All News

Obama’s Power Africa and the continent's Energy problems

Power Africa, an initiative started by President Barack Obama, looks to all resources to meet high energy demands.

The initiative looks to increase the number of people who have access to power in sub-Saharan Africa.

Lai Yahaya, team leader for President Obama’s Power Africa Senior Advisors Group, says following the Africa Leaders’ Summit, held in Washington DC, he is positive at the fact that African countries are intensifying efforts to reform and to liberalise environments.

“What Power Africa is trying to do is bringing together the support available from a number of US agencies. But in a sense really it’s just recognising the importance of power sector development,” said Yahaya to CNBC Africa.

One of the major hindrances that the continent faces is not being able to meet the energy demands of the rapidly growing population.

“The biggest challenge is ‘how do you reach rural populations?’ So it’s not just meeting the demands of the youth budge, it’s how do you meet rural populations in a way in which is cost effective for private sector operations to be able to provide electricity,” he said.

Yahaya says there is a lot of talk about various kinds of energy resources and which is best but at the end of the day the continent just needs a sustainable source of energy.

“The concern I have about some of the discussion about renewables or non-renewables or solar and various things is that. Frankly because of the demand we need to use whatever resources we have.”

Moving forward, Yahaya says that with all the new technology developments the cost of providing solar-powered energy has decrease, making it more affordable for the masses.

Related News

Swaziland in SACU funds shocker

The ministry of finance says member states revenue shares for 2015/16 will be concluded in December after South Africa, being the manager of the pool has provided the forecast of the size of the pool for the next (2015/16) financial year and has provided the audited size of the pool for the previous year (2013/14)

Revenue receipts from the Southern African Customs Union (SACU) for the next financial year (2015/16) might drop.

They are expected to fall below the E7.4 billion that the government received during the current financial year, the ministry of finance has reported.

This could spell disaster for the country as it is likely to relive challenges the country faced in 2011 when it had to freeze salary increases for it to cope with the cash-flow problems the country faced.

The possible SACU money drop is according to the second quarter performance report for the ministry tabled by Minister Martin Dlamini in Parliament on Monday.

The second quarter of the government financial year covers three months, from July to September.

The major cause for concern is the performance of the economy of South Africa, being the major contributor into the Southern African Customs Union revenue pool. The ministry of finance says member states revenue shares for 2015/16 will be concluded in December after South Africa, being the manager of the pool has provided the forecast of the size of the pool for the next (2015/16) financial year and has provided the audited size of the pool for the previous year (2013/14).

The ministry further stated that the modest growth of the South African economy of 1.9 percent in 2013 from 2.5 perecnt in 2012, the protracted mining sector strikes and a decline in that country’s manufacturing sector output remained a cause for concern as they may translate to a decline in extra-SACU imports. Such could lead to a reduction in the size of the revenue pool.

The ministry further noted that recent estimates put the 2014 South African Growth Domestic Product (GDP) growth at 1.4 percent and if the audited size of the revenue pool is below the forecast which was provided in 2012, then, the country would be required to pay more money back into the pool.

It says such a situation could further diminish revenue for the next financial year (2015/16).

“Considering all the above factors, particularly the level of intra-SACU imports for Swaziland and the economic performance of the South African economy, SACU receipts for the country for 2015/16 might fall below the 2014/15 level of E7.4billion,” the ministry reported.

In September, finance ministers from the union’s member states participated in the SACU Task Team on Trade Data reconciliation.

The purpose of the meeting was to finalise the process of reconciling intra-SACU trade data for 2012/13 which would be used to determine their revenue shares for the next financial year (2015/16).

In the meeting, member states further presented and confirmed their GDP and population data for 2012, in line with the SACU Agreement which requires member states to submit their data GDP, population and intra SACU imports and exports for the most recent financial year for purposes of sharing.

This finalised intra-SACU trade data for 2012/13, GDP and population levels would be used to determine revenue shares for 2015/16.

Revenue receipts from SACU finance about 60 percent of the national budget.

Last week, South Africa’s Finance Minister Nhlanhla Nene announced that his country’s economic growth was much slower than anticipated.

According to a report from SAPA, the minister said the GDP growth was expected to be half of what was forecast in February, at 1.4 percent. Nene warned that South Africa has reached an economic turning point.

He announced firm measures to check South Africa’s worsening debt outlook, warning that the country had reached an economic turning point. Nene said GDP growth was now anticipated to be 1.4 percent this year (2014/15), almost half of the 2.7 percent forecast in February. He said growth was expected to reach three percent in 2017.

Expenditures growing twice more than revenue

Government expenditures are growing more than twice as fast as revenues.

This has been the trend from the last financial year, 2013/14 and the situation is still the same even in this financial year.

During the 2013/14 financial year, revenue grew around E700 million while expenditures increased by E2.3billion. This financial year, expenditure is projected to increase by E2.2 billion while revenues are projected to grow by only El billion. The finance ministry said this is despite an outstanding revenue collection performance on the part of the Swaziland Revenue Authority (SRA). It said the recent expenditure-revenue divergence will affect available financing over the medium term. The finance ministry further stated that line ministries are failing to mitigate high expenditures in the medium to long term. However, the ministry is positive that in the next two quarters, budget execution would materialise as planned.

It says over-expenditures related to the wage bill and other unbudgeted decisions may or may not be contained under the existing 2014/15 budget.

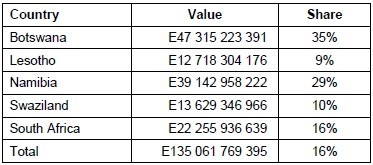

The intra-SACU trade data for the countries was presented as follows:

Member states’ presentations of GDP and Population levels:

What it would mean if SACU money drops

It would be not the first time Swaziland is faced with such woes with the SACU money drop.

Swaziland’s SACU receipts dropped to E1.9billion in 2011. This followed a global economic meltdown which hit the world hard around 2010. Swaziland encountered serious financial challenges then.

Recap of 2011 challenges

-

Government could not cope with some of its responsibilities. It struggled to pay civil servants’ salaries which accounted for over 40% of its expenditure.

-

In light of the low SACU revenue, the International Monetary Fund (IMF) proposed various fiscal adjustment strategies for the government.

One of the key recommendations for Swaziland was to reduce the huge public sector wage bill.

-

Government announced that 7 000 public service jobs would be cut in 2011 a move that was expected to save money but also came with fears that such could compromise public service delivery and further contribute to an unemployment rate that already stood at 40 percent at the time.

-

Government suspended new recruitments into the civil service, froze salary increases and short-term borrowing.

-

The IMF predicted that if government did nothing to confront its economic problems, public debt would hike from 19 percent of GDP in 2010 to 31 percent in 2011, eventually constituting 75 percent of GDP by 2015. However, the public debt stock currently stands at E6.9billion, which amounts to 16.7 percent of GDP.

SD granted E8m from COMESA

Swaziland has been granted E8million for funding of national programmes related to regional integration.

However, the ministry of finance is required to submit projects that are regional integration related to be considered for the funding.

While the country gets the funding offer, it has still not been able to adopt any COMESA harmosined standards.

The ministry of finance says this is due to inconsistency in the procedures for harmonisation between COMESA and the Southern African Development Community (SADC) as Swaziland is affiliated to both regional organisations.

It says the situation has historically put the country in a position where it can only focus on standards harmo0nisation under SADC given her deeper integration within SADC and her stronger industrial and economic ties to South Africa.

Related News

Minister pours cold water on World Bank Ease of Doing Business report

The government has dismissed a new report by the World Bank showing that Kenya has made a slight improvement in its business regulatory environment.

