All News

Sudan agrees to undertake tough reforms to improve trade sector and boost economy

Sudan policy makers met to discuss and finalize key policy actions to help tackle critical trade challenges holding the country’s economy back, including increasing trade capacity and diversification of exports. The policy actions were drawn from the World Bank’s latest draft Diagnostic Trade Integration Study (DTIS) Update.

Despite implementing several critical and difficult reforms to help restore macroeconomic balances and improve the business enabling environment during the last two years, Sudan is still experiencing a large deficit that is being met by short term borrowing. Apart from addressing the economic imbalances, the country also needs to ensure proper alignment of its exchange rate in order to pave the way for building competitiveness and increasing investments. This includes implementing a package of reforms aimed at lowering the barriers to trade through reduced trade taxes, streamlined border and regulatory policies, and improved transport and logistics.

The current onerous regulatory polices hinder competition and increase trade costs, while policies which protect the domestic agriculture market undermines production for regional and export markets.

Over 100 representatives from the government, private sector, and donor community attended the two-day workshop to discuss the proposed actions and recommendations from the draft DTIS Update. The workshop is part of the Integrated Framework initiative, which is sponsored by the World Bank Group, the IMF, UNDP, WTO, UNCTAD, and the ITC, and was facilitated by the World Bank.

“The role of this report is to raise the profile of the key reforms – facilitating trade in agriculture, reducing non-tariff barriers, modernizing customs and logistics, and raising the profile of services. These reforms are critical to Sudan’s efforts to diversify its economy, an objective where the World Bank stands ready to provide technical advice and assistance,” said Xavier Furtado, the World Bank Group’s Country Representative in Sudan.

The key message of the report is that lowering trade costs is essential for Sudan to diversify the economy through more varied agriculture exports and through higher value activities, such as processed agricultural foods and light manufacturing.

“The workshop discussed and prioritized the Action Matrix that will be implemented by the EIF (Enhanced Integrated Framework) in collaboration with donors,” said Mrs. Margam Elemam Mohi Eldin Eleman, Undersecretary in the Ministry of Trade and EIF Focal Point for Sudan. “The interest of workshop participants’ in the implementation of the streamlined Action Matrix will be crucial for successful implementation,” she added. She also noted that participants agreed that comments raised by government and stakeholders will be addressed in the final report.

According to Michael Geiger, World Bank Senior Economist and task leader of the report, the DTIS Update will take into account the input from the workshop and be finalized in October 2014.

Related News

Inequality clouds growing economy

Angola needs to diversify its oil economy

Angola has one of the world’s fastest growing economies. Its economy grew by 5.1% in 2013. As major public infrastructure investments in energy and transport kick in, its growth is projected to reach 7.9% in 2014 and 8.8% in 2015. Yet, the United Nations Development Programme (UNDP) reports that around 36% of Angolans live below the poverty line and one in every four persons is unemployed.

According to the International Monetary Fund (IMF), Angola is a “post-conflict country that produces a lot of oil and faces the challenges of both.” Despite being the fifth largest economy in Africa, ordinary Angolans have seen little change in their standard of living. Only 37.8% of country’s 21 million people have access to electricity. While about half of the population has access to safe drinking water, this number falls to 34% in rural areas, says the World Bank. There are few jobs for the unemployed, mostly under 25 years, who make up 60% of the population. What should Angola do to change the current situation? Experts say the solution is for Angola to diversify its economy, save and invest for the future – especially in skills and infrastructure development – and improve governance.

A need for diversification

Angola is Africa’s second biggest oil producer after Nigeria. Its oil comes almost entirely from offshore fields, off the coast of Cabinda and from deep-water fields in the Lower Congo basin, in addition to small-scale production from onshore fields. Last year, according to the US Energy Information Administration, an agency that provides statistics and analyses on energy, Angola produced 1.85 million barrels of petroleum per day, and oil revenues could top $60 billion this year, notes the African Economic Outlook, a report produced jointly by the African Development Bank, the Organization for Economic Co-operation and Development, UNDP and the UN Economic Commission for Africa. But as with other oil-producing countries in Africa, oil has not proved to be a benefit to Angolans. If anything, say analysts, it has produced few jobs and increased inequality and allegations of corruption.

Angola’s mineral product exports as a share of total exports are more than 95%, according to data from the World Bank and the Organization of the Petroleum Exporting Countries (OPEC). Oil production and its supporting activities contribute about 45% to the nation’s gross domestic product (GDP) and 80% to government revenues. With little diversification, the Angolan economy has limited investment and job opportunities, and generates growth only for a small group of elites, economists say. In fact, in terms of the composition of its exports, Angola is the world’s second most concentrated economy after Iraq, says UNDP.

The World Bank has identified three problems facing the Angolan economy: high dependence on oil revenue, making the country vulnerable to oil price volatility; an economic system that is prone to corruption; and the absence of a diversified job market. The British magazine, The Economist, reported last April that Angola was “still much too oily,” because oil provides few jobs, especially good jobs, and according to the government’s own admission, there has been a “failure to develop the non-oil economy.” In fact, the oil industry employs just 1% of Angolan workers, which is a factor in the 26% unemployment rate.

