All News

Shaping globalization

Done wisely, it could lead to unparalleled peace and prosperity; done poorly, to disaster

Globalization is the big story of our era. It is shaping not just economies, but societies, polities, and international relations.

Many assume it is also, for good or ill, an unstoppable force. History, however, suggests this is not so. We can neither assume globalization will persist, nor that it will be desirable in all respects. But one thing we must assume: it is ours collectively to shape.

If globalization is done wisely, this century could prove an unparalleled era of peace, partnership, and prosperity. If it is done badly, it might collapse as completely as pre-World War I globalization between 1914 and 1945.

Globalization is the integration of economic activity across borders. Other forms of integration – above all, the spread of people and ideas – accompany it. Three interacting forces – technology, institutions, and policy – shape it.

Over the broad sweep of history, technological and intellectual innovation is the driving force behind globalization. It has lowered the cost of transportation and communication, increasing opportunities for profitable economic exchange over greater distances. In the long run, such opportunities will be exploited.

Even before the industrial revolution, mankind’s ability to navigate the seas in sailing vessels facilitated the birth of global empires, transoceanic movement of people, and an expansion in worldwide commerce. But technological change accelerated after the industrial revolution, creating new opportunities.

Driving the globalization of the late 19th and early 20th centuries were the steam locomotive, the steamship, and the telegraph. Driving the globalization of the present era are the container ship, the jet aircraft, the Internet, and the mobile phone.

The integration of communications and computing is the technological revolution of our era. By 2014, the world had 96 mobile-phone subscriptions and 40 Internet users for every hundred inhabitants. Twenty years earlier neither was significant. Information is increasingly digital and the world increasingly interconnected. This is a revolutionary transformation.

Institutions also matter. Historically, empires facilitated long-distance commerce. That was true before modern times and, still more, with the European maritime empires from the 16th to the 20th centuries. Today, the institutions that facilitate long-distance commerce are treaties and multilateral organizations: the World Trade Organisation (WTO), the International Monetary Fund, and regional clubs, such as the European Union.

Semipublic and purely private institutions also matter. Think of the chartered trading company, notably the British East India Company, and then, since the 19th century, the limited liability joint-stock company. Also important are organized markets, notably financial markets, which developed from simple beginnings into the 24-hour, around-the-globe networks of today.

While technology’s arrow has moved in one direction – toward opportunities for economic integration – institutions have not. Empires have come and gone. When the European empires disappeared after World War II, most of the newly independent countries turned away from international commerce, judging it exploitative.

This brings to mind the third driver – policy. The movement of newly independent developing countries toward self-sufficiency was a policy reversal. The most important reversal of all was the worldwide collapse in globalization that followed the two world wars and the Great Depression. The monetary order then disintegrated, and trade became increasingly restricted.

After World War II, a limited liberalization, largely of trade and the current account, spread across the high-income economies, under U.S. auspices. Then, in the late 1970s and in the 1980s and 1990s, domestic market liberalization, opening of international trade, and loosening of exchange controls spread across the world.

Crucial steps on this journey were China’s adoption of “reform and opening up” in the late 1970s under the leadership of Deng Xiaoping; the election of Margaret Thatcher as U.K. prime minister in 1979 and Ronald Reagan as U.S. president in 1980; the launch of the European Union’s “single market” program in 1985; the Uruguay Round of multilateral trade negotiations, which began in 1986 and ended eight years later; the collapse of the Soviet empire between 1989 and 1991; the opening up of India after its foreign exchange crisis of 1991; the 1992 decision to launch a European monetary union; the creation of the WTO in 1995; and China’s entry into the WTO in 2001.

Embrace of markets

Underlying these changes was a rejection of central planning and self-sufficiency and an embrace of markets, competition, and openness. This is not a global empire. For the first time in history, an integrated world economy connects activities located in a large number of independent states with the shared goal of prosperity.

It worked, albeit imperfectly. According to the McKinsey Global Institute (2014), flows of goods, services, and finance rose from 24 percent of global output in 1980 to a peak of 52 percent in 2007, just before the Great Recession. Between 1995 and 2012, the ratio of trade in goods to world output rose from 16 to 24 percent.

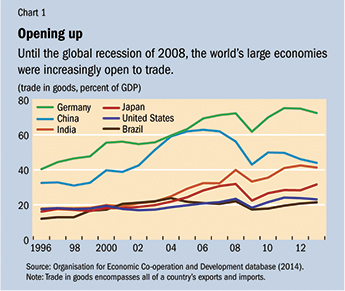

Virtually all economies became more open to trade. The ratio of trade in goods (exports plus imports) to GDP in China rose from negligible levels in the 1970s to 33 percent in 1996 and 63 percent in 2006, before plunging during the financial crisis. The ratio of India’s trade to GDP rose from 18 percent in 1996 to 40 percent in 2008 (see Chart 1).

Virtually all economies became more open to trade. The ratio of trade in goods (exports plus imports) to GDP in China rose from negligible levels in the 1970s to 33 percent in 1996 and 63 percent in 2006, before plunging during the financial crisis. The ratio of India’s trade to GDP rose from 18 percent in 1996 to 40 percent in 2008 (see Chart 1).

An important driver of trade expansion was the availability of low-cost workers in emerging economies. Before World War I, the big opportunity was to incorporate undeveloped land, particularly in the Americas, into production for the global market. This time, the biggest opportunity is incorporating billions of previously isolated people as workers and then consumers and savers.

Trade involving emerging economies duly exploded. In 1990, 60 percent of trade in goods was among the high-income economies, another 34 percent was between high-income and emerging market economies, and just 6 percent was among emerging market economies. By 2012, these ratios were 31 percent, 45 percent, and 24 percent, respectively.

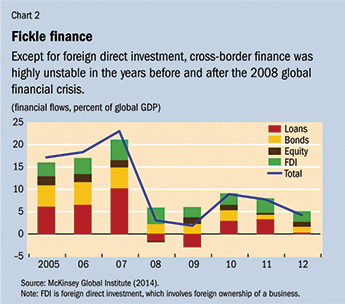

Global companies are central players. This is shown by, among other things, the growth of foreign direct investment (FDI), which results in cross-border ownership of businesses. In 1980, FDI was negligible. Today, it is not just a large flow (averaging 3.2 percent of global output between 2005 and 2012) but a stable one. It has proved triply helpful – as a source of knowledge transfer, a vehicle for promoting cross-border economic integration, and a stable form of finance.

Other areas of finance have been far less stable. Total cross-border financial flows peaked at 21 percent of global output in 2007, before collapsing to 4 percent in 2008 and 3 percent in 2009. A modest recovery ensued. But cross-border lending, bond issuance, and portfolio equity flows had not recovered to precrisis levels even by 2012. Cross-border lending, predominantly from banks, was particularly volatile, as is usual in crise s (see Chart 2).

Other areas of finance have been far less stable. Total cross-border financial flows peaked at 21 percent of global output in 2007, before collapsing to 4 percent in 2008 and 3 percent in 2009. A modest recovery ensued. But cross-border lending, bond issuance, and portfolio equity flows had not recovered to precrisis levels even by 2012. Cross-border lending, predominantly from banks, was particularly volatile, as is usual in crise s (see Chart 2).

While trade, finance, and communication have grown rapidly, this is not so true of movements of people. Although, international travelers and foreign students increased markedly, migrants grew at virtually the same rate as the global population – despite huge gaps in real wages. Trade and capital flows are, to an extent, a substitute for movement of people. Yet great pressure for movement of people from poor countries to richer ones persists, particularly across the Rio Grande and the Mediterranean Sea.

Globalization, then, has meant growing cross-border economic activity. But the story is more complex when it comes to prosperity.

Globalization, then, has meant growing cross-border economic activity. But the story is more complex when it comes to prosperity.

