All News

Annual EAC Secretary General’s Forum for Private Sector, Civil Society and Other Interest Groups Opens in Entebbe Friday

Uganda’s Minister for East African Community (EAC) Affairs Hon. Shem Bageine will officially open the annual EAC Secretary General’s Forum for Private Sector, Civil Society and Other Interest Groups at the Imperial Resort Beach Hotel on Friday, 12th September, 2014.

This year’s theme is: “EAC: My Home, My Business”.

Over 100 delegates from the Partner States are expected to attend the two day event; the third in series since 2012. The first was held in Dar es Salaam, United Republic of Tanzania, and second was last year in Nairobi, Republic of Kenya.

The delegates will be drawn from the Partner States’ Private Sector Organizations (PSOs), Civil Society Organizations (CSOs), professional bodies, academia/universities, media, EAC organs and institutions, development partners and other interest groups.

The EAC Deputy Secretary General (in charge of Productive and Social Sectors), Hon. Jessca Eriyo, said that the Forum’s objective was to provide a platform for regular dialogue between the EAC Secretary General and the Private Sector, Civil Society and other interest groups on how to improve the EAC integration process.

“The 3rd Forum is an opportunity to widen and deepen EAC integration process and ensure stakeholder participation and inclusivity,” according to Hon. Eriyo.

She added: ”The Forum will provide a space to dialogue on opportunities and challenges provided by the Regional integration process as well as share experiences.”

Professor Yash Tandon from Uganda, a renowned intellectual and policy-maker among others, will give a key note address on the Forum’s theme. Prof Tandon is the former Executive Director of the South Centre; a think tank founded by leaders of the South, among them China, India and Brazil. Tanzania’s Founding President Dr Julius Nyerere was the first Chairman of the Centre.

Other papers to be tabled at the Forum include: “Post 2015 EAC Development Agenda”; ”The Rights and Freedoms under the EAC Common Market Protocol”; “Food Security, Climate Change Mitigation and Adaption” and; “Enhancing the Competitiveness of the EAC”, among others.

The Forum’s Regional Dialogue Committee has been working hard for over five months to ensure the success of the Conference.

The Forum’s symbolic kick-off is tomorrow, Thursday 11th September, 2014 with a community service and sensitization at the Nakiwogo Market, Entebbe.

Later delegates and members of the public will engage in cleaning up exercise of the Market. A voluntary HIV/AIDS counseling and testing will also be conducted; courtesy of the Entebbe Municipal Health Department.

The East African Business Council (EABC) is tasked to lead organization of this year’s Forum.

Background

The Dialogue Framework Forum for Private Sector, Civil Society and other interest groups in the EAC integration process was endorsed by the EAC Council of Ministers at its 26th meeting in November 2012 in Nairobi, Kenya.

The Forum is guided by the principles of cooperation for mutual benefit, trust, goodwill, active and constructive participation, inclusivity and respect for diverse views.

Related News

Effective marketing, perception management needed for FDI

The much-needed foreign direct Investment (FDI) required to revive the country’s ailing industry can best be attracted through effective marketing and perception management, an official with the Zimbabwe National Chamber of Commerce (ZNCC) has said.

The international investment community has continued to withhold direct capital inflows primarily citing lack of policy clarity.

This scenario has partly led to a nationwide scaling down and, in many cases, shutting down of industries compounded by an acute liquidity crunch.

ZNCC vice-president David Norupiri yesterday said agro-based linkages need to be revived for downstream industries to benefit as Zimbabwe is an agro-based economy.

“We are an agro-based economy. There has been no support from the banking sector as far as agriculture is concerned as compared to previous farmers who had access to loans,” he said.

He said should Zimbabwe choose to go the path of export-led growth and industrialisation, the positive ripple effects would also lead to a stemming down of finished imports, which have affected local manufacturers.

“The protection of industry would also need to be complemented by initiatives that are in line with regional countries. Non-tariff barriers such as new standards of import quality and issues to do with licensing would also be helpful to protect local industry,” he said, adding that government had already done enough in as far as coming up with direct tariffs.

A recently published United Nations Conference on Trade and Development (UNCTAD) World Investment Report for 2014 shows that FDI inflows stagnated at $400 million last year.

This is in comparison to the $1,8 billion in FDI inflows for Zambia, Mozambique with $5,9 billion and South Africa with $8,1 billion out of $13,1 billion that flowed into the Sadc region.

In a September trade brief for South African-based Trade Law Centre authored by Brian Mureverwi (click here to download the paper), it is argued that export-driven industrialisation is typically designed to ensure that returns on exports are no less attractive than returns on domestic sales.

“The policy mix requires that where possible inputs are provided at world prices, and exports of the final product are subsidised to compensate for more costly inputs of domestic provenance. At the same time, the domestic market is not strongly protected from competing imports,” he said.

The document states that industrial policy should be dynamic and government departments must have the ability as well as motivation to constantly adapt to the changing needs of the industrial sector.

Another possible route would be import substitution industrialisation (ISI) where domestic businesses receive duty-free imported inputs and protected from finished imports.

“For ISI to yield positive results for development, it should provide limited, time-bound protection. Industries that fail to become competitive should not be protected indefinitely,” said Mureverwi.

Related News

Trade: Mauritius to set up a National Export Strategy

Mauritian Industry and Commerce Minister Cader Sayed Hossen Wednesday indicated that Mauritius will soon set up a National Export Strategy to address trade opportunities and challenges as a result of erosion of trade preferences in a bid to formulate a roadmap for key sectors with export potential.

Taking part in an economic discussion organised by the Mauritius Export Association (MEXA) in Port Louis, Hossen said the island cannot wait for the dark clouds of economic downturns in Europe to be cleared.

“We need to seize opportunities that are lurking on the economic horizon”, he said, emphasising that taking advantage of the African renaissance, the high purchasing power in the Gulf countries, an increasingly open market in India and capturing opportunities in niche segments in traditional markets would be the island’s major strategic trade thrusts.

Hossen said Mauritius needs also to have a regional export strategy as one of the drivers for high growth by leveraging on economic diplomacy as well as improving air and sea connectivity.

“GDP in Africa is projected to grow by over 60 percent by 2020 and consumer expenditure in the continent can move beyond the US Dollar one trillion mark in the near future.

“There is indeed no doubt that Mauritius can fully capitalize on its potential as a corridor for trade between Asia and Africa”, the Minister observed.

For his part, MEXA’s chairman, Phil Ryle, said that by the nature of its business the export sector is vulnerable to the whims and caprices of global economy.

“There is no doubt that diversification of the export market has made the sector more resilient over time”, he said.

PANA reports that 60 percent of Mauritius exports go to the European Union.

Related News

Fostering the spirit of entrepreneurship

Lessons for Namibia from the 2nd Brazil-Africa Forum 2014

Last week I moderated a session, titled ‘Africa and South America: Challenges for connecting the two continents’, one of the many sessions at the second Brazil-Africa Forum held in Fortaleza in the Ceara province of Brazil. The role of the Brazil Africa Institute is to link in promoting the interests of Brazil and African countries.

What is significant about the partnership between Brazil and Africa is that improved structural changes and a healthy policy environment that will foster a positive entrepreneurial spirit is needed in both continents. This two-day event was attended by high-ranking government officials, business leaders, potential investors, and representatives from think tanks and the academic sector.

Africa has become increasingly an attractive hub for foreign investors in the last 10 years, and interestingly enough our continent has a positive Gross Domestic Product (GDP) growth, at 6.6 percent in 2013, due to an increase in prices of commodities.

The forum also looked at infrastructure, partnerships and development that could ensure a good environment for public and private companies to create partnerships for future infrastructural projects and contribute to strengthening the confidence of both African and Brazilian investors. If we wish to sustain the benefits of economic growth as Africans, we need to address the gaps in infrastructure, continue investing in renewable energy, promote education and skills development, ensure food security and enhance the productive capacity of the agriculture sector.