The Center for Scientific Studies and Research (CEIC) at the Catholic University of Angola, by contrast, sees the oil-dominated economy expanding substantially since independence, particularly since the end of the civil war in 2002. While conceding that diversification was largely absent from government policy until 2011, the CEIC says that other sectors are now contributing to the GDP, though not substantially.

All that glitters

In addition to oil, Angola exports diamonds. It is Africa’s second largest source of rough diamonds after Botswana and the fourth in the world. The main reserves are concentrated in the north-eastern region. Diamond production generates over $650 million annually, although exact numbers are uncertain due to illegal diamond mining and smuggling.

But the diamond industry is often alleged to be involved in human rights abuses, such as forced overtime without adequate compensation and creating environmental degradation through mining activities. Rafael Marques de Morais, an Angolan journalist, human rights activist and anti-corruption campaigner, recently filed a criminal complaint against two diamond mining companies and their directors, including top military officers. In response, authorities labelled him an “official suspect” and officials from some mining companies have accused him of defamation. Isabel dos Santos, the billionaire daughter of the Angolan president, is said to be one of the main beneficiaries of the diamond trade in Angola, according to an article this year in Forbes business magazine.

Agriculture is a lifeline

Besides oil, other contributors to GDP include non-oil energy, agriculture, fisheries, manufacturing and construction sectors. Angola has high quality soil and good water supplies, which potentially could make commercial farming a valuable industry, according to the African Development Bank (AfDB). Currently, agriculture accounts for only 11% of GDP but 70% of total employment.

In 2013, farm output grew by 8.6%, mostly through strong growth in cereal production, notes the African Economic Outlook. The National Cereals Institute of Angola says that the country requires 4.5 million tonnes of grain a year but only grows about 55% of the corn, 20% of the rice and just 5% of the wheat needed for local consumption. Higher government spending on agriculture could change that and make Angola self-sufficient, suggests the Food and Agriculture Organization, the UN body that mobilizes efforts to eradicate hunger and poverty. However, overall, Angola’s agricultural sector is growing impressively. The Comprehensive African Agriculture Development Programme (CAADP), an initiative of the African Union, reported in 2011 that the sector grew at more than 25%, surpassing the 6% target set for African countries. That growth rate made Angola’s agriculture the fastest growing on the continent, followed by Namibia’s at 15% growth rate.

More expatriate workers

Angola has also become a magnet to economic refugees from China and Portugal. “Definitely more Portuguese people are coming here in recent years, not only because of the bad financial situation in Europe but because Angola is one of the fastest-growing economies in the world,” observes Luis Ribeiro, a Portuguese national who runs a pizzeria in Luanda.

They are joining an influx that includes Chinese, Brazilian and, to a lesser extent, British investors. “We’ve always been one of the biggest communities, but we’re slowly being surpassed by the Chinese,” Mr. Ribeiro, told The Guardian, a British daily. “The Chinese are very resilient people and are prepared to do the donkey work that Portuguese and Angolans are not.”

Portuguese engineers, for example, may make €900 per month in Portugal, but they make four times more in Angola, reported the British Broadcasting Corporation (BBC). As a consequence of this reverse population flow, Luanda, Angola’s capital, “has overtaken Tokyo as the world’s most expensive city to live in for expatriates,” according to the American news channel, CNN.

Chinese investors are heavily involved in Angola’s large-scale public works such as roads, rails and other infrastructure. But critics say these investors do not create sufficient jobs because they bring most of their workers from China. In 2008 alone, the Angolan consulate in China issued more than 40,000 visas to Chinese workers, reports the bimonthly global affairs journal, World Affairs. For example, the China International Trust and Investment Corporation employed 12,000 Chinese workers and only a handful of Angolans during the peak of the Kilamba Kiaxo social housing development project in Luanda. In addition, the journal states that while the majority of Chinese in Angola work in the construction sector, thousands later branch out into real estate, retail, street hawking, etc.

Future prospects

In 2013 the Angolan economy weakened because of lower-than-expected oil spending and mismanagement of the public debt. But the AEO report predicts that with increasing diversification, the non-oil sector could expand by 9.7% and the oil sector by 4.5% in 2014.

Worried about the uneasiness among its population over growing inequality amid rapidly rising economic growth, the government is now taking steps to improve the lives of its citizens. There are ongoing investments in electricity, water and transport. As part of the infrastructure-for-oil trade agreement between China and Angola, rail infrastructure is expanding. To create more jobs, the government has introduced a new foreign exchange currency law for the oil industry and reformed the regulations governing the mining sector. Introduced in November 2012, the law also cuts business taxes from 35% to 25%, which in return has led to significant investments by companies including diamond producers De Beers and Sumitomo Corp. Both companies are currently developing an ammonia and urea plant. This year, Angola’s central bank plans to de-dollarize the foreign exchange market to limit the use of foreign currency in local transactions. In the past, most oil receipts were conducted offshore; the new laws require transactions to be handled onshore.