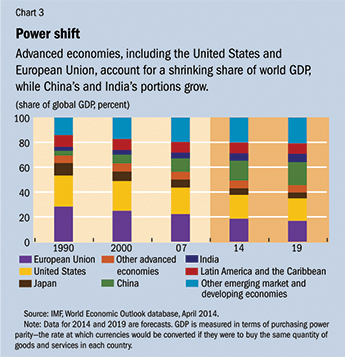

The age of globalization has driven rapid shifts in the location of economic activity. In 1990, the share of the high-income economies in global output at purchasing power parity (or PPP, the rate at which currencies would be converted if they were to buy the same quantity of goods and services in each country) was 70 percent, with the European Union contributing 28 percent and the United States 25 percent. By 2019, according to the IMF, this total will be down to 46 percent.

Over the same period, China’s share is forecast to rise from 4 percent to 18 percent and India’s from 3 percent to 7 percent. The rapid growth of the most successful emerging market economies, which caused this shift, would not have occurred without the access to trade and know-how provided by globalization (see Chart 3).

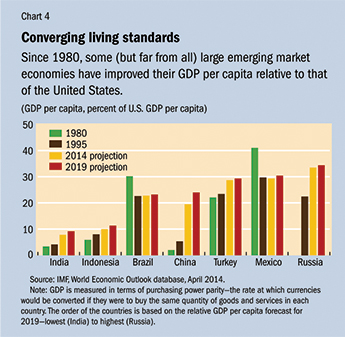

A degree of convergence in standards of living has also occurred (see Chart 4). China’s GDP per capita, relative to the United States, is forecast to rise from 2 percent in 1980 to 24 percent in 2019. This is an extraordinary performance by any standard. China has become a middle-income country with a GDP per capita at PPP forecast to be higher than Brazil’s by 2019. India, too, has registered convergence, though on a more modest scale. Indonesia and Turkey have also done quite well. But Brazil and Mexico are forecast to be poorer relative to the United States in 2019 than they were back in 1980. Seizing the opportunities afforded by globalization turns out to be hard.

Decline in mass poverty

The age of globalization has brought an extraordinary decline in mass poverty, again largely due to China. In east Asia and the Pacific, the proportion of the population living on less than $1.25 a day (at PPP) fell, astonishingly, from 77 percent in 1981 to 14 percent in 2008 (World Bank, 2014). In south Asia, the proportion in extreme poverty declined from 61 percent in 1981 to 36 percent in 2008. In sub-Saharan Africa, however, the share of people in extreme poverty was 51 percent in 1981 and still 49 percent in 2008.

Finally, globalization has been associated with complex shifts in the distribution of incomes across and within countries. The World Bank’s Branko Milanovic (2012) suggests that the degree of inequality among individuals across the globe has stayed roughly constant in the era of globalization, with rising inequality within most economies offsetting the success of some large emerging economies in raising their average incomes relative to those in rich countries. He also shows that the top 5 percent of the global income distribution enjoyed large increases in real income and the top 1 percent very large increases between 1988 and 2008. Those in the 10th to the 70th percentiles from the bottom also did quite well.

Two groups, however, did relatively badly – the bottom 10 percent, the world’s poorest, and those in the 70th to the 95th percentiles from the bottom, who are the middle- to lower-income groups in high-income countries. Thus, a globally beneficial rise in real incomes was associated with rising inequality within many high-income countries. The explanations are complex, but globalization was surely among them.

What might lie ahead?

Technology will continue to drive integration. Soon, almost every adult and many children are likely to own a smart mobile device that offers instant access to all the information available on the World Wide Web. It will make the transmission of everything that can be digitized – information, finance, entertainment, and much else – essentially costless. An explosion of exchange is certain.

While some areas of technology are making leaps, others, such as the cost of transporting goods and people, are not falling to any significant degree. This suggests that technological advances will open up far greater opportunities for trade in ideas and information than in goods or people.

The future of institutions and policy is more doubtful.

Perhaps the most obvious institutional and policy failure has been in liberalized and globalized finance. There were 147 banking crises between 1970 and 2011 (Laeven and Valencia, 2012), some of global significance – particularly the Asian crisis of 1997-98 and the Great Recession of 2008-09 – and the subsequent crisis in the euro area. These shocks have had huge economic and fiscal costs. Despite efforts to make the financial system more robust and regulation and supervision more effective, success remains uncertain.

Floating currencies

Closely related to the financial disorder is the monetary system. Since 1971, the global regime has been one of floating currencies, with the U.S. dollar dominant. This has proved workable. But it has also been quite unstable. Many complain that it has permitted the United States to adopt policies that cause unpredictable and unmanageable shifts in capital flows to and from hapless outsiders. Nevertheless, the unloved floating dollar standard is likely to endure, because no other currency and no other global arrangement have any hope of commanding the needed consent, at least in the near future.

Trade policy has been relatively robust, with backsliding into protectionism remarkably well contained in high-income economies. Yet the effort to complete the Doha Round of multilateral trade negotiations has essentially failed, and the future of ambitious (and controversial) plans for plurilateral trade agreements is uncertain. The high tide of trade liberalization may have passed. The growth of world trade in goods may also have slowed permanently.

Some governments are seeking to control the Internet. But the likelihood is that this effort will not halt the flow of commercial activity, though it may restrict the ability of citizens to access politically uncomfortable opinions. Meanwhile, restrictions on movement of people are likely to increase rather than fall in the years ahead.

While economies have become more interconnected, governments continue to supply security, implement laws, regulate commerce, and manage money. Where commerce flows freely, more than one jurisdiction is affected and, by definition, all involved must agree to the legal and regulatory frameworks within which transactions occur.

This contrast between the economic and political dimensions of our globalizing world is a source of unpredictability. The more commerce is to flow, the more states must agree to deep coordination of their institutions and policies, as is evident in the European Union. Such integration can also cause tension, as the euro area crisis showed. For many countries today, a comparable degree of integration remains unthinkable.

For these reasons, globalization is sure to remain somewhat limited. People trade more with fellow citizens than with foreigners. This is in part a result of distance. But it is also a matter of trust and transparency. Borders matter and will continue to do so.

Ultimately, governments must consent to openness. In doing so, they will take into account the domestic political realities. In a world of sluggish growth and rising inequality in many countries, notably high-income ones, the durability of such consent cannot, alas, be assumed. Human beings remain tribal and states remain rivals.

In 1910, at the apogee of pre-World War I globalization, British politician and journalist Norman Angell wrote The Great Illusion, which argued that war would be economically futile. He was right. Intellectually, the leaders of almost all countries now agree: conflict cannot enhance the prosperity of their nations. Yet, as the events of 1914 proved, the fact that war is ruinous does not guarantee it will be avoided, though nuclear weapons have raised the cost of conflict to unimaginable heights.

Even if peace among the great powers is maintained, the cooperation needed to secure an ever more integrated and prosperous global economy may not be. Foremost among the challenges ahead is managing the declining power of the West and the rise of China and other emerging markets. History teaches that neither technology nor economics guarantees globalization’s future in the short to medium term; only political choices do. The onus on us all is to manage the opportunities offered by globalization wisely.

Martin Wolf is Associate Editor and Chief Economics Commentator at the Financial Times. This article appears in the September 2014 issue of Finance & Development, published by the IMF.

Related News

South African citrus growers seek panel on EU black-spot dispute

Citrus growers in South Africa, the world’s biggest orange exporter, asked the government to set up an independent panel to help resolve a dispute with the European Union over the region’s stricter import requirements.

The association wants the panel to consider the merits of the findings of a report, which stated that citrus black-spot disease, a fungus that causes fruit blemishes and sometimes affects South African produce, can’t be established or spread to EU fruits, Chief Executive Officer Justin Chadwick said.