The Director of Program for Energy and Infrastructure: Mossid Emissiry from NEPAD (New Partnership for African Development) based in South Africa introduced the audience to the Program for Infrastructure Development in Africa (PIDA) launched by the African Union in 2010. Emissiry pointed out that the objectives of this program are to promote socio-economic development and poverty reduction in the African continent through improved access to integrated and continental infrastructure networks and services.

On the other hand Brazil has enormous investment opportunities across various sectors. The chief executive officer of Angola Cables Antonoi Nunes talked us through the South Atlantic interconnection through an undersea cable. Angola Cables is the telecommunications provider, and they wish to build a cable from Angola through the Atlantic Ocean to Fortaleza, Brazil, directly and another one to Miami, USA. This is more about integrating the continents and making communication and access to the various markets possible.

Another interesting project at the forum was from Camargo Correa a Brazilian construction company that works to transform realities. One particular and insight point addressed by Kallil Farran, the Sustainable Development Manager, was the issue of Corporate Social Responsibility.

Camargo Correa expands its operations to Angola by building road infrastructure and in Mozambique they brought hope by building classrooms for communities where there were none.

All participants of the forum visited some of the social and welfare projects of Camargo Correa, Villa da Mar, project for the recovery and redevelopment of the waterfront in Fortaleza.

What are the lessons for me as a Namibian from the Brazil-Africa Forum? I can honestly say that Brazil and African countries have common challenges, given that Brazil and most African nations experienced colonization in the past. There is so much to teach and learn from one another. I picked up a few significant points one of which is “leadership”. I think through this forum both Brazil and Africa are trying to tell one another that ‘We have to believe in ourselves before we have to prove anything as that will be the key to reach our potential.’

Secondly, this platform should be seen as a partnership between Brazil and Africa and should be a win-win situation and no party should exploit the other.

Namibia can indeed try and learn from successful partners of Brazil in the region and join forces and as a nation we can only become better.

From Camargo Correa I learned that value in a company should not only be created for shareholders, but also for the society, through attitudes aligned with demands and challenges.

Corporate social responsibility is an issue some Namibian companies take very lightly. Companies will write out cheques for a project, but are never interested in the actual project, whether it was well executed or not.

Dr Wilfred Isak April holds a PhD (Entrepreneurship) from New Zealand. He currently lectures in Entrepreneurship and Management at the University of Namibia.

Related News

Checkers and Shoprite probed over mislabelling

The Namibian Standards Institution (NSI) has launched an investigation into Freshmark, Checkers and Shoprite outlets for mislabelling fresh produce.

The enterprises have labelled products indicating that they are grown in Namibia when in actual fact they are imported from South Africa.

Last week, The Namibian reported that the Freshmark products, which are sold by Checkers and Shoprite, are grown in South Africa although the labels say they are produced in Namibia. This revelation led to the NSI launching an investigation, in which sample products were taken from several Checkers and Shoprite shops.

The Namibian understands that the NSI plans to take strict measures to rectify the issue.

NSI general manager for corporate services, Rozina Jacobs, confirmed that the body has launched an investigation into the matter.

She said the NSI instituted an investigation on Checkers City Centre and Shoprite Lafrenz in Windhoek and found that both shops had misleading labels.

“We have taken samples and issued prohibition to both shops while we are investigating. They have 11 days to rectify the situation,” Jacobs said.

Speaking from Shoprite headquarters in South Africa, spokesperson Sarita van Wyk said the produce carrying the ‘Product of Namibia’ signage originates from Namibia.

“Shoprite is committed to procure as much produce as possible locally in countries where we operate and only import if the required quality is not available locally or out of season,” said Van Wyk.

She said their fresh produce procurement arm, Freshmark, however, utilises South African packaging “that is produced in bulk as a cost-saving exercise in the interest of our customers’ pockets”.

Van Wyk said the exact country of origin is indicated by the sticker applied to the package.

“We will however revisit this practice and investigate alternative methods. Shoprite apologises for any misunderstanding this may have caused some of our loyal customers and valued Namibian fresh produce suppliers,” she said.

A consumer, Reinhold Kambuli, who alerted The Namibian of the mislabelling, said this kind of action cost the Namibian farmers because Namibian customers assume they are buying local products.

Team Namibia CEO Daisry Mathias yesterday said she had contacted Shoprite and Checkers to arrange a meeting next week to discuss the issue.

“We need the retailers on board, to stop this,” she said.

Related News

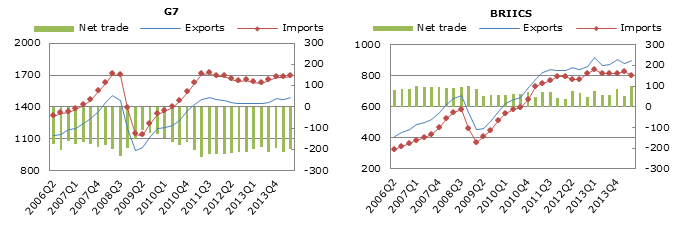

Merchandise trade broadly stable in Q2 2014, with diverging patterns across major economies

Total merchandise trade of the G7 and BRIICS economies combined was broadly stable in the second quarter of 2014, with exports rising 1.5% and imports falling 0.8% compared with the previous quarter.

This broad stability however masked diverging patterns across countries.

In the United States and Canada, both exports (up 2.2% and 4.7%, respectively) and imports (up 2.7% and 4.9%, respectively) rose strongly in the second quarter of 2014. By contrast, in Japan, merchandise trade declined, with both imports and exports contracting (by 7.8% and 0.5% respectively) as the effects of the April's increase in the consumption tax unwound.

Among the major EU countries, in Germany exports increased by 0.5% and imports decreased by 1.3%. In France both exports and imports fell (by 0.6% and 0.2%, respectively). In Italy exports remained broadly flat while imports rose (by 1.4%). In the United Kingdom both exports and imports rose compared with the previous quarter (by 0.4% and 1.1%, respectively).

In China, exports rose by 2.9% and imports contracted by 4.1%, partly reflecting lower commodity prices. Exports also rose and imports fell in Russia (by 2.8% and minus 3.8%, respectively) and in Brazil (by 0.7% and minus 6.6%, respectively). In Indonesia and South Africa both exports and imports declined (by 3.4% and 0.9%, for Indonesia and by 3.9% and 2.0% for South Africa).

|

Merchandise trade in US$ billion |

|

|

|

Source: Statistics on International Trade Database, OECD |

Related News

Uganda’s oil bonanza

Excitement as estimate of Uganda’s oil reserves jump to 6.5 billion barrels

On Aug.28, the government revised upwards the country’s petroleum resources by over 85% to about 6.5 billion barrels of oil initially in place.

This was an upgrade of the 3.5 billion barrels of oil, which the government announced about a year ago.

In addition, about 500 billion cubic feet of non-associated gas (independent gas) is also now estimated to have been discovered in Uganda to date. The gas volumes are equivalent to about 90 million barrels of oil equivalent.

Ernest Rubondo, the commissioner for Petroleum Exploration and Production Department (PEPD), had a day earlier told an oil conference organized by the Konrad Adenauer Stiftung Foundation and Leo Africa Forum that the increase in the estimated petroleum resources is as a result of the evaluation of the data and information acquired from the appraisal of 13 oil wells by the oil companies licensed in the country during the ongoing evaluation of the discoveries in the Albertine Graben.

Explaining the sudden improvement in the country’s petroleum fortunes over the last one year, Rubondo said in the past, calculating recoverable quantities has not been as accurate, since it has always been based on analogues from elsewhere in the world. However, Uganda is now relying on its own data. Rubondo told The Independent on Aug. 27 that some of the fields had been discovered to be broader, while more oil had also been encountered in additional layers of some of the fields during the appraisal.

