Search News Results

Sharing the wealth

Countries that enjoy a resource windfall should be prudent about distributing it all directly to their people

Angola is the second largest oil producer in sub-Saharan Africa and one of the continent’s richest countries. Yet more children under the age of five die there than in most places in the world.

Most resource-rich countries lack the types of institutions needed to manage natural resource wealth effectively, and past performance does not bode well for countries with a resource windfall. Many of their citizens face continued poverty with little prospect of a significant improvement in living conditions. Angola’s under-five infant mortality rate is a vivid example.

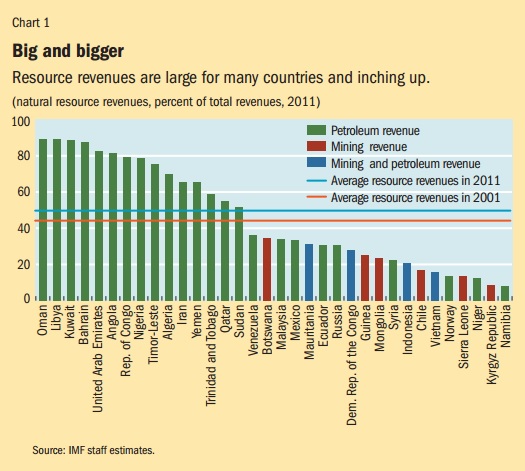

In recent years, high commodity prices and new natural resource discoveries have increased many countries’ resource revenues, both as a share of the  budget and in percent of GDP, offering new prospects for raising the population’s standard of living (see Chart 1 - click to enlarge). But few countries stand out as good examples of effective resource wealth management. Botswana, Chile, Norway, and the U.S. state of Alaska are some exceptions.

budget and in percent of GDP, offering new prospects for raising the population’s standard of living (see Chart 1 - click to enlarge). But few countries stand out as good examples of effective resource wealth management. Botswana, Chile, Norway, and the U.S. state of Alaska are some exceptions.

The experience of the success stories suggests that natural resource wealth management requires a commitment to three interrelated principles: fiscal transparency, a rules-based fiscal policy, and strong institutions for public financial management. For example, Norway and Alaska are models of transparency in the way they collect and budget natural resource revenue. This transparency helps people understand the use of resource wealth and holds political leaders accountable for their decisions. Chile’s fiscal rules protect resource wealth from the vagaries of political pressure, and its strong institutions are able to manage public investment. This helps transform natural resource wealth into productive assets, including infrastructure and human capital.

Some suggest that governments should give up their resource revenue and distribute it directly to the population. There are some good arguments to support this view – and strong arguments against it. Direct distribution is not a silver bullet (Gupta, Segura-Ubiergo, and Flores, 2014).

Devil’s excrement

The weak track record of most resource-rich countries’ use of natural resource revenue supports the view that new discoveries could be as much a curse as a blessing. Why does this happen?

A resource boom can cause a currency’s real exchange rate to appreciate, which reduces the competitiveness of the country’s exports and diverts resources toward sectors of the economy that don't engage in foreign trade – what is widely known as Dutch disease. Moreover, analysts have found that resource wealth is often associated with government corruption that undermines democratic accountability. These arguments are often used to suggest that natural wealth can become a “resource curse.” This idea was captured vividly by Juan Pablo Pérez Alfonso, Venezuela’s former minister of mines and hydrocarbons and cofounder of the Organization of the Petroleum Exporting Countries, who described petroleum as the “devil’s excrement” and warned of its potential to spawn waste, corruption, excessive consumption, and debt.

Many resource-rich countries lack both robust public finance management systems to ensure the transparency and efficiency of their budget process and the checks and balances in the decision-making process that are needed to ensure an effective use of resource wealth. Without them, they have struggled to follow the positive example of countries like Botswana, Chile, and Norway.

Building strong, stable institutions takes time. In the meantime, some scholars suggest, countries should distribute their resource revenues directly to the population, to boost economic growth and improve living standards (see “Spend or Send” in the December 2012 F&D).

Various arguments support this view, chiefly the claim that distribution prevents the government from misusing resource revenues and increasing its size. Some resource-rich countries arguably would welcome some form of direct distribution of revenue, but in others it could constrain the optimal provision of public goods. Moreover, even if the goal is to limit the size of the government by limiting access to resource revenue, alternatives such as reducing taxes are probably more efficient.

Another argument focuses on the impact of taxation on accountability (Sandbu, 2006). If resource revenues were distributed to the population and taxed to finance a portion of public goods, citizens would demand greater accountability in public spending programs. But this assumes that the gains from greater government accountability outweigh the efficiency losses associated with transferring revenues to the population and then taking some back. It also does not take into account that the transfer mechanism may be afflicted by the same institutional weaknesses and corruption as those of a typical resource-rich country.

How much and to whom

Direct distribution is a way to transfer some or all resource revenue to citizens to reduce the government’s discretionary authority over such resources and foster greater accountability. Discretionary authority and accountability are linked because citizens are less inclined to demand accountability if politicians can choose who is to receive resource revenues.

Views differ on how much of the revenues to distribute. One extreme calls for passing all natural resource revenues on to citizens, while more moderate proposals – Birdsall and Subramanian (2004) proposed for the case of Iraq distributing at least half – suggest returning only a portion of revenue or even just part of the investment income from a natural resource fund. The debate over how much to distribute centers around the economic consequences of such distribution, including the impact on work incentives, household savings, and overall macroeconomic stability.

As for who should receive resource revenues, distributing resources to all citizens has the appeal of eliminating political discretion over which groups should benefit. But universal transfers can have unintended consequences – such as encouraging families to have more children, which can be avoided by limiting transfers to adults. Some argue for pursuing social goals by targeting the poorest segments of the population or imposing conditions such as children’s school attendance. These laudable goals could help galvanize support for such mechanisms. They could, however, also lead to tension between reducing the coverage by targeting a particular segment of the population – particularly the poor, whose political voice is usually weaker – and increasing accountability. Moreover, the poor are not well equipped to handle income volatility, which these mechanisms would need to address.

Some argue for direct distribution outside the budget, which is subject to government corruption. This proposal would set aside resource revenue from the budgetary accounts and subject it to scrutiny, perhaps by an independent body rather than the parliament. Collection and distribution could even fall to an institution other than the national tax agency. Proponents of this idea contend that a separate mechanism to distribute resource revenues is more credible in the eyes of the population. But however achieved, direct distribution is not a recipe for eliminating corruption. It is naive to assume that a corrupt government would agree to direct distribution to deal with the problem. And there is no guarantee that the mechanism for distribution would not suffer from similar corruption.

Speaking from experience

Alaska has implemented the best known and perhaps most successful example of a direct distribution mechanism. But it is a conservative model with a relatively small dividend amounting to only 3 to 6 percent of Alaskans’ per capita income. Just a share of Alaska’s oil revenue goes into the fund, and only the investment income from this fund is distributed – subject to a cap of 5 percent of the fund’s total market value. The fund is managed by the Alaska Department of Revenue, and strong checks and balances within the budget make it in many ways a model of transparency. The case is widely viewed as a success, but one that was clearly achieved from a position of institutional strength and transparency, not as a solution to an institutional problem.

Given the limited number of direct distribution mechanisms worldwide, a look at related policies offers insight into what does and doesn’t work. It is always risky to make inferences from related policies, but the following cases provide some lessons:

-

Venezuela has established a series of social programs called misiones. One focuses on adult literacy and remedial high school classes for dropouts; another on universal primary health care; and yet others on the construction of new houses for the poor, retirement benefits for the poor, food at discounted prices, and scholarships for graduate studies. As highlighted by Rodrίguez, Morales, and Monaldi (2012), these programs are funded directly by the state oil company and are therefore run outside the budget. As such, they give increased discretionary authority to the government. Some studies suggest that these programs suffer from as much corruption and populist pressure as the budget itself – which calls into question whether direct mechanisms outside the budget circumvent corruption.