Citrus from the country, which represents about a third of all the EU’s imports, has been subject to more stringent checks to prevent the spread of the disease to the bloc, the European Commission, the EU’s administrative arm, said in May. While the International Plant Protector Convention, which aims to stop the movement of pests, has a dispute-resolution mechanism that South Africa wanted to start in 2010, it was postponed to allow the EU to do its own assessment.

“Now that it is clear that the dispute has not yet been resolved, we have asked the Department of Agriculture to resume with that IPPC process to get resolutions,” Chadwick said by phone from Hillcrest, near Durban in the southeastern part of the country. “We are asking for an expert panel to be formed, an independent panel that will consider the merits of the group that has sent the latest paper and report.”

While CBS results in leaf-spotting, it isn’t harmful to humans. The fungus can survive transport and storage and could establish itself in EU areas that produce citrus, the European Food Safety Authority has said.

“The regulations that Europe has put in place to restrict the imports of citrus are unnecessary and are without technical justification,” Vaughan Hattingh, who is CEO of Citrus Research International and was one of the contributors to the report, said by phone from Cape Town. “If the government as an exporting country wishes to challenge the import regulations that Europe has in place, they can use this document as supporting evidence for their argument.”

Related News

Civil society gathers at UN to help shape new vision for global development, prosperity

Civil society converged on United Nations Headquarters in New York on 27 August 2014 to make their voices heard regarding the future global development agenda that will point the way forward on a range of issues such as eradicating poverty, eliminating hunger and combating disease.

The 65th Annual UN Conference for Non-Governmental Organizations, on the theme “2015 and Beyond: Our Action Agenda,” brings together an unprecedented number of civil society members to discuss the way forward after the deadline for achieving the set of anti-poverty targets known as the Millennium Development Goals (MDGs).

“All of you are raising your voices for our common values. I’m deeply encouraged by this unprecedented show of interest,” Secretary-General Ban Ki-moon told the opening session in a video message.

“I depend on NGOs to push world leaders along the right path. You understand that sovereignty carries responsibility. You know that political power is a sacred duty. And you have grassroots influence that can make history.”

He said that the UN is now poised to make “monumental decisions for our world,” noting that the MDGs have achieved unprecedented success, lifting more families out of poverty, putting more children in school and preventing more disease than any campaign ever.

“I thank you for contributing to these results. I call on you to intensify progress. And I count on you to help shape a new vision for sustainable development.”

In particular, the conference – a joint effort between the UN Department of Public Information and the Executive Committee of NGOs associated with DPI – will focus on the following areas: poverty eradication; sustainability; climate justice; human rights; and partnerships and accountability frameworks.

Susana Malcorra, Chef de Cabinet in the Executive Office of the Secretary-General, told the gathering that the conference is both crucial and timely as it comes while Member States are negotiating the post-2015 development agenda.

“That new agenda will point the way forward on some of the biggest issues of our time, from eradicating poverty, eliminating hunger and combating disease to empowering women and girls, boosting health care, improving education, strengthening institutions, promoting rights, transforming economies, protecting the environment and tackling unsustainable production and consumption practices.

“Across this spectrum of opportunity and challenge, civil society needs to be heard more than ever before,” she stressed. “No discussion or negotiation of a post-2015 development agenda will succeed without your voices and input.”

This year’s conference is also timely, as it comes less than a month before the Secretary-General’s Climate Summit, slated for 23 September, and the start of the General Debate of the 69th General Assembly one day later, when world leaders will gather to discuss, among other world priorities, the post-2015 development agenda.

“We are indeed gathered here at a critical time in the post-2015 process as the international community strives to achieve the Millennium Development Goals while formulating the post-2015 development agenda,” said the Acting Head of the Department of Public Information, Maher Nasser.

He added that 2015, which also marks the 70th anniversary since the establishment of the UN, is recognized as a once-in-a-generation opportunity for global action.

“DPI is co-hosting this conference because of the tremendous importance that the UN attaches to civil society,” said Mr. Nasser. “We are committed to working with our NGO partners to ensure their voices are part of the conversation around all major global issues.”

Related News

A BRICS book to be launched

Partnership for Development, Integration and Industrialisation

The Department of International Relations and Cooperation will jointly host an event with the Embassy of the People’s Republic of China (PRC) this Friday, 29 August 2014, at which a BRICS book will be launched. All BRICS countries will be represented.

The publication consists of a compilation of thirteen peer-reviewed papers by BRICS academics along with keynote addresses and full text of the Recommendations of the Fifth BRICS Academic Forum, the Declaration on the Establishment of the BRICS Think Tanks Council and the pdf eThekwini Declaration of the Fifth BRICS Summit (1.12 MB) .

As co-chairs of FOCAC (Forum on China-Africa Cooperation) over the next three years, South Africa and China will also use the event to reflect on FOCAC affairs and implementation of the Beijing Declaration and the Beijing Action Plan (2013-2015) of the Fifth Ministerial Conference of the FOCAC, thereby injecting new impetus to the development of China-Africa relations and elevating the New Type of China-Africa Strategic Partnership to a higher level.

The year 2013 marked the 15th anniversary of the establishment of diplomatic relations between the Republic of South Africa and the People’s Republic of China (PRC). The evolution of the relationship between South Africa and China is characterised by the establishment of diplomatic relations in 1998; signing of the Pretoria Declaration on Partnership in 2000; establishment of Bi-National Commission in 2001; elevation of a Partnership to Strategic Partnership in 2004; a Programme for Deepening Strategic Partnership in 2006; as well as the signing of the Beijing Declaration on the Establishment of a Comprehensive Strategic Partnership in 2010.

South Africa and China share a sound political relationship which can be used better to lay the basis for implementing South Africa’s economic objectives. As much as China has become South Africa’s single largest trading partner in the world and South Africa, China’s largest trading partner in Africa, there is a need to work towards operationalising critical areas that have been identified in achieving South Africa’s economic objectives.

Related News

RIDMP: Funding sets SADC integration on course

The much-awaited Regional Infrastructural Development Master Plan (RIDMP) has taken off ground with the Southern African Development Community (SADC) approving US$997 million part funding towards the cause, as the region seeks to deepen integration.

The money is part of the US$500 billion mooted and approved by the SADC Heads of State and Government in Maputo during the 32nd regional summit regarding the master plan, which is intended to upgrade various infrastructural projects in the 15-member states to improve intra-trade.

In a statement issued after the 34th SADC Heads of State and Government Summit that ended on August 18, in Victoria Falls, Zimbabwe, SADC Executive Secretary Stergomena Tax said the resources would go towards various obligations needed to be undertaken in the region to support regional trade.

The SADC Council of Ministers that preceded the Summit has approved the list of potential regional infrastructure investment projects to be considered for funding under the 2015/16 annual action plan.

In the infrastructure development master plan, SADC has among other projects, roads, railways, bridges, border facilities and hydro-electricity generation, some of which have not been implemented and others have stalled due to financial issues.

Tax says infrastructure development had been identified as key to the process of regional integration and that it is one of the four priority areas in the revised Regional Indicative Strategic Development Plan (RISDP).

The other three are industrialisation and market integration, peace and security as well as special projects.

“These four programmes are inter-linked and are geared to enhance socio-economic development and eradicate poverty. You can’t enhance intra-regional trade in the region if you have no capacity to produce and add value to production. Trade must be supported by infrastructure,” added Tax.

The Council of Ministers also endorsed the decision by the Committee of Ministers to address some of the implementation changes of the SADC Free Trade Area.

Meanwhile, the SADC Secretariat has been tasked to facilitate the implementation of all pillars of the development integration agenda, which entails fast-tracking the co-ordination of measures for effective implementation of the SADC industrial development policy framework.

It will also facilitate the industrial upgrading and modernisation programme to boost the region’s productive competitiveness and industrial capacity. This is expected to bring about equity, fairness and balance in intra-regional trade, the statement adds. The planned implementation and finalisation of the development master plan for the region was initially set to run from 2014-2027, as approved by the SADC leadership during Maputo summit two years ago.