But Angola needs more sound policies to attract investors to all sectors, not just diamonds and oil, experts say. Currently, the World Bank’s “Ease of Doing Business” report ranks Angola 179 out of 189 countries. This low ranking has to change for the economy to live up to the expectations of its 21 million people.

This article appears in the August 2014 edition of Africa Renewal, published by the United Nations.

Related News

IMF and EAC team up to develop finance data

The East African Community (EAC) and the International Monetary Fund (IMF) have come together to help regional states in compiling finance statistics for their different governments.

Once done, the initiative will assist the EAC partner states meet the fiscal data requirements associated with the East Africa Monetary Union (EAMU) Protocol.

Speaking about the initiative, the EAC deputy secretary in charge of planning and infrastructure, Dr Enos Bukuku, said: “The intervention is timely in facilitating production of robust statistical data required for the establishment of the regional monetary Union and transition to EAC single currency by 2024”.

Mr Bukuku noted that GFS will be compiled in accordance with internationally agreed methodological standards, would not only provide the region with an important framework for comparing, analysing and evaluating fiscal policy, but also an opportunity to improve government and public sector performance.

Experience

Mr Barredo Capelot, the director of the Government Finance Statistics and Quality Directorate in Eurostat, while sharing lessons from the European experience that may be relevant for East Africa, said: “Solid and comprehensive fiscal statistics are essential for regional integration and preserving macroeconomic stability.”

EA monetary union

The leaders of five East African countries signed a protocol last November laying the groundwork for a monetary union within 10 years that they expect will expand regional trade.

Heads of state of Uganda, Kenya, Tanzania, Rwanda and Burundi, which have already signed a Common Market and a Single Customs Union, say the protocol will allow them to progressively converge their currencies and increase commerce.

In the run-up to achieving a common currency, the EAC nations aim to harmonise monetary and fiscal policies and establish a common central bank. Kenya, Uganda, Tanzania and Rwanda already present their budgets simultaneously every June.

Related News

Nigeria aims to boost competitiveness and regional non-oil exports

“Some objectives of our trade agenda include: to achieve non-oil exports to ECOWAS from the present nine per cent to 20 per cent by 2015, with the ultimate goal of increasing the value of Nigeria’s recorded export to ECOWAS from $276 million in 2011 to $706 million in 2015,” declared Olusegun Aganga, Minister of Industry, Trade and Investment, while speaking at the seventh National Council on Industry, Trade and Investment held in Markudi, Nigeria end of August.

Aganga explains that this target was part of a larger strategic plan elaborated by the Nigerian Government aimed at increasing Nigeria’s non-oil as a proportion of total export from current five per cent in 2011 to 20 per cent by 2015, and 40 per cent in 2020.

“In the area of trade, I am glad to inform that we have just completed a new National Trade Policy and Strategy, which will soon be presented to the Federal Executive Council for approval,” he announced.

According to the Minister, this is the first time after 10 years that the country’s trade policy has been reviewed.

“For the first time in Nigeria’s history, we will have a trade policy that integrates with the industrial and investment priorities of the Nigerian people. Nigeria’s priorities for trade will facilitate job creation in Nigeria, and boost exports on non-oil products to new markets,” he said.

Efforts to shape a competitive industrial sector underway

Last week, President Goodluck Jonathan unveiled plans to pass laws that will support industrial competitiveness across various economic sectors.

Some sources indicate that the move is intended to tackle certain challenges being faced by the industrial sector with regard to policy inconsistencies.

“The task of industrialising our nation is a collective responsibility which will be pursued with vigour by all stakeholders. Necessary support structures and enablers are being put in place to make the industrial sector globally competitive,” said President Goodluck Jonathan, who was represented by Vice-President Namadi Sambo, at the yearly general meeting of the Manufacturers Association of Nigeria (MAN) in Lagos on 28 August.

“Prior to now, our country’s export consisted largely of raw material in their primary forms. The time has come to reverse this trend. We must boost our industrial capacity; create more jobs and wealth in the economy,” he added.