But despite the sudden jump in volume, the government said recoverable or proved oil reserves have only improved marginally, from 1.2 billion barrels to 1.4 billion barrels. Previously, Uganda’s proved oil reserves were estimated at 1.2 billion barrels of oil from the 3.5billion barrels of oil initially in place. Rubondo said Uganda’s new proved oil reserves had been calculated using an average of 30% of in place volumes, which is the world average.

However, some oil fields in countries like Norway and the USA have been able to achieve recoverability of up to 60%.

According to the commissioner, the reduction in the ratio between the oil in place and recoverable oil is mainly due to an improved understanding of the nature of the petroleum reservoirs in Uganda through the appraisal work undertaken on each of the discoveries.

The recoverability of oil depends on several factors including; reservoir quality, oil properties (including viscosity) and the technology used in production of the oil while reservoir quality mainly depends on the type of rock, its consolidation, porosity and permeability.

The oil companies licensed in the country are further working with the government in carrying out studies to determine the most suitable enhanced oil recovery method applicable to the discoveries in the Albertine Graben.

A range of improved technology such as the use of gas injection, steam flooding and injection, polymer flooding and microbial injection are some of the possible techniques that can be used to increase the recovery factor. However, it is also important to note that the methods used for enhanced oil recovery need to be closely evaluated as they have an impact on the cost of oil production. The commissioner said the increase in Uganda’s petroleum resources is an achievement given that with improved technology, the recoverable resources have potential to increase.

However, Bwesigye Don Binyina, an energy and mineral specialist, says he would not be excited as yet with Uganda’s new volumes because different companies use different technologies to do such appraisals. He expects the picture to be clearer when further appraisals are done in future.

“Logical mathematics would mean that if the oil in place has almost doubled you would expect the recoverable reserves to increase markedly, as well,” he said.

Of the 21 discoveries made in the country to date, the three companies – CNOOC, Total E&P Uganda and Tullow Oil – have submitted applications for production licenses for the 13 discoveries whose appraisal has been completed.

One year ago, the government issued its first production licence to the Chinese firm, CNOOC, following a satisfactory review of the firm’s field development plan. That licence was issued for the Kingfisher discovery – one of the first discoveries announced almost eight years ago in the mid-western district of Hoima.

The government is also in the final stages of reaching an agreement on the most suitable lead investor for its 60,000 barrels-of-oil refinery and related downstream infrastructure it is planning to set up in Hoima.

In June, two of the four bidders that submitted proposals to the government for the role of lead investor for the refinery were given the green-light to progress to the next stage of the tender process.

Two consortia – SK Group of South Korea and Russia’s RT Global Resources – are currently undergoing scrutiny by the government with assistance from its transaction advisor – Taylor Dejongh.

Rubondo said additional exploration and appraisal is expected to be undertaken in the country, and the expectation is that this could lead to additional resources being discovered.

He added that they expect the moratorium that was slapped by the government in 2007 on licensing new exploration firms to be lifted by the end of this year.

Bwesigye noted that the new development is nonetheless good news for Uganda because this means that the country’s economies of scale will go up and the cost of doing business in this sector is likely to go down since it is most likely to attract more foreign direct investment in the near future.

Related News

Mixed bag of fortunes for SADC

The Southern Africa region has continued on a positive economic growth path with significant differences in growth rates among countries in the region.

Mozambique, Zambia and Angola registered the fastest growth rates, exceeding the 7 percent growth rate target of the Southern African Development Community (SADC), supported by positive performance of the mining sectors and strong public expenditure, according to a recent African Development Bank (AfDB) report.

The report titled “Southern Africa Review Quarterly and Analysis” says that officials in Zimbabwe also predict a significant acceleration of growth (from 3.7 percent in 2013 to 6.1 percent in 2014) premised on the successful implementation of its Zimbabwe Agenda for Sustainable Socio-Economic Transformation (ZIM-ASSET) and the completion of on-going institutional and structural reforms encompassing the mining sector.

“However, there are significant negative pressures to growth in Zimbabwe arising from liquidity constraints, weak aggregate demand and infrastructure bottlenecks,” states the report.

In Malawi, the report says, growth is expected to accelerate to 6 percent in 2014, up from an estimated 5 percent in 2013, benefiting from a good tobacco harvest.

However, the continued suspension of budget support following the exposure of government officials’ misuse of public funds and the suspension of uranium mining activities due to low global ore prices present downward risks for Malawi.

AfDF says the Namibian economy is growing at 5.3 percent, reflecting a mild acceleration of growth relative to the fourth quarter of 2013, driven by increased mining and construction activities.

In Lesotho, the report says the 2014 first quarter growth is expected to be as high as that observed in the last quarter of 2013 (about 5 percent), given accelerated growth in the diamond mining, telecommunications and trade sectors.

Growth in Mauritius is accelerating but remains moderate (3.7 percent in 2014) in tandem with the recovery trend in its major economic partner, Europe.

Growth is decelerating in South Africa, where persistent structural constraints to growth, including the labour unrest and the interest rate hike implemented to ease exchange rate pressures, have dampened growth.

Developments in South Africa, AfDB noted, are expected to negatively affect Swaziland’s growth outlook. Inflation was moderate across the board in the first quarter of 2014, supported by easing exchange rate pressures, moderate external prices and weak domestic demand.

All countries except Malawi reported single-digit inflation, four meeting the SADC convergence target of less than 5 percent and one (Zimbabwe) registering a deflation rate of -0.91 percent in March 2014.

There were price pressures arising from rising fuel prices, increasing public wages and seasonal food shortages in a number of countries including Mauritius and Zambia.

Not all countries have reported first-quarter data on external balance, fiscal balance and debt.

The report says early indications suggest that most countries met the SADC convergence targets in the first quarter of 2014.

“However, a deterioration of the external position was observed in about half of the countries due to large imports of capital equipment and manufactured goods (Mozambique and South Africa), slow growth in the economies of major trading partners and sources of capital (Mauritius) and lower export revenues from mining (Angola, Zambia and Malawi),” says the report.

In Malawi, notes the report, the suspension of budget support also weighed in. Fiscal deficits widened in the majority of countries due to expansionary fiscal policies in Angola, Mauritius, Mozambique and Swaziland, revenue constraints arising from decelerating economic activity in Zimbabwe; and from the suspension of budget support in Malawi.

Nevertheless, the report says, the fiscal position of the Southern African Customs Union (SACU) countries is generally improving as the countries pursue fiscal consolidation (Botswana, Lesotho, and Namibia) and improve domestic resource mobilisation (Swaziland and Namibia) while also benefiting from SACU revenue inflows in the first quarter of 2014.

“Countries stayed within the SADC convergence target on debt, although debt levels are increasing in a number of countries including Angola, Mozambique and Zambia, to fund fiscal deficits.

“This performance has affected the level of international reserves, which decreased in Angola, Mozambique, and Zambia though for Angola stayed within the SADC convergence target of six months of import cover,” say the report.

The report says the region’s 2014 outlook is positive overall. Average growth is expected to rebound to 4.9 percent in 2014, up from the 4.3 percent average growth rate estimated for 2013. Average inflation should drop to about 6 percent, following significant disinflation in Malawi.

At least four countries expect to post a positive current account balance in 2014, compared to only one country at the end of 2013. Seven countries are expected to have increased their international reserves to at least four months of import cover by the end of 2014, compared to four countries in 2013, although the majority will still fall short of the SADC convergence target.

However, the AFDB report says, growth is partially driven by expansionary fiscal policy measures that will negatively affect the fiscal balance and debt levels in a number of countries.