Accordingly, the RIDMP was intended to lure potential investors into the rolling-out of the Regional Infrastructure Development Master Plan Vision 2027 - a 15-year blueprint that will guide the implementation of cross-border infrastructure projects within the set period.

The RIDMP is being implemented over three 5-year intervals that include the short-term (2012-2017), medium-term (2017-2022) and long-term (2022-2027).

So far, priority infrastructure projects at a cost of about US$500 billion have been identified and the 2013 Maputo Investor Conference was part of the marketing strategy to mobilise resources for their implementation.

Other interventions include Road shows that are planned to take place in Asia and Europe.

The Master Plan is in line with the Programme for Infrastructure Development of Africa (PIDA), which is a continental initiative of the African Union Commission, in partnership with the United Nations Economic Commission for Africa, African Development Bank and the NEPAD Planning and Coordinating Agency.

Following the adoption of the Master Plan, the SADC Secretariat in collaboration with the SADC ministries responsible for the six sectors, namely Energy, Transport, Tourism, ICT and Postal, Meteorology and Water are formulating frameworks to guide the implementation of efficient, seamless and cost-effective trans-boundary infrastructure networks in an integrated and co-ordinated manner.

In the energy sector, the master plan is expected to address four key areas of energy security, improving access to modern energy services, tapping the abundant energy resources in the continent and up-scaling financial investment whilst enhancing environmental sustainability.

In the water sector, the master plan prioritises strengthening institutions, preparation of bankable strategic water infrastructure development projects; increased water storage to prepare for resilience against climate change; increasing access to safe drinking water; and enhancing sanitation services for SADC citizens, facilitating and co-ordinating the SADC Regional Water Programme.

In the sub-sectors of road, rail, ports, inland waterways and air transport networks, the plan focuses on effective regulation of transport services, liberalisation of transport markets, development of corridors and facilitation of cross-border movement, construction of missing regional transport links, corridor management institutions establishment for Beira, Lobito and North-South Corridors, and harmonisation of road safety data systems.

In the information communication technology (ICT) sector, the plan’s focus is on addressing harmonisation of SADC regional ICT policy and regulatory frameworks, SADC regional ICT infrastructure development, international and regional co-ordination; co-ordination and harmonisation of SADC ICT and postal strategic plans and programmes, facilitation of policy dialogue and implementation of the transport, communication and meteorology protocol.

In the tourism sector, strategy is geared towards achieving enhanced socio-economic development, facilitating joint marketing of SADC as a single destination, increasing tourism arrivals and tourism receipts from source markets, and developing the tourism sector in an environmentally sustainable manner.

In the meteorology sector, the plan focusses on ensuring availability of timely early warning information relating to adverse weather and climate variability impacts.

Another highlight in the meteorology sector is the development of a framework for harmonised indicators for the provision of relevant climate forecasting information to facilitate preparations of mitigation measures against droughts, floods and cyclones.

Related News

Downstream value addition is critical for radical transformation

South Africa can overcome the blockages to an inclusive productive economy with the recognition that manufacturing, with its multiplier effects, is critical to inclusive growth and job creation.

This is according to Trade and Industry Committee Chairperson, Ms Joan Fubbs. She was speaking on the first day of a three day-colloquium on beneficiation. This colloquium forms part of an ongoing oversight over the implementation of the revised Industrial Policy Action Plan (IPAP), which started in the Fourth Parliament. The Committee had found that import parity pricing and high administered prices had constrained the development of the manufacturing sector.

All of the stakeholders who participated actively shared the view that an inclusive expanding economy would be elusive until the destructive monopoly pricing of mineral feedstock was effectively addressed, high administrative input costs tackled and the implementation of the industrial policy was undertaken through a coordinated approach among the various government Departments and that regulation and competition policy was practised in a complementary and mutually reinforcing manner.

Value addition, particularly of mineral resources and other natural resources, is directly correlated with job creation, especially in downstream value addition. Several stakeholders pointed out that import parity pricing and other factors limited opportunities for expanded beneficiation. The Competition Commission of South Africa emphasised that “the advantages of those controlling minerals and production of derivative products are not flowing through competitive prices for downstream industries”.

The Industrial Development Corporation (IDC) underlined the accelerated shift towards a rapid sustainable and inclusive development in the primary beneficiation of raw materials and the critical need to develop industry wide value chains. The IDC said they totally supported the Department of Trade and Industry’s (DTI) “call for increased local content in components, vehicles, and the establishment of a multi RSA OEM automotive assembly plant,” which targeted 1 500 jobs and could reduce import leakages. It also pointed to the resuscitation of foundries and Tool, Die and Mould (TDM) industries by 2020 to further support beneficiation initiatives.

Three issues needed to be considered when addressing industrialisation. The strengthening of material resources as the building blocks for industrial development, the need for the Committee to check on where South Africa fitted into the global value chains and thirdly given our commitment to development the need to diversify and focus on exports where the country has an export competitiveness.

Ms Fubbs said the ensuing discussion was robust and proposals included the introduction of domestic pricing controls on strategic minerals, alignment of beneficiation strategies, a review of licensing conditions and recognition of the role infrastructure played, and an industrial policy implementation task-team that will ensure that there is coordination of beneficiation efforts among the stakeholders.

“There is a clear link between behaviour of upstream firms and the costs of downstream firms,” said Professor Simon Roberts of the University of Johannesburg. He added that with respect to plastics, the cost of polymers in South Africa, although not the only input was the largest costing 40% to 60% and had a serious impact on price competitiveness.

Independent expert, Dr Paul Jourdan, called for the introduction of a “resource Rent Tax” (50% on returns above normal ROI) as well as the “amendment of the Mineral and Petroleum Resources Development Act (MPRDA) objectives to include maximisation of the developmental impact of mining to allow for back and forward linkages conditionality and minimum RDI spend.”

The South African Mining Development Association called for unencumbered ownership that would realise through the alignment of the B-BBEE with the Mining Charter the vision of the National Development Plan for 2030. It also pointed to the need to address Transfer Pricing to encourage the aggressive pursuit of a developmental pricing agenda.

Currently, South Africa’s largest exports are mineral resources, yet the country imports processed or finished goods manufactured from these very same resources but at substantially higher prices. It is critical that the country changes this reality.Said Ms Fubbs: “We need to move up the value chain and add value to the country’s mineral and natural resources. Mineral resources have been identified as potential key drivers of industrialisation”. Mineral resources include polymers, ferrous metals, platinum group metals and titanium; while natural resources include primary agricultural, forest and fishery products. However, other areas of value-addition are also possible through technological developments and the advancement of the knowledge economy in advanced manufacturing sectors such as the software and aerospace industries.

This conversation on beneficiation continues as the Committee goes on day 2 of the colloquium. The focus will be on iron ore-steel and polymer value chain. Participants will mainly be companies in this sector.

Related News

Time for Singapore to make Africa a priority

This week, the government of Singapore will be hosting its third Africa-Singapore business forum. The forum will bring African private and public sector leaders to Singapore to discuss investment opportunities across the continent. But the forum could also serve a more strategic purpose by encouraging a broader evaluation of Singapore’s relationship with the continent.

Today, China is by far the most active Asian player in Africa. But with the right approach, Singapore could be at the forefront of Asian engagement – even supplanting China.

China’s trade with Africa will total almost US$300 billion this year. Accurate figures for foreign direct investment (FDI) are more difficult to find, but here, too, the numbers are surely quite high – with multi-billion dollar investments in infrastructure, resources, and manufacturing spread over a large number of African markets. And this does not include the more than US$75 billion Beijing has committed to Africa over the past decade.

But this investment has not created positive feelings in Africa towards China. I spent the past two years living in Ethiopia and travelling to other countries in the region. During my time on the continent, I frequently heard government officials resentfully complain about the heavy-handedness with which the Chinese government has been flexing its political muscle.