-

Experience with income support programs in advanced economies highlights the plausible negative impact of direct distribution transfers on the labor supply. These programs are meant to provide basic support to households that have little or no earnings. Some of this income support is then taxed away. Such programs have been criticized for providing insufficient incentives to low-income earners to work; earned income credit programs for which only workers are eligible are one alternative.

-

The conditional cash transfer programs now popular in many developing economies can also dampen the incentive to work. These programs seek to reduce poverty by providing support – in the form of a cash transfer – subject to certain conditions, such as enrolling children in school or receiving vaccinations. The objective is to break the cycle of poverty by helping the current generation while promoting investment in the future generation. Most studies have found that the impact on the labor supply is negligible if the transfer is small and the benefits are targeted to the poorest households. Programs with larger transfers and with broader coverage – including better-off segments of the population – reduce labor participation more.

-

Large energy subsidies in oil-rich countries are popular because the population expects to reap benefits from the abundance of oil resources. Pretax subsidies that allow firms and households to pay less than prevailing international prices are about 8½ percent of GDP in the Middle East and North Africa region. These generalized subsidies lead to inefficient resource allocation – which hurts growth – and disproportionately benefit those who are better off, which only worsens income inequality. Despite these drawbacks, the public supports subsidies because it sees no other way of benefiting from the abundance of natural resources.

-

Worker remittances – money sent home by people working abroad – place additional resources in the hands of the household sector, as do direct distribution mechanisms. Experience suggests that most remittances are used for current consumption, and their impact on long-term growth is inconclusive. This casts doubt on the claim that direct distribution does not exacerbate Dutch-disease effects because the private sector will save when it receives a windfall just as the government does.

Lessons learned

Several lessons emerge from the Alaskan experience and that of related policies.

First, the overall design of fiscal policies could include direct distribution mechanisms, starting small to limit the impact on the labor supply. Limiting the proportion of resources directly distributed would ensure enough is available to the government for the provision of critical public services, as well as to ameliorate the impact of Dutch disease – as stressed by Hjort (2006).

Second, direct distribution is just as subject to corruption as public programs, so it should not be established outside the budget.

And, finally, it is important to remember that direct distribution of resource revenues doesn’t safeguard the needs of future generations.

Before embarking on direct distribution of resource revenues, a country must prepare its fiscal framework by

-

determining the level of public revenue and spending necessary to ensure domestic macroeconomic stability and sustainable external balances;

-

adopting policies that mitigate the impact of volatile commodity prices on revenue;

-

accounting for uncertainty in the level of natural resource production and how much revenue the economy can absorb; and

-

saving resources for future generations.

Direct distribution does not obviate the need to address these issues head-on. Although some argue that shifting the burden of managing volatility to the private sector could lead to improved outcomes, there is little evidence to support such a claim. As noted earlier, evidence from remittance-receiving countries suggests that the bulk of the money received is used for consumption rather than saving. While public sector management of volatility in resource-rich countries has been far from stellar, an IMF study (2012) shows that it seems to have improved as these countries shifted from policies that reinforced changes in commodity prices between 1970 and 1999 to broadly neutral ones in the past decade.

Direct distribution can have a significant impact on income distribution. In Ghana, for example, resource revenues amount to about 5 percent of GDP. The poorest 10 percent of the population earns only 2 percent of GDP, so universal direct distribution would raise the income of that group by about 25 percent. But the distribution of resource revenues would reduce the budgetary resources available for the provision of public services, which could in turn have adverse consequences on income distribution.

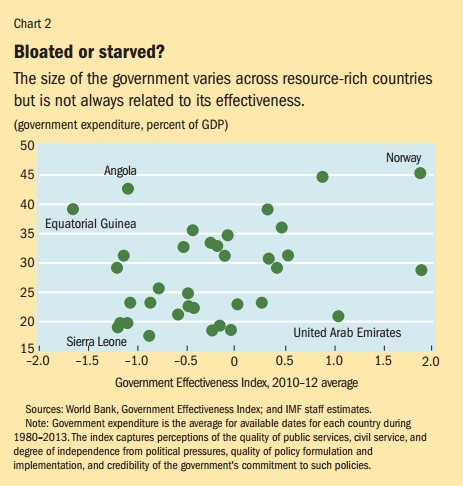

Another effect of direct distribution would undoubtedly be smaller government. Shifting resources to the private sector could curtail wasteful spending in some resource-rich countries but in others it could lower public spending to the point of threatening necessary infrastructure and public goods. Total  expenditure in resource-rich countries averages about 28 percent of GDP, which seems broadly in line with that in non-resource-rich economies. But there are significant differences in government size and institutional capacity across resource-rich countries (see Chart 2 - click to enlarge). The likely impact on income distribution and provision of public services only reinforces the need to start small when it comes to direct distribution.

expenditure in resource-rich countries averages about 28 percent of GDP, which seems broadly in line with that in non-resource-rich economies. But there are significant differences in government size and institutional capacity across resource-rich countries (see Chart 2 - click to enlarge). The likely impact on income distribution and provision of public services only reinforces the need to start small when it comes to direct distribution.

Worth pursuing?

While the view that direct distribution leads to increased accountability is appealing, large-scale direct distribution has not been tested anywhere in the world. There is little evidence that the extreme of distributing all resource revenues to the population is effective, but a case for modest direct distribution similar to the Alaskan model could be considered.

Even judicious distribution must be implemented under an appropriate fiscal framework and on a small scale to reduce the very plausible risk that distribution will stifle the provision of critical public services, lead to a drop in labor participation, or strain the government’s administrative capacity.

Sanjeev Gupta is a Deputy Director and Enrique Flores is a Senior Economist, both in the IMF’s Fiscal Affairs Department, and Alex Segura-Ubiergo is the IMF’s Resident Representative in Mozambique.

This article is published in Finance & Development, December 2014, Vol. 51, No. 4.

Related News

Azevêdo: Africa set to benefit from WTO breakthrough on Bali

Director-General Roberto Azevêdo, in his address to the African Union Conference of Ministers of Trade on 4 December in Addis Ababa, Ethiopia, said that African nations stand to benefit from the recent WTO decisions on the Bali agreements, including on the Trade Facilitation Agreement, which would support “your efforts at regional integration in a very practical way”. He urged African members to “engage even more” in the WTO.

This is what he said:

Good morning. I’m delighted to be here, and to have the opportunity to address you today.

I travel a lot as Director-General – pretty much all over the world in fact. But everywhere I go I get asked the same question.

People want to know about my view of the global economy – what the next big trend is going to be and where the opportunities will lie for trade and investment.

And I always give the same answer: Africa.

I talk about Africa’s dynamism – that it has the youngest population and the highest growth.

And I talk about the sense of energy and purpose that I find in every African leader or businessperson I meet.

Right now I think Africa’s potential is unmatched. And I think that trade has a crucial role to play in helping to realize this potential.

I know I’m not alone in this view.

It was notable that a recent survey of global public opinion found that it was not the people of Asia or North America who have the most positive view of trade – but the people of Africa.

And this is largely down to the leadership that ministers and policymakers – all of you – are showing on this issue.

You are taking huge strides forward in regional integration.

There is a lot of excellent work going on to lower barriers and streamline procedures so that you can trade with each other more effectively.

