News

Côte d’Ivoire Economic Update: Skilled labor force and connectivity needed to modernize economy

With a GDP growth rate projected to reach 7 percent in 2018 and 2019, Côte d’Ivoire continues to be one of the most dynamic economies in Africa.

The sixth Economic Update for Côte d’Ivoire, launched on 8 February 2018 by the World Bank notes the undeniable performance of the Ivoirian economy, but also points out the urgent need to encourage greater private sector participation and to improve public finance management, especially in education and health.

The report entitled, At the Gates of Paradise, proposes a strategy based on three complementary pillars:

-

Opening the country’s economy to attract foreign investors in order to benefit from transfers of technologies and skills.

-

Strengthening local competencies to assimilate, adapt and successfully implement new technological tools.

-

Lowering physical and virtual transportation costs, by improving the performance of the Ivoirian ports (and their related connections), but also by reducing the costs associated with the use of mobile telephone and Internet tools.

Additionally, the report focuses on how the country can make up its technological lag. “Economic theory has long demonstrated the key role played by technological innovation in a country’s development process,” said Jacques Morisset, Lead Economist, World Bank.

“To be successful, Côte d’Ivoire must not only open up to the exterior but also enhance the skills of its labor force and the connectivity of its economy. These two factors play an essential role in the dissemination of new imported technologies and their adaptation to the local economic fabric.”

This model for the dissemination of technology has been implemented by numerous countries in Asia and more recently in Africa.

“The strategy behind the success of money transfers by mobile phones that is now spreading all over Africa would help firms operating in Côte d’Ivoire become more competitive and so create productive jobs for the fast-growing labor force,” said Pierre Laporte, World Bank Country Director in Côte d’Ivoire. “It will enhance the excellent performance achieved the country these last few years.”

At the Paradise’s Doors – Key Messages

After analyzing recent developments in the Ivoirien economy and its outlook for the short and medium term, this sixth report on the economic situation in Côte d’Ivoire focuses on how the country can make up its technological lag.

Although Côte d’Ivoire has embarked on a trajectory of strong growth after more than a decade of political instability, its aim of becoming an emerging economy will not be achieved without more productive businesses, as they are the country’s main employers and generate most of its revenues.

State of the Ivorian economy

With a rate of growth that is expected to hold steady at around 7.6 percent in 2017, Côte d’Ivoire continues to be one of the most dynamic economies in Africa, if not the world. As the catch-up effects that prevailed at the exit from the post-electoral crisis of 2011 have dissipated, this solid performance is explained by the rebound of agriculture owing to favorable rainfall and higher prices. It also demonstrates Côte d’Ivoire’s resilience to internal and external shocks.

The political and social climate, which deteriorated in the first half of the year as a result of the demands of some military personnel and civil servants, has calmed, and the sharp drop in cocoa prices has been offset by an excellent harvest.

The main monetary and financial variables stayed on their trend in recent years. Inflation held steady at around 1 percent annually owing to the prudent monetary policy of the BCEAO. Credit to the economy grew around 14 percent, reflecting strong demand in the private sector and the banks’ gradual diversification toward small and medium enterprises. The financial system is stable, respecting regional prudential ratios, and the rate of nonperforming loans stands at around 8 percent.

Although the current account deficit has stabilized at around 1 percent of GDP, this conceals significant developments. The 20 percent increase in exports reflects rising agricultural prices and good harvests. Imports have remained relatively stable, although the increase in purchases of oil has been offset by a decline in purchases of capital and intermediate goods. Inflows of external capital have financed the current account deficit, particularly government borrowing on the international market, with the result that the international reserves have risen significantly.

The Government’s fiscal position remains under control, although its deficit rose from 4 percent of GDP in 2016 to 4.5 percent in 2017. A number of factors explain this deterioration. First, the Government had to undertake additional expenditures to respond to the demands of certain groups in the armed forces and the public sector. As well, the authorities chose to absorb the rising oil prices and the decline in cocoa prices on the international markets by reducing the taxes on these products rather than allowing these fluctuations to flow through to pump prices and producer prices for cocoa beans. The fiscal policy was thus mobilized in support of cocoa producers and transport companies/motorists in 2017 to keep the social peace.

To offset this new spending, the authorities achieved budget savings over the year. Capital expenditures were reduced from the amount in the approved budget, and the authorities were also successful in increasing the collection of some taxes, particularly the corporate income tax.