The 2015 Ease of Doing Business index report fails to capture recent developments, according to Industrialisation and Enterprise Development Cabinet Secretary Adan Mohamed.

The study was released by the global lender on Tuesday and shows that the country edged to position 136 this year from last year’s position 137 in the global competitiveness ranking.

Mr Mohamed said on Wednesday that the survey did not include reforms undertaken by the government in the last one year and, therefore, did not reflect the current situation in the country.

“These latest results do not capture the reforms undertaken by the government in the last 12 months. We see an improving business climate as a result of the reforms that various government agencies have undertaken, but more needs to be done,” Mr Mohamed said.

The Kenya Private Sector Alliance (Kepsa) backed the government’s position.

The minister cited the reduction of the period taken to register a company from 32 days a year ago to a day, the introduction of an electronic tax payment system (iTax) by the Kenya Revenue Authority and decentralisation of Huduma Centres as some of the initiatives by the government to improve the business environment but which were omitted in the survey.

NOT REPRESENTATIVE

At the meeting, Kepsa said the survey included responses from as low as two participants in some categories, a situation they said was not representative of the entire country.

“Kenya has recently become the leading destination for global-scale investments with major companies choosing to locate their African operations through their headquarters in the country, an achievement we are proud of,” Kepsa chief executive Carole Kariuki said.

The government now plans to carry out periodic surveys to audit progress of reforms in business regulation.

Mr Mohamed said a team of 40 individuals drawn from government agencies, the private sector and leading business schools in the country had been identified to carry out the exercise.

“We are optimistic that going forward and given the Business Environment Delivery Unit launched recently, we will see our country ranked even higher in coming years,” he said.

The World Bank report shows that sub-Saharan Africa had the highest number of reforms last year with 74 per cent of the region’s economies improving their business regulatory environment for local entrepreneurs.

In the East Africa, Rwanda and Burundi were cited as having made significant multiple improvements in the past five years, alongside Cape Verde and Ivory Coast.

Related News

The Continental Free Trade Area: What’s going on?

Regional integration has been a core element of African countries’ development strategies since independence.

The Africa-wide development agenda, as championed by the African Union (AU), is based on regional integration and the formation of an African Economic Community (AEC). This was laid out in the 1980 Lagos Plan of Action for the Economic Development of Africa and the Abuja Treaty of 1991.

The Africa regional integration roadmap considers the Regional Economic Communities (RECs) as the building blocks of the AEC. The AEC is to be formed in six phases over 34 years, as outlined below:

At its 18th Ordinary Session in January 2012 in Addis Ababa, on the theme “Boosting Intra-African Trade,” the Assembly of Heads of State and Government of the AU adopted a decision and a declaration that reflected the strong political commitment of African leaders to accelerate and deepen the continent’s market integration. The Heads of State and Government agreed on a roadmap for establishing a Continental Free Trade Area (CFTA) by the indicative date of 2017.

As highlighted in the roadmap, the CFTA is set to build on the Tripartite FTA negotiations, which would create a free trade area among the 26 countries of the East African Community (EAC), the Common Market for Eastern and Southern Africa (COMESA) and the Southern African Development Community (SADC). Since the formal launch of the negotiations in 2011, significant progress has been made, and leaders have expressed confidence that the negotiations will be successfully concluded by the end of 2014, with the agreement to be fully implemented by 2016. The 26 Tripartite countries represent close to 60 percent of the AU’s GDP and population, and an FTA among them would constitute a fundamental building block for the CFTA.

The 18th AU Summit in early 2012 opened the discussions on a second bloc of combined RECs (ECOWAS, ECCAS, CEN-SAD, and AMU) to emulate the TFTA. Initial consultations took place in April 2013, and the first negotiation meeting on the second bloc occurred in December 2013. A formal Memorandum of Understanding outlining how decisions will be made and establishing coordination mechanisms still needs to be signed, along with the launching of work on technical studies and key institutional preparatory work on the formation of this second bloc.

Rationale for a CFTA

During its 19th Ordinary Session in July 2012, the AU adopted a decision that highlighted the gains from the CFTA for intra-African trade, through the High-Level African Trade Committee and the consultations of the Committee of Seven Heads of State and Government, which addresses the challenges of intra-African trade, infrastructure and productive capacities.

The creation of a single continental market for goods and services, with free movement of business people and investments, would help bring closer the Continental Customs Union and the African Common Market envisaged in phases 4 and 5 and turn the 54 single African economies into a more coherent, larger market. The larger, more viable economic space would allow African markets to function better and promote competition, as well as resolve the challenge of multiple and overlapping RECs, helping thereby to boost inter-REC trade. Moreover, the sheer size of the single market would provide a more conducive environment for industrial diversification and regional complementarities than what is viable under existing individual country approaches to development.

The United Nations Economic Commission for Africa (UNECA) calculates that the CFTA could increase intra-African trade by as much as $35 billion per year, or 52 percent above the baseline, by 2022. Imports from outside of the continent would decrease by $10 billion per year, and agricultural and industrial exports would increase by $4 billion (7 percent) and $21 billion (5 percent) above the baseline, respectively. If coupled with complimentary trade facilitation measures to boost the speed and reduce the cost of customs procedures and port handling, the share of intra-African trade would more than double over the baseline, to 22 percent of total trade by 2022.

Looking at the potential impact on the EAC for instance, one can see the potential for significant gains from a CFTA. Despite significant increases in intra-community trade within the EAC, the levels of trade between the EAC and other African countries, particularly those outside of the Tripartite area, remains limited. There has been renewed interest in expanding trade and investment links further afield. For example, Nigeria – which officially became the largest economy in Africa in 2014 – and the ECOWAS sub-region could present a significant export market for EAC businesses. In 2012, EAC exports to ECOWAS amounted to $132 million, for a market of close to 300 million people. West Africa currently relies on extra-African imports of coffee and tea, and the EAC could be in a position to tap into this market, if high tariffs and weak transport links can be addressed. In May 2014, Kenya and Nigeria signed trade pacts aimed at deepening trade ties, following high-level political meetings and several large Nigerian business delegation visits to East Africa. Trade with neighbouring Central African States (ECCAS) has shown significant growth, with exports to the region expanding by close to 40 percent between 2010 and 2012, from $1.2 billion to almost $1.7 billion. The CFTA would further open doors to West and Central Africa, through the reduction and eventual elimination of tariffs and improved trade facilitation and infrastructure.

Current Status of the CFTA

The January 2014 AU Heads of State meeting reaffirmed the commitment to the CFTA roadmap, and highlighted the need to launch the CFTA negotiations in 2015.

The second meeting of the Continental Task Force on the CFTA took place in Addis Ababa in early April 2014. The meeting put forward draft objectives and guiding principles for negotiating the CFTA, which were presented to the Extraordinary Session of the Conference of AU Ministers of Trade (CAMOT) in Addis Ababa between April 23 and 28 this year. The session was attended by officials from member states, six RECs (including the EAC), and private sector organisations (East African Buisness Council, CBC, Federation of West African Chambers of Commerce).

Key recommendations from the ministers included the following:

-

Further discussions on and refining of the Draft Objectives and Principles and the Draft Institutional Arrangements for the CFTA, should be undertaken and presented to the 9thSession of CAMOT (scheduled for early December 2014).

-

The AU Commission should prepare Draft Terms of Reference of the CFTA-Negotiating Forum based on best practices in the RECs and/or the Tripartite FTA and submit a draft for discussion at the next meeting of senior trade officials.

During the June AU Heads of State Meeting in Malabo, the High Level African Trade Committee (HATC) called on member states to maintain the momentum in the CFTA time table, and authorised trade ministers to meet as often as needed to ensure the launch remains on track.