I have heard numerous examples of transit costs being halved, and transit times being reduced from days or weeks to just hours.

The African Union’s Action Plan for Boosting Intra-African Trade is very important here. And of course there is your work towards creating a Continental Free Trade Area.

This regional integration is totally compatible with the multilateral agenda – indeed I think this work will support wider integration into the global trading system.

The fact that intra-African trade remains just a tenth of Africa’s total trade shows that improving regional integration is critical. But it also shows that engaging at the global, multilateral level remains vital.

That’s why while you are pursuing these regional efforts, you are also making your voices heard more loudly than ever at the WTO.

The WTO gives you a seat at the global table, and I strongly welcome your engagement.

In fact, my message today is that you should seek to engage even more in the weeks to come. We are coming to a defining period in our work when it will be crucial that your voices are heard in full.

I will say more about this in a moment.

But first, I’m sure you are all aware that since July there has been an impasse in the implementation of the Bali Package which has had a paralyzing effect on negotiations across the board.

The impasse related to the political link between two issues – the Decision on Public Stockholding for Food Security Purposes, and the Trade Facilitation Agreement.

I’m pleased to say that last week – almost on the anniversary of the Bali conference – we resolved this impasse.

It was a major breakthrough for all of us.

WTO members came together in a Special General Council meeting and took three very important decisions.

First, they clarified the Bali Decision on Public Stockholding for Food Security Purposes to say that the peace clause agreed in Bali will remain in force until a permanent solution is found to that issue. This was a key issue for one member in particular.

I know food security is also a very important issue for many of you, and so I can assure you that this clarification does not substantively change what we agreed in Bali – nor does it compromise in any way the policy space that exists in the agreements today.

Second, members adopted the protocol of amendment which formally inserts the Trade Facilitation Agreement into the WTO rulebook.

This clears the path for the Trade Facilitation Agreement to be implemented and come into force.

Members will now go ahead and ratify the Agreement, following their domestic procedures.

It is estimated that the Agreement will reduce trade costs by up to 15% in developing countries.

This is particularly important for Africa where the cost of customs procedures tends to be higher – around 30% higher than the global average according to UNECA.

But, moreover, this Agreement is important for Africa because it supports your efforts at regional integration in a very practical way.

For the first time in the WTO’s history, this Agreement states that assistance and support should be provided to help developing countries achieve the capacity to implement it.

So, for those countries with less-developed customs infrastructure, the Agreement will mean a boost in the technical assistance that is available to them.

To ensure that this commitment is honoured, I worked with the coordinators of the Africa Group, the LDC Group and the Africa, Caribbean and Pacific Group at the WTO. We decided the best approach was to create a new initiative, to be called the Trade Facilitation Agreement Facility.

This Facility will ensure that LDCs and developing countries get the help they need to develop projects and access the necessary funds to improve their border procedures, with all the benefits that that can bring.

The Facility is already in place and it became operational when members took this decision last week.

And donors are already very interested and involved.

We have already received a great deal of support and interest – and we have built strong partnerships with a number of organisations in support of this work, including the World Bank.

So I urge you to look at how this Facility and the various other trade facilitation projects can support you.

Members took a third decision last week as well – which was arguably the most important of all. It concerns the WTO’s post-Bali work.

With this decision, members agreed that this work will resume immediately and that they will engage constructively on the implementation of all the Bali Ministerial Decisions.

This means taking forward:

-

the decisions on agriculture and cotton,

-

the monitoring mechanism, which originated from an Africa Group proposal, and

-

the LDC decisions on duty-free-quota-free, the services waiver and rules of origin.

It is vital that we use the momentum we have now to take these decisions forward with the priority they deserve.

Moreover, this decision means agreeing the work programme on the remaining DDA issues.

Under the decision taken last Thursday, all 160 WTO members committed to delivering the work programme by a new target date of July 2015.

I think this is an important moment – and a real opportunity.

The big, tough issues of agriculture, services and industrial goods will all be back on the table.

I urge you to engage fully in the discussions that will take place between now and July, to ensure that the outcomes reflect your concerns.

But I would also urge you to focus a critical eye on what is important for you now.

Focus on what is truly important – and what you think is doable.

We can achieve a great deal here, but if we over-reach then we will simply get stuck once again – and I think that is the worst-case scenario for developing countries.

So please, get engaged in the discussion.

I will be here to listen to you and support you in any appropriate way that I can.

These next few months will be critical.

We are also approaching an important moment in the Aid for Trade calendar.

The Fifth Global Review of Aid for Trade will be held at the WTO in Geneva from 30 June to 2 July 2015 – and I would like to extend an invitation to you all.

I will be using the event to bring together numerous key figures – heads of agencies, donors and regional development banks – to see what more we can do to support you to build your trading capacity and further the good work that is already being done.

So please come to Geneva and take part in that meeting.

This is also an important time for the Enhanced Integrated Framework for the LDCs – of which the WTO is a key partner.

The EIF is now up for evaluation and I have been arguing strongly for the initiative to continue into a new phase so that it can continue to assist LDCs to become more active players in the global trading system. And I hope you will also lend us your support here.

So, while there is a lot of work ahead of us, I think the WTO is going into the New Year with a lot of momentum.

The breakthrough last week put the WTO back in the game. It put our negotiations back on track.

But the decisions that members took were not an end in themselves. Rather, they were a means to allow us to pursue the greater ends of:

-

delivering the Trade Facilitation Agreement – and the vital support that goes with it,

-

taking the other Bali decisions forward,

-

and delivering the work programme to tackle the remaining issues of the DDA.

You are the leaders who can seize this opportunity – and realize the potential that I talked about at the start of my remarks.

So I look forward to your renewed and redoubled engagement in 2015.

I will be here to help you in any way I can.

Thank you.

Related News

India to press G20 for deadline to cut remittance costs: sources

India will press the Group of 20 economies to set a two-year deadline to reduce the cost of international money transfers, two government sources said, potentially saving more than $20 billion for developing countries.

The world’s largest recipient of remittances – of about $70 billion a year – won the backing of G20 leaders last month in Brisbane to take “strong practical measures” to cut the average cost of sending money home to 5 percent.

Despite that pledge, big banks are pulling out of handling remittances over rising compliance costs. In one case, 20 remittance firms sued Australia’s Westpac Banking Corp to stop it quitting the business.

“We will demand a deadline of two years at the next G20 meeting,” one of the sources, with direct knowledge of the matter, told Reuters.

The official is part of an Indian delegation that plans to attend a meeting of G20 deputy central bank governors in Istanbul on Dec. 11-12. Turkey has just taken over the annual presidency of the G20, an intergovernmental forum.

In 2011, G20 members agreed to bring down the global average cost of remittances to 5 percent by 2014, but that deadline has been missed.

The cost of remittances from G20 countries has fallen to 8.3 percent from 9.1 percent in 2011, the World Bank estimates. That has saved nearly $30 billion for migrant families since 2010, it said in a report to the G20.

Prime Minister Narendra Modi, who attended last month’s G20 summit, is pushing for Indians to save about $3 billion a year, partly helping bridge its current account deficit, the official said.

“The money belongs to poor families of developing countries and cannot be taken away in the name of transaction fees,” said another official.

Several Indian banks have brought down costs by up to 30 percent by offering services that allow Indian migrants in the United States and Britain to send money directly from their bank account or credit card to recipients in India.

Saudi Arabia has reduced remittance costs to near 3 percent, and India is hopeful that other G20 countries would agree to set a deadline to reduce the costs.

The government estimates that about 22 million Indians live abroad, with large communities in the Middle East, the United States and Britain.