Two initiatives helped reduce fiscal risks and improve public management in two sectors that are strategic for the country. First, the Government undertook to improve the payment of its electricity bills in the context of a consolidation plan intended to reduce the deficit in this sector. Second, a financial audit of some operations on the cocoa market identified numerous irregularities. Their correction should improve the governance within this market. These two initiatives send a positive signal that should encourage private sector investment.

The fiscal deficit has been financed by concessional aid and nonconcessional borrowing.

While the Government mainly accessed the regional market in 2016, in 2017 it tapped the international markets as it had in 2015. The issuance of euro bonds in June 2017 for a net amount of US$ 1.2 billion was a resounding success, with demand standing at four times this amount and a yield lower than the yield of the previous issuance in 2015. A portion of these bonds was denominated in euros, limiting the exchange risk for the country. However, the level of the public debt increased, from 47 percent of GDP in 2016 to over 50 percent in 2017.

Côte d’Ivoire’s short- and medium-term outlook remains encouraging. The GDP growth rate should reach 7 percent in 2018 and 2019. Modern services such as communications, finance and transport should continue to support the Ivoirien economy, and construction should also continue to grow steadily. All of these sectors should benefit from the country’s rapid urbanization and economic growth. The industrial sector should grow owing to the expansion of the food processing industry. The contribution of agriculture should be comparable to previous years although it remains dependent on weather conditions.

Prices, money and credit should maintain their current trajectory. The current account deficit is expected to stabilize at around 2 percent of GDP, while remaining vulnerable to changes in the terms of trade and weather conditions.

The fiscal adjustment planned for 2018 and 2019 is a key feature of the Government’s economic policy. It is aimed at maintaining debt sustainability and achieving the WAEMU target. The fiscal deficit should decline from 4.5 percent of GDP in 2017 to 3.0 percent of GDP in 2019. This adjustment is based on an increase in revenues (approximately 0.8 percent of GDP) and a reduction in current expenditures, which should return to their 2016 levels as a percentage of GDP (i.e., without the 2017 security spending). This strategy requires improving the efficiency of public spending so that the Government can achieve its ambitious infrastructure and social service objectives without spending more. There seems to be significant room for improvement both in the management of public investment and in the provision of public services in the areas of education and health.

Côte d’Ivoire has thus far benefited from generally favorable terms of trade and weather conditions in recent years, unlike the majority of African countries. However, the Ivoirien economy remains vulnerable to external risks such as fluctuations in the prices of agricultural and mining products, weather conditions, global and regional security risks, and a tightening of the regional and international financial markets.

On the domestic front, the presidential elections planned for 2020 could create uncertainties and even some instability, which could slow private investment. The Government could be tempted to spend more to support economic activity and maintain the social and political peace. The Government must also successfully increase its revenues while controlling its spending in order to avoid further debt, since the sustainability of the public debt has deteriorated, as indicated in the recent joint analysis by the International Monetary Fund (IMF) and World Bank.

As of end-2017, Côte d’Ivoire continues to be classified as a country with a moderate risk of debt overhang. However, it seems more vulnerable to slower economic growth, higher interest rates or a deterioration in its fiscal position owing to the steady increase in its debt in recent years. This risk is even higher if the debt of the public enterprises is taken into account, particularly enterprises in the energy sector. Contingent risks relating to some public banks (currently undergoing restructuring) and the public-private partnership programs should also be taken into account.

How to accelerate the economic transformation of Côte d’Ivoire?

Since the end of the crisis in 2012, the performance of the Ivoirien economy has been remarkable, with a per capita growth rate exceeding 5 percent per year. Despite this upturn, per capita income is today below levels in the early 1980s and has just caught up to the level reached in 1990. Although the political events that rocked Côte d’Ivoire largely explain this relative stagnation of incomes, they are not the entire explanation.

An examination of the economic growth factors during the period 2002 through 2014 shows that although Ivoiriens worked more, they did not necessarily work better. The employment rate did indeed increase significantly (even faster than the population growth rate), but incomes did not follow the same positive trend, for at least two reasons. The first is that labor productivity in the key sectors increased only slightly during this period and even declined in agriculture. The second reason is that while Ivoiriens left unproductive sectors to move to those with higher productivity, this movement was only partial and gradual. By way of comparison, in East Asia intersectoral productivity gains were 3 to 5 times more rapid, while the structural transformation generated by labor mobility contributed to 2 percent of growth each year as against just 0.5 percent in Côte d’Ivoire.