Related News

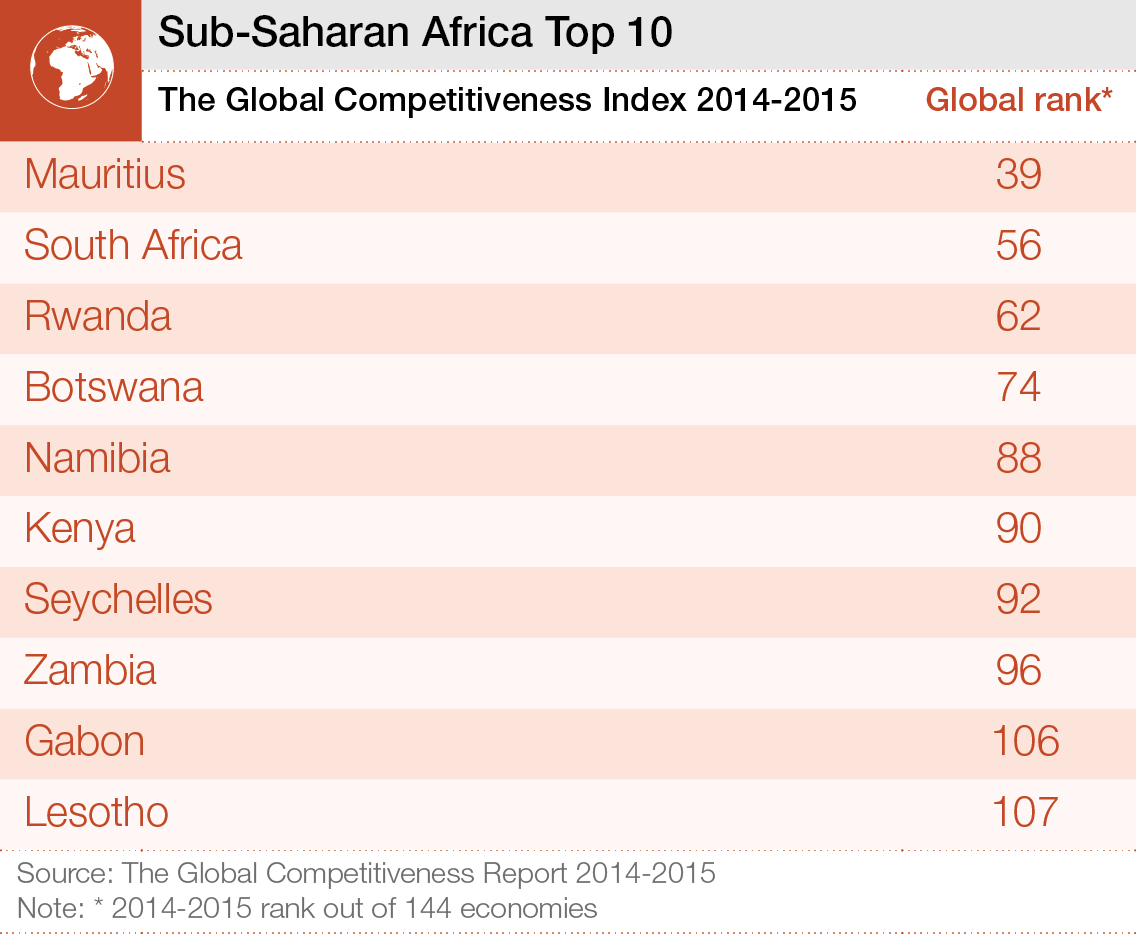

Top 10 most competitive economies in sub-Saharan Africa

The sub-Saharan African region has provided something of a silver lining in an otherwise broadly felt global economic downturn in recent years, according to the latest edition of the World Economic Forum’s Global Competitiveness Report, which assesses 144 economies. Sub-Saharan economies continued to register impressive growth rates of close to 5% in 2013 – with rising projections for the next two years – below only emerging and developing Asia.

Yet significant risks remain. More than half of the 20 lowest-ranked countries in the report are sub-Saharan, and many markets have insufficient infrastructure and poor levels of health and basic education. More than a decade of consistent high growth has not yet trickled down to all segments of the population and most economic activity takes place in the informal sector, which employs more than 80% of the population.

The region’s challenge is to turn high growth into inclusive growth and make the transition from agriculture-based economies to higher value-added activities.

The report ranks markets on 12 key measures that influence competitiveness, including infrastructure, education and innovation. The following are the top 10 performers in the region.

1. Mauritius consolidates its leading position in the region this year, benefiting from relatively strong and transparent public institutions, clear property rights, strong judicial independence and efficient government. The country’s transport and communications infrastructure is well developed by regional standards and it is making improvements to the efficiency of its markets. As income per capita rises and Mauritius moves up the value chain, more effort will be needed to develop its human capital by improving higher education and training, and mobilizing talent more efficiently, including increasing the share of women in the labour force.

2. South Africa ranks highly for certain aspects of quality of its institutions, including intellectual property protection, property rights, the efficiency of its legal framework and the accountability of private institutions. It also has an efficient market for goods and services. But the country’s strong ties to advanced economies have affected key macroeconomic indicators, and there remains a lack of public trust in politicians and government. Security is a significant concern, health indicators are poor, and higher education and training remains insufficient. Raising education standards and making the labour market more efficient will thus be critical if high unemployment rates are to be addressed.

3. Rwanda has a low GDP per capita by regional standards, but is recognized for its relatively strong institutions and reasonably efficient goods and labour markets. Limited access to finance is seen as the greatest obstacle to doing business in Rwanda, followed by the inadequate education of the work force, the lack of capacity to innovate and poor infrastructure.

4. Botswana’s greatest strengths are its relatively reliable and transparent institutions, efficient government spending, its labour market and low levels of corruption in regional comparison and a sound macroeconomic environment. Heavy reliance on diamond mining renders the country vulnerable to fluctuations in demand, and the quality of education is mediocre. Yet the biggest challenge facing Botswana is health: the country has one of the highest rates of HIV infection and one of the lowest life expectancies in the world.