Related News

Road to Dignity by 2030: UN chief launches blueprint towards sustainable development

Calling for inclusive, agile and coordinated action to usher in an era of sustainable development for all, Secretary-General Ban Ki-moon on 4 December 2014 presented the United Nations General Assembly with an advance version of his so-called “synthesis report,” which will guide negotiations for a new global agenda centred on people and the planet, and underpinned by human rights.

“Next year, 2015, will herald an unprecedented opportunity to take far-reaching, long-overdue global action to secure our future well-being,” Mr. Ban said as he called on Member States to be “innovative, inclusive, agile, determined and coordinated” in negotiating the agenda that will succeed the landmark Millennium Development Goals (MDGs), the UN-backed effort to reduce extreme poverty and hunger, promote education, especially for girls, fight disease and protect the environment, all by 2015.

In an informal briefing to the 193-Member Assembly, the UN chief presented his synthesis report, The Road to Dignity by 2030: Ending Poverty, Transforming All Lives and Protecting the Planet, alongside the President of the General Assembly, Sam Kutesa who also addressed delegates, describing the process of intergovernmental negotiations that fed into the report’s compilation to set the stage for agreement on the new framework at a September 2015 summit and stressing the “historical responsibility” States faced to deliver a transformative agenda.

The synthesis report aims to support States’ discussions going forward, taking stock of the negotiations on the post-2015 agenda and reviewing lessons from pursuit of the MDGs. It stresses the need to “finish the job” – both to help people now and as a launch pad for the new agenda.

In the report’s conclusion, the Secretary-General issues a powerful charge to Member States, saying: “We are on the threshold of the most important year of development since the founding of the United Nations itself. We must give meaning to this Organization’s promise to ‘reaffirm faith in the dignity and worth of the human person’ and to take the world forward to a sustainable future… [We] have an historic opportunity and duty to act, boldly, vigorously and expeditiously, to turn reality into a life of dignity for all, leaving no one behind.”

Never before has so broad and inclusive a consultation been undertaken on development, Mr. Ban told the Assembly on 4 December, referring to the consultations that followed Rio+20 [the 2012 UN Conference on Sustainable Development], adding that his synthesis report “looks ahead, and discusses the contours of a universal and transformative agenda that places people and planet at the centre, is underpinned by human rights, and is supported by a global partnership.”

The coming months would see agreement on the final parameters of the post-2015 agenda and he stressed the need for inclusion of a compelling and principled narrative, based on human rights and dignity. Financing and other means of implementation would also be essential and he called for strong, inclusive public mechanisms for reporting, monitoring progress, learning lessons, and ensuring shared responsibility.

He also welcomed the outcome produced by the Open Working Group, saying its 17 proposed sustainable development goals and 169 associated targets clearly expressed an agenda aiming at ending poverty, achieving shared prosperity, protecting the planet and leaving no one behind.

Discussions of the Working Group had been inclusive and productive and he the Group’s proposal should form the basis of the new goals, as agreed by the General Assembly. The goals should be “focused and concise” to boost global awareness and country-level implementation, communicating clearly Member States’ ambition and vision.

The synthesis report presented dignity, people, prosperity, the planet, justice and partnerships as an integrated set of “essential elements” aimed at providing conceptual guidance during discussions of the goals and Mr. Ban stressed that none could be considered in isolation from the others and that each was an integral part of the whole.

“Implementation will be the litmus test of this agenda. It must be placed on a sound financial footing,” he said welcoming the work of the Intergovernmental Committee of Experts on Sustainable Development Financing and encouraging countries to scale up their efforts.

The Financing for Development Conference in Addis Ababa next year would play a major role in outlining the means for implementation, and he stressed the “key role” national Governments would play in raising domestic revenue to benefit the poorest and most vulnerable members of society.

Official development assistance (ODA) and international public funds, particularly for vulnerable countries, would also be vital to unlocking “the transformative power of trillions of dollars of private resources”, while private investment would be particularly important on projects related to the transition to low-carbon economies, improving access to water, renewable energy, agriculture, industry, infrastructure and transport.

Implementation would also rely on bridging the technology gap, creating a new framework for shared accountability, and providing reliable data, which he called the “lifeblood of sound decision-making.”

Stressing his commitment to ensuring the best outcome from the post-2015 process, he underlined the need for States to be guided by universal human rights and international norms, while remaining responsive to different needs and contexts in different countries.

“We must embrace the possibilities and opportunities of the task at hand,” he said.

In an earlier interview with the UN News Centre Amina J. Mohammed, the Secretary-General’s Special Adviser on Post-2015 Development Planning stressed that one of the report’s main “takeaways” is that “by 2030 we can end poverty, we can transform lives and we can find ways to protect the planet while doing that.”

“I think that’s important because we’re talking about a universal agenda where we’re going to leave no one behind. It’s not doing things by halves or by three-quarters, it’s about everyone mattering… To say you don’t want to leave anyone behind is to look to see who is the most vulnerable and smallest member of the family and what is it that we’re going to have to do to ensure that they’re not left behind, because that will be the litmus test and success of what we do.”

Related News

Xi hails ‘China’s good friend’ Zuma

Chinese President Xi Jinping on Thursday hailed visiting South African President Jacob Zuma as China’s “good friend”, months after the latter’s government refused the Dalai Lama a visa.

“President Zuma is the Chinese people’s old friend and good friend,” Xi said as he welcomed Zuma on a state visit as trade and political ties between Pretoria and Beijing grow closer.

“South Africa is the comprehensive and strategic partner of China in Africa,” said Xi, who visited South Africa in March 2013 as part of his first foreign trip as head of state.

“We are good friends and good brothers that mutually benefit each other.”

Zuma, who is accompanied by a high-profile delegation including ministers for the environment, international relations, trade and energy, transport and finance, responded by thanking Xi for his “warm hospitality” since arriving.

“For me, this is a manifestation of the friendship and solidarity that exists between the People’s Republic of China and the Republic of South Africa,” Zuma said.

China is South Africa’s single largest trading partner, while South Africa is China’s largest trading partner on the continent.

South Africa joined the BRICS bloc of developing economies with Brazil, Russia, India and China in 2011.

During the apartheid era, Zuma’s African National Congress was supported by Moscow while Beijing backed the rival Pan Africanist Congress, but in recent years South Africa has maintained a strongly pro-China foreign policy.

In the last five years Pretoria has thrice declined a visa for the Dalai Lama, the exiled Tibetan spiritual leader and Nobel Peace Prize winner.

Dozens of Nobel laureates boycotted a September meeting in Cape Town following the latest refusal, which was widely regarded as a sign of South Africa’s deference to Beijing.

Fellow laureate and anti-apartheid activist Desmond Tutu also slammed the government over the visa refusal. The meeting was forced to moved to Rome.

During Zuma’s visit, China announced the signing of a series of agreements, including a memorandum of understanding on nuclear energy cooperation between China National Nuclear Corporation and the South African Nuclear Energy Corporation.

China said that the two sides agreed a five-to-10 year strategic programme on cooperation, as well as to improve bilateral cooperation in trade and investment between China’s ministry of commerce and South Africa’s department of trade and industry.

Detailed terms of the agreements were not immediately available.

South Africa said last month it had signed a nuclear energy cooperation agreement with China, calling the deal a “preparatory phase for a possible utilisation of Chinese nuclear technology”. The deal followed similar agreements with Russia and France.

South Africa, which has one nuclear plant, is plagued by electricity blackouts and is seeking to reduce its heavy reliance on coal-fired power stations.

Electricity constraints have been blamed for limiting economic growth and productivity.

Zuma earlier held talks with Chinese Premier Li Keqiang, with Li congratulating Zuma on his re-election in May as South Africa’s president.