Labor productivity within the Ivoirien economy has risen since 2012, by about 4-5 percent per year, but businesses still lag behind the production frontier achieved by the emerging countries. This lag exists in the productivity of both labor and capital and in almost all sectors of the economy. Only a few productivity niches have appeared, such as mobile telephony and money transfers.

To make up this lag, Côte d’Ivoire must improve its economic and institutional framework. According to economist D. Rodrik, such an improvement in the overall framework within which businesses operate can accelerate a country’s speed of convergence with the economies of the most advanced countries by making the private sector more efficient. This movement is already under way in Côte d’Ivoire as shown by the increase in its score in the Country Policy and Institutional Assessment (CPIA) from 2.7 in 2010 to 3.4 in 2017, the largest increase among the developing countries as measured by the World Bank over the past 10 years. This increase reflects the efforts undertaken by the Ivoirien authorities to improve the country’s macroeconomic, structural, institutional and legal conditions. However, this progress will have an impact only in the medium term, as the effect on the productivity of businesses is generally slow.

The speed of Côte d’Ivoire’s convergence could accelerate if it adopts and adapts new technologies by means of a technological catch-up initiative or an unconditional convergence, i.e., one that is not necessarily linked to the conditions that prevail in the country. Few countries have successfully achieved this catch-up without having prioritized openness to the rest of the world through foreign investment and exports. These two vectors promote the transfer of technology and skills since the vast majority of new technologies, including those that can shape the Africa of tomorrow, are often proprietary developments by companies in advanced countries. Seeking partnerships should therefore be a priority.

A focus of Côte d’Ivoire’s National Development Plan is to increase foreign direct investment (FDI) and exports. Although some specific initiatives have been launched, particularly in the agri-food processing sector, this strategy has not yet taken off. The weight of FDI and exports in GDP has not increased in recent years. According to the World Bank only 3 percent of Ivoirien companies use imported technology licenses as against 15 percent in the rest of Africa. Moreover, Ivoirien companies spend less on research and innovation than their African counterparts.

To be successful, Côte d’Ivoire must not only open up to the exterior but also enhance the skills of its labor force and the connectivity of its economy. These two factors play an essential role in the dissemination of new imported technologies and their adaptation to the local economic fabric. This model for the dissemination of technology has been implemented by numerous countries in Asia and more recently in Africa, including Rwanda and Ethiopia. To use the words of a senior Malaysian official, “the contribution of foreign investment and exports is proportional to their capacity to train local workers and entrepreneurs, who will in turn train other workers and entrepreneurs.” Good connectivity is also essential to the flow of products, services, persons and ideas.

This report proposes a strategy involving three complementary pillars that will help generate a virtuous circle allowing Côte d’Ivoire to make up its technological lag and converge more rapidly with the most advanced countries:

-

Pillar one: A policy of openness must be defined on the basis of Côte d’Ivoire’s comparative advantages. An indicative list of potential products is proposed on the basis of the theories of revealed comparative advantages and product space. These industries can potentially attract foreign investors and turn toward exports in order to benefit from transfers of technologies and skills, which are still badly needed in Côte d’Ivoire.

-

Pillar two: The capacity to assimilate, adapt and successfully implement a new technological tool will, to a great extent, depend on the skills available in the country. Unfortunately, Côte d’Ivoire’s lag in terms of the development of its human capital is an obstacle. While the reform of the education system is essential, it must be accompanied by training partnerships with private companies, particularly foreign companies, and training of Ivoiriens abroad. Here, the openness will help strengthen local competencies, which will in turn themselves reinforce the country’s openness.

-

Pillar three: Good connectivity facilitates trade and increases the size of the market, generating economies of scale that are often essential to the establishment of foreign businesses and development of export activities. This requires lowering physical and virtual transportation costs and also reducing distances, for example through urbanization. The priorities are to improve the performance of the Ivoirien ports (and their related connections), to reduce the costs associated with the use of mobile telephone and Internet tools (1.5 to 3 times more expensive than in Ghana, for example) and to better manage the urbanization process by increasing the economic density of cities while controlling congestion costs.

Understanding the State of the Ivorian Economy in Five Charts

The Sixth Economic Update for Côte d’Ivoire notes the undeniable performance of the Ivoirian economy, but also points out the urgent need to work on certain aspects. The main needs are to encourage greater private sector participation and to improve public finance management, especially in education and health.

