News

Development Assistance Aspects of Cotton: Seventh periodic report by the WTO Director-General

Since my last Periodic Report on the Development Assistance Aspects of Cotton to the membership in October 2013, four Rounds of the Director-General’s Consultative Framework Mechanism on Cotton (DGCFMC) have taken place, bringing the total number of such rounds held since 2004 to date to 23. The 24th Round of Consultations is scheduled for 27 November 2015. The Evolving Table on Cotton Development Assistance (ET), our well-known tool to track developments in financial assistance to the cotton sector, has been revised four times, including the latest update [of 27 October 2015].

I would like to commend Australia, Canada, the European Union – and several of its Member States, Japan, Switzerland and the United States. I would also like to commend Brazil, China and India on the specific platform of South-South Cooperation for Cotton-Sector Development. The support and engagement of these Members in the consultative forum has contributed to enhance the dialogue and consolidate the partnership between providers and recipients of development assistance for cotton.

Several multilateral and regional agencies have also been actively participating in this process, namely: the Food and Agriculture Organization (FAO), the International Cotton Advisory Committee (ICAC), the International Monetary Fund (IMF), the International Trade Centre (ITC), the United Nations Conference on Trade and Development (UNCTAD), the United Nations Industrial Development Organization (UNIDO) and the World Bank.

Context

The world cotton market has registered major changes in respect of global production, planted area and trade over the last two seasons. In a difficult context, marked by dwindling cotton prices and compounded by the persistence of sluggish world economic growth, the cotton sector of several LDCs and, in particular, African cotton-producing countries, has managed to remain stable. Cotton production in Africa increased by 13% in 2014/15 in relation to last season, to reach 1.69 million tons, accounting for 6% of world output and 14% of the global cotton area. Conversely, due to weak overseas demand, exports from African countries decreased by 7% in the 2014/15 season, amounting to 1.22 million tons. Exports from all major exporters, with the exception of India and the Francophone African countries, are expected to fall in the 2015/16 season. More detailed information on developments in the cotton sector worldwide and, more specifically, in Africa, is given in the Annex to this Report.

Implementation

As Members are aware, the work on cotton in the WTO follows a two-track approach, involving the development assistance aspects as well as the trade-related aspects of cotton. As regards the development assistance aspects, there is evidence of deeper consolidation of progress. The figures in the Evolving Table on Cotton Development Assistance show that the implementation of commitments is progressing, thereby shrinking the gap between commitments and disbursements. The traditional bilateral donors as well as relevant multilateral institutions have continued to be at the forefront of this process, accompanied by some developing Members on the platform of South-South Cooperation. This positive dynamic was complemented by the pursuit of domestic reform initiatives undertaken by the beneficiaries of cotton development assistance, as reflected in the tenth revision of the Table on Domestic Cotton Sector Reforms.

The trade-related aspects of cotton need to be assessed in the context of overall progress in the agriculture negotiations. In relation to this track, it is worth recalling the 2013 Bali Ministerial Decision whereby Ministers reaffirmed the importance of cotton and agreed to hold dedicated discussions on a bi-annual basis under the aegis of the Committee on Agriculture in Special Session to examine relevant trade-related developments across the three pillars of market access, domestic support and export competition in relation to cotton. As per this mandate, three such dedicated discussions have been held so far; the next one being scheduled for 27 November 2015. In these discussions, Members have engaged in focused examination of all forms of export subsidies, export measures and domestic support for cotton, as well as tariff and non-tariff measures applied to cotton exports from LDCs in markets of interest to them.

Evolution of cotton development assistance

Development assistance to the cotton sector provided by Members and relevant multilateral agencies shows a positive consolidation. The latest information is reflected in the twentieth version of the Evolving Table, which I forwarded to the membership on 27 October 2015. In summary, the results are as follows:

-

In Part I, on Cotton Specific Development Assistance (of active operational activities), the number of individual beneficiaries stands at 28. The total number of commitments is 35, and the total value of these commitments is approximately US$226 million. Disbursement flows reached US$102 million. The ratio of total disbursements to total commitments is 45%.

-

In Part II, on Agriculture and Infrastructure-Related Development Assistance (of active operational activities), the number of individual beneficiaries stands at 32. The total number of commitments is 54, and the total value of these commitments stands at US$4.97 billion. The disbursement flows reached US$3.05 billion. The ratio of total disbursements to total commitments is 61%.