“You have always attached high importance to South Africa’s relations with China and you have made unrelenting efforts to grow China-South Africa relations,” Li said.

“We have always appreciated our interaction between China and South Africa. I must say that we feel very much at home,” Zuma responded.

» Read more: South Africa signs agreements of cooperation with China

Related News

“Moving from business by necessity to entrepreneurship by choice” – The African Union Commission supports women in agribusiness

The African Union Commission is implementing a project to empower women through agricultural entrepreneurship. The project, supported by the UNDP, and implemented by UN Women through the African Centre for Transformative and Inclusive Leadership (ACTIL) – a joint programme of UN Women Eastern and Southern Africa Regional Office (ESARO) and Kenyatta University – involves a series of transformational leadership training workshops for Women in agribusiness.

Women farmers are the pillars of agriculture and food security in Africa. While millions of women in sub-Saharan Africa contribute to their national agricultural output, family food security, and environmental sustainability – as producers, resource managers, sellers, processors and buyers of food – they are still marginalized in agricultural marketing and business systems. Women in agriculture face unique challenges compared to their male counterparts: they operate smaller farms; keep fewer livestock. Women also have less access to agricultural and business information and extension services, and to credit and other financial services. They are less likely to use inputs such as fertilizers, improved seeds and mechanical equipment, and often have little influence within agricultural value chains.

In spite of the challenges there are many women that are breaking through the barriers and establishing themselves in agribusiness, as producers, processors, marketers and exporters. The African Union Commission is focusing on such women. The training aims to enhance women’s productivity, benefits from, and leadership role in agribusiness. The transformational leadership approach espoused by UN Women (ESARO) and ACTIL motivates women in agribusiness to understand the players and dynamics in their respective value chains, and to position themselves not only to seize opportunities for maximizing profits but also to mobilise other women and youth in the sector for greater impact.

This initial phase of the project benefits women and youth from Benin, Burkina Faso, Burundi, Cameroon, Cote d’Ivoire, DRC, Ghana, Kenya, Niger, Nigeria, and Uganda. The training is organized in three sessions: two sessions in English in Nairobi, Kenya, at the Africa Centre for Transformative and Inclusive Leadership (ACTIL) and one session in French at the Songhai Centre in Porto Novo, Benin. One hundred and thirty women will have benefited from the project by the end of December 2014.

Related News

Finance for climate action flowing globally

Finance for Climate Action Flowing Globally stood at $650 Billion annually in 2011-2012, and possibly higher

Hundreds of billions of dollars of climate finance may now be flowing across the globe annually according to a landmark assessment presented on 3 December 2014 to governments meeting in Lima, Peru at the UN Climate Convention meeting.

The assessment – which includes a summary and recommendations by the UNFCCC Standing Committee on Finance and a technical report by experts – is the first of assessment reports that puts together information and data on financial flows supporting emission reductions and adaptation within countries and via international support.

The assessment puts the lower range of global total climate finance flows at $340 billion a year for the period 2011-2012, with the upper end at $650 billion, and possibly higher.

-

Support from developed countries to developing countries amounted to between $35 and $50 billion annually, with multilateral development banks (MDBs), climate-related Official development Assistance (ODA) and other official flows (OOF) representing significant shares of resources channeled through public institutions

-

Funding through dedicated multilateral climate funds – including UNFCCC funds ($ 0,6 billion) – represented smaller shares during the same period, and do not include the recent pledges for the Green Climate Fund amounting to nearly $10 billion.

The assessment notes that the exact amounts of global totals could be higher due to the complexity of defining climate finance, the myriad of ways in which governments and organizations channel funding, and data gaps and limitations – particularly for adaptation and energy efficiency.

In addition, the assessment attributes different levels of confidence to different sub-flows, with data on global total climate flows being relatively uncertain, in part due to the fact that most data reflect finance commitments rather than disbursements, and the associated definitional issues.

The assessment is an important contribution of the Standing Committee on Finance that enhances transparency and clarity on climate finance flows – including information on international support to developing countries.

In addition, the assessment includes a set of recommendations by the Standing Committee on Finance to the Conference of the Parties, which, among other things, include ways to strengthen transparency and accuracy of information on climate finance flows through working towards a definition of climate finance and further efforts that would enable better measurement, reporting and verification.

The assessment also recognizes the need for understanding the impacts of climate finance associated with emissions reductions and activities to boost resilience to climate change.

The 2014 Biennial Assessment and Overview of Climate Finance Flows has been prepared by the Standing Committee on Finance following a mandate by the Conference of the Parties. The 2014 report was prepared with input from a wide range of experts and contributing organizations that collect data on climate finance flows.

Christiana Figueres, Executive Secretary of the UNFCCC, said: “Finance will be a crucial key for achieving the internationally-agreed goal of keeping a global temperature rise under 2 degrees C and sparing people and the planet from dangerous climate change”.

“Understanding how much is flowing from public and private sources, how much is leveraging further investments and how much is getting to vulnerable countries and communities including for adaptation is not easy, but vital for ensuring we are adequately financing a global transformation,” she said.

“I would like to thank the Standing Committee on Finance and the numerous experts and organizations who have contributed to this important assessment. It provides a baseline and a foundation upon which future assessments and more importantly future climate action can be refined and focused,” said Ms. Figueres.

“This first biennial assessment represents a milestone of the work of the Standing Committee on Finance. It is an important information tool for Parties to the Convention that provides a picture of climate finance flows and how they relate to climate actions, including the objectives of the Convention” said Standing Committee on Finance co-chairs Diann Black Layne and Stefan Schwager.

“Going forward, the Standing Committee on Finance will contribute further to improvements in the information on climate finance flows, including through collaborations with data collectors and aggregators,” they added.

More Facts and Figures from the 2014 Biennial Assessment and Overview of Climate Finance Flows Report:

-

Global total flows: Most climate finance in 2011/2012 is raised and spent at home – in developed countries 80 per cent of the funds deployed for climate action are raised domestically.

-

The same pattern is seen in developing countries where just over 71 per cent comes from national sources

-

Around 95 per cent of global total climate finance is spent on mitigation or cutting emissions with 5 per cent on adaptation.

-

Subsidies for oil and gas and investments in fossil fuel-fired generation are almost double the global finance for addressing climate change

-

Flows from developed to developing countries: Multiple sources were involved in providing funding to support climate action in developing countries ranging from Multilateral Development Banks (MDBs) and Overseas Development Assistance (ODA) to multilateral climate funds – including funds administered by the Operating Entities of the Financial Mechanism of the Convention and the Kyoto Protocol.

-

For example, finance from MDBs is around between $15 and $23 billion annually; multilateral climate funds including via the GEF were about $1.5 billion, including those linked to the UNFCCC at about $0.6 billion a year.

-

48 to 78 per cent of finance is reported as fast-start finance (2010-2012), in Biennial Reports (2011-2012), through multilateral climate funds, and through MDBs supports mitigation, or other/multiple objectives (6 to 41 per cent)

-

Adaptation finance in the same sources ranges from 11 per cent to 24 per cent.

Notes

The assessment has tried to identify the flows to various sectors and initiatives – real precision in this area will have to await future assessments and the numbers need to be treated with caution.

Assessing investments in adaptation is particularly difficult often because they can form part of a larger project such as an investment in a port of water supply system.

Meanwhile, there is also no universal operational definition of what constitutes adaptation and in addition publicly funded adaptation actions within countries – both developed and developing – is rarely reported or available.

As a result, flows from developed to developing countries are not really known with precision.