African businesses, meanwhile, argue that Chinese companies do not abide by their contractual obligations. And African consumers regularly deride the poor quality of Chinese products that find their way into the marketplace.

Singapore’s brand, by contrast, is very strong. Most African leaders are familiar with Singapore’s story. Many have even explicitly stated that they would like their country to become the Singapore of Africa. Their desire to do so makes sense: the top priorities for most African countries include achieving rapid economic growth, maintaining political stability, and ensuring a safe environment in the face of terrorist threats, crime, and regional conflict. In the context of such goals, the Singaporean model seems very attractive.

Singapore is relevant to Africa for other reasons, too. First, many of the sectors in which Singapore excels are the same sectors in which Africa is arguably in greatest need of investment. These include shipping, seaports, airports, energy, financial services, and water sanitation, among many others.

Second, because Singapore is a small country, African leaders do not view it as posing a strategic threat. They would therefore not be concerned if Singaporean companies won tenders for projects of strategic significance, such as deep-sea ports and other vital infrastructure.

Third, Singapore serves as the key gateway to Asean. So, even though Singapore would not be able to match China in terms of overall trade and investment volumes, its ability to unlock the potential of the greater Asean region can multiply its significance in Africa many times over.

Of course, it is not as though Singapore is unaware of Africa. Indeed, Singapore’s trade with Africa has been growing at over 10 per cent per year, and reached approximately US$11 billion in 2013. Singaporean FDI into Africa now stands at over $16 billion.

The point, however, is that Singapore has the potential to put in place a strategic partnership with Africa that could go far beyond merely achieving incremental increases in trade and investment.

Such a partnership would require a concerted and cross-functional effort on the part of the Singapore government. An interesting way to launch that effort would be for Singapore to host a high-profile summit for African leaders aimed at providing tools on how to apply the Singaporean model in an African context.

Thereafter, the Singapore Cooperation Programme, the primary platform through which Singapore offers technical assistance to other countries, could announce bold new initiatives aimed specifically at Africa. At the same time, the Singapore government might consider enhancing the resources available to International Enterprise Singapore (IES). This is the government agency charged with spearheading the overseas growth of Singapore-based companies and promoting international trade. With additional resources IES could achieve greater coverage across the African continent and also help market Singapore as the gateway to Asean.

Finally, the Singaporean government could – perhaps in coordination with the United States – consider looking at potential areas of security cooperation in the areas of counterterrorism and counternarcotics, among others.

Such a combination of steps would help to establish substantial goodwill at the government-to-government level, build key relationships, and increase private sector exposure to opportunities in Africa. All of this, in turn, could have a truly transformative effect on the level of engagement between Singapore and Africa.

With six of the world’s 10 fastest growing economies, a population of over one billion that is expected to grow to four billion by 2100, and many other factors in its favour, Africa is poised for a breakout century. Singapore should seize the opportunity to establish a strong foundation for a lasting partnership.

Alexander Benard is COO of Schulze Global Investments, a private equity firm focused on frontier markets and headquartered in Singapore.

Related News

Namibia to sign SADC Protocol on Trade in Services after ‘internal consultation’

Minister of Trade and Industry, Calle Schlettwein, has rubbished reports as “factually incorrect” by some local media houses who have accused Namibia of refusing to sign the Southern African Development Community (SADC) Protocol on Trade and, or the SADC Protocol on Trade in Services at the recent SADC Summit in Victoria Falls, Zimbabwe.

“Namibia has signed and ratified the SADC Trade Protocol, which establishes the SADC wide free trade area. Namibia was in fact one of the founder signatories of this protocol and remains a strong proponent of strengthening inter-SADC and inter-Africa trade. Namibia is the second strongest SADC country in respect of inter-SADC and inter-Africa trade following South Africa,” explained Schlettwein in parliament last week.

Regarding the SADC Protocol on Trade in Services, which was adopted in 2012, Schlettwein clarified that Namibia will only consider committing to it once the country has comprehensive information available and only when it has concluded its internal consultation with stakeholders in all the identified service sectors.

This protocol is comprised of the protocol itself and a number of annexes which will contain the details as to which sector and to which level different service sectors would be liberated. The sectors that were identified as priority service sectors to be liberated are financial services, energy, construction, communication and tourism, some of which are regulated in Namibia.

“Most of these annexes are still under consideration and SADC member states are negotiating the offers to be made. At the time when the protocol was adopted Namibia indicated that it needed more time to consider the protocol together with its annexes so as to have the whole picture before committing to it,” explained Schlettwein.

During the recent SADC summit in Zimbabwe the master of ceremonies of the closing session, in line with SADC tradition, placed before Heads of State and Governments all adopted protocols that had not yet been signed. Namibia indicated that she was not yet ready to sign the Protocol on Trade in Services.

Related News

EAC boss roots for a 24-hour-regional-economy

The East Africa Community Secretary General Dr Richard Sezibera has advised regional private and public sector players to consider embracing the ideals of a 24-hour-economy to accelerate economic growth.

The East Africa Community boss, who was speaking at the launch of regional retailer, Nakumatt Holdings, 50th branch opening in Arusha, Tanzania over the weekend noted that the region’s reliance on an 8-12-hour economic production cycle is slowing down regional growth.

The branch which represents a US$2 million investment by Nakumatt is also a major milestone for the retailer, as it had earlier set a corporate target to open its 50th branch by February 2015 under its Nakumatt 2.0 Corporate Development Strategy.

On his part, Dr Sezibera noted that, in the face of globalization, East Africa’s economy, cannot afford to remain shut overnight as other competing economies in the world operate round the clock.

“At the East Africa Community, we are working hard to support economic development by clearing Non-Tariff barriers and on the same vein, we are actively working to encourage both the private and public sector to adopt a 24 hour approach to business and service delivery,” Dr Sezibera confirmed.

“Companies such as Nakumatt has played a key part in fostering innovative practices such as their round the clock operations which can be easily emulated by other private and public sector players,” he added.

He further commended homegrown business organisations such as Nakumatt for playing a key role in driving regional integration. Retailers and finance institutions’ he noted have been at the forefront in building a significant regional presence.

During the function, Nakumatt Holdings, Managing Director Atul Shah, described the opening of Nakumatt Arusha as a golden jubilee milestone as it now ranks as the 50th branch in East Africa. The new branch located, at the Tanganyika Farmers Association shopping complex in Arusha, Tanzania, also sets the pace for the retailer’s renewed growth plans in the region and beyond.

Across the region, Nakumatt has been at the forefront in the promotion of regional retail trade integration and currently operates 8 branches in Uganda, 3 in Tanzania and 2 in Rwanda alongside its 37 Kenya stores.

He further reiterated Nakumatt’s commitment to support the growth of formal retail in East Africa by playing a mentorship role. Plans, he added are already underway to transform some of Nakumatt Tanzania branches into 24 hour outlets.

“My dream is to ensure that we double the formal retail penetration in East Africa from the current less than 14% to at least 30% in the next ten years,” Shah said. And added: “Such growth for formal retail sector will require concerted efforts amongst all stakeholders and will in turn inspire regional growth. My dream is to see thousands of farmers and other cottage industries accessing formal retail markets such as Nakumatt.”

Alongside the dream, Shah further expressed his personal ambition to see the East African countries host the 2030 Football World Cup.

“As East Africans we must embrace a common vision to inspire regional development and foster social cohesion. In my view, nothing does this better than a common dream to host a global soccer bonanza,” he said.

Currently enjoying a more than US$600 million turnover for its regional operations, Shah confirmed that Nakumatt’s future looks bright with its pan African expansion plans now trained on such markets as Botswana, Zambia, South Sudan and Burundi among others.

