News

Harnessing the buy side’s potential to develop East Africa’s capital markets

A key step in developing a local capital market is to develop the “buy side” – to encourage greater participation of local institutional investors such as pension funds and insurance firms. If managed well, these pools of savings can become important sources of long-term financing, including for infrastructure, which can drive socioeconomic growth.

The share of residents in East African Community (EAC) countries Kenya, Rwanda, Tanzania, and Uganda who access pension and insurance products is still small, although growing. Savings managed by local institutional investors in these countries nearly doubled in just four years, to about $19 billion by early 2016. We recently surveyed buy-side institutions in these four countries to ask how they are managing savings across asset classes and EAC countries.

We found that most of these investors want to further diversify their portfolios, but they are impeded largely by a lack of investable securities and risk-management products that allow them to invest in a way that meets their aims. This points to a need in these markets for more long-term investment vehicles, in particular – as well as market participants. For example, a large majority of surveyed investors showed strong interest in new vehicles such as a regional “fund of funds” that could pool their resources and manage risk by investing across diverse infrastructure projects by sector and country.

There already are clear signs that pension funds, in particular, have been diversifying their portfolios over the past decade – shifting further away from the most liquid asset classes. Surveyed pension funds hold an average of just 1 percent in cash and demand deposits across the EAC focus countries. And pension fund and insurer investments in short-term government securities typically fall well below national and even internal ceilings. Survey findings show pension funds generally hold much more in longer-term than short-term government securities. But very limited corporate bond holdings, even for pension funds, is at least partly the result of small market size and lack of product.

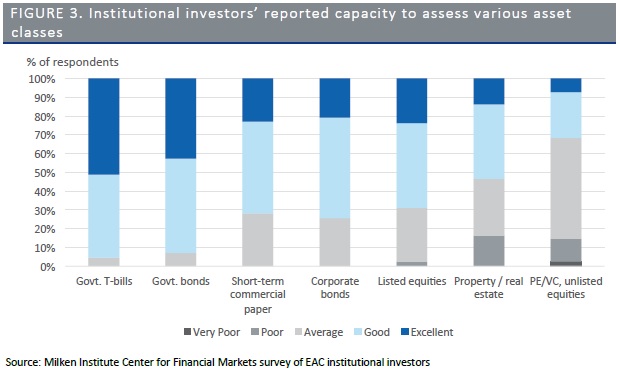

Our findings also show that tiny allocations so far to private equity and venture capital (PE/VC) reflect limited experience and capacity evaluating these new asset classes – more so than lack of demand or investment limits. In fact, national regulatory approaches are still evolving. Greater clarity on how regulators will treat these new asset classes may encourage more investment. While certainly not risk-free, some investment in PE/VC as part of a well-managed portfolio could help generate returns. At the same time, it will be important to boost risk-evaluation capacity among regulators, investors, and financial intermediaries.

How do national regulations affect how these investors manage their portfolios? We found that in most cases, national regulatory investment limits are not the binding constraint preventing local institutional investors in the EAC from further diversifying their portfolios. Their actual allocations to public equities and corporate bonds generally fall well below national regulatory caps. And internally set targets tend to fall well below national ceilings – as does actual investment in these securities.

Around half of investors said they invest some of their portfolio assets outside their home countries – typically in other EAC countries. How can these EAC markets draw on regional ties to attract institutional investors? Roughly half of survey participants said access to better strategies and instruments for managing foreign exchange risk would make them more likely to invest in assets across EAC borders.

We found that some investors may not be clear on the intraregional restrictions by asset class they actually face. Regulators should step up communications with investors to ensure they clearly understand both the limits and opportunities in how they invest within the EAC and across asset classes. A well-functioning buy side can reduce an economy’s reliance on foreign portfolio investors, increasing its resilience to sudden capital inflows and outflows. Further progress on intraregional integration within the EAC may help mitigate some of the risks associated with cross-border investment. Limited investable securities in local capital markets strengthens the case for easing or harmonizing restrictions intraregionally. This, in turn, could improve market liquidity, deepen the EAC’s capital markets, and make it easier for local institutional investors to diversify their portfolios.

Jim Woodsome is a Senior Research Analyst at the Milken Institute’s Center for Financial Markets.

See the findings from this research below or on the Milken Institute website.