5. Namibia continues to benefit from a relatively well-functioning institutional environment, with well-protected property rights, an independent judiciary and a fairly efficient government. The country’s transport infrastructure is also good by regional standards and financial markets are reasonably developed. However, infant mortality remains high and life expectancy is low, largely due to high rates of communicable diseases. School enrollment rates are low compared to other sub-Saharan economies. Namibia needs to improve its human resource base to diversify its economy and harness new technologies to improve productivity.

6. Kenya continues its upward trend from last year and is making improvements on almost all pillars of the index, most notably in the areas of market efficiency. Its economy is supported by financial markets that are well developed, and since the adoption of a new constitution in 2010, the government has become more efficient and levels of corruption are gradually decreasing. Education is generally good, though tertiary enrollment rates are low considering Kenya’s shift towards middle-income status. The country’s telephony and electricity infrastructure does not meet the needs of an economy that is the largest in East Africa. Health and security continue to be concerns.

7. Seychelles is one of only a handful of sub-Saharan economies to have noteworthy health and education systems. It has good infrastructure by regional standards, and significantly higher-than-average GDP per capita. Access to finance is the number one barrier to doing business in the country, along with a poor work ethic among the work force.

8. Zambia, like many of its neighbours, suffers from poor infrastructure and its health and primary education provisions are lacking. The country’s business sector is also troubled by a lack of access to finance and by corruption; there is also a lack of technological readiness. Zambia does, however, have better higher education and training provisions – although still low in international comparison – than some nearby economies, and a more efficient goods market.

9. Gabon’s macroeconomic situation is more positive than many other countries in the region, although on most other measures of competitiveness it ranks just as poorly. It also lacks good health and education services and suffers from high levels of corruption. Access to finance is the biggest hurdle to growth for businesses in Gabon, followed by the lack of good infrastructure and poor levels of education among the work force.

10. Lesotho has positive macroeconomic conditions have helped the country climb up the global rankings, though the provision of health and education is lacking, as is the case in many countries in this region. Access to finance and concerns about corruption are the biggest business challenges in Lesotho, along with the poor provision of infrastructure and an inadequately educated work force.

Read the Press Release here.

Related News

Jobs recovery to remain weak in 2015, says OECD

Unemployment will remain well above its pre-crisis levels next year in most OECD countries, despite modest declines over the rest of 2014 and in 2015, according to a new OECD report.

The Employment Outlook 2014 says that average jobless rates will decrease slightly over the next 18 months in the OECD area, from 7.4% in mid-2014 to 7.1% at the end of 2015. Almost 45 million people are out of work in OECD countries, 12.1 million more than just before the crisis. Globally, an estimated 202 million people are unemployed, with many more in low-paid and precarious jobs.

The Outlook also analyses the impact of the crisis on wages. It finds that real wage growth has come to a virtual standstill since 2009 and wages actually fell in a number of countries by between 2% and 5% a year on average, including in Greece, Portugal, Ireland and Spain.

This slowdown has been fairly evenly spread across the earnings distribution. However, slower real wage growth, and cuts in wages in some cases, result in real hardship for low-paid workers, the report warns.

“While wage cuts have helped contain job losses and restore competitiveness to countries with large deficits before the crisis, further reductions may be counterproductive and neither create jobs nor boost demand,” OECD Secretary-General Angel Gurría said while launching the report in Paris. “Governments around the world, including the major emerging economies, must focus on strengthening economic growth and the most effective way is through structural reforms to enhance competition in product and services markets. This will boost investment, productivity, jobs, earnings and well-being.”

Policy makers must ensure in particular that any further wage adjustments are not concentrated among low-earners. This is also relevant in countries where unemployment has fallen sharply since the crisis, such as Germany and the United States where the proportion of low-earners exceeds the OECD average and concerns one-fifth and one-quarter of workers respectively.

Mandatory minimum wages, which now exist, or are being implemented, in 26 OECD countries and a number of emerging economies, as well as in-work benefits, can help underpin the wages of low-paid workers.

Long-term unemployment has likely peaked but remains a major concern, says the report. Just over 16 million people – over one in three of the unemployed – had been out of work for 12 months or more in the first quarter of 2014, almost double the number at the start of the crisis.

In countries hardest hit, notably in Southern Europe, this has led to a rise in structural unemployment which will not be automatically reversed by a pick-up in economic growth, warns the OECD. Policy makers should prioritise efforts on helping the long-term unemployed back to work through more personalised job-search assistance and training programmes.

The Outlook also includes a new framework for assessing job quality, looking in particular at earning levels and distribution, job security and the quality of the work environment. It reveals wide differences between countries and between socio-economic groups, with youth and low-skilled having lower quality jobs. But it finds no evidence of a trade-off between job quantity and quality.