The Role of RECs

Even though member states have the sole mandate to negotiate and agree to international trade agreements, the RECs can play an important role in facilitating the negotiations and building national-level capacity and ownership, especially if the CFTA structure is to build on the Tripartite FTA as well as ECOWAS and ECCAS FTAs (CFTA acquis).

In terms of the implementation strategy for the broader Boosting Intra-African Trade (BIAT) initiative, the April Extraordinary Session of the CAMOT recommended the following:

-

The AU Commission, REC Secretariats and UNECA should continue their consultations with all Member States in order to ensure ownership;

-

There is need for more coordination between AUC and RECs including the exchange of information on integration so that regional processes will feed into continental processes;

-

Member States and REC Secretariats should designate national and regional focal points and establish the technical working groups for the BIAT/CFTA in line with the July 2012 Summit Decision.

Opportunities and challenges

Negotiating an agreement of this magnitude will be an enormous undertaking, and will require the political will of leaders across the continent. Important issues to be considered include:

-

The AU includes many smaller least-developed countries, as well as economic powerhouses such as Nigeria and South Africa. It will be important that the CFTA negotiating framework allows for all member states to effectively participate and the negotiations reflect the interests of the poorest countries on the continent. Capacity building on the key technical issues will be a vital component to ensure all countries can effectively engage.

-

The TFTA negotiations included two phases, the first covering tariff liberalisation, rules of origin, customs procedures and simplification of customs documentation, transit procedures, non-tariff barriers, trade remedies and other technical barriers to trade and dispute resolution, and the second covering trade in services, facilitating movement of business people, competition policy and intellectual property. It may be more practical for the CFTA to cover all of these areas from the get-go, to conform to modern FTA structures.

-

Constructive engagement with the private sector and civil society will be vital to generate the momentum to drive the process forward. The private sector must be engaged from the start, including via national and regional chambers of commerce, to understand the process and potential economic benefits from the agreement. In November 2013, the Pan-African Chamber of Commerce and Industry (PACCI), representing 35 national chambers, signed a Memorandum of Understanding with the African Union outlining its support to the CFTA process and highlighting the need to engage with the business community.

The way forward

The meeting of trade ministers in December will be a critical milestone as the AU Commission will present key negotiating principles for consideration prior to the January 2015 High Level African Trade Committee, currently chaired by the President of Ghana, John Dramani Mahama.

To ensure the successful launch of the negotiations by June 2015, there will be a need for further thinking on the key technical issues and structure for the negotiations, as well as a concerted drive to engage with the private sector and the public at large across the continent to ensure this will not be just another Addis-driven “top-down” political exercise.

Ilmari Soininen is a senior consultant with Saana Consulting and a grant officer with the DFID Trade Advocacy Fund.

This article is published under Bridges Africa, Volume 3 - Number 9 by the International Centre for Trade and Sustainable Development.

Africa still attractive despite challenges

The confidence index for Africa among business leaders has remained unchanged over the third quarter of 2014, according to YPO Global Pulse.

The Young Presidents’ Organisation (YPO) Global Pulse Confidence Index for Africa released on Tuesday puts Africa at 61.9 points despite the Ebola outbreak that is rampaging West African states.

According to Paul Kavuma, CEO at Catalyst Principal Partners, business leaders in Africa maintained a cautious optimism.

“Any sort of confidence rating over 60 per cent still shows strong confidence and optimism in the economy. So generally Africa although it remains stagnant from one perspective, it is actually stagnant but at a high level and while it may have been stagnant because there are some economics that have been under more pressure while others have been really racing well and doing extremely well,” Kavuma said in a statement.

Slight alterations were seen in Africa’s one year outlooks for sales and capital spending. Employment confidence rose marginally by one-tenth of a point to 57.4.

“While there were increased geopolitical risks in the third quarter coming from both inside and outside the continent, they are not yet expected to be long-lived enough to counteract the economic tailwinds of infrastructure investment and strengthening services sector,” Paul Berman chair at YPO’s Africa region said in a statement.

The quarterly electronic survey conducted in the first two weeks of October with 2,431 CEO’s across the globe, including 152 in Africa saw variations in confidence at the country level. South Africa, the highest weighting in the index shaved off 1.3 points to read at 63.3 points while Africa biggest economy, Nigeria, rose marginally by 0.4 points to 56.7. Meanwhile, Kenya, East Africa’s largest economy climbed 3.7 poijnts to 68.7 over the third quarter.

“If you look at the macro environments, it is improving. We [East Africa] have got better governance, better accountability, more investment in infrastructure, better provision of services and the business community therefore is responding whereas if you look at our economy in East Africa 20 years we probably had very export orientated economy,” Kavuma explained.

Meanwhile globally, the YPO confidence index dropped by 0.8 points. Confidence in Asia declined by 1.8 points, Australia dipped 1.5 points, Canada shaved off 0.7 points despite it being the world most upbeat region, European Union was down 2.5 points and the United States also down by 0.6 points.

Nonetheless, the Middle East and North Africa were up with a reading of 65.8 points.

Related News

Delays in mega projects bleed the nation

Three road projects, two dams and one hospital financed with public money have run short of time and price, consuming far more money than originally designed, hence pressure on public coffers, a new survey discovered.

The Adiremet-Dejen Dansha, Azezo-Gorgora, Mhal Meda-Alem Ketema road projects, the Ribb and Tendaho Kessem irrigation dam projects, as well as the Jimma University Teaching & Referral Hospital have taken time beyond original schedule and budgets, according to the report. These were half of the 16 government financed projects found to be failing to meet budget both in time and cost, Construction Sector Transparency Initiative (CoST) Ethiopia said.

CoST is a global initiative started in South Africa and the United Kingdom in October 2012, with the support of the World Bank. Ethiopia is one of the five African countries covered In the Initiative. Guatemala, the Philippines, and Vietnam are the other countries where CoST looks at major roads, water and building projects and their procuring entities as well as the way in which procurements are carried out.

“The aim of these surveys is to guarantee that government entities engaged in the construction of large projects have a transparent procuring system,” said Eyasu Yemer, country manager at CoST Ethiopia.

Close to 25 projects in Ethiopia – from roads to education, water and health sectors – were under the watchful eyes of CoST during its pilot phase five years ago before the official launch in 2012. It found at the time that “the feasibility and design stage as well as bid evaluation process and contract implementations,” are found to be a major cause of concern, according to CoST.

Its latest report was a result of its second scrutiny on Ethiopia, focusing on 16 projects. The findings were tabled two weeks ago to officials from the Federal Ethics & Anti-Corruption Commission (FEACC) and the construction as well as procurement agencies at the Elilly Hotel, on Guinea Conakry Street, near the United Nations compound in Kazanchis area.

The second phase of Adiremet-Dejena-Dansha project, a 97Km road construction in northwestern regions of Tigray Regional State, was reckoned to be finalised in February 2012. It was only three fourth of the projects that came to finalisation this month. The price of time lag on this has cost the federal roads authority an additional 274 million Br from the originally projected cost. Lack of transparency and prolonged procurement, design modification as well as limited capacity of the contractor, are attributed as major problems, according to the report.

Contracted out to the Chinese Hunan Huanda Road & Bridge Corporation (HHRBC), this road will connect, upon completion, areas in the Tigray Regional State to the Gondar-Humera road at Dansha Town.

Another project, a 72Km road from Mehal Meda to Alem Ketema, undertaken by Sunshine Construction Plc, remains under construction, although its deadline passed in September 2014, after three years of work. With a budget of 802 million Br, the project was only 30pc completed during site inspection by COST-Ethiopia in June 2014.