With the opening of Nakumatt Mlimani, Nakumatt Pugu road and Nakumatt Arusha, Shah pointed it out that Nakumatt now has four running stores in Tanzania. The three new stores are the latest additions to the existing Nakumatt Moshi store which opened its doors in 2011 in the bustling town at the foot of Mt Kilimanjaro.

In Kenya, Nakumatt is also gearing up for the opening of two new stores in Kenya by the end of the year.

Alongside the store openings, Nakumatt is also actively enhancing its private brands (Nakumatt Select and Nakumatt Blue Label) roll-out across the East Africa region.

Related News

Weak exports push Uganda’s trade account deficit to Shs613 trillion

Weak commodity exports amid increased importation of goods and services into the country have worsened Uganda’s trade balance.

The Central Bank State of the Economy report for August states that Uganda’s trade balance continues to deteriorate on account of stagnant exports and high import requirements.

This implies that Uganda’s trade position with the rest of the world is not favourable and the country is spending more on imports than it is earning from exports.

According to the report, Uganda’s trade deficit fell by 11.4 per cent, implying that total trade deficit stood at $2.123 billion (about Shs550.918 trillion) in 2012/13. However, in the financial year 2013/14, the deficit rose to $2.365 billion (about Shs613.717 trillion).

The executive director of research, Bank of Uganda, Dr Adam Mugume, said during the period under review, private consumption imports decreased by $6.9 million (about Shs17.905 billion) to $352.5 million (about Shs914.737 billion).

“Exports earnings as a share of Gross Domestic Product (GDP) declined to 11.4 per cent from 13.6 per cent in Financial Year (FY) 2012/13 and 15.4 per cent in FY 2010/11,” he said.

Dr Mugume added: “Imports expenditure as a percentage of GDP declined to 21.5 per cent from 23.5 per cent in FY2012/13, but could have actually been higher had the implementation of the Karuma project not been deferred.”

The Central Bank report shows that external sector imbalances continue to persist. In FY 2013/14, the current account deficit is projected at $ 1.63 billion (about Shs2.758 trillion) which is about 8 per cent of GDP from $ 1.72 billion (about Shs2.781 trillion) in 2012/13. The deficits on the trade account and income account more than offset the surplus on the services and foreign transfers.

In quarter two of 2014, the current account deficit increased by 32 per cent to $435.8 million (about Shs11.309.trillion) driven mainly by a larger deficit on the trade and income account.

Going forward, the Central Bank anticipates that imports are expected to increase as government infrastructure projects commence and private agents stock up for the December festive season.

In an interview with Daily Monitor on Friday, the managing director of Alpha Capital, Mr Stephen Kaboyo said: “Looking at the Balance of Payment (BOP) position, you clearly see the trade imbalance, indicating that the country is running a huge current account deficit.”

Weak shilling

The war in South Sudan has also put pressure on Uganda’s export performance. Uganda’s weak export performance in part reflects the depreciation of the Uganda Shilling relative to other regional currencies, particularly the Kenyan Shilling and Congolese Franc.

Related News

Harnessing Mauritania’s natural resources to promote economic growth and sustainable development

Sound management of natural resources in Mauritania has the potential to spur further economic growth and build a foundation for sustainable development in the country, according to a new World Bank Group report released today.

In the first Mauritania Economic Update, the World Bank analyzes current macroeconomic trends and identifies ways to help a resource-abundant country like Mauritania to address the challenges of achieving inclusive socioeconomic development.

“A resource-rich developing economy like Mauritania, with its high growth rates, can become one of the success stories in Sub-Saharan Africa. The country has considerable untapped potential and, with the ongoing diversification agenda and efforts to increase productivity, can rapidly achieve sustainable and inclusive development,” says Vera Songwe, Country Director for Mauritania.

Mauritania’s economy grew robustly at 6.7% in 2013, backed by a thriving mining sector, a strong rebound in agriculture, and expansions in services. The mining sector represents roughly one-fourth of GDP, almost 20% of total revenues, and more than half of total exports.

The country recently graduated as lower-middle income country thanks in large part to its considerable endowment of natural resources. A continuation of these relatively robust growth conditions is anticipated over the next three years, as the economy benefits from a continued expansion of mining output, particularly of iron ore.

The challenges of inclusive growth, economic diversification, and resource utilization efficiency

Mauritania has succeeded in increasing per capita income over recent years, thanks to a natural resources boom. However income distribution has remained relatively unchanged for the last two decades and the challenges of unemployment – especially for the under 35 and those living in rural areas – remain daunting.

“For a considerably endowed country like Mauritania, good management of natural resources is essential to ensuring that growth is shared.

“Mauritania should continue on the path of productive investments in the energy and infrastructure sectors, as well as in improving social spending and public services delivery, particularly in health and education,” says Gianluca Mele, Country Economist for Mauritania.

Policy makers in Mauritania face a difficult trade-off between responding to the immediate needs of the population and making investments to prepare for a future when non-renewable resources are exhausted or less readily available. According to the report, the key policy question facing the country is how to set up a foundation for long term growth given that an important portion of the country’s wealth stock is progressively and unavoidably being eroded.

Local worker at the artisanal fishing port of Nouakchott.

Recommendations

In addition to highlighting the importance of continuing to improve the efficiency of resource utilization, the update offers four areas of policy focus that could help Mauritania unleash its growth potential:

Considering the establishment a savings mechanism for stabilization and inter-generational transfers: The possibility of keeping at least a portion of natural resources revenues in a sovereign wealth fund should be carefully scrutinized. Mauritania counts on a successful precedent, that of a crude oil fund created in the mid-2000s, which today accounts for approximately $115 million (equivalent to almost 3% of GDP).

Investing resource revenues domestically: Fiscal analysis of Mauritania reflects a recent policy shift in this direction. Public expenditure appears to be reoriented toward areas such as energy and transportation infrastructure, as well as toward phasing-out subsidies and abandoning a reactionary approach to crises in favor of systematic methods to handle external vulnerabilities such as food crises.

Strengthening public financial management: The Government of Mauritania has recorded positive improvements in fiscal consolidation, such as a revamped coordination between customs and fiscal authorities, a tax base expansion (tax revenues moved from 14% GDP in 2009 to over 22% in 2013) and increased visibility of budget data through the adoption of the BOOST platform in 2014. Mauritania should continue consolidating public finance management by strengthening the efficiency of medium term expenditure frameworks (MTEFs), and by streamlining public procurement procedures.

Enhancing the quality of public services and fostering transparency in the public sector: While Mauritania has registered remarkable achievements in primary enrollment and gender balance in schools, more needs to be done to improve the quality of health-related services, as maternal and infant mortality Millennium Development Goals (MDGs) appear to be largely out of reach. It is also critical that the country commits to ensuring that the selection processes within the public sector follow transparent paths built on meritocracy, and that statistical intelligence is produced and disseminated regularly.

Related News

High noon for India in Africa

As India plans to host the third India-Africa Forum Summit in December, the implications of a similar event that took place in Washington earlier this month should not be lost on us

Our news media’s constant focus on the United States notwithstanding, it seems to have completely missed a historic move earlier this month by President Barack Obama with potentially serious implications. From August 4 to 6, he hosted the first ever ‘U.S.-Africa Leaders Summit’ in which over 45 of Africa’s heads of states participated. In his welcome address, President Obama leveraged his own African lineage by telling them that apart from being a proud American, he also stood before them “as the son of a man from Africa.”

The summit had an unambiguous economic focus. During its three days of deliberations, U.S. ‘commitments to Africa’ worth $33 billion were announced. These included: $14 billion in investment by U.S. companies; $7 billion to finance U.S. exports; and $12 billion for a ‘Power Africa’ initiative to boost electricity availability. Over 90 American companies participated in the summit.

Cynosure of many eyes

Because of its vast natural resources, acute infrastructure deficit, high population growth and growing middle class, Africa has long been a cynosure of many eyes. Countries such as China, India, Japan, Brazil, Turkey and South Korea, as well as organisations such as the European Union (EU), the Commonwealth and La Francophonie, have been regularly hosting Africa-focussed summits. The U.S. is the latest to join this Africa rush.

