News

Global growth strengthens in line with economic forecasts, but prospects for some of world’s poorest regions deteriorate: UN report

Shifting international policy landscape heightens uncertainty around prospects for world trade, development aid and climate targets

Growth in the global economy has picked up in the last six months in line with expectations, but in many regions, growth remains below the levels needed for rapid progress towards achieving the Sustainable Development Goals, according to the United Nations World Economic Situation and Prospects as of mid-2017 report, launched on 16 May at UN Headquarters.

The report identifies a tentative recovery in world industrial production, along with reviving global trade, driven primarily by rising import demand from East Asia. World gross product is expected to expand by 2.7 per cent in 2017 and 2.9 per cent in 2018, unchanged from UN forecasts released in January this year. This marks a notable acceleration compared to just 2.3 per cent in 2016.

In a statement on the report, Mr. Lenni Montiel, Assistant Secretary-General for Economic Development in the UN Department of Economic and Social Affairs, underscored the “need to reinvigorate global commitments to international policy coordination to achieve a balanced and sustained revival of global growth, ensuring that no regions are left behind.”

According to the report, underpinning global economic recovery is firmer growth in many developed economies and economies in transition, with East and South Asia remaining the world’s most dynamic regions. However, economic recovery in South America is emerging more slowly than anticipated, and gross domestic product (GDP) per capita is declining or stagnant in several parts of Africa.

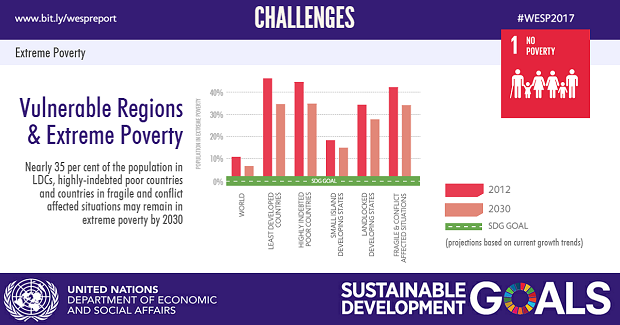

Forecasts for GDP growth in some of the least developed countries (LDCs) have been revised downward since January, with growth in the group as a whole projected to remain well below the Sustainable Development Goals target of at least 7 per cent. The report notes that under the current growth trajectory and assuming no decline in income inequality, nearly 35 per cent of the population in LDCs may remain in extreme poverty by 2030. Additional policy efforts are needed to foster an environment that will accelerate medium-term growth and tackle poverty through policies that address inequalities in income and opportunity.

The report points to a combination of short-term policies to support consumption among the most deprived and longer-term policies, such as improving access to healthcare and education and investment in rural infrastructure.

The report states that inflation dynamics in developed economies have reached a turning point, and risks of prolonged deflation have largely dissipated. By contrast, inflationary pressures have eased in many large emerging markets, allowing interest rates to come down.

The report further stresses heightened uncertainty over international policy, which will hinder a strong rebound in private investment globally. Corporate sectors in many emerging economies are vulnerable to sudden changes in financial conditions and destabilizing capital outflows, which could be triggered by faster-than-expected interest rate hikes in the United States.

The report highlights some positive developments related to environmental sustainability. The level of global carbon emissions has stalled for three consecutive years. This reflects growing renewable power generation, improvements in energy efficiency, transition from coal to natural gas, and also slower economic growth in some major emitters. But, the report also warns against waning commitments going forward.

Looking ahead, the report advocates for renewed global commitments to deeper international policy coordination in key areas, including aligning the multilateral trading system with the 2030 Agenda for Sustainable Development; expanding official development aid; supporting climate finance and clean technology transfer; and addressing the challenges posed by large movements of refugees and migrants.

Economic outlook by region: Africa

Growth in Africa remains subdued due to more severe headwinds than previously expected. Modest growth rates of 2.9 per cent and 3.6 per cent are expected in 2017 and 2018, respectively, down from forecasts of 3.2 per cent and 3.8 per cent in January.

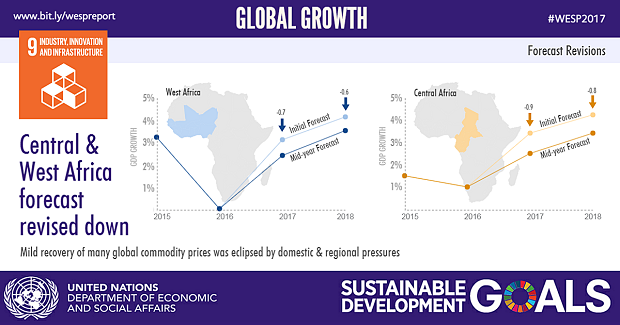

Forecasts for 2017 were lowered in all sub-regions except Southern Africa, which is expected to benefit from the small recovery in commodity prices and a better harvest. However, tighter external financing conditions, currency depreciation and political instability could undermine prospects. In East Africa, growth will be driven by investment supported by government incentives, while current weather patterns will act as a significant drag on growth. Despite remaining the fastest growing African region, the situation of the poorest remains critical. In North Africa, the downward revision is primarily driven by rapid inflation in Egypt. Stronger growth is anticipated in 2018, as the stabilizing security situation and stronger demand from Europe should prompt a recovery in tourism and trade. The prospects for Central Africa remain subdued as a result of low oil revenues and political stability risks. Similarly, pressures on the oil sector and foreign exchange constraints keep growth prospects down in Nigeria and, consequently, West Africa.

Despite tight monetary stances, inflation will remain elevated due to gradually rising commodity prices, lagged effects of currency depreciations, and dry weather in East Africa. High food inflation is particularly worrying, as it has a severe impact on the poor. Fiscal deficits remain stable but high, as a result of increases in infrastructure and social spending.

The outlook is subject to a number of risks. A more pronounced slowdown in China would negatively impact many economies that receive rising levels of FDI and investment finance from China. A sharper rise in global yields and a stronger US dollar would deteriorate external financing conditions, slightly offset by increased remittances. Security issues and political instability also pose critical threats. More than 20 million people face starvation and famine in northeast Nigeria, Somalia and South Sudan due to drought and protracted conflicts. Finally, should weather-related shocks continue, severe economic and social consequences are expected.