The delay was caused due to change in the first design, which took a year and a half, according to Samuel Tafesse, chairman of Sunshine Construction. Nonetheless, completion is now expected in February 2016, he told Fortune.

The construction of Ribb Irrigation Dam in South Gonder, in the Amhara Regional State, was projected to cost 1.3 billion Br upon completion two years ago. A redesign work carried out in October 2007 led to price escalation that nearly doubled the cost, which the Ministry of Water, Energy & Irrigation (MoWEI) hopes would develop 20,000ha of farm land. The project was 62pc complete in June 2014.

“We understand that there is a delay in the time of completion on these specific projects and a cost overrun,” said Bezuneh Tolcha, communication director at the Ministry. “This came about because of machinery and human resource shortages with the contractors.

The contractors are the state owned Water Works Design & Supervision Enterprise (WWDSE) and Water Works Construction Enterprise (WWCE).

Atakilt Teka, chief executive officer of WWCE, blames outdated cost valuation conducted in 2005.

“This in return made us short in finance, of which machinery could neither be bought nor rented,” Atakilt told Fortune. “There was also a shortage of inputs such as cement; we are running the project at a Negative cost.”

The response from the federal agencies responsible for these projects is quite cautious.

“We are yet to find out the details of the findings,” Samson Wendimu, communications manager of the Ethiopian Roads Authority (ERA), told Fortune. “We have already begun working with CoST-Ethiopia. We welcome their recommendations though.”

Related News

Integration: Rwanda back to ECCAS

Since 2010, Rwanda withdrew itself from the Economic Community of Central African States (ECCAS). This absence within the biggest grouping of Central Africa will be for short-term according to the Rwandan Minister of Foreign Affairs. Participating on 27th October 2014 in a military operation including troops coming from eight countries of the community, Louise Mushikiwabo announced the return of his country into the big family.

“Rwanda is henceforth a country very far from tragedy (genocide of 1994), that stabilized itself and is ready to contribute to ECCAS, so at the next ECCAS summit that is going to take place in a few weeks, Rwanda is going to reinstate this organization”, indicated the Minister who explained the withdrawal of his country by the financial crisis that has shaken Rwanda since the genocide of 1994.

“We suspended our participation because, since the genocide of 1994, Rwanda has been a country in reconstruction. Thus, we thought that we could not completely contribute to ECCAS”, specified Louise Mushikiwabo.

Created in 1984, ECCAS has for mission “promotion and strengthening of harmonious cooperation and dynamic, well-balanced and self-maintained development in all domains of economic and social activity, particularly in the domains of industry, transport and communications, energy, agriculture, natural resources, business, customs, monetary and financial questions, human resources, tourism, education, culture, science and technology and movement of people in order to realize collective autonomy, raise the standard of living of populations …”

It includes at present ten countries: Angola, Burundi, Cameroon, Central Republic of Africa, Congo, Gabon, Equatorial Guinea, Democratic Republic of Congo, Sao Tome and Principe and Chad.

Related News

Kenya, Mozambique in deal to boost trade

Kenya and Mozambique on Wednesday signed a bilateral agreement to cut restrictions on air travel between them.

The deal signed by Transport Cabinet Secretary Michael Kamau and Mozambique Deputy Minister for Transport and Communications Manuela Joaquim Rebelo is also aimed at increasing the volume of trade between the two countries while improving bilateral relations.

It also allows privately owned airlines with substantial local ownership from both countries to apply for licences to fly between Maputo and Nairobi.

Currently national carrier Kenya Airways and LAM Mozambique Airline are the only ones allowed to operate between the two countries with five frequencies weekly.

The introduction of other airlines will spur competition which will likely lead to a fall in the cost of flying with Mr Kamau insisting that the government would not try to regulate the price but provide conditions that would attract more players in the industry.

“It is a free market and there is no way we can control ticket prices. The only thing we can do is to promote an environment that supports growth.”

While calling for privately owned airlines to apply and operate on the route, Mr Kamau said the government was committed to implementing an open sky policy with all African countries.

“There is no reason why someone travelling to a destination in Africa has to go through the Middle East or Europe,” the minister said, adding that Kenya was negotiating with Rwanda to sign a similar agreement.

IMPROVE CONNECTIVITY

“As a ministry, we are committed to negotiating and renewing bilateral air service agreements to expand the air route network available to local airlines on the continent in order to improve connectivity which will allow flexibility in movement of cargo and passengers,” he said.

The agreement also allows airlines to sign code share agreements which will make it cheaper for smaller airlines to travel between the two countries with minimal losses.

A code share agreement is a deal where two or more airlines share the same flight to cut losses associated with below capacity flights.

Related News

Sub-Saharan Africa implements the most business regulatory reforms worldwide

A new World Bank Group report finds that Sub-Saharan Africa had the highest number of business regulatory reforms globally in 2013/14, with 74 percent of the region’s economies improving their business regulatory environment for local entrepreneurs.

Doing Business 2015: Going Beyond Efficiency finds that Benin, the Democratic Republic of Congo, Côte d’Ivoire, Senegal, and Togo are among the 10 top improvers worldwide, having improved business regulation the most in the past year among the 189 economies covered. Since 2005, all countries in the region[1] have improved the business regulatory environment for small and medium-size businesses, with Rwanda implementing the most reforms, followed by Mauritius and Sierra Leone.

The report series shows that over the past five years, 11 different Sub-Saharan African countries have appeared on the annual list of the 10 global top improvers. Some have done so multiple times, such as Burundi, Cabo Verde, Côte d’Ivoire, and Rwanda.

“Sub-Saharan African economies have come a long way in reducing burdensome business regulations,” said Melissa Johns, Advisor, Global Indicators Group, Development Economics, World Bank Group. “Our data show that Sub-Saharan Africa accounts for the largest number of regulatory reforms making it easier to do business in the past year, with 75 of the 230 documented worldwide. Yet despite broad regulatory reform agendas, challenges persist in the region, where business incorporation continues to be costlier and more complex on average than in any other region.”

The report finds that Senegal implemented regulatory reforms in six of the 10 areas tracked by Doing Business – a global high for the year. Thanks to such reforms, Senegal is gradually narrowing the gap with best practices seen elsewhere. For example, in 2005, completing every official procedure to import goods from overseas took 27 days. Today it takes 14 days, the same as in Poland.

This year, for the first time, Doing Business collected data for a second city in the 11 economies with a population of more than 100 million. In Nigeria, the report now analyzes business regulations in Kano as well as in Lagos.

The report this year also expands the data for three of the 10 topics covered, and there are plans to do so for five more topics next year. In addition, the ease of doing business ranking is now based on the distance to frontier score. This measure shows how close each economy is to global best practices in business regulation. A higher score indicates a more efficient business environment and stronger legal institutions.

The report finds that Singapore tops the global ranking on the ease of doing business. Joining it on the list of the top 10 economies with the most business-friendly regulatory environments are New Zealand; Hong Kong SAR, China; Denmark; the Republic of Korea; Norway; the United States; the United Kingdom; Finland; and Australia.

[1] Excludes South Sudan, which was added to the Doing Business sample in 2013.

About the Doing Business report series

The annual World Bank Group flagship Doing Business report analyzes regulations that apply to an economy’s businesses during their life cycle, including start-up and operations, trading across borders, paying taxes, and resolving insolvency. The aggregate ease of doing business rankings are based on the distance to frontier scores for 10 topics and cover 189 economies. Doing Business does not measure all aspects of the business environment that matter to firms and investors. For example, it does not measure the quality of fiscal management, other aspects of macroeconomic stability, the level of skills in the labor force, or the resilience of financial systems. Its findings have stimulated policy debates worldwide and enabled a growing body of research on how firm-level regulation relates to economic outcomes across economies.