The region’s economic landscape for 2014 will be affected by a number of factors, including on-going institutional and structural reforms, as well as national elections, in some countries. Elections are expected to worsen the fiscal positions of Mozambique and Malawi, increase inflation risk in Malawi and increase uncertainty with respect to capital and investment inflow in Malawi.

Mozambique holds its elections in October while Malawi held its polls in May.

That said, the reports observe, important institutional and structural reforms are on-going in line with the development aspirations of member countries.

In the first quarter of 2014, Angola launched its ambitious electricity sector reform programme.

Malawi registered significant progress in the implementation of the public finance management reforms embedded in the Extraordinary Performance Assessment Framework.

Zambia reformed legislation in an attempt to improve the business climate; while in Zimbabwe, new foreign currencies were added to the multicurrency basket to facilitate trade and investment.

The report says in order to strengthen and sustain the positive growth trend, SADC member countries should pay particular attention to the issues including sustainable management of revenues from extractive industries and economic diversification in resource-rich countries; building resilience to external economic shocks in globally integrated economies, through economic diversification and diversification of target markets.

They further need to enhance capital budget absorption capacities to maximise benefits from expansionary fiscal policies; and public finance management reforms to reduce imbalances in budget allocations, improve domestic resource mobilisation and enhance safeguards.

Related News

G20 faces persistent gaps in employment and job quality

The ILO, along with other international organizations - including OECD, IMF and the World Bank, have produced a number of reports on employment issues that have been prepared to inform the labour ministerial discussions. These reports help identify policy gaps where actions will have the most impact.

A large and persistent shortfall in the number and quality of the jobs being created in G20 countries is affecting prospects for re-igniting economic growth, according to a report entitled G20 labour markets: outlook, key challenges and policy responses, prepared by the ILO, the OECD and the World Bank Group for the G20 Labour and Employment Ministers meeting taking place in Melbourne on 10-11 September 2014.

Despite some recent improvement, slow recovery from the financial crisis means that many G20 economies still face a substantial jobs gap, which will persist until at least 2018 unless growth gains momentum. With more than 100 million people still unemployed in the G20 economies and 447 million 'working poor' living on less than $2 a day in emerging G20 economies, the weak labour market performance is also threatening economic recovery because it is constraining both consumption and investment.

“The basic message of the report is that the labour markets of the G20 countries are still struggling, 6 years after the crisis began, both in terms of the quantity and the quality of employment. So there is really no room for complacency. More jobs with better pay contribute to household incomes, which in turn boost consumer demand. When firms see demand picking up they will invest, so creating a virtuous circle.”

Sandra Polaski, Deputy Director General for Policy, ILO

Key findings of the report include:

-

Wage growth has significantly lagged behind productivity growth in most G20 countries, while wage and income inequality either remains high or has widened.

-

Real wages have stagnated, or even fallen, for many in advanced G20 economies.

-

In emerging G20 economies, high levels of under-employment and informality are constraining both current output and future productivity.

“Jobs are a foundation for economic recovery,” the report says. “G20 countries need more and better jobs as a foundation for sustained growth and wellbeing of their societies”.

Despite overall slower growth, a number of emerging economies have made major progress in reducing absolute poverty, and some have also reduced income inequality.

“We are seeing wage and income inequality widening in many G20 countries, and if the goal is stronger, sustained, and balanced growth then inequality cannot be ignored. Equally, the situation of young people who are out of work is acute, and countries that ignore their plight do so at their own peril. We know that can spark unrest which can in turn further disrupt unemployment and growth prospects. There is no magic formula to solve this jobs crisis but we do know that it requires a ‘whole of government’ approach, involving the active collaboration of many ministries.”

Nigel Twose, Senior Director for Jobs, World Bank Group

However, informal employment remains a major obstacle to improving job quality, particularly in emerging and developing countries.

Looking ahead, the report says that achieving sustainable, equitable and inclusive growth requires policies across all relevant sectors that improve productivity and wages, employment opportunities and outcomes, particularly for those groups most affected by the crisis or who are vulnerable.

“Creating more and better jobs is really the defining challenge for the G20 countries. What we have seen, especially in the advanced economies, is that real wage growth has been pretty flat and in a number of countries real wages have declined. So the challenge is to not only to create many more jobs, but also to improve the quality, the productivity and the reward people get from their work.”

Stefano Scarpetta, Director, Employment, Labour and Social Affairs, OECD

Demographic changes, such as rapid population ageing in some countries and rising youth populations in others, also mean that governments need to promote the labour market participation of women, youth and other under-represented and vulnerable groups, enhance their skills and provide job-search support.

The report also highlights social protection, social dialogue, rights at work, and workplace safety as areas in need of further action.

Quality job creation and robust, equitable growth are intertwined goals, the study concludes. “Policy interventions that address both the demand and supply sides of the labour market are essential to reverse the current self-reinforcing cycle of slow growth, low job creation and low investment. Such policies would be much more effective if taken collectively and coordinated at the G20 level.”

Other reports prepared for the G20 labour ministers’ meeting:

Informality and the quality of employment in G20 countries

For many G20 countries, structural underemployment, informality and qualitative indicators of employment are more significant measures of the challenges they face in achieving inclusive growth and decent employment for all than unemployment rates alone.

Achieving stronger growth by promoting a more gender-balanced economy

G20 countries have much to gain from increased female labour force participation in terms of economic growth and increased welfare. But merely increasing labour force participation among women will not be enough to ensure that gender gaps in economic empowerment are eliminated. (Joint ILO, IMF, OECD, World Bank report)

Creating Safe and Healthy Workplaces for All

Every year, almost 1.3 million people die from a work-related disease in the G20 countries and about 221,000 suffer a fatal occupational accident. The G20 also experienced around 196 million non-fatal occupational accidents (with at least four days absence) in 2010.

Related News

Malawi 2014/15 Budget Statement

Extracts from the 2014/15 Budget Statement, delivered in the National Assembly of the Republic of Malawi by Minister of Finance, Economic Planning and Development, Honourable Goodall E. Gondwe, on Tuesday, 2nd September, 2014

Introduction

Mr. Speaker, Sir, and honourable members, almost exactly half a century ago, our founding Parliament sat in Zomba as we are here in Lilongwe, pondering on a strategy for boosting the economic development of an independent Malawi and how to achieve a path of accelerated economic growth that would propel the economic welfare of its citizenry. From reading hansards of the time, it is inescapable to see that here were leaders oblivious of their own comforts but singularly devoted to their country.

The result, Mr. Speaker, Sir, is a transformed country. From one with barely a road system to speak of to a country that boasts of more than 1,000 kilometres of tarmacked road system. A country that produced less than 10 megawatts of electricity to one that produces power of almost 350 megawatts of electricity. A country that had less than 30 university graduates to one that has thousands of such people. From a country, honourable members, whose public service was exclusively led by expatriates, to one which is now entirely managed by a cadre led by Malawians educated at a university established during this very first half century of its independence. A country that had a rudimentary banking system, to a Malawi that has a sophisticated financial network. A country, Mr. Speaker, Sir, whose parliament building is the envy of most African countries.

Honourable members, one can go on and on to describe the achievements that we made within the last 50 years including the discernible transformation of our cities and the establishment of scores of primary, secondary and technical schools. These have been the results of an utmost dedication of our predecessors to the welfare of their countrymen.

Having said all this, Mr. Speaker, Sir, it is also a widely held view that despite these achievements, poverty continues to prevail in rural and in urban areas of Malawi. In general, although our Gross Domestic Product has more than tripled during this period, because of a huge population growth that has quadrupled to approximately 16 million people, our income per capita continues to be at the tail end of other African countries.

Honourable members, we do not need to be reminded that as a first group of political leaders of the next 50 years, we are also charged with the same responsibility as were our founding fathers; to mobilise and lead the country in its fight against poverty, disease and hunger that continue to afflict our people. Like our predecessors, we are expected to chart a path for a further transformation of Malawi. Our people demand that we put the enhancement of their welfare before our own.