Work in the Consultative Framework Mechanism continues to move forward. A tangible proof of this progress is the increased level of reporting by donors in all parts of the Evolving Table (ET) and the acceleration in the implementation of activities. There has been a significant reduction in the gap between commitments and disbursements, in particular in Part I of the ET. Thanks to the active engagement and involvement of participants in this forum, new initiatives are being discussed aimed at reinforcing regional integration on cotton in Africa. Participants are also continuing their collective monitoring and follow-up of projects to enhance the delivery of assistance. This is work in progress and there is still scope for further improvement. I would encourage providers of assistance as well as beneficiaries to pursue this positive trend.

South-South cooperation on cotton

Brazil, China and India have been showing notable leadership in this area. The important contributions and support initiatives of these Members in favour of LDCs and African countries are duly recognized. South-South Cooperation on cotton has become the epitome of the collaborative spirit that enabled to forge and consolidate a strong and lasting partnership amongst WTO Members and related multilateral and regional institutions.

Domestic cotton sector reforms

I would like to commend the cotton proponents for keeping Members regularly informed about their domestic reform priorities and action plans. The most recent information in this regard is shown in the last version of the Table on Domestic Cotton Sector Reforms, which I circulated to the membership on 27 October 2015. The information contained in this document has proved to be useful to better identify the kind of assistance needed, promote efficiency in the utilization of resources and foster the information exchange between providers and recipients to enhance cotton development assistance.

Conclusion

I welcome the continuous progress registered in the cotton sector, particularly in Africa. I underscore the need for continued engagement to address all aspects of the cotton dossier. On the development assistance aspects of cotton, sustained engagement and enhanced coordination between assistance providers and recipients, including “in-country” focal points, can bring positive results in the implementation of activities in support of the cotton sector.

The vital importance of cotton to particular LDCs as well as to a number of developing economies, especially in Africa, is continually recognized in the WTO. As a result, the cotton dossier remains at the core of our work. The dedicated discussions in relation to the trade-related aspects of cotton are enhancing transparency and monitoring of trade-related developments in this sector. I hope to see further progress in the cotton dossier in the coming days, including in the context of MC10.

Annex: Cotton sector developments

Cotton trade

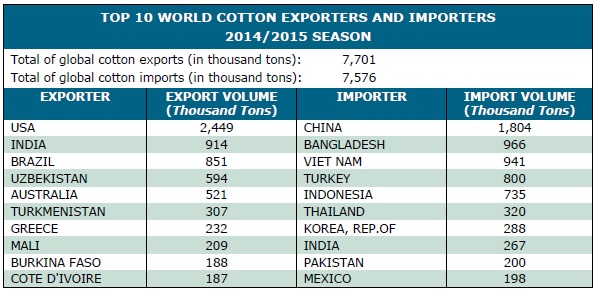

The volume of world cotton trade contracted significantly by 13% in 2014/15 compared to the last season, reaching 7.6 million tons. The average price of cotton continued its downward trend and slipped by 20% from last season to an average of 71 US¢ per pound in the 2014/15 season. World cotton stocks increased by 7% to a record 21.8 million tons, out of which China’s share represented 12.7 million tons. World ending stocks are projected down by 5% next season to 20.6 million tons.

In the framework of continued sluggish world economic growth, major changes were registered in export and import flows in 2014/15, showing a mixed picture amongst the main players. Exports from the largest world exporter, namely the United States, rose by 7% to 2.5 million tons, accounting for 32% of total world exports whereas exports from African countries dropped by 7% to 1.22 million tons. Brazil’s exports jumped by 75% to 851,000 tons, while those from India and Australia slipped by 55% and 50% to 914,000 tons and 467,000 tons, respectively. Exports from all major exporters, with the exception of India and the Francophone African countries, are projected to decline in the 2015/16 season.

In 2014/15, imports from China, the largest importer in the world, fell sharply by 41% to 1.8 million tons. This decline was only partly offset by higher imports from other countries, in particular, Bangladesh, Viet Nam and Indonesia. China’s imports are forecast to fall further in 2015/16 by 24% to 1.4 million tons.

The top 10 cotton exporters and importers in the 2014/15 season are shown in the Table below.

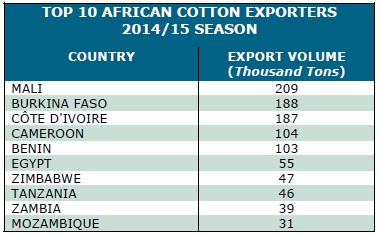

Focussing more specifically on Africa, the trade performance in African countries in 2014/15 was generally characterized by a decline in exports due to low global demand. Cotton exports fell by 9% in Francophone African countries from the previous season. However, a recovery is anticipated for this region in 2015/16, and the share of CFA countries’ world exports is expected to rise to 14%. A few examples of countries whose cotton exports did increase in 2014/15 include, among others: Egypt (+110%), Togo (+17%) and Uganda (+8%). The following Table lists the top 10 African cotton exporters in 2014/15: