursday, the population of these cities is projected to almost double by 2030, growing by around 32-million people. In fact, the latest UN projections indicate that, by 2030, two of the “Next 10” – Dar es Salaam and Luanda – could have bigger populations than London has now.

Cities are the typical entry points for businesses looking to expand into new markets, because they enable closer interaction with customers in a relatively small geographical area.

“The report projects that economic activity in the ‘Next 10’ cities could grow by around US$140-billion by 2030,” Stanley Subramoney, strategy leader for PwC’s south market region, said in a statement.

This is roughly equivalent to the current annual output of Hungary, Subramoney said, adding that this was a conservative estimate that did not take into account real exchange rate appreciation, despite relatively strong projected growth in these economies.

Roelof Botha, economic adviser to PwC, said that, in addition to high rates of GDP growth, rapid urbanisation and the so-called demographic edge, “a number of other economic phenomena in the region are starting to appeal to the global investment community”. These include:

-

Significant new discoveries of mining and energy resources, in particular gold and gas;

-

Substantial investment in infrastructure and capital formation by the private sector, which has witnessed an increase in the ratio of total fixed investment to GDP from 17.7% in 2000 to an estimated 23% in 2013;

-

Sustained growth in per capital incomes, which has led to demand shifts that are benefiting household consumption expenditure on durables, semi-durables and services; and

-

The ability of a growing number of countries to raise financing for infrastructure projects on the international capital market, in particular Kenya and Rwanda. Both of these countries have recently managed to sell government bonds globally at single-digit yields, which obviate the need for excessive debt servicing costs.

It was factors such as these which had seen a return to sound growth in foreign direct investment (FDI) inflows into a number of key African economies last year, Botha said.

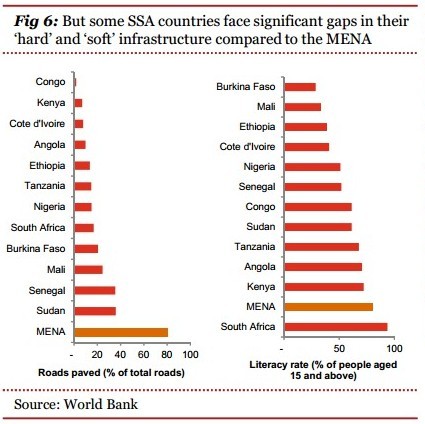

However, according to PwC, there are three issues that sub-Saharan Africa has been struggling to resolve for a number of decades, and which could slow the pace at which the “Next 10” cities grow.

These are: the low quality of “hard” infrastructure like roads and railways; inadequate “soft” infrastructure like schools and universities: and “growing pains” arising from political, legal and regulatory institutions struggling to deal with bigger, more complicated economies.

“The challenges that policy makers face is to convert Africa’s demographic dividend into economic reality by overcoming these hurdles,” Subramoney said, adding: “History suggests this will not be a quick or easy process. Infrastructure development is a key driver for progress across Africa and a critical enabler for sustainable and socially inclusive growth.

“However, investors should form their own plans to mitigate these problems by supporting infrastructure skills and development programmes.”