This then, honourable members, is the challenge before us. We must lead the country even better than they did. Our aim must be to erase this constant and irritating cliché which repeatedly says that “Malawi is one of five poorest countries in the world”. As the first parliament of the coming half century, let us begin to address this challenge with the passion of patriotism.

The creation of institutions that are necessary in the governance of an independent country is one of the most important accomplishments that were made during that period. Institutions such as the University of Malawi, the Reserve Bank of Malawi, the Malawi Revenue Authority, the Roads Authority, ADMARC, the Anti-Corruption Bureau and othersare vital in a country. At the top and centre of these is the Civil Service. Although indeed this existed during the colonial era, it has had to be fine-tuned to serve independent Malawi. It is important, therefore, that from time to time, its place in society be reviewed and reformed so that its effectiveness continues.

Global Economy Developments

Mr. Speaker, Sir, on the global front it is mostly the sluggish recovery of world economies and the prospects for oil prices that have a high impact on the stability of our economy. Global real output is projected to grow by 3.6 percent in 2014 and strengthen to 3.9 percent in 2015 from 3.0 percent recorded in 2013. Thus although the recovery has strengthened, it is not yet robust. On one hand, there is a pick-up in growth for advanced economies but on the other, economic growth is slowing in emerging economies. Unemployment remains stubbornly high in many countries while the sustained growth momentum in low income countries has not seen reduction in poverty levels. Overall, the slow global growth dampens demand for Malawi’s traditional exports resulting in stagnation of export earnings.

Sub-Saharan Africa

Coming to our region, growth in Sub-Saharan Africa (SSA) remained strong in 2013 at 4.9 percent, virtually unchanged from 2012. This was underpinned by improved agricultural production and investment in natural resources and infrastructure. SSA growth is projected to accelerate to about 5.4 percent in 2014 and 5.5 percent in 2015, reflecting positive domestic supply side development and strengthening global recovery. Nearer home, growth in South Africa is projected to improve only modestly from 1.9 percent in 2013 to 2.3 percent in 2014 as a result of stronger external demand. Mr. Speaker, Sir, it is important to note that a strong growth in the South African economy will positively impact our economy as it is a major importer of our products.

The world's oil prices have been high since 2010, fluctuating around US$100 per barrel as demand for oil keeps rising, driven by emerging economies. Supply has also lagged behind demand due to geopolitical conflicts in some of the oil-producing countries such as Iraq, Libya, Syria and Nigeria. Since the start of the year, conflicts in the Middle East have escalated and, if sustained for longer periods, could have significant impact on the global economy through higher oil prices which could consequently lead to an increase in domestic pump prices.

Performance of the Malawi Economy in 2013

Mr. Speaker, Sir, performance of the Malawi economy in 2013 has been mixed and subdued by the “cashgate” scandal. In accounting for performance in 2013, let me begin by reminding honourable members that as a country we are for the period, 2011-2016, guided by the Malawi Growth and Development Strategy (MGDS) that the Bingu Administration pioneered. This is our overarching medium term development framework whose objective is to reduce poverty through sustainable economic growth and infrastructure development. In this context, we are pursuing an export led growth that is expected to significantly contribute to poverty reduction. In the same vein, while we have nine key priorities, we will pay special attention to the sectors that can quickly contribute to growth such as agriculture and those that constrain growth such as energy and transport. I will thus provide more detail pertaining to agriculture, energy, transport and manufacturing among others.

Mr. Speaker, Sir, during 2013/14 the economy registered an average GDP growth of 6.1 percent. This growth was as a result of good performance in the agriculture and manufacturing sectors. In particular, the 2013 growth in manufacturing was attributed to higher agricultural inputs and a more constant supply of fuel and other raw materials. The sector registered increased capacity utilization of above 73%. However, the contraction in fiscal expenditure in the last half of 2013 as a result of the ‘cashgate’ scandal exerted significant challenges to the economy particularly on inflation and the exchange rate.

Consequently, the annual average inflation rate for 2013 was at 27.3 percent. In order to contain inflationary pressures, the monetary authorities continued to pursue a tight monetary policy. In this regard, the policy rate was maintained at 25.0 percent until July 2014 when it was reduced to 22.5 percent. Mr. Speaker, Sir, with the reduction in the policy rate we should start registering growth in the private sector credit to support economic growth in the country. The pursuance of a tight monetary policy has successfully managed to contain growth in money supply from an annual growth of 34.3 percent in June 2013 to 24.8 percent in June 2014 which is in tandem with the nominal GDP growth projected at around 28.2 percent for 2014.

Mr. Speaker, Sir, as the House is aware, Government in 2012 liberalized the foreign exchange regime in order to support the build-up of foreign exchange reserves. The deregulation of the foreign exchange market and implementation of market determined exchange rate regime eliminated misalignments and distortions in the foreign exchange market. This policy stance is what has always been emphasized in all countries with an International Monetary Fund programme. And as is always the case in countries that have just adopted the flexible exchange rate regime, the resultant inflationary pressures take a long time to settle as has been the case in Malawi.

That notwithstanding, the official foreign exchange reserves have been maintained above 2 months of imports since July 2013 thereby enabling importation of essential commodities such fuel, fertilizer, pharmaceuticals and raw materials. The central bank will continue to implement policies that aim at accumulating reserves to around 3.0 months of imports. The implementation of a flexible exchange rate regime coupled with the national export strategy should expand and deepen the export base and help to improve the current account balance in the Balance of Payment (BOP).

As alluded to earlier, our situation was also fuelled by the ‘cashgate’ scandal which led Government to drastically cut funding to some sectors of the economy. At the same time, however, the Government borrowed heavily through ways and means advances leading to accumulation of the stock of domestic debt to around MK340 billion by end May 2014. I am, however, pleased to inform this August House that the situation has abated during the last three months.

The government wishes to emphasise that as part of the financial program with International Monetary Fund, it will continue to pursue macroeconomic reforms that were agreed under that programme, including the automatic pricing of fuel and the flexible exchange rate regime.

The 2014/15 Budget

Mr. Speaker, Sir, the resource envelope of this budget is severely constrained as predicted by many analysts. This is so because of the huge amount of arrears, a large stock of domestic debt and the more daunting task of making up for a severe cut back of donors’ financial support of the budget.

The total expenditure this year is projected at MK742.7 billion representing an increase of 16.3 percent over last year’s total budgeted expenditure. Of the total expenditure, MK535.1 billion is recurrent expenditure and MK194.6 billion will be the expenditure on development account. The recurrent budget includes an amount of K163.3 billion for wages and salaries. This is 24.4 percent higher than last financial year’s provision for wages and salaries. Honourable members will, therefore, note that this year’s average wage increase is proposed to be 24.4 percent.

Within such an environment, it is projected that total revenues and grants will amount to K635.6 billion compared to a budgeted amount of MK603.4 billion in 2013/14, an increase of only 5.3 percent. In this budget, domestic revenues are estimated at MK525.3 billion compared with a final revised estimate of MK441.6 billion in the 2013/14 financial year. Tax revenues are estimated to increase to MK470.1 billion from K388.4 billion that was registered in the 2013/14 financial year. Grants for the 2014/15 financial year are projected at K110.3 billion which is less than half of the amount of MK240.4 billion that was budgeted last year.

Tax revenues at MK470.1 billion have been estimated to grow by 21.1 percent over last financial year’s collection while non-tax revenues at MK55.2 billion have been estimated to grow by only 3.7 percent. These growth rates are conservative when compared with growth rates of more than 35 percent in domestic revenues for the previous two years. However, the Government will continue with efforts to improve revenue administration and collection and it is envisaged that actual collection will be far higher than projected in the budget.