It would, however, be incorrect to consider Washington a latecomer to the ‘Africa Party.’ Historically, the slave trade provided an umbilical cord between the U.S. and Africa. Bilateral landmarks include American Friendship Treaty with Tunisia in 1799 and establishment of Liberia in 1821. They also include American support for Apartheid regime in South Africa and for right wing dictatorships in countries from Morocco to Congo to Angola during the Cold War. Subsequently, the U.S. did help in the dismantling of Apartheid and getting Namibia its freedom.

In 2007, the U.S. Army created the Africa Command (Africom), which has been steadily expanding its presence in the continent. Lately, however, Pentagon has been alarmed, in the aftermath of the Arab Spring, at the spread of Islamic terrorism across large swathes of Africa: Maghreb, Sahel, Nigeria, the Central African Republic and Somalia.

Economically, the American presence in Africa has been large but is currently declining. Till 2008, the U.S. was Africa’s largest trading partner. This was spurred by import of African oil worth over $100 billion – part of U.S.’ strategy to reduce dependence on the Gulf. However, thanks to a shale revolution, the U.S. has become the world’s largest oil producer and its oil imports from Africa are set to plummet to a mere $15 billion for the year 2014. This has dramatically reduced U.S.-Africa trade to around $60 billion in 2013, nearly a third of China’s trade with Africa. If this trend continues, India may well overtake the U.S. as Africa’s second-largest trading partner this year. However, the U.S. still remains Africa’s largest aid provider and a major investor.

Against this backdrop, many observers see the Washington Summit as a U.S. bid to find new economic paradigms for its Africa profile to catch up with China and other stakeholders on Africa. The sceptics, however, point out that with U.S. economy still in recovery mode, no early surge in American demand for African raw materials is likely.

Further, the U.S. products, services and technology are often either unsuitable or too expensive for Africans. Its Asian competitors have an edge here, in industries ranging from mobiles to medicines. The U.S. niche areas for Africa include: export of commodities (foodstuff, refined products); supply of equipment (for power, aviation, construction etc); and projects for mineral exploitation, hotels and hospitals.

Following the Chinese strategy

A closer look at the Washington Summit’s outcome also reveals that the U.S. intends to follow the Chinese strategy of long-term soft funding for Africa. Beijing has for long provided concessional loans to African countries to cushion them from the lower quality (and higher costs) of its products and projects; the U.S. and American MNCs would possibly do the same. For most African governments facing a serious capital crunch, such long-term soft loans are often irresistible. Second, with many African states facing serious security challenges, the U.S. may also leverage its Africom umbrella to gain an economic advantage.

As New Delhi plans to host the third India-Africa Forum Summit (IAFS-3) in December 2014, what are the implications of the Washington event for us?

First, forceful re-entry of the U.S. and its deep-pocketed MNCs may lead to a more intense and potentially unfair competition in Africa. Second, greater U.S. engagement in infrastructure building may release synergies in Africa that we can leverage. For example, better roads can mean more Indian vehicles being sold. Third, if American MNCs increase production of primary commodities in Africa, it may benefit India as their end-user. Fourth, Indian subsidiaries of the U.S. MNCs stand to gain.

Finally, over the past 15 years, India has successfully created some key interfaces in Africa in areas such as power, Information and Communications Technology, and healthcare. A U.S. entry into these may affect market access for us. Africans, who have often played the China card with us, could now play the U.S. card as well.

India would do well to prepare IAFS-3 with a Strengths, Weaknesses, Opportunities and Threats (SWOT) review of the past six years of the IAFS process. The following domains suggest themselves:

-

Being a developing country with income level comparable to most African nations, India cannot sustain the IAFS process on the basis of freebies alone. Instead, African countries should be invited to become co-stakeholders in the process.

-

While the African Union Commission can be a political umbrella for the IAFS process, India should, on its own, choose both the recipients for our developmental cooperation and the manner in which we plan to extend it. We must not abdicate this important task to the African Union (AU) bureaucracy.

-

There is a need to revamp the Line of Credit approach to projects as it has rarely delivered the intended results. Instead, greater support should be given to private sector-driven projects through initiatives like lower interest rates, risk mitigation, etc.

-

We should harness our assets in Africa, such as the Indian diaspora there; a growing acceptance of the quality of our healthcare and educational facilities; relevance of our developmental model; and the greater willingness of our private sector to engage the continent.

Mahesh Sachdev retired last year as India’s High Commissioner to Nigeria. His book, Nigeria: A Business Manual, was published last week.

Related News

Zim, China sign nine mega deals

Zimbabwe and China yesterday signed nine landmark agreements that will see the emerging global giant from Asia providing financial support for the much-needed economic enablers in critical sectors that include energy, roads, national railway network, telecommunications, agriculture and tourism as part of the Zimbabwe Agenda for Sustainable Socio-Economic Transformation.

One of the four pillars of Zim-Asset is the Infrastructure and Utilities cluster which spells out a number of major projects to revive the economy by rehabilitating, upgrading and building key physical as well as social infrastructure and utilities to enable the turnaround of the economy and create business and employment opportunities.

Funding was, however, a major challenge to achieving the goals of the Infrastructure and Utilities cluster, but thanks to close to a year of thorough negotiations that included several visits to Beijing by Zimbabwean officials and Cabinet ministers, nine solid funding commitments were made yesterday by the Chinese government in a development that is set to open a new page in the transformation of the economy by funding key infrastructure projects that create jobs and spur economic growth and development.

Government ministers from the two countries under the watchful eyes of Presidents Mugabe and Xi Jinping become the second major, cluster-specific statement since the launch of Zim-Asset last October; the first being the US$180million agriculture support facility that has since scored dividends for the Food Security and Nutrition Cluster which has ushered the country towards a path of national food self-sufficiency within the first year of the new Government that was sworn in on September 11 last year. The development impact of this agriculture input support facility on economic factors such as employment creation is yet to be assessed.

Finance and Economic Development Minister Patrick Chinamasa signed two master loan agreements with the China Export and Import Bank and the China Export and Credit Insurance Corporation. Minister Chinamasa told The Herald after the signing ceremonies that the agreements provided securitisation framework for infrastructural and productive sectors.

“We have signed agreements which provide securitisation framework under which projects in infrastructural and productive sectors can be funded,” said Minister Chinamasa.

“The agreements with the China Exim Bank puts into place a framework under which we can secure funding for projects in the productive and infrastructural sectors on a case by case basis that also puts into place securitisation framework on the basis of which we can then submit projects for funding. But that funding will only come from China Exim Bank.

“The agreement with the China Export and Credit Insurance Corporation is also providing securitisation framework for infrastructure and productive projects that can be funded by both the State and non-State financial institutions. It’s opening up other sources of funding. These projects will be anchored on securitisation.”

Contrary to media reports that Zimbabwe was to securitise the funding of the agreed projects with minerals, the fact is that no sub-soil assets were used to securitise the commitments whose security is enterprise-based and commercially pegged to the performance and cashflows of the state enterprises concerned be it Zesa, NRZ, NetOne, Zinara etc.

Minister Chinamasa said only viable projects would attract such funding, adding that the Zimbabwean delegation was not in China to look for budgetary support contrary to reports in some sections of the media.

“No country sets aside a lump-sum payment for no specific projects,” he said. “Projects must demonstrate their ability to pay for themselves. You will not come to China to ask for money to invest in a project that won’t pay for itself. That would not make economic sense”.

Minister Chinamasa said he also signed another agreement on economic and technical cooperation on provision of emergency food donation by the Chinese Government to the Government of Zimbabwe and a concessionary loan agreement for the NetOne Network Expansion Phase Two project.