The Outlook highlights that an important dimension of job quality is the stability of the employment contract. In particular, efforts are needed to address the gap in employment protection between permanent and temporary workers. Temporary jobs are often not an automatic stepping-stone to a permanent job. In Europe, for example, less than half of temporary workers in a given year had full-time permanent contracts three years later.

It is encouraging that some countries have embarked on reforms in this area, says the report. These will take time to deliver results and it is essential that countries stay the course. Others should follow their lead. In emerging economies, informal employment looms large and major efforts are needed to promote job creation in the formal sector with adequate employment protection, while broadening the scope and coverage of social protection.

The jobless outlook for 2015 diverges widely among countries, with unemployment falling but still remaining very high in Spain (around 24%) and Greece (around 27%). The euro area will see joblessness decline to 11.2% at the end of 2015, from 11.6% in mid-2014, and above 10% in Italy, Portugal, the Slovak Republic and Slovenia. Unemployment is forecast to fall below 5% by the end of 2015 in Austria, Germany, Iceland, Japan, Korea, Mexico, Norway and Switzerland.

Related News

Corruption concerns taint burgeoning China-Africa trade

Africa’s mineral, timber and oil wealth has been highly sought – and fought over – for years, mainly by Western nations.

Today, though, Africa has become a strong trading partner for China, which surpassed the United States in 2009 and whose bilateral trade reached $210 billion in 2013.

In February, China’s President Xi Jinping hosted Senegal’s President Macky Sall and told him this fast-growing trade relationship with Africa “stands witness to the endlessly renewed vitality of Sino-African friendship, to the scale of the potential for co-operation” and “Sino-African strategic partnership.”

Chinese Premier Li Keqiang has announced plans to double bilateral trade with Africa to $400 billion a year by 2020.

But there are concerns some of that trade may be illicit.

China aggressively pursues and locks in economic opportunities using, according to analysts, suitcases full of cash when it is needed to close the deal. Another tactic used by Beijing is the “gift” of building and donating public works projects to African states that have raw materials and other things that China wants access to.

Summit addressed corruption

At a summit on Africa hosted by the Obama administration in August in Washington, corruption was high on the agenda. And, there were complaints that Beijing is not adhering to international anti-corruption conventions as it secures African business.

Meanwhile, U.S. corporations are bound by the U.S. Foreign Corrupt Practices Act and also the United Nations Convention Against Corruption (UNCAC). It is a crime for a U.S. entity to bribe or otherwise improperly gain business overseas. Because of that, the U.S.-Chinese economic competition in Africa can be described as an uneven playing field, analysts say.

“China is observing the United States and increasingly, many other wealthy western nations in the OECD [Organization for Economic Cooperation and Development] such as Germany enforce their anti-bribery laws,” said anti-corruption specialist Andrew Spalding at the University of Richmond. “China knows that this gives its own companies a competitive advantage. Accordingly, the more the west enforces anti-bribery laws, the greater the incentive for China not to enforce.”

Spalding said that “China has passed a foreign bribery prohibition to satisfy its requirements under the UNCAC, but UNCAC does not require enforcement. It would seem [that] neither cultural or economic factors, nor its membership in UNCAC, will pressure China to address foreign corruption.”

Corruption abounds in Africa

But China has a fertile corruption field in Africa. The continent has long suffered from rampant corruption.

When nearly 50 African leaders came to Washington in August, U.S. Vice President Joseph Biden was blunt in his remarks about corruption’s endemic prevalence on the continent.

“It’s a cancer in Africa,” Biden said. “It not only undermines but prevents the establishment of genuine democratic systems. It stifles economic growth and scares away investment. It siphons off resources that should be used to lift people out of poverty.”

Sub-Saharan Africa’s record suffers

Sub-Saharan Africa’s anti-corruption record is, overall, dismal.

The good governance group Transparency International’s latest global Corruption Perceptions Index, released in December 2013, reported that of the 20 most corrupt nations, half are in sub-Saharan Africa. Somalia came in at the very bottom, with Sudan, Chad and Eritrea ranking very low on the index.

Some in business circles have proposed that the United States scale back on its anti-corruption measures so as to enable American companies to more aggressively compete for African business.

Spalding stands steadfast against that idea.

“We cannot, and will not, repeal or scale back anti-bribery laws,” he said. “Foreign bribery prohibitions are here to stay.”

Spalding proposes “encouraging and assisting African governments in enforcing their own domestic bribery laws through joint enforcement and other forms of institution building.”

Joseph Siegle, with the Africa Center for Research Studies at the National Defense University in Washington, said illicit activity causes Africa to ultimately wind up with less .

“In a competition involving corruption,” he said, “there will always be actors willing to take the process one rung lower. This process would simply accelerate a race to the bottom. … With these actors, however, there is a risk premium on the part of African governments and business partners. There is often a poorer standard of performance, lower reliability and fewer avenues of recourse if there are disagreements over a contract.

“Business transactions with international partners upholding the rule of law, in contrast, are more apt to be sustainable and bring African businesses into other corporate networks, creating more opportunity over the short and long term,” he said.