On donor support, Mr. Speaker, Sir, the European Union, the World Bank and the African Development Bank have indicated that they could provide budget support amounting to over MK43.0 billion. Nevertheless, as the pledges are conditional on demonstrated progress in the implementation of the agreed public finance management reforms, we have assumed that none will be received. However, we believe that by mid-year we will have made sufficient progress in implementing the public finance management reforms enough to achieve the critical mass necessary to trigger disbursements of the budget support.

Mr. Speaker, Sir, honourable members should note that this financial year we have assumed that Malawi will not receive budgetary support.

At this point, I would like to remind the house that our understanding is that, in principle, only budgetary support is being withheld by donors. Therefore dedicated and project grants should not be part of withheld grants. In actual fact, however, even dedicated grants were severely curtailed from a commitment of MK93.6 billion to MK31.1 billion last financial year that was actually received. Therefore, this year Government has reduced its expected amount of dedicated grants to MK38.5 billion while project grants, that fund development projects, have remained at a high figure of MK71.8 billion. As honourable members will see, therefore, even the total amount of these two categories of grants is budgetted at less than half the 2013/14 budgeted amount of MK240.4 billion.

Amicable discussions are still continuing with donors and it is hoped that grants in excess of the budgeted amount could be received in the course of the year. We also expect far higher domestic revenue than projected in the budget.

Trade Agreements and International Taxation

Mr. Speaker, Sir, Malawi remains committed to the tariff offers made under the SADC Trade Protocol in order to facilitate regional integration within the SADC region. In this regard, Malawi now undertakes to further reduce the tariffs that are applicable to South Africa in line with the SADC Trade Protocol.

Mr. Speaker, Sir, to improve international taxation and encourage foreign direct investment, Malawi Government through its Diplomatic channels will continue to engage other Governments in the negotiation of new Double Taxation Agreements (DTAs). In addition, Government will continue to review the old DTAs especially those that negatively impact on our tax base through the loss of taxing rights.

Conclusion

In conclusion, if, Mr. Speaker, Sir, you were to ask me the theme of this year’s budget, without hesitation I would say “Restoration of Fiscal discipline as a Foundation for Poverty Reduction”.

National Speaker of Assembly, Richard Msowoya, adjourned Parliament to resume on Wednesday, 10 September 2014 to allow the Parliamentary Committee on Finance to thoroughly scrutinise the budget estimates for 2014/15 financial year.

Related News

Poultry import restrictions under attack

Major players in the South African poultry industry are asking Namibia’s High Court to set aside the restrictions on the importation of poultry products that the Minister of Trade and Industry, Calle Schlettwein, announced in April last year.

With a review application that the South African Poultry Association and five companies involved in the South African poultry industry lodged against the Minister of Trade and Industry, the government and Namib Poultry Industries in the Windhoek High Court still in its early stages, preliminary skirmishes in the case have started to crop up in court.

No date has been set yet for the hearing of the main case, in which the South African Poultry Association and South African poultry exporters Crown Chickens, Supreme Poultry, Rainbow Farms, Astral Foods and Afgri Poultry are asking the High Court to review and set aside the import restrictions on poultry products announced in the Government Gazette on 5 April last year.

Schlettwein announced the import restrictions in terms of the Import and Export Control Act.

He announced that the importation of poultry products into Namibia would only be allowed in accordance with an import permit issued by the Ministry of Trade and Industry, and that no more than 900 tons of poultry products may be imported into Namibia per month.

The import restrictions provide protection to the Namibian poultry industry, which had been complaining that it was battling to compete with more established producers of poultry products that have been able to market their products in Namibia at lower prices than Namibian producers – mainly Namib Poultry Industries – could match without suffering financial losses.

In one of the preliminary brushes between the parties involved in the case, Judge Harald Geier postponed an urgent application by the South African Poultry Association and the five South African poultry exporters to an undetermined date yesterday.

The postponement was accompanied by an agreement by the law firm representing Namib Poultry Industries, Theunissen, Louw & Partners, to treat ten files with documents coming from the association and the South African companies as confidential, not to disclose it to Namib Poultry Industries or anyone else, and to use the documents only for the pending review application.

The five poultry exporters and the association initially wanted the court to order Theunissen, Louw & Partners to hand the ten files to the registrar of the High Court for safekeeping and not to disclose any of the documents or information in it to Namib Poultry Industries or anyone else.

The files were handed over to Theunissen, Louw & Partners after Namib Poultry Industries had filed an application in which it asked to be provided with documentation that it claimed was relevant to the main case.

According to lawyer Ian Petherbridge, who is representing the South African companies and the South African Poultry Association, the documents contain confidential trade information, were meant only for the use of the lawyers of Namib Poultry Industries, and were not to be disclosed to the Namibian company.

With the urgent application about the documentation postponed, another preliminary hearing in the main case – about the provision of a record of the decision that Schlettwein took when the import restrictions were approved – is due to take place in the Windhoek High Court on 29 September.

Beatrix de Jager and senior counsel Andrew Corbett, instructed by Martin Strydom, represented the South African companies and the association in court yesterday. The other parties in the case were not represented.

Related News

Rwanda looks to fuel re-exports to strengthen forex reserve position

Rwanda looks to focus on oil re-exports as it continues to seek ways that could expand its export earnings and strengthen the country’s foreign exchange reserve position.

According to Robert Opirah, the Ministry of Trade and Industry director general for trade and investment, the government has already called for contractors to bid for the construction of a 150 million-litre capacity fuel reserve facility as it prepares for the venture.

Opirah said the strategic project will besides boosting the country’s fuel reserves, strengthen Rwanda’s capacity to engage in the oil and oil products re-export business, serving neighbouring countries including Burundi and eastern Democratic Republic of Congo.

“We want experienced operators to construct the facility that will hold over 150 million litres of fuel reserves, which is enough to support the re- exports sector,” Opirah, also the in charge of fuel importation at the ministry, said in an exclusive interview with Business Times.

He also revealed that more storage facilities with the capacity to hold 42 million litres would be operational by the end of the year.

“This will boost the country’s current fuel reserve capacity from 30 million litres to over 70 million litres by the end 2015, and more than 200 million litres by 2017,” he noted.

Oil Com and SP new fuel storage facilities, which have a combined capacity of 42 million litres, will also be completed by the end of the year, Opirah added.

He said Oil Com is building reserves in Gatsata that will have a capacity of 20 million litres, while that of SP located in Kabuga will bring on board 22 million litres by the end of the month.

“With the already existing government reserves, the total fuel reserve capacity is projected to reach over 200 million litres in the next five years. This is enough to supply the local market and export the remaining to the neighbouring markets like the eastern DRC and Burundi,” Opirah said.

He said there are also other companies currently constructing oil storage facilities, including Abbarci Petroleum Marketing Company, ORYX Petroleum, PROTEK and Mount Meru Petroleum

Rwanda’s re-exports increased by 47.4 per cent in value during the first half of the year, and were dominated by petroleum products and vehicles.

These products were mainly jet fuel sold to airlines refueling at the Kigali International Airport and other petroleum products re-exported to eastern DRC and Burundi.

Last year, government and the private sector teamed up to construct extra fuel reserves across the country at an estimated cost of over $30 million (about Rwf21.2 billion).

These initiatives are geared at cushioning the country in case of instabilities in fuel prices on the global market, fuel importers said.

Victor Nduwumwami, the president of the Rwanda Fuel Importers Association, said catering for the growing fuel demand in the country is the only way to keep the economy on track.

“The economy is growing and so is the demand for fuel and its products; and one way to satisfy this demand is by ensuring you have enough volumes all the time.

“Constructing more fuel reserves will also help us counter price instabilities given the kind of precarious situation in the Middle East, which is the main source of our oil supplies,” Nduwumwami said.