Foreign Affairs Minister Simbarashe Mumbengegwi signed another agreement on behalf of the Zimbabwean Government on mutual exemption of visa requirements for holders of diplomatic and service passports. He also signed another agreement on the confirmed minutes of the Ninth Session of the Joint Commission of Economic, Technical and Trade Cooperation that met from August 21 to 22 in Beijing ahead of President Mugabe’s state visit to China.

Tourism and Hospitality Industry Minister Walter Mzembi signed an agreement between his ministry and the National Tourism Administration of China on cooperation in the field of tourism whose implementation will lead to an increase of revenues from Chinese visitors to Zimbabwe.

Related News

Nigeria waiting for G-20 deal on ‘bail-in’ bond for banks

The Federal Government and the Financial Regulatory Authority may tap into the G-20 proposal that will require the top banks in the country to issue special bonds as capital that can assist them in times of crises. Sources close to the Presidency disclosed that if the G-20 proposal scales through, Nigeria will take a cue from it.

In the international financial community, government leaders are expected to agree in November after the IMF/World Bank meeting in October that the world’s top banks must issue special bonds to increase the amount of capital which can be tapped in a crisis instead of calling on taxpayers to come to the rescue.

The bonds, to be known as “Gone Concern Loss Absorption capacity” or GLAC, are seen by regulators as essential to stopping the world’s biggest lenders from being “too big to fail,” Reuters reported.

According to international financial sources, the plans are being drafted by the Financial Stability Board, the regulatory task force of the Group of 20 economies which declined to comment ahead of a G20 summit in November, when G20 leaders will discuss the reform before it is put out to public consultation.

The reform would put in place the final major piece of G20 regulation on banking as the global body turns to a “post-crisis” agenda of fostering economic growth and bedding down the rules it has approved. There had been unease in Asia and parts of Europe over how big the bond issues need to be to provide this cushion but there is now a new optimism amongst bankers and regulators that the G20 will reach a deal in November. “The industry is definitely in favour of making resolution, supported by an appropriately flexible concept of GLAC, work. That is the key pending aspect on ending too-big-to-fail,” said Andres Portilla, director of regulatory affairs at the Institute of International Finance, a Washington-based banking and insurance lobby.

“What is likely to happen is that there will be a consultative proposal, but without all the detail that a lot of people would like,” Portilla added. However, a G20 source said a deal was not only expected but would also be more detailed than some parties anticipate, which is essential for conducting a thorough impact assessment before finalizing the rules.

“The authorities and the FSB are working to have a proposal that will contain sufficient granularity of numbers to be a meaningful consultation and quantitative impact study to calibrate the final rule,” the source said.

Top banks expect they will have to hold GLAC bond capital equivalent to about 10 per cent of their risk-weighted assets on top of their core capital buffers which currently stand at around 10 per cent. But they hope for some leeway if they can show that they can already be wound down smoothly in a crisis because of simplified structures.

The G20 source poured cold water on this, saying regulators believe all the world’s top 29 banks earmarked for tougher supervision will need a significant cushion of such so-called “bail-in” bonds for some time to show they can be shut without public aid.

Regulators ultimately want to price bank debt better and end the cheaper funding that too-big-to-fail banks enjoy because markets assume governments would never allow them to collapse.

Efforts by the authorities so far are having an impact. “We have been lowering our systemic support assumptions for banks or changing their outlooks to ‘negative’ to reflect the ongoing effort by governments to try to eliminate that support,” said Johannes Wassenberg, managing director of banking at Moody’s credit rating agency in Europe.

In May, Moody’s lowered its outlook to ‘negative’ on more than 80 banks in the European Union after the bloc approved a law requiring banks to hold a buffer of potential bail-in debt like GLAC.

“Adopting GLAC is the final chapter in reforming the condition of banks,” said Thomas Huertas, a former UK banks supervisor and now a regulatory consultant with EY.

The plans for bail-in bonds are among the last of what G20 officials call the “heavy lifting” on banking industry reforms that came in the aftermath of the financial crisis.

With much of the work on defining how to make banking safer completed, the G20’s focus will shift to implementation of its rules and behaviour at banks after lenders were fined for rigging the LIBOR interest rate benchmark, with similar allegations in the currency markets now emerging.

Related News

‘Movement restrictions over EVD hurting sub-regional economy’

Containment efforts in Nigeria lower impact

Business activities across the West African countries may have been gravely affected by the spread of the deadly Ebola Virus Disease (EVD), due to limitation of movements at the borders.

The indications from the Borderless Alliance, recently suggested that the West African countries have been losing huge revenue due to limitations to cross-border businesses across the region.

However, the current containment efforts in Nigeria have limited the pangs of the disease on the nation’s economy.

Indeed, the Economic Community of West African State (ECOWAS), recognizing this fact, has described the Ebola outbreak in West Africa as not only a health emergency but a “destructive element” in the region’s march towards socio-economic development.

The Borderless Alliance, in a statement signed by the President of its Executive Committee, Ziad Hamoui, advised its “members who are engaged in regional trade and transport, to exercise the highest levels of precaution, in order to ensure the safety of their personnel and their families at all times. Member organizations are, hereby, requested to instruct their representatives to adhere to all required health and safety guidelines, especially while completing formalities or crossing borders,”

Borderless Alliance is an institution of a multi-lateral partnership of private and public sector stakeholders working to increase trade in West Africa, and eliminate barriers to trade.

Hamoui said that, in order to prevent unnecessary health risks to its operational team, Borderless Alliance has suspended temporarily, some of its already planned activities in the affected countries, pending visible improvements of the situation in those countries.

African countries tightened travel curbs in recent times in an effort to contain the Ebola outbreak, ignoring World Health Organization warnings that such measures could heighten shortages of food and basic supplies in affected areas.

The group however, said its Border Information Centers across the region, would make available printed material for distribution to economic operators at the border crossings.

“Finally, and while we do not wish to overstep our mandate as a regional advocacy group that promotes economic integration and targets trade barriers, we stand ready to collaborate with relevant stakeholders, as well as regional authorities, within our capacity and if deemed necessary.

“Borderless Alliance offers its condolences to the victims of this recent deadly outbreak. We express our full support and solidarity with all regional governments and the people of West Africa, in their efforts to contain this danger and bring things back to normalcy. Trade facilitation will help the affected areas and people recover after this crisis has passed,” he stated.

The Vice President of the ECOWAS Commission, Dr. Toga Gayewea McIntosh said “this is a community challenge that can only be faced through solidarity, working together and integrating our responses.”

The disease has claimed more than 900 lives since its outbreak in the region in March 2014, with most of the deaths reported in Guinea, Sierra Leone and Liberia, and five in Nigeria.

As precautionary and preventive measures, ECOWAS has also suspended its meetings involving officials from member states while its Lagos Liaison Office has been disinfected.

The vice president said a Solidarity Fund has been set up to enable the region combat the outbreak, as ECOWAS continues to work with member states to defeat the disease.

Related News

Addressing SPS issues in the SADC region

Regional Economic Integration Support (REIS) Programme, funded by the European Union, has been a catalyst for the rapid development of Sanitary and Phytosanitary (SPS) management in the region over the past fifteen months. Aimed at facilitating the improvement of trade in agricultural commodities within the region and internationally, fostering compliance with regional and international multilateral trade agreements and creating awareness of SPS measures amongst farmers and agro-food processors; the Programme is supporting meetings of the regional SPS Coordinating Committee (SADC SPS CC), the Livestock Technical Committee (LTC), the Plant Protection Technical Committee (PPTC) and the Food Safety Technical Committee (FSTC); and it is also facilitating workshops to raise awareness on SPS issues amongst food and agriculture stakeholders.

SADC’s approach to SPS management is based on provisions of the World Trade Organization (WTO) Agreement on the Application of SPS measures (or the ‘WTO SPS Agreement’ for short) which are mirrored in the SPS Annex to the SADC Protocol on Trade.