William Fanjoy, with the U.S. Commerce Department’s U.S. Export Assistance Center, said American business attributes ultimately trump shady deals with others.

“U.S. companies can never ‘sweeten’ a deal in Africa, but they do offer African partners quality, responsiveness, financing, training and a long-term business relationship,” Fanjoy said. “After years of getting to know Chinese poor quality, we find that African companies are seeking out known American quality and reliability.”

African countries split on convention

While the United States and China, along with other nations, compete for Africa’s wealth and business, the continent has taken steps to address illicit economic activity.

The African Union in 2003 forged its Convention on Preventing and Combatting Corruption, which so far has been ratified by only 35 of the AU’s 54 members. Transparency International notes, however, that many of those signatory states “have not taken action to implement the necessary legal frameworks” supporting the AU’s Convention.

In 2012, a high-level anti-corruption working group was launched by the United Nations and the African Union. The goal is to find ways to curb illicit financial flows from sub-Saharan Africa, which the good governance group Global Financial Integrity says took 5.7 percent of the region’s collective GDP. This U.N.-AU group is expected to issue a report on its strategies for fighting illicit activity later in 2014.

Transparency International puts the responsibility for combatting corruption not only on those African states but also on the G20 – the world’s top 20 nations measured by their economies.

The group is calling for adopting mandatory reporting standards for the natural resource sector for all G20 countries, and country-by-country reporting by multi-national companies.

This would show where the money for oil, gas, logging and precious minerals goes. T-I says “only if leaders and civil society work together to enforce tough laws, and share information on illicit financial flows, will these latest commitments stop the pillaging of Africa.”

Africa attracts China

As for China, Africa is a continuing lure.

Former New York Times reporter Howard French, who wrote a book on the burgeoning China-Africa ties, reported that “China’s Export-Import Bank extended $62.7 billion in loans to African countries between 2001-2010, or $12.5 billion more than the World Bank.”

U.S. President Barack Obama said this summer that China can be good business for Africa, as long as trade is above board.

“My view is the more the merrier,” he said. When I was in Africa, the question of China often came up, and my attitude was every country that sees investment opportunities and is willing to partner with African countries should be welcomed.

“The caution is to make sure that African governments negotiate a good deal with whoever they’re partnering with,” Obama said. “And that is true whether it’s the United States; that’s true whether it’s China.”

Related News

Nigeria, Angola, South Africa lead in non-oil export to U.S.

Nigeria, Angola and South Africa were the three leading exporters to the United States in 2013 within the provisions of the African Growth and Opportunity Act (AGOA), according to data from the Nigerian Export Promotion Council (NEPC).

The data showed that Nigeria’s non-oil exports amounted to $3.0 billion (N486 billion) in 2013, representing a 15.9 per cent increase from the preceding year.

Also, non-oil exports from Nigeria to member countries of the Economic Community of West African States (ECOWAS) stood at $375 million (N60.7) in 2013, an increase of 20 per cent y/y.

According to the NEPC, cocoa emerged again as the leading non-oil export commodity, earning a total of $759 million during the period. Nigeria is ranked the fourth largest exporter of cocoa and its by-products globally.

The NEPC identified 14 key non-traditional products, which offer comparative advantage as cassava, shea products and potatoes.

Meanwhile, analysts at FBN Capital argued that for Nigeria to tap effectively into this segment, it is imperative that export commodities meet high standards in order to compete in the global market.

The FBN Capital stated: “There are multiple challenges for non-oil exporters. These include infrastructure deficiencies, high costs of production and weak logistics. A disturbing obstacle is the bad reputation associated with the products, which has led manufacturers in some segments to brand their goods other than ‘made in Nigeria’.”

It added: “Nigerian cuisine and the film industry (Nollywood) are areas the FGN intends to promote internationally. Taking a cue from China which has a strong presence globally in the export of its cuisine, the FGN will initially focus on cities such as London, Houston, Toronto and Johannesburg which have high diaspora populations.”

However, the FBN Capital predicted that a sustained growth ahead in export diversification due to developments in agribusiness, the cement segment and mining. It said: ”While substantial oil production losses may have raised the profile of non-oil exports, we should remember that Nigeria’s economic model is based on import substitution rather than export diversification.”

The FGN said its focus is the creation of employment through import substitution, preferably in the taxpaying formal economy, and the resulting foreign exchange savings from domestic production, for example, food crops, vehicles and petroleum products.”

The Federal Government recently unfolded plans to increase the country’s non-oil exports to the Economic Community of West African States from $276.5 million (N45.62 billion) in 2011 to $706.1million (N116.5 billion) by 2015.

Minister of Industry, Trade and Investment, Mr. Olusegun Aganga disclosed this during the 7th National Council on Industry, Trade and Investment in Markurdi, Benue State.

Related News

The AfDB releases its North Africa 2014 Report

The AfDB North Africa 2014 report focuses on inclusive growth, providing an overview of the AfDB’s activities in the region, along with a summary of the socio-economic situation in each of the five countries covered.