According to statistics, demand for petroleum products, including automotive oil, kerosene, fuel, heavy oil and premium motor spirit, is on the rise. On average fuel consumption in the country has increased from 32 per cent to 48 per cent.

Currently, the 30 million-litre total fuel storage capacity is split among the five depots of Gatsata in Kigali, Kabuye, Rwabuye in the Southern Province and at the Kigali International Airport in Kanombe.

Related News

Is bigger better for ASEAN in a mega-regional world?

Big-block trade agreements or ‘mega-regionals’, revolving around one or more major powers, are the latest trend in trade policy negotiations. ASEAN is involved in two: the American-led Trans-Pacific Partnership (TPP) and the Chinese-led Regional Comprehensive Economic Partnership (RCEP). But are mega-regionals good for trade and economic growth? Will they spur regional and global economic integration? And where does ASEAN stand?

As of 2013, there were 261 FTAs concluded in Asia, over 100 of which are already in force. Asia’s three major powers, China, Japan and India, are heavily involved as are ASEAN countries Singapore, Malaysia and Thailand. ASEAN also has its own ASEAN Free Trade Area (AFTA), which will be upgraded into the ASEAN Economic Community (AEC) in 2015. And ASEAN has collective FTAs with China, Japan, South Korea, India, and Australia-New Zealand.

The strength of FTAs varies enormously. US FTAs in Asia are by far the strongest. They have the widest sectoral coverage and go deepest with disciplines to ensure market access. But they contain exemptions for politically sensitive sectors and are riddled with complex and discriminatory rules-of-origin (ROO) requirements. EU FTAs in Asia are also relatively strong. But intra-Asian FTAs are generally ‘trade-light’. The better ones remove tariffs on most goods, but they are weak on disciplining protectionist regulatory barriers in goods, services, investment and public procurement. That is true across the board of Chinese, Japanese and Indian FTAs, as well as the FTAs of ASEAN countries.

Overall, the new wave of FTAs has not given a big boost to trade and foreign investment. But nor has it impeded trade growth. Effects have been broadly neutral, or at best marginally positive.

Now attention has shifted to mega-regionals. There are three being negotiated: the TPP, RCEP and the EU-US Transatlantic Trade and Investment Partnership (TTIP). The TPP’s membership is 12 to date (US, Mexico, Canada, Chile, Peru, Australia, New Zealand, Japan, Singapore, Brunei, Malaysia and Vietnam). It started earlier than the others and is the closest to completion. RCEP’s members are the ASEAN 10 countries plus China, Japan, South Korea, India, Australia and New Zealand. Taken together, these three mega-regionals account for the bulk of world trade and GDP.

Mega-regionals potentially amplify the gains from trade liberalisation. If done cleanly and comprehensively, they would iron out distortions caused by multiple and overlapping FTAs among members (such as differing ROOs). With a bigger integrated economic space, they can reap economies of scale and spur technological innovation. This is particularly important for global supply chains. Regional production networks to serve global markets are the biggest drivers of productivity, employment and growth in international trade. They have a big stake in integrated regional and cross-regional markets. Still, mega-regionals are not ’multilateral’: they discriminate against non-members. That is a big potential source of disruption to global supply chains.

The TTIP and the TPP are the most ambitious mega-regionals. They cover markets for all goods, services, investment and government procurement, and go deep into regulatory disciplines – including on intellectual property, food safety and technical standards – and customs procedures. In the TPP, ‘twenty-first century’ innovations include rules to facilitate supply chains and e-commerce.

But there are major barriers that stand in the way of success.

Protectionist lobbies are big obstacles in several countries, including parts of agriculture and autos in the USA, agriculture in Japan, government procurement in Malaysia, and state-owned enterprises in Vietnam. The US insists on intellectual-property, public-health, labour and environmental standards, and ROO requirements that may impede market access for developing countries. And the Obama administration lacks Trade Promotion Authority from Congress, without which the TPP is unlikely to be concluded and ratified. The TTIP has also been slowed down by obstacles on both sides of the Atlantic.

RCEP looks the least ambitious. If it follows the pattern of intra-Asian FTAs, it will remove tariffs on about 90 per cent of goods over a fairly long timeframe. But it will have weak disciplines on non-tariff regulatory barriers that are the biggest obstacles to trade in the region. It might end up agglomerating the ‘noodle-bowl’ of FTAs among members rather than ironing out distortions among them. In such a scenario, RCEP will create little new trade and investment, and cause extra complications for global supply chains. But negotiations still have some way to go.

Much depends on US and Chinese leadership. President Obama’s leadership is needed to conclude a ‘high-quality, twenty-first century’ TPP – and open the door to eventual Chinese membership. But Obama has conspicuously failed to lead on international trade. Similarly, the Chinese leadership has been defensive on trade policy for almost a decade. But there are signs that China is becoming interested again in regional and global trade liberalisation. It will take Chinese leadership to inject more ambition into RCEP.

All ASEAN countries are in RCEP and four are in the TPP. What should they do on mega-regionals? First, they should push for ambitious agreements that are wide (with maximum sectoral coverage) and deep (with strong disciplines on regulatory barriers), with relatively simple ROOs and open accession clauses for non-members. Only this type of mega-regional is likely to create significant trade and investment, and facilitate the expansion of global supply chains. Second, they should back this up with intra-ASEAN measures, such as accelerating progress on the AEC and strengthening provisions in existing FTAs.

But it must be recognised that mega-regionals, and indeed other FTAs, are not a universal remedy. Political realities will inevitably dilute their ambition and quality. Given their gaps and distortions, they are unlikely to deliver the huge gains that many pundits predict. This applies to the TPP, RCEP and the AEC. The key policy implication that follows is that ASEAN countries should go as fast, wide and deep as possible with unilateral liberalisation. They should also ‘multilateralise’ preferences in existing FTAs as far as possible, that is, to extend them to non-members on a non-discriminatory basis. This is how ASEAN countries have liberalised and integrated into global supply chains in the past. That is unlikely to change in the future.

Razeen Sally is Associate Professor at the Lee Kuan Yew School of Public Policy, National University of Singapore.

Related News

Joint tax deal to rein in EAC sugar cartels as pact takes effect

Kenya, Uganda and Tanzania will from next week jointly collect custom taxes on sugar, dealing a blow to cartels involved in dumping of the commodity in the regional markets.

The Kenya Revenue Authority said the three countries would trade in sugar under the Single Customs Territory (SCT) arrangement – which allows for joint collection of customs taxes by the EAC partners – starting September 15.

“Duty shall be paid to the destination country before release of goods from the originating country,” Beatrice Memo, commissioner for customs services said Tuesday.

Under the SCT deal that began on April 1, clearing agents with East African Community have been granted rights to relocate and carry out their duties in any of the partner states as part of a strategy to improve flow of goods and curb dumping.

Importers of commodities covered under the SCT are required to lodge the import declaration forms in their home country and pay relevant taxes first to facilitate the export process.

The tax authorities in the respective countries would then issue a road manifest against the import documents submitted electronically by the revenue authority of the importing country.

Massive shortage

Sugar industry regulators and tax agencies in EAC have been involved in frequent stand-offs over dumping of duty-free sugar within the region.

The feud has mainly drawn Kenya against Rwanda and Uganda with the former accusing the two countries of abetting the malpractice that renders its own millers uncompetitive.

At a meeting in Kampala in July Rwanda was reprimanded and urged to step up surveillance on duty-free sugar imported into its market to avoid dumping in other EAC countries.

Like Uganda, Rwanda was in 2011 allowed to make duty-free imports to cover for a massive shortage of the commodity in its domestic market due to drought. Critics claim part of duty-free sugar imports into Rwanda later found its way into other EAC markets, hurting local millers.