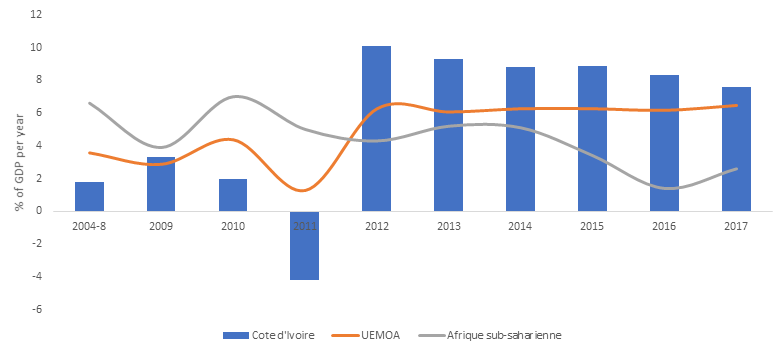

Côte d’Ivoire’s economic growth remains among the fastest on the African continent

In 2017, Côte d’Ivoire continued to be one of the most buoyant economies in Africa, with a growth rate expected to hold steady at around 7.6% (Chart 1). This positive performance is due to the recovery in agriculture, and shows Côte d’Ivoire’s resilience to domestic and foreign shocks. The short- and medium-term outlook remains encouraging. The GDP growth rate is forecast at 7% in 2018 and 2019. Nonetheless, the Ivoirian economy remains vulnerable to external risks such as fluctuations in agricultural and extractive commodity prices, climate conditions, global and regional security risks, and tight regional and international financial markets.

Chart 1. Côte d’Ivoire’s economic growth (Source: World Bank).

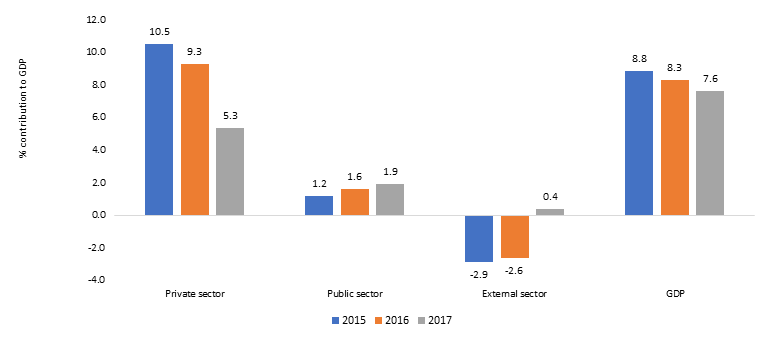

Growth increasingly driven by the public sector as the private sector’s contribution slows

The private sector’s contribution to Ivoirien growth has decreased since the end of the crisis in 2012 (Chart 2). However, there has been an increase in the foreign and public-sector contributions associated with the Government’s pro-cyclical policy and a positive external environment (in terms of export revenues and foreign investments). The authorities have taken forward an ambitious public investment program to narrow infrastructure and social services gaps, which had widened over more than a decade of political crises.

Chart 2. A downward trend in the private sector’s contribution (Source: World Bank).

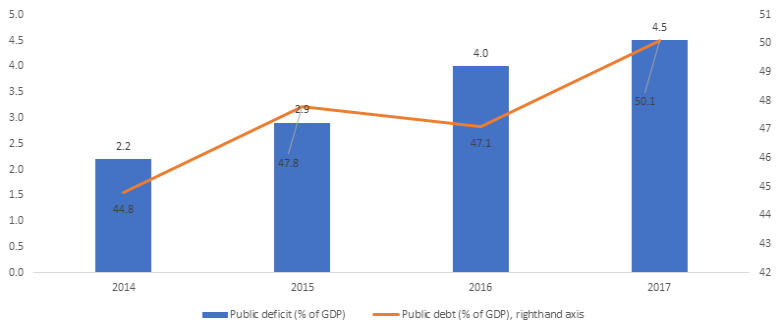

Budget deficit and public debt have both grown

The Government’s fiscal situation deteriorated in 2017. The budget deficit grew from 2.9% of GDP in 2015 to 4% of GDP in 2016 and 4.5% in 2017 (Chart 3). The deterioration in the fiscal situation was due to stagnating domestic revenues (around 19.5% of GDP), whereas public expenditure increased more sharply (+0.6% of GDP) owing to security and social contingencies.