Related News

Watchdog gets nod to effect market studies

All recommendations made by the Competition Authority to streamline agriculture products markets must be implemented immediately, the President said Thursday.

Addressing delegates at the World Competition Day celebration, President Uhuru Kenyatta said this would boost wealth creation by farmers.

He told the Competition Authority to work closely with other government agencies in implementing the recommendations of market studies in tea, artificial insemination, seeds and sugar.

“Eradication of marketing distortions may reduce our poverty levels by a further 1.5 per cent. This is our key agenda and we have to achieve it,” he said in a speech read on his behalf by National Treasury Cabinet Secretary Henry Koskei.

FINANCIAL INCLUSION

The function was at Safari Park Hotel, Nairobi.

The President also told the Competition Authority to expedite the Product Market Regulatory Indicative Study, which it is conducting and have the findings discussed with stakeholders in February.

This will aid in modernising regulatory aspects and help in realisation of Vision 2030, he said.

The study covers telecommunications, transport, investment policy, retailing, banking, insurance and energy.

The President said the government had increased the authority’s budget to enable it conclude cases such as abuse of market dominance in telecommunications.

“These cases will go a long way in deepening financial inclusion, through easing access to mobile money transfer and also lead to consumer savings, as a result of increased competition,” he said.

He told county governments not to introduce regulations and restrictive conditions in issueing licences that could impede the proper functioning of demand and supply of products.

ACTION PLAN

The progress made so far

-

Competition Authority: We dealt with 88 merger applications by June, compared with 65 the previous year, says Director-General Wang’ombe Kariuki.

-

Also finalised 23 cases of restrictive trade practices, compared with 16; and 15 consumer cases compared with six in 2013.

-

World Bank: An impact assessment supported by the global lender shows that the retailing trade restrictive case resulted in consumers saving about $1 million (Sh90 million), while money transfer rates fell by 67pc.

Related News

AfDB releases report on trade finance in Africa

Trade finance is essential for international trade. This financial intermediation helps firms to manage risks inherent in international transactions, improve their liquidity and enable them to optimally invest to enhance their growth.

It is for this reason that, in 2013, the Board of the African Development Bank (AfDB) approved a US $1-billion trade finance (TF) program to support African trade and provide financing to underserved African-based financial institutions and enterprises. Despite its importance, there is a great deal we do not know about the trade finance market in Africa. This includes the size of the market, the variations across sub-regions, the scale of financing gap, the trade finance devoted to intra-African trade, the relative importance of on-balance sheet versus off-balance sheet financing, and constraints faced by banks.

The report Trade Finance in Africa seeks to fill the above information gap. It is based on a unique survey of the trade finance activities performed by commercial banks in Africa in 2011 and 2012. Our survey questionnaire was sent to approximately 900 banks on the continent. We received a high response rate, resulting in a dataset that covers 276 banks across 45 countries. All the sub-regions on the continent are represented in the survey.

We found that the size of bank-intermediated trade finance is approximately US $330 billion to US $350 billion and approximately 93% of banks have trade finance assets. This is roughly equal to one-third of total African trade. The market is not uniformly distributed across sub-regions as the average trade finance assets per bank in Northern Africa dwarfs those of the other sub-regions. The share of bank-intermediated trade finance that is devoted to intra-African trade is limited, and comprises approximately 18% (US $68 billion) of the total trade finance assets of African banks.

It should be noted, however, that the share of intra-African trade accounts for 11% (US $110 billion) of the value of total African trade. Given the estimated rejection rates of trade finance applications reported in the survey, the conservative estimate for the value of unmet demand for bank-intermediated trade finance is US $110 billion to US $120 billion, significantly higher than estimated earlier figures of about US $25 billion. These figures suggest that the market is significantly underserved.

African banks face numerous constraints in meeting the demand for trade finance. The survey reveals that the main constraints are limited US dollar availability (by far the dominant currency in international trade, and by extension, trade finance) and insufficient limits with confirming banks for confirming letters of credit. Other constraints include small balance sheets, which tends to make single obligor limits frequently binding. These constraints also suggest that the AfDB’s trade finance program, as well as those implemented by other international financial institutions, are needed and well suited to relaxing some of the most binding constraints.

Finally, the survey shows that the outlook of banks for trade finance remains positive, with 72% expecting to increase their trade finance activities in the immediate future. However, banks foresee obstacles to their trade finance portfolio growth such as low US dollar liquidity, regulation compliance, slow economic growth in some markets, and the inability to assess the credit-worthiness of potential borrowers.

Infographics

Related News

Trade Experts in Addis to discuss the launch of the Continental Free Trade Area

The three-day Senior Officials Meeting of the 9th Ordinary Session of the African Union Conference of Ministers of Trade (CAMOT-9) opened on Monday 1st December at the African Union Headquarters in Addis Ababa, Ethiopia. The Senior Officials session is taking place to prepare for the Ministerial session which will be held on 4th and 5th December, of which will discuss, among other things; global trade and Mega Regional Trade Agreements, Declarations on WTO EPAs, AGOA and investment trends, their implications within the context of Africa’s commitment to forge ahead its integration notably towards the launch of the Continental Free Trade Area (CFTA) negotiations in 2015.

The African Union Conference of Ministers of Trade is meeting this year at a point where the Economic Report for Africa 2014 mentions that the industrialization is a “precondition for Africa to achieve inclusive and sustainable economic growth.” The report also highlights that in the past decade the contribution of manufacturing and industry to aggregate output and GDP growth has either stagnated or declined for most countries, while, the agriculture sector, which employs up to 60 per cent of the African labour force, is characterized by limited value addition, as forward linkages to industry and service sectors are weak.

In her opening statement, the AUC Director for Trade and Industry, Mrs. Treasure Maphanga, reminded the experts that as Africa meets to discuss the advancement of its regional integration agenda, the world is moving, mentioning examples of the Trans-Atlantic Trade and Investment Partnership (TTIP), a trade and Investment agreement that is presently being negotiated between the European Union and the United States, the Trans-pacific Partnership negotiations between the US and Pacific Countries, as well as the FTA which in being negotiated between China, Japan, and South Korea.

Mrs. Maphanga hence stressed that CFTA is an important opportunity to develop and harmonize regulations in a number of trade-related services sectors that will backstop the industrialization process. “As you consider the draft texts for the CFTA negotiations, we wish to remind all of us that the continent is looking for greater ambition than the Tripartite Negotiations. We are seeking to develop an agreement that enables deep integration amongst all African economies, with a focus on Boosting Intra-African Trade and implementing the Action Plan that includes Trade-related Infrastructure, Productive capacity and Trade facilitation”, suggested Mrs. Maphanga.

In his remarks on behalf of Dr. Carlos Lopes, United Nations Under-Secretary General and Executive Secretary of the Economic Commission for Africa (UNECA), Dr. Stephen Karingi, Director, Regional Integration and Trade Division, noted the robust economic growth experienced by Africa over the last decade and driven by high commodity prices had little impact on poverty eradication and had not altered economic structures.

Hence, he said, it is clear that if business as usual persists, Africa is likely to continue seeing growth that will not impact on widespread poverty levels and economic structures will likely remain the same, and that Africa’s transformation will be still born, and the risk of being caught up in the middle income trap will become real. “Therefore, as we meet here, it is my hope that our discussions will be informed by the big picture of sustainability and structural transformation of our economies,” said Dr. Karingi.

The Establishment of the Continental Free Trade Area (CFTA) was decided in the 18th Ordinary Session of the Assembly of Heads of State and Government of the African Union which was held in Addis Ababa, Ethiopia in January 2012, which will bring together fifty-four African countries with a combined population of more than one billion people and a combined gross domestic product of more than US $ 1, 2 trillion dollars.