The partner states agreed to include sugar among the goods cleared under the Single Customs Territory arrangement by November 1.

“The advantage of the SCT platform is that it will make trade in sugar even more efficient and fast and we want it added to the list of products covered under the arrangement,” head of Sugar Directorate Rosemary Mkok told the Business Daily following the Kampala meeting.

Related News

PM urges FAO to back Indian cause at WTO

Visiting director Jose da Silva briefed about subsidy stance

Prime minister Narendra Modi on Tuesday asked United Nations Food and Agriculture Organisation (FAO) to take the lead to protect the interests of the poor and farmers at the WTO as industrialised nations are stonewalling on the public procurement issue, a livelihood concern for the developing countries.

He told the visiting FAO director general Jose Graziano da Silva, who himself had championed a “no hunger project” in Brazil some years ago, that FAO should take the lead at the WTO to ensure that developed countries do not become adamant on the issue.

The WTO negotiations ran into rough weather in July last as India, articulating developing countries' concern, blocked the trade facilitation agreement (TFA) after United States and European Union dragged their feet in working out a permanent solution to food security and public procurement.

The food security programme, along with public procurement, are aimed at providing subsidised food grain to one billion poor in the world, including 300 million in India, and this was negotiated at the WTO general council as part of a single undertaking at the Bali trade talks last year. Instead, industrialised nations pushed only the TFA, which is of interest to them.

“India does not stand in the way of a rule-based global trade agreement, but cannot sacrifice the interests and food security of the poor and the farmers,” Modi told the FAO director general when he called on him.

Food security is part of the mandate of Doha Development Round of negotiations at the 160-member WTO, which began in 2001. It has missed several deadlines right from 2005 as developed countries refused to walk the talk.

Though developed countries have pledged support to the issue, they are unwilling to move forward when it comes to framing actual rules at the WTO on food security and public procurement.

Food security cannot be driven by the interests of Cargil and other multinationals involved in agri-products, trade analysts said, wondering how tiny subsidies given to poor farmers in developing countries would distort world trade.

In fact, long-term dumping of food grains by United States and developed countries distorts trade. Recently, the European Union provided $400 million to its farmers to burn farm products after Russia imposed a ban on food imports due to the standoff on Ukraine.

Even today, India’s food grain prices are 30 per cent less than world prices and yet the tiny subsidy given to poor and subsistence farmers are shown as trade-distorting subsidies, trade analysts told FC.

Food security is a compelling issue in poor countries like Zambia, Ghana, Zimbabwe Malawi Nigeria, Egypt, Botswana Tunisia, Bangladesh, Sri Lanka and Jordan apart from India, China and Indonesia.

Public procurement is not something that had been invented by India and other developing countries, trade analyst Abhijit Das, who is a professor at the Indian Institute of Foreign Trade, said recently. He pointed out that public procurement was a policy adopted by industrialised nations during early stages of their development in the middle of the last century.

Related News

Pressure as EU issues new trade ultimatum

Critics say Uganda should not sign because EPAs will lead to more poverty and not development in poor countries

October 1, 2014 is an important date in the ten-year old trade negotiations between the European Union and ACP countries over the so-called Economic Partnership Agreements (EPAs). While EU boss in Uganda is quick to point out that the date is neither an ultimatum nor a deadline; come Oct. 01, the EU – a grouping of 27 European countries – will withdraw its free market access to countries that have not yet ratified the agreements.

Apparently, the EU is forced to act because it is also under pressure from other sources. With the US initiated AGOA planned for extension for another 15 years and the US promising $33 billion in trade deals, and with the Chinese also becoming a key player in developing countries, the EU doesn’t appear to have much time to tie up its trade relations with ACP countries. Development campaigners are crying foul, poor countries that depend on Europe as a key export market are feeling the pressure but the EU top officials say they have waited long enough.

Ambassador Kristian Schmidt, the EU Head of Delegation to Uganda, denied that the date was a deadline but suggested that the trade agreements are for the mutual benefit of both Europe and the ACP countries. “October 1 is neither an ultimatum, nor a deadline for EPA negotiations. It is the date when the Amendment of the so-called Market Access Regulation enters into application,” he said in an e-mail to The Independent. “From that date, only those ACP countries that have opted for an EPA will continue to benefit from free access to the EU market, unless they are Least Developed Countries (LDCs) and can, as such, export their products to the EU duty-free quota-free anyway.”

He added, “This regulation was always meant to be a temporary bridging measure, which advanced the application of the EU part of the deal while the ACP countries were proceeding with the signature and ratification of the interim EPAs made in 2007. It is therefore only normal that the EU is withdrawing free market access from those countries that have not seen through their commitments,” says Kristian Schmidt.

Schmidt noted that the EU has always wanted the African members of the ACP to sign the EPA`s for three main reasons; the first being the conviction that the EPAs on the table would better allow EU/African partners to benefit from trade opportunities on European markets, and to deliver export growth and diversification. New generous so-called “rules of origin,” for example, would allow African producers to accumulate added-value in the region, while still enjoying free access on EU markets, he added. “Our African trade partners had to find a way together to replace the previous ACP-EU trade arrangements that were found to be incompatible with the WTO rules because they discriminated against other developing countries,” he said, adding that EPAs as region-to-region agreements, are “a perfect fit with Africa’s own processes for regional integration, which Europe fully supports for both economic and political reasons.” Citing the EAC, Schmidt said the EPA with the EU would help to make the EAC internal market a reality.

Schmidt however suggested that he partly understood why some African countries are reluctant. “All trade negotiations touch on vested interests and negotiators on both sides are subject to a lot of sectoral pressure and lobbying,” he said. But at the strategic level, he added, African countries have repeatedly confirmed their strong commitment to the EPA agenda as is the case at the final declaration of the Africa-EU Summit 2014. “Agreement with West Africa was reached, so let’s hope an agreement with the EAC is also imminent. If not, LDCs will continue to benefit from free access to the EU market under the so-called ‘Everything But Arms’ (EBA) scheme, but not from the new improved EPA rules. Other African countries that do not fulfil the requirements of the Market Access Regulation would still benefit from generous trade preferences under the Generalized Scheme of Preferences (GSP), according to Schmidt.

EPA opposition persists

For apparent fear of this situation, a couple of ACP countries have opted out of the regional blocs and are now ready to sign as individuals. If the EAC bloc continues to dillydally, Kenya, the only country in the region that is not an LDC, could go it alone.

The SADC grouping recently agreed to settle for the EPAs and have finalised the text of the agreement, confirmed by the chief negotiators, and is now going to be presented for signature and ratification according to the domestic procedures of each partner.

Relatedly, West Africa finalized its negotiations after the EPA was successfully closed in Brussels on Feb.06 before the agreement was initialed on June 30. On July 10, ECOWAS Heads of State endorsed the EPA for signature. This development has now heaped more pressure on other regional blocs.

Africa Kiiza, a program officer for trade negotiations at the Southern and Eastern African Trade Information and Negotiations Institute (SEATINI)-Uganda, is worried about the consequences of the pressure on poor countries like Uganda. “If Uganda signs basing on deadline other than content, this would put her economy at stake,” he says. Kiiza notes that even if Uganda signs the EPA, it still won’t benefit until it addresses her supply side capacity constraints. It should be noted that the EAC countries have not effectively utilized these preferences and have remained largely exporters of raw materials to the EU because of the critical long-standing market entry barriers in the EU i.e. Sanitary and Phyto-Sanitary measures, Rules of Origin, Technical Barriers to Trade and subsidies; and because of the supply side constraints within the EAC countries. However, Emmanuel Mutahunga, the acting executive director of the Uganda Export Promotions Board, and who has been a key figure in the EPA negotiations from the very onset, says there is nothing to worry about because significant progress has been made on the negotiations.