Chart 3. Growth in budget deficit and public debt (Source: World Bank and IMF).

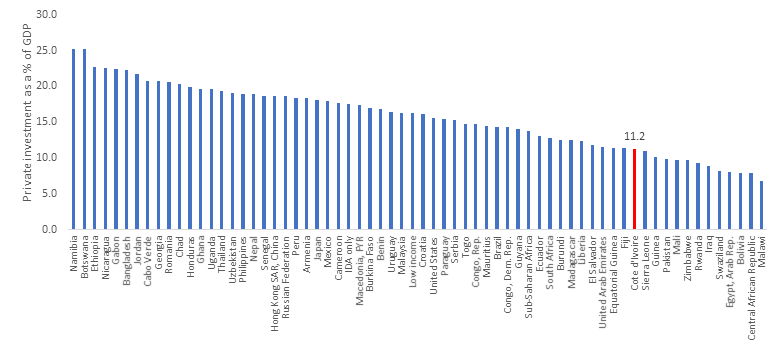

Private investment is still relatively low and needs to be encouraged

The rate of private investment jumped between 2011 and 2017, rising from 5.7% to 12.0% of GDP between 2011 and 2012 before stabilizing at approximately 11% of GDP between 2013 and 2017. Yet this rate is still too low, as shown by Chart 4, especially when compared with the emerging countries, where it can top 25% of GDP, and even the stronger-performing Sub-Saharan African countries such as Ghana (19%) and Uganda (18%). Côte d’Ivoire has also failed so far to attract significant inflows of foreign direct investments, which account for just 1.5-2% of GDP, far from the rates observed in Ethiopia and Mozambique. The development of the private sector is decisive if Côte d’Ivoire is to maintain its rapid growth rate and redistribute the fruits of economic growth more equitably across the entire population.

Chart 4. Share of private investment in GDP per African country (Source: World Bank)

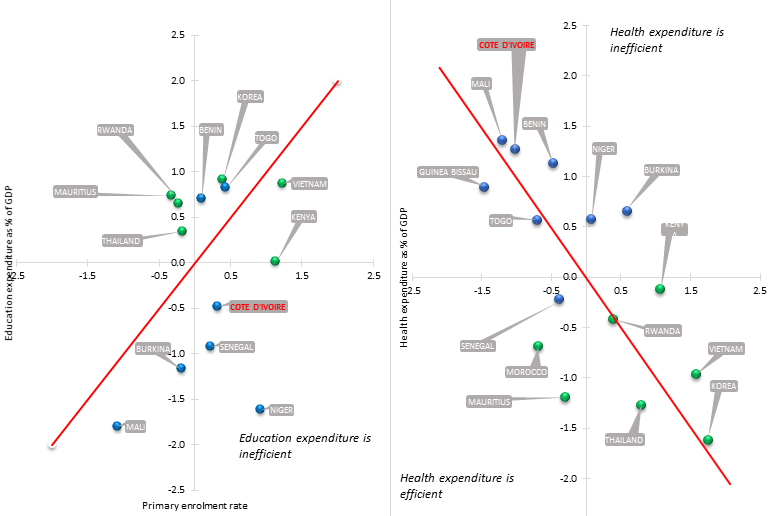

Public expenditure efficiency needs to be improved, especially in the social sectors

In addition, the fiscal consolidation planned by the Ivoirien authorities in 2018 and 2019 is creating an urgent need to improve the efficiency of public expenditure. If the central government cannot spend more, it will have to spend better to achieve its ambitious infrastructure and social services goals. It will need to improve both the allocation of public expenditure (“knowing where to spend”) and its financial efficiency (“knowing how to spend”).

The report provides a comparative analysis (Chart 5) of a sample of some 20 countries in the sub-region and countries that could serve as models for central government to improve the efficiency of its education and health expenditures (which account for nearly one-third of the budget). This analysis shows that, despite considerable central government expenditure on education, the results in terms of primary school enrolment remain disappointing. By way of comparison, Benin spends proportionally less than Côte d’Ivoire, but has a higher rate of pupils enrolled in primary education.

The fact that Côte d’Ivoire spends relatively little on the health sector explains its modest maternal mortality outcomes. Only Mali and Guinea Bissau put fewer resources into health than Côte d’Ivoire.

Chart 5. The efficiency of public expenditure in the social sectors (Source: World Bank). Note: Each variable is measured in terms of deviation from the sample’s mean. The blue dots represent the WAEMU member countries.