Each year the report team works to improve the methodology and to enhance their data collection, analysis and output. The project has benefited from feedback from many stakeholders over the years. With a key goal to provide an objective basis for understanding and improving the local regulatory environment for business around the world, the project goes through rigorous reviews to ensure its quality and effectiveness. This year’s report marks the 12th edition of the global Doing Business report series.

Related News

Doing Business rankings use expanded data analysis

Singapore tops the list of business-friendly economies globally, while five of the top 10 most improved countries are in sub-Saharan Africa, according to the World Bank Group’s Doing Business 2015 rankings.

The 12th annual report finds that the 10 economies with the most business-friendly regulatory environments are Singapore; New Zealand; Hong Kong SAR, China; Denmark; the Republic of Korea; Norway; the United States; the United Kingdom; Finland; and Australia.

The 10 economies that have improved the most since the previous year are Tajikistan, Benin, Togo, Côte d’Ivoire, Senegal, Trinidad and Tobago, the Democratic Republic of Congo, Azerbaijan, Ireland, and the United Arab Emirates.

Sub-Saharan African countries had the highest number of regulatory reforms – 75 of 230 around the world – while emerging Europe and Central Asia had the highest percentage of improving countries. Progress was uneven in the Middle East and North Africa, with conflict-affected Syria near the bottom. South Asia saw the lowest number of reforms.

While 80% of countries in the study improved their business regulations last year, only about one-third moved up in the rankings. However, the gap between the best- and worst-performing countries continues to narrow as countries improve their business climates, said Rita Ramalho, manager of the Doing Business Project.

“It’s easier to do business this year than it was last year, than it was two years ago or 10 years ago,” she said. “We see that the economies that score the lowest are reforming more intensely, so they are converging toward the economies that do the best.”

For example, in 2005 it took an average of 235 days to transfer property in the lowest-ranked countries and 42 days in the top-ranked countries – a difference of 193 days. The gap now has narrowed to 62 days (around 90 days for the lowest-ranked and less than 40 for the top-ranked).

The report measures the ease of doing business in 189 economies based on 11 business-related regulations, including business start-up, getting credit, getting electricity, and trading across borders. The report does not cover the full breadth of business concerns, such as security, macroeconomic stability, or corruption.

This year’s report, “Doing Business 2015: Going Beyond Efficiency”, uses new data and methodology in three areas: resolving insolvency, protecting minority investors, and getting credit.

“We want people to be aware this is a different report and that we’re measuring new areas we weren’t measuring before,” said Ramalho.

For that reason, the report cannot be directly compared with last year’s, she said. (The 2014 rankings have been recalculated based on the new methodology.)

“Doing Business is by and large about the efficiency of regulations – how fast, how cheap, how simple it is to get a transaction completed. But now we’re branching out to also measure the quality” of regulations, she said.

New data reveal regulatory efficiency and regulatory quality go hand in hand. “We see a high correlation between the two. Countries that do it fast and cheaply are also likely to do it well,” said Ramalho.

The resolving insolvency indicator, for example, previously focused on the efficiency of the bankruptcy court system. This year’s report looks at the strength of the underlying legal system governing insolvency and whether laws follow good practices. Countries that rank low on this indicator often have outdated laws or lack an insolvency law altogether. Some countries have good laws on the books but do not implement them efficiently. Yet, without a well-functioning insolvency process in place, it’s more difficult for entrepreneurs to get financing and less likely they would risk failure or venture into a new business, said Ramalho.

“No one, looking ahead, would start a business if it’s very hard to close one,” she said. “Failure is part of life, so you want to have a legal system that knows how to deal with that.”

The 2015 report also includes data from two cities rather than one for 11 countries with more than 100 million people (Bangladesh, Brazil, China, India, Indonesia, Japan, Mexico, Nigeria, Pakistan, the Russian Federation, and the United States). In most cases, the report did not find significant differences between the two cities in terms of business climate.

Next year, Doing Business will enhance methodology, data collection, and analysis for five more indicators: obtaining construction permits, getting electricity, registering property, paying taxes, and enforcing contracts.

Related News

WTO publishes annual package of trade and tariff data

The WTO released on 28 October 2014 new editions of its key statistical publications: International Trade Statistics, Trade Profiles, World Tariff Profiles and Services Profiles. The four publications provide a detailed breakdown of the latest trade developments.

International Trade Statistics 2014 provides a detailed overview of world trade up to the end of 2013, covering merchandise and services trade as well as trade measured in value-added terms.

A variety of charts illustrate noteworthy trends in global trade while numerous tables provide more detailed data. A chapter on methodology explains how the data are compiled.

World Tariff Profiles 2014 provides a unique collection of data on tariffs imposed by WTO members and other countries. It is jointly published by the WTO, the International Trade Centre (ITC) and the UN Conference on Trade and Development (UNCTAD).

The first part of the publication provides summary tables showing the average tariffs imposed by individual countries. The second part provides a more detailed table for each country, listing the tariffs it imposes on imports (by product group) as well as the tariffs it faces for exports to major trading partners. The profiles show the maximum tariff rates that are legally “bound” in the WTO and the rates that countries actually apply. This edition of World Trade Profiles has anti-dumping measures as its special topic, and includes a compilation of frequently asked questions.

Trade Profiles 2014 provides a snapshot summary of the most relevant indicators on growth, trade and trade policy measures on a country-by-country basis.

The data provided include basic economic indicators (such as gross domestic product), trade policy indicators (such as tariffs, import duties, the number of disputes, notifications outstanding and contingency measures in force), merchandise trade flows (broken down by broad product categories and major origins and destinations), services trade flows (with a breakdown by major components) and industrial property indicators.

Services Profiles 2014 provides key statistics on “infrastructure services”, i.e. transportation, telecommunications, finance and insurance, for some 150 economies.

The information is derived from multiple sources, such as national accounts, employment statistics, balance of payments statistics, foreign affiliates’ trade in services statistics, foreign direct investment statistics and quantitative indicators largely sourced from international/regional organizations and specialized bodies. The profiles reflect data as contained in the WTO’s Integrated Trade Intelligence Portal (I-TIP) services database as of July 2014.

All three profiles – World Tariff Profiles, Trade Profiles and Services Profiles – are now available in the WTO Statistics Database in Excel and HTML formats, and the PDF versions are available in English on the WTO web site. The WTO Statistics web page also contains updates of the International Trade and Market Access data online application, the Tariff Analysis Online and Tariff Downloads applications, new versions of World and Regional Export Profiles (a PDF snapshot of 2013 merchandise exports globally and by region) and World Commodity Profiles (a PDF snapshot of 2013 merchandise exports and imports for total merchandise trade, agriculture, fuels and mining and manufactured products), and World maps, which allow for comparison between countries or customs territories on selected economic indicators.

Related News

‘The only way to stop Ebola is at its source’ – UN chief

Secretary-General Ban Ki-moon on Tuesday urged countries that have imposed travel bans or closed their borders in response to the Ebola outbreak of the need to convey a sense of urgency without inciting panic, saying “the only way to stop Ebola is to stop it at its source.”

Mr. Ban spoke to reporters alongside African Union Commission Chairperson Nkosazana Dlamini-Zuma and World Bank President Jim Yong Kim in the Ethiopian capital of Addis Ababa, where they had discussed how the three organizations and their partners can help efforts to stop the Ebola epidemic unfolding in West Africa.

Meanwhile, the Geneva-based UN World Health Organization (WHO) welcomed the approval by Swissmedic – the Swiss regulatory authority for therapeutic products – for a trial with an experimental Ebola vaccine at the Lausanne University Hospital, saying “this marks the latest step towards bringing safe and effective Ebola vaccines for testing and implementation as quickly as possible.”