Statements

» Statement by H.E. Mrs Fatima Haram Acyl - AU Commissioner for Trade and Industry

» Statement by Abdalla Hamdok Deputy Executive Secretary UN Economic Commission for Africa

» Speech delivered by ITC Executive Director Arancha González

Related News

Fighting climate change and poverty at the same time

Worldwide, close to 1 billion people live in poverty on less than $1.25 per day and more than 800 million are undernourished. Many of them are on the front lines of climate change. Extreme weather and droughts can put their food and water supplies at risk, raise prices, and destroy homes and businesses that are often built at the edges of livable land. They have little resilience to the volatility or economic havoc climate change can bring.

More shocks can also pull those just above the poverty line under, threatening to reverse decades of progress toward eradicating extreme poverty. At the World Bank Group, we are working on ways to address both climate change and poverty at the same time.

As climate negotiators gather in Lima for the latest round of UN climate talks, the impact on poverty should run throughout the discussions of risks and solutions.

“We’re only beginning to see the clear impacts of climate change. As these impacts deepen, the poor will have less means to cope. Climate change will put at risk the international community’s goal of ending poverty,” said World Bank Group Vice President and Special Envoy for Climate Change Rachel Kyte.

“To protect the poor, we must invest in resilience, including social protection measures, access to insurance, natural resources restoration – everything that will help them bounce back better when shocks come,” Kyte said.

That combination of climate action and social protection is important and urgent. The recent Turn Down the Heat report warns that the world will see the effects of temperatures about 1.5°C above pre-industrial times even with concerted action to lower emissions, and much worse if emissions continue unabated, making poverty even harder to escape. Even 1.5°C of warming will bring more severe droughts and sea level rise that can flood low-lying areas and contaminate coastal cropland.

Protecting the Poor and the Planet

Policies for mitigating and adapting to climate change must be designed to protect the poor. That is why the World Bank works with client countries to analyze the impacts of climate change risks and responses on poverty.

Research underway this year and next is finding that climate-related policies paired with social policies can both reduce poverty and modernize economies that were once carbon-intensive.

British Columbia, for example, has shown how revenue from a carbon tax can provide targeted support for the poor while also reducing business and income taxes. The Canadian province created a low-income climate action tax credit that provides quarterly payments to the poor to offset higher prices. Today, British Columbia has one of the lowest income taxes in the country, a thriving economy fueled in part by green growth, and its emissions have fallen.

Similarly, governments can reduce harmful fossil fuel subsidies and use the savings to create targeted support for the poor who most need assistance when fuel prices rise. Studies have found that fossil fuel subsidies tend to be inefficient and regressive: The wealthiest 20 percent of households in low- and middle-income countries receive about six times more of the benefit than the poorest 20 percent. Building in new sources of support for the poor – such as energy credits, reduced public transit fares, or cash transfers – while phasing out harmful subsidies can provide the intended support more efficiently.

Building resilience also helps poor communities deal with the effects of climate change. Better land-use planning and improved infrastructure, for example, can reduce vulnerability to future climate change. When Hurricane Tomas hit St. Lucia in 2010, the damage cost the island nation 43 percent of GDP. The World Bank has helped St. Lucia improve data sharing to build back better, reduce future losses, and improve its disaster preparedness and capacity to respond.

Eliminating poverty and keeping it at bay as we deal with climate change requires wider use of what we already know works: well-funded social protection programs that can easily be scaled up in the event of a disaster; the data and capacity to identify the transient poor and provide them with support; and financial inclusion that allows the poor to save and borrow so they can bounce back more quickly from shocks. Access to health care and education are also important for recovering from shocks and getting out of poverty.

Opportunities in Climate Action

At the UN Framework Convention on Climate Change Conference of Parties in Lima, we will be talking about these and other policy options.

Our research has found that with smart policies and careful urban planning, the same development work needed to accommodate a growing population today, such as clean and accessible transportation systems and energy efficient buildings, can help mitigate climate change, increase resilience to its effects, and increase opportunities for the poor through new jobs and greater access to work, health care, and education.

Climate action can create new income opportunities. Many ecosystem-based adaptation and mitigation measures require labor-intensive activities, such as reforestation and land restoration. Policies that encourage green industries also create new opportunities through retraining and diversification of economic activity and trade patterns. Inclusiveness is a critical part of green growth and building livable cities.

Turn Down the Heat and the recent IPCC Fifth Assessment Report make clear that we must deal with climate now. Failing to do so will raise the costs and risks for everyone.

Related News

Beyond tariff walls: Non-tariff hurdles in sub-Saharan Africa

It is often said that international trade is no longer a game of tariffs but rather a game of quality, standards, and compliance with the requirements of the global market. Exporters, more specifically those from developing countries, feel this the most as they struggle with what is known as non-tariff measures (NTMs) in their daily quest for international competitiveness.

NTMs are officially defined as “policy measures on export and import, other than ordinary customs tariffs, that can potentially have an effect on international trade in goods. They are mandatory requirements, rules or regulations legally set by the government of the exporting, importing or transit country”. NTMs become an obstacle to trade for exporters and importers when they are perceived to be “burdensome” by the latter. Since 2010, the International Trade Centre (ITC) has been working with the private sector from developing countries, collecting information on the various obstacles to trade faced by the business community in these countries. This project was initiated in order to increase transparency about NTMs by disseminating relevant information and by analysing the non-tariff obstacles to trade. The ultimate goal is to reduce or eliminate those barriers, thus improving the business environment. In sub-Saharan Africa (SSA), the ITC NTM Surveys have already been conducted in Burkina Faso, Côte D’Ivoire, Guinea, Kenya, Madagascar, Malawi, Mauritius, Senegal, Rwanda, and Tanzania.

Beneficiary countries are already using the findings of the ITC NTM Surveys to remove impediments to trade. To mention but a few: In 2013, Mauritian customs authorities eliminated the need for imports of rooibos tea to be cleared by the Tea Board; the Senegalese export promotion agency is considering the NTM Survey findings and recommendations in its export development strategic plan for 2014-2017; and similarly the government of Madagascar intends to integrate some of the findings into its trade policy and trade negotiations. The ITC NTM Surveys are also extensively used to inform the work of other development partners, such as in the framework of diagnostic trade integration studies, for example in Malawi.

Which are the most burdensome NTMs for African exporters?

The results of the surveys done in the ten SSA countries show that the top three NTMs identified by exporters as most burdensome are conformity assessments, technical requirements as well as rules of origin and the related certificates of origin. Other identified barriers include pre-shipment inspections and further entry formalities, charges, taxes and other para-tariff measures, including licensing or permits to export. Overall, 64 percent of the interviewed companies in SSA were reported being affected by NTMs. The figure of 64 percent found in SSA is above the average (50 percent) obtained from the total number of countries surveyed by the ITC so far. This would imply therefore that exporters and importers in this region seem to be more affected by burdensome NTMs.

In the agricultural sector, “technical requirements”, which include sanitary and phytosanitary measures (SPS) implemented to protect human, animal and plant life (e.g. requirements such as tolerance limits for residues and measures for labelling and packaging), and “conformity assessments” are perceived as the most challenging by SSA exporters. Conformity assessments refer to control, inspection and approval procedures (such as testing) which confirm that a product fulfils the technical requirements and mandatory standards imposed by the importing country. These two categories are known as SPS measures and Technical Barriers to Trade (TBT) in the NTM classification. They are inevitable for most agricultural products since they are put in place to meet public policy objectives, such as consumer protection. These product-specific, legally binding requirements are challenging predominantly in developed markets like the EU. Exporters usually complain that such regulations are particularly burdensome in their implementation process because of associated delays and high fees.