Also today, the UN Mission in Liberia (UNMIL) reported that its Chinese peacekeeping contingent will assist in the construction of an Ebola Quarantine and Control Center in the Liberian capital, Monrovia. The project is expected to take 21 days to complete.

The UN continues to work with its partners to ramp up efforts to tackle all aspects of the outbreak, and in Addis Ababa today, Mr. Ban said: “Ebola is a major global crisis that demands a massive and immediate global response. No country or organization can defeat Ebola alone. We all have a role to play.”

In that regard, the Secretary-General said he was very heartened to learn of the pledges by African nations, most recently Ethiopia, Burundi and Nigeria and the Democratic Republic of the Congo, to deploy medical personnel to assist Ebola victims that have claimed nearly 5,000 lives in Guinea, Liberia and Sierra Leone.

“I am particularly encouraged by the decision of Nigeria and the Democratic Republic of the Congo to deploy medical personnel, and of Senegal to serve as a logistics hub for the response, following success in containing their own outbreaks,” he said.

The UN chief said he is in constant contact with world leaders “to help us create dedicated medical facilities for in-country treatment of responders and to put in place medical evacuation mechanisms.”

“We have a long way ahead to contain and curb the Ebola outbreak and to help the affected countries rebuild their health systems to better withstand future shocks,” he said.

According to WHO spokesperson Tarik Jasarevic, the agency has 176 health personnel on the ground, while 700 had been deployed and rotated since the beginning of the outbreak. At any given time, he said there were about 200 people on the ground. In addition, medical teams from other organizations including medical teams from Cuba, China, and other countries.

Mr. Jasarevic stated that 230 more burial teams are needed, to ensure 70 percent of safe burials. Eight to 10 people are needed for one burial team.

In response to a question about the politicians in Australia and the United States calling for restrictions on people returning from affected countries, Mr. Jasarevic said mandatory quarantine was not recommended, as people were not contagious until they were showing symptoms.

The Secretary-General in Addis Ababa drew attention to travel bans and border closures imposed by some countries, saying such measures will only isolate the affected countries, and obstruct response efforts.

“The only way to stop Ebola is to stop it at its source,” Mr. Ban said.

“I thank the African Union (AU) for its strong and consistent position on this point,” he said, and asked the AU to continue to appeal to its member states not to impose travel restrictions or close their borders, but rather to deploy the essential human resources.

“We urgently need more trained foreign medical teams to deploy to the region,” he said.

Meanwhile, the UN World Food Programme (WFP) noted that the spread of Ebola was disrupting food trade and markets in the three affected countries. In Geneva, WFP spokesperson Elisabeth Byrs said that in Sierra Leone, local weekly markets were banned. In Monrovia, the price of cassava flour had more than doubled after the closure of the border with Sierra Leone, and in Liberia prices for imported rice had continued to increase beyond the summer pattern, Ms. Byrs said.

“Should the Ebola epidemic last another four to five months when farmers would begin to prepare their lands, there would be a real concern that planting for the 2015 harvest could be affected,” she said.

Related News

Are we heading for “same old, same old” for the proposed Tripartite FTA Rules of Origin?

SADC, COMESA and EAC comprise 26 Southern and East African Countries currently negotiating a comprehensive tripartite FTA with new preferential origin rules.

The SADC-COMESA-EAC Tripartite Free Trade Area (TFTA) was formally launched at a summit in Johannesburg, South Africa, in June 2011. This followed a Tripartite Summit in Uganda in 2008 where the heads of State and Government of the respective regional economic communities (RECs) agreed on a “programme of harmonization of trading arrangements amongst the three RECs, free movement of business persons, joint implementation of inter-regional infrastructure programmes as well as institutional arrangements on the basis of which the three RECs would foster cooperation”.

The comprehensive TFTA would be negotiated in tranches, with market access forming part of the first 3-year tranche. This self-imposed deadline has come and gone, with significant progress made on market access offers and in other areas.

Rules of Origin (RoO) are the regulations that specify the level of local processing of materials and goods, where these contain imported content, that must be undertaken in order to earn local origin status, and thus qualify for trade preferences. With so much at stake – since RoO count among the critical fine-print that defines trade liberalisation at a practical level – this aspect of the negotiations was always going to be fraught with challenges. Key amongst them is the fact that each of the respective RECs apply their own set of origin rules, notwithstanding a frequent misperception that two of the RECs (COMESA and EAC, with overlapping membership) already employ the same rules.

Towards a common TFTA RoO standard

In order to give effect to the notion of a preferential trade area, the regions will have to adopt a common RoO standard. In this respect, history is not particularly kind, given that the SADC FTA RoO negotiations took a decade to complete (exceptions remain), having switched to a line-by-line approach under the Amended Trade Protocol. SADC adopted the “European style” RoO, similar to what South Africa already had in its bilateral agreement with the EU, and which the other partner states already knew from the EU GSP and Cotonou arrangements. This ‘new’ model has implications for the TFTA negotiations, as it significantly increases the areas of divergence with COMESA and EAC rules.

TFTA negotiations are conducted through the Tripartite Trade Negotiations Forum (TTNF), with specific technical areas being dealt with by Technical Working Groups (TWG), for example on RoO (the RoO TWG had met seven times as of August 2014), the TWG on trade remedies, the TWG on customs cooperation and so forth. Given the substantial differences between the respective REC RoO, and the sensitivities around RoO, the TWG adopted a somewhat practical approach, involving an audit of the respective RoO instruments and drawing up three matrices identifying cases where the product-specific rules (also known as the ‘list rules’) are substantively the same across the RECs, instances where they are similar, and those where they are different. Given the complexities involved in achieving a common outcome, and the pace of the negotiations, it was agreed in the TTNF not to re-open negotiations in those categories where ‘common or identical’ rules exist. These commonalities would thus represent a low hanging fruit, so to speak, to cover at least some product categories when the trade agreement launches.

This exercise resulted in 15 percent of tariff headings being identified as having common rules – not necessarily verbatim but to equal effect. An additional 29 percent were found to have ‘similar’ rules. More than half of the rules were found to be different (in other words neither common nor similar) across the RECs, implying that common rules would need to be negotiated on a line-by-line basis in these instances. This has not happened yet but indications are that the process could begin in earnest later in 2014 at the next TWG meetings.

Without doubt, this is a daunting process not only given the divergent economic offensive and defensive interests within the 26-member TFTA group and the different levels of development, but also from an entirely different perspective: This involves negotiations

(a) that are often highly technical in nature and therefore demanding on the officials tasked with negotiations (along with the fact that there is often personnel change among officials, which risks undermining continuity);

(b) that by nature (should) require broad national consultations and scenario planning to derive informed positions;

(c) whose outcomes and implications are often difficult to measure or predict; and

(d) which potentially impede on current or future policy space, often leading to reservations or intense caution among those involved in the negotiation process.

What progress thus far?

Essentially, the focus to date has been both on the RoO audit (the ‘matrices’), broad agreement on how to deal with the common rules, and on the RoO Protocol. This text – the main RoO Protocol – comprises the general RoO clauses representing the overall framework, dealing with important principles such as cumulation, certification, principles and definitions of what constitutes “wholly produced”, simple (or insufficient) processing, aspects around fisheries (definition of vessels, ownership and registration criteria), agreement on the type of competent authorities tasked with administering origin certification, and so forth.

Notable (albeit expected) early outcomes include provisions for full cumulation among TFTA member states, thus allowing joint compliance with the respective origin requirements among Member States, an aspect that reduces the individual burden of compliance and which is a common feature among preferential trade agreements.

While these developments represent headway towards a TFTA that significantly liberalises trade between Member States and is an important stepping stone in relation to a continental FTA, they might represent relatively little practical benefit to traders and other stakeholders within the region initially. This is notwithstanding the recently agreed roadmap, which proposes signature on at least a partial FTA and agreement on the remaining processes of ratification at the Third Tripartite Summit later this year (with formal launch of the TFTA early in 2015).

The crux for traders however is to what extent tariff liberalisation offers have been agreed and concluded, what is considered ‘sensitive’ and thus excluded from liberalisation, and what the RoO will look like. This process, concerning more than half of the applicable RoO, will no doubt be a difficult and likely time-consuming task.

For example, in terms of the design of RoO, how will countries weigh up local development needs and possible incentives for local production against competing interests in neighbouring countries? What will textile RoO look like, when some countries – as has historically been the case – seek to protect upstream cotton (and to a far lesser extent fabric production) by in effect barring an outcome that would see producers being able to tap into global supply chains for competitive (in terms of price, quality and variety) fabric and yarn to ensure competitive local manufacture of garments? How will say coffee bean or tobacco leaf interests weigh against the needs for some flexibility of downstream beneficiation activities?

How will potentially protectionist leanings by say more industrialised Member States (with greater vested interests relating to established industries) reconcile with those countries that would benefit from greater flexibility? Questions like these raise the all-important issue of development in the TFTA and the role that RoO can, or indeed should, play. The evidence whereby highly restrictive RoO induce development is tenuous, especially within an environment of decreasing tariff barriers (in a sense the counterweight to restrictive rules), which raises the question to what extent ‘development’ should even be considered as something for which RoO are an ‘appropriate’ tool, and to what degree they should carry the burden of responsibility for this.

In that regard, how do we even begin to define ‘development’ in the RoO context? Is a set of (RoO) criteria, designed to induce local economic activities in the hope that a “captive” downstream sector will later utilise these supplies for further beneficiation, a realistic outcome that leads to development? Will these (final) products still be internationally competitive in the respective export market? Or can it not be accepted as realistic that development may more likely flow from “development-friendly” rules where the incentive is provided by flexibility in sourcing (since this is attractive to producers of intermediate and final goods), given that producers would in any case most likely (still) chose local supplies over imports if these are competitive, irrespective of RoO? It is critical not to overlook the link between restrictions that protect upstream suppliers or impose heavy local processing requirements, and the ultimate objective of final goods being able to still compete in the export market.

There is little doubt that rules that simply mitigate (or avoid) the risk of trade deflection and transshipment will often not lead to significant benefits under a preferential trade framework. The regional evidence in TFTA points to relatively low levels of intra-regional trade.

While a good overall balance between these somewhat opposing approaches to RoO is desirable, this will likely remain a challenging task in the broader TFTA context. Given the complexities of RoO negotiations, and the task of doing this for such an extensive list of products currently subject to dissimilar rules within the respective RECs, it may be worthwhile to focus less – perhaps – on the line-by-line negotiations with all its complexities, but rather to ensure first and foremost that mechanisms are agreed that will reduce the effective restrictiveness and compliance burden of the RoO outcome. Specifically, this means a strong focus on extensive and full cumulation among Member States, but also mechanisms for administrative cooperation between all customs bodies and border agencies, to ensure smooth passage for regionally traded goods and agreed instruments to ensure efficient cooperation on the enforcement side.

At a practical level, this could involve a number of features, including:

-

A common free-standing instrument on administrative cooperation on all RoO matters and signed by all parties (rather than bilateral arrangements), to ensure seamless application and respect for the principle of cumulation.

-

Comprehensive and ongoing training and capacity building programs for RoO ‘operators’ (both within customs agencies and private sector) and a priority focus on trade facilitation.

-

A facility such as the Binding Origin Information (BOI) certification, currently available for imports into to the European Union, which could give operators greater long-term certainty through an advanced and binding ruling on the origin status of their goods, usable throughout the TFTA region and respected at each border.

-

A RoO “helpdesk”, specifically to assist regional operators and customs bodies on technical matters relating to the interpretation of rules (or resolution of RoO-related disputes), could potentially play an important role in facilitating and growing regional trade under TFTA preferences. Inconsistent application and adjudication of the rules has been an issue afflicting operators throughout the TFTA region, imposing significant yet avoidable costs on traders and creating uncertainty.

Conclusion

It is worth recalling that it is primarily individuals and firms, not States, which trade with each other and who are the ultimate beneficiaries of RoO. It is they who carry the burden, or enjoy the practical benefits, of regional trade preferences and the associated RoO criteria. While is known that limited consultation between private sector stakeholders and government negotiators does take place, there is an overriding sense that this is not necessarily so throughout the TFTA region and positions are often developed by second-guessing what might be a desirable (and desired) outcome. The TFTA process offers the opportunity of a RoO outcome that deals with some of the challenges and at times highly restrictive practices of the past. A little bit of thinking outside the box here and there may be some of the tonic that is needed during the next phase of negotiations.

Eckart Naumann is a consultant economist, and Associate of the Trade Law Centre (TRALAC), based near Cape Town, South Africa.

Related News

Kenya to review growth target after rebasing – central bank chief

Kenya will review its economic growth target for this year after it recalculated the size of the economy, a move that led to a jump in annual growth rates, its central bank governor said on Monday.

Government officials put 2013’s gross domestic product at $53.4 billion – 25 percent higher than previously stated – after updating the base year for its calculation.

Growth for 2013 was revised up to 5.7 percent from 4.7 percent. The higher growth trend was confirmed when the statistics office said the economy expanded by 5.8 percent in the second quarter, up from 4.4 percent in the first three months.

In September, Treasury Cabinet Secretary Henry Rotich said Kenya was expected to grow by between 5.3 to 5.5 percent in 2014, down from 5.8 percent previously forecast.

“The National Treasury (finance ministry) will review the previous growth target that was based on the old GDP series and is expected to announce new targets,” Njuguna Ndung’u told Reuters.

Ndung’u said he expected the economy to remain resilient this year and in the medium-term mainly due to its diverse nature.

The 5.8 percent expansion in the second quarter surprised many because it came about despite a slump in the tourism sector following a spate of attacks blamed on Islamists.

Output from the construction, manufacturing and financial services rose during the period.

“Various economic and financial indicators including cement and electricity production and consumption coupled with the sustained confidence in the economy suggest a continued pick-up in economic activity,” the central banker said.

He also cited increased foreign direct investment in transport and energy infrastructure, declining commercial lending rates and improvement in the management of spending by new local government units called counties.

Related News

Why banks should embrace structured trade finance

A number of developments have taken place in the banking industry globally and in Rwanda, in particular, with regard to the way conducting of business.

We have recently witnessed mergers and acquisitions in Rwanda’s financial sector and opening shop of new banks on the market.

These developments imply growing competition in local banking industry and call for a lot of innovation on the part of the banks, especially in aggressively rolling out of the existing trade products and developing of new ones.

Structured financing of commodity trade could be one of the measures banks should consider. These techniques of financing and the different applicable trade finance tools originated from the Latin American financial crisis in the mid-1980s. During that period banks were involved in international commodity finance and relied on balance sheet analysis and government guarantees for ascertaining the credit worthiness of borrowers. Security was at times enhanced by tangible assets such as real estate offered as collateral.

However, the international environment for commodity finance has continued to evolve, driven especially by the development of information technology, consolidation of commodity trading and processing industries and increasing liberalisation.