This result comes as no surprise, as the globally most widespread NTMs relate to technical factors like SPS measures. Most developed nations have strict quality and food safety standards and are increasingly introducing stringent food safety regulations. The EU, for instance, has a whole raft of regulations that require exporters from outside the EU to meet the same standards as EU members when it comes to foodstuffs. Moreover, new rules are increasingly being introduced, for example for labelling. The United States, through its own Food Safety Modernization Act (FSMA), also places extensive requirements on imports.

With TBTs increasing globally, they leave SSA exporters (including those concerned with conformity assessments) vulnerable especially due to the lack of the necessary infrastructure in their respective home countries. Furthermore, delays experienced with the home administration (e.g. at customs) have dire consequences for exports, particularly of perishable agricultural products (e.g. fresh food).

As far as manufacturing exports are concerned, technical requirements are often less important than in the agricultural sector. However, challenges from conformity assessment still stand out at 44 percent and concerns about rules of origin, i.e. the criteria used by importing countries to assess whether a product is eligible for preferential treatment, are also quite pronounced (17 percent of total NTMs reported for SSA countries). For instance, burdensome NTMs related to rules of origin were commonly reported by exporters in Côte d’Ivoire.

Who applies NTMS?

The ITC NTM Surveys suggest that, among the challenging NTMs reported by exporting companies, on average around 70 percent are applied by the partner countries and 30 percent happen at home. Comparatively, in SSA, nearly 40 percent of NTMs are reported to be applied by the home country, while about 60 percent are reported to be applied by partner countries. Therefore, if SSA countries want to boost their competiveness and establish themselves on the main stage of international trade, their national and local authorities need to address the obstacles to trade linked to NTMs occurring at home, although it is also clear that domestic efforts need to be complemented with a continued engagement with international trading partners.

The findings also show that many burdensome NTM cases are associated with partner countries with which SSA countries already have free trade agreements (FTAs) or regional trade agreements (RTAs). For example, in Guinea there were reports about customs surcharges (e.g. surtax or additional duty) imposed by Mali and Côte d’Ivoire, all of whom are members of the Economic Community of West African States (ECOWAS). 64 percent of NTM reports from Guinea concern neighbouring ECOWAS countries. We see similar results for other regions: In Tanzania, for example, an overwhelming majority (64.4 percent) of the reported cases of NTMs are applied by partners from within regional frameworks, i.e. the East African Community (32.9 percent), followed by the Southern African Development Community (31.5 percent). This indicates that there is still room for the elimination of non-tariff barriers by RTA/FTA counterparts. Tackling these obstacles could help achieve better trade integration among SSA countries.

The way forward

Problems linked with NTMs are often exacerbated for landlocked countries (such as Rwanda), where obstacles associated with transit countries are particularly severe, including in terms of weighbridge charges and delays before goods can be delivered. One significant intervention to consider is to establish a results-oriented dialogue and negotiation with regional partners or bilaterally with neighbours.

In addition to government requirements, SSA exporters sometimes face onerous standards imposed by private clients. For example, the Rwandans particularly reported Fair Trade certificates demanded by clients in the European Union, especially for Rwanda’s important coffee and tea products. The costs and delays associated with these certificates are said to cause serious hindrances for exporters.

Taken together, SSA exporters and importers report a large amount of NTMs faced in their efforts to engage in the global trading system. There seems to be consensus that technical measures, conformity assessments, different charges, rules of origin and customs procedures are among some of the most burdensome restrictions traders encounter. Hence, a number of initiatives are being launched to address these measures both internationally and domestically, but more work is needed to alleviate such constraints. For instance, there is scope for improved engagement between policy makers and their exporters and importers. Better dialogue between the different stakeholders from both private and public sectors can prepare the ground to develop effective and sustainable policies to remedy some of the concerns, as well as to clarify those instances where lack of awareness may be also one of the obstacles. Traders from a number of SSA countries indicated their desire for a one-stop shop or single window to process documentation. Others highlighted the need for a single enquiry point to obtain all the necessary documents required in destination and home markets to qualify for certifications.

Tackling such obstacles could help SSA countries take giant leaps towards improving their trade environment.

The debate surrounding NTMs is ongoing and numerous questions about their legitimacy are being raised. Even though it is generally accepted that NTMs may have the best policy intentions in terms of public health, their frequency and complexity negatively affect the trade flows of more vulnerable countries, such as those from the SSA region. Furthermore, they are sometimes perceived as protectionist measures used by governments. Regardless of their underlying motives, NTMs actually impose costs that have negative impacts on trade competitiveness, particularly for small and medium-sized enterprises (SMEs) in emerging and developing countries. Often NTMs themselves are not barriers per se, but the procedural obstacles associated with them have negative consequences for trade. The problems found impacting industries in SSA take an even more burdensome toll on trade and are more surprising at a time when individual governments and the international community are mobilizing all efforts to alleviate poverty and promote engines of growth.

Poonam Mohun is NTM Project Market Analyst, Market Analysis and Research, International Trade Centre. The views expressed herein are those of the author and do not necessarily reflect the views of the International Trade Centre or of the United Nations.

This article is published under Bridges Africa, Volume 3 - Number 10.

Related News

Governors of Central Banks appreciate regional growth

Governors of Central Banks in COMESA Member States have appreciated the 6.6% average growth performance of the region and emphasized that such growth should be sustained and be inclusive.

In their 20th Meeting that ended Thursday 27th November 2014 in Kinshasa, Congo (DR) the Governors emphasized the importance of policies that stimulate demand and trade within the region.

According to a report of the meeting sent by the Director of COMESA Monetary Institute (CMI) Mr. Ibrahim Zeidy the Governors underscored the importance of laying a solid foundation in the medium term for a fully-fledged inflation targeting framework, in order to make the region a zone of macroeconomic stability.

“Volatility in exchange rates tend to impact on trade and subsequently on output, inflation, FDI and the investment climate in general,” they noted.

In his address to the meeting Secretary General of COMESA, Mr. Sindiso Ngwenya, underlined the need for speedy implementation of Regional Payment and Settlement System (REPSS).

“I want to urge all member Central Banks to expeditiously use REPSS for payment for their intra-COMESA transactions as it will significantly contribute to the expansion of intra COMESA trade,” he said.

His address covered strategic issues of the COMESA integration agenda including the removal of tariff and non-tariff barriers, progress report on COMESA FTA, progress report on Tripartite Arrangement, trade promotion and facilitation, strategies to move to high value addition to export products, COMESA industrial policy and COMESA activities related to extractive industries.

Mr Ngwenya emphasized the importance of member countries to get a greater share of resource rents from extractive industries and underscored the COMESA Monetary Cooperation programme that would make trade and investment easy and inexpensive.

He therefore emphasized that member countries should intensify the process of macroeconomic convergence and intermediation in the region.

The Committee of Governors of Central Banks also reviewed the activities that were undertaken by the COMESA Monetary Institute (CMI) and COMESA Clearing House (CCH) for enhancing monetary cooperation in the region and making the region a zone of macroeconomic and financial stability.

These activities included the outcome of workshops, trainings and research activities which were undertaken by CMI and activities undertaken by CCH for the operationalization of the Regional Payment and Settlement System (REPSS).

They also deliberated on challenges in the disbursement of loans by commercial banks in the region. They agreed that an Action Plan proposed by the Central Bank of Congo should be used as inputs into the existing COMESA Financial System Development and Stability Plan which was adopted by the COMESA Committee of Governors of Central Banks in 2009.

Related News

TTIP: What are the implications for emerging powers and the international order?