With the consolidation of the commodity industry, only a small number of large creditworthy traders are actively involved in trade, in addition to an increasing number of niche players that are difficult to finance. These niche players if they come for finance, they want the money almost at zero cost.

Due to the effect of consolidation, companies have become much large, with increased credit requirements (compared with own equity), modest capital base and limited access to government guarantees. However, given the high default rate of commodity traders, banks have become hesitant to advance unsecured credit.

Due to privatisation, commodity-trading activities are now controlled by private companies, which has seen the previous government-to-government business backed by state bank letters of credit being replaced by commercial bank funding.

These developments have increased economic and political risks in emerging markets; and the traditional tools are no longer sufficient to dealing with the growing risks and are, therefore, less viable. Producers, processors, traders and banks that fail to adapt to the new realities of international commodity and financial markets risk losing out.

That’s why financial institutions need to adapt the basics of using the new trade finance tools.

The future will see various structured finance tools like pre-shipment or pre-export financing, post-shipment financing, warehouse receipt financing, and structured trade and commodity financing utilised by a number of banks. Large continental and regional banks have already moved in this direction, but most local banks in the market in are yet to embrace it.

All these fundamental tools rotate around identifying the probable risks at whatever level, and the best possible mitigation measures. As banks take on the credit risk, independent collateral managers take on the performance risks on ground.

Commercial banks can make better use of increasingly common external tools that ease the risks, like collateral management services while extending pre or post shipment finance, not just to control goods at one point in the marketing chain (inventory or stock financing), but to control trade flows in the value chain from farm gate to final destination expecting reimbursements through export receivables.

Collateral management services are available locally and globally. In Rwanda, commodities being handled under these highbred services include maize, fertilisers, sugar, rice, petroleum products and pharmaceuticals, among others.

The benefits of these new trade finance services go both ways; for banks, these services provide the ability to lend out more than it would been possible if only physical assets were considered; they reduce the number of non-performing loans as these are transactional based financing and the banks have a constant flow of information through the independent third party. For the trader, the ability to borrow more than what their physical collateral permits is second to none, plus a certain level of proper business management through the collateral manager’s reports.

These services provide comfort to both the financing and borrowing parties that a collateral manager is willing and able to take on the performance risk on ground.

Importantly, there banks need to build their capacity and improve skills in structured finance to be able to apply the tools effectively.

Greater skills in structured finance will, among other things, enable bankers to identify new revenue streams that can be used to underwrite medium and long-term financing.

The writer is the ACE Global Depository Rwanda country manager.

Related News

Trade and Industry working on accelerating manufacturing

The Ministry of Trade and Industry is in the process of developing the first set of sector growth strategies as part of an industrial policy implementation strategy to accelerate manufacturing activities and value addition, and develop local value chains within the country as well as beyond Namibia’s borders.

“We are pursuing industrial cooperation at bilateral and regional level through the Southern African Customs Union (SACU) and the Southern African Development Community (SADC). Just a few days ago I had the privilege to launch the negotiations towards a Retail Charter for Namibia that would, amongst others, provide for local sourcing and supplier development, aimed at enhancing access for local manufacturers to retail shelf space. In addition, we are also reviewing the SME policy, which is largely aimed at assisting SMEs with entering formal business and the manufacturing sector in particular, to enhance linkages and coordination,” said Trade and Industry Minister, Calle Schlettwein.

Speaking at the Namibian Manufacturing Association (MNA) Manufacturer of the Year gala event on October 23, Schlettwein said that in the current financial year a total of 1006 companies, mostly SMEs, have benefited through the ministry’s Business Support Service Programmes

“In our quest to industrialize, Namibia can expect tough competition from a number of sources. In order to remain competitive and relevant, Namibia will have to frequently review and analyze her incentive regime that includes tax and non-tax incentives. I’m glad to inform you that the manufacturing incentives are being reviewed at the moment. The main aim of the incentive regime is to develop our industrial competencies and capacities with the ultimate view to explore the frontiers of our production possibilities. In this, regard, government will deliberately strive to implement measures that will make it easier for businesses to set up and operate in Namibia,” said Schlettwein.

The minister continued that the manufacturing sector plays a strategic role in economic development and is the component of industry that presents significant opportunities for sustained growth.

Such growth, he said, must further translate into sustainable employment and equalized wealth distribution.

“To illustrate, in NDP4, the manufacturing sector is identified as a priority which in the year 2012 generated exports to the value of N$21 billion, the equivalent of 53 percent of total exports of goods that year. Of the N$21 billion, 49 percent consisted of food products and beverages, 13 per cent of refined zinc and blister copper, and the remainder – other manufactured goods. The constant growth in the sector (1.2 percent in both 2011 and 2012) can mainly be attributed to the sub-sector ‘other food products and beverages’ that recorded an increase of 6.5 percent in real value added, following a decline of 5.4 percent a year earlier. This sub-sector alone contributed 40.4 percent of the total manufacturing in 2012 (NSA, National Account 2012),” said Schlettwein.

According to the Namibia Statistics Agency’s Labour Force Survey 2013, there are 32 769 employed workers in the manufacturing sector compared to 28 409 employed in 2012 and related industries which effectively comprises 4.8 percent of the total labour force. This figure shows that the sector is still relatively small in employment terms but expanding (despite the trend towards automation in manufacturing).

- Related: Public Procurement Bill to benefit manufacturing industry (The Villager, 27 October 2014)

Related News

Agreement reached to launch Africa’s largest Free Trade Area

The Tripartite Sectoral Committee of COMEA-EAC-SADC Ministers meeting in Bujumbura, Burundi from 24-25 October 2014 has agreed that the Tripartite Summit of Heads of State and Government to be held in Egypt in mid-December 2014 would launch the Tripartite Free Trade Area (FTA).

The decision to launch the Tripartite FTA took into account the fact that the majority of the Tripartite Member/Partner States have made ambitious tariff offers and were agreed on Rules of Origin to be applied in the interim whilst further work continues on product specific Rules of Origin.

The Tripartite TFA encompassing 26 Member/Partner States from the Common Market for Eastern and Southern Africa (COMESA), East African Community (EAC) and the Southern African Development Community (SADC), with a combined population of 625 million people and a Gross Domestic Product (GDP) of USD 1.2 trillion, will account for half of the membership of the African Union and 58% of the continent’s GDP.

The Tripartite FTA popularly known as the Grand Free Trade Area, will be the largest economic bloc on the continent and the launching pad for the establishment of the Continental Free Trade Are (CFTA) in 2017.

The Tripartite FTA offers significant opportunities for business and investment within the Tripartite and will act as a magnet for attracting foreign direct investment into the Tripartite region. The business community, in particular, will benefit from an improved and harmonized trade regime which reduces the cost of doing business as a result of elimination of overlapping trade regimes due to multiple memberships.

The launching of the Tripartite Free Trade Area is the first phase of implementing a developmental regional integration strategy that places high priority on infrastructure development, industrialization and free movement of business persons. In order for the Tripartite FTA to realize inclusive and equitable growth, the meeting agreed on the need for expeditious formulation and implementation of a regional industrial programme.

The Chairperson of the Ministerial meeting, Honourable Chiratidzo Iris Mabuwa, Deputy Minister of Commerce and Industry of Zimbabwe, hailed the agreement to launch the Grand FTA as a milestone in regional and continental integration.

“Africa has now joined the league of emerging economies and the grand FTA will play a pivotal and catalytic role in the transformation of the continent,” she declared at the close of the meeting. “We have made significant progress in negotiations on trade in goods, and we now need to expedite negotiations on trade-related areas, including trade in services, intellectual property and competition policy to ensure equity, among all citizens of the wider region.”

Related News

Leaders commit billions in major new development initiative for the Horn of Africa