The African Development Bank (AfDB) has released its North Africa 2014 annual report, entitled Looking for inclusion (click here to download). This year’s report focuses on the pressing need for inclusive growth and development, as demonstrated by the uprisings experienced in several countries in the region in early 2011.

The report includes a brand new indicator, which measures the extent to which growth may be considered inclusive. The data reveal an important observation: in 2008-2010 (i.e. immediately before the “Arab Spring”), the five countries in the North Africa region (Morocco, Algeria, Tunisia, Libya and Egypt) posted below-average performance figures.

Tunisia was the highest-ranked country in the region, followed by Egypt, Libya, Morocco and Algeria respectively.

Despite improvements in the North African economies, both in real terms and in comparison with other developing nations, the report reveals deepening inequalities between social groups in two key areas: the labour market and regional variations. Furthermore, these very same inequalities are recognised as the main obstacles to inclusive growth. Genuinely inclusive growth would help to deliver fairer distribution of wealth between age groups, social classes and regions in these countries.

The report also reveals the existence of a two-tier labour market in the region, with a marked rift between the formal and informal sectors. Less than 50% of the working-age population is employed in the formal labour market, and the unemployment rate across the region stands at around 10% – considerably higher than the global average. Furthermore, people in the 15-24 age bracket are three times more likely to be unemployed than adults aged 25 and over. The unemployment rate is especially high among young, educated people and women. Indeed, women are twice as likely to be unemployed as men. The situation among young women (aged 15 to 24) is even worse, with people in this category three times more vulnerable to unemployment than women aged over 24.

In many cases, long-term unemployment leads to permanent withdrawal from the labour market. This, in turn, results in chronic poverty, marginalisation and, as demonstrated by the Arab Spring, social unrest.

A high proportion of North African workers are in unstable employment in the so-called “informal” sector, with no contract or social protection. Only 30% of workers in Morocco, 46% of workers in Tunisia and 50% of workers in Egypt have a contract of employment. Generally speaking, informal-sector workers experience substandard working conditions (compared with the formal sector) and receive extremely low wages, and in some cases no pay whatsoever.

However, the picture is not the same across North Africa. Income levels and other well-being indicators vary markedly by geographical location, including within individual countries. These differences are also reflected in the quality of public services and social welfare provision, as well as in private-sector employment opportunities and public-sector development assistance for the private sector.

The key message of the 2014 report is that the North African countries now have a historic opportunity, as the working-age population is set to continue growing until 2020. Provided that the region is able to sustain an effective labour market and attract sufficient investment, this population growth should help to deliver strong growth.

The AfDB remains one of the region’s key partners in its efforts to overcome these challenges. The Bank is currently supporting more than 100 projects in the region, funded by loans and grants totalling US $7 billion.

Related News

Improving regional integration in Africa

The resolution of outstanding issues under the Economic Partnership Agreements, among others, will no doubt facilitate regional trade in Africa, writes Eromosele Abiodun

In the years before the global financial crisis in 2008, global trade increased exponentially. While African countries benefited from this increase, their share in world trade has remained low. Africa’s export trade amounts to only about three per cent of world exports. This poor trade performance partly relates to trade protection outside Africa against African products, but it also stems from constraints that inhibit trade within Africa. With the expectation of a generally moderate recovery of the global economy and of world trade, it is even more important than before to foster African countries’ trade with economies both outside and inside Africa.

Experts have said rapid conclusion and resolution of the outstanding issues in the Economic Partnership Agreements (EPAs) negotiations are crucial to Africa’s medium-term prospects in both regional and international trade. Indeed, among the different measures that several advanced countries adopted in 2009 to curb the effect of the financial crisis, trade protectionism has been on the rise. Protectionism increased despite repeated assurances in the context of the G20 meetings in London, as well as in the context of World Trade Organisation (WTO) talks.

Often stimulus packages were geared to favour domestic sectors, such as through export support, or to favour buying, lending, hiring or investing in local goods and services. Such measures clearly discriminate against developing countries, including those in Africa, on several levels. Unfortunately, African governments lack the resources to curb the domestic impact of the crisis with the same type of measures. Also, African companies face unfavourable treatment precisely in markets where additional spending is being promoted. Hence, with these new measures African products easily face discriminatory treatment in relation to similar domestic products and services in developed countries, despite the general agreements about preferential treatment they may enjoy.

FG’s Task Force

To check the situation in the West African Sub-regional, the Federal Government of Nigeria recently set up a task force on trade facilitation in Nigeria with a mandate to remove all bottlenecks to trade between Nigeria and its neighbouring countries.

The Task force member comprises representatives of Ministries of Commerce Trade and Investment, Ministry of Finance and Ministry Transport. Others are: the Nigeria Customs Service (NCS), Nigeria Shippers Council (NSC), the Nigerian Port Authority (NPA), National Agency for Food, Drug Administration and Control (NAFDAC), the Standards Organisation of Nigeria (SON), Nigeria Quarantine Services (NQS), the Nigerian Police, the Central Bank of Nigeria (CBN) and Nigeria Road Safety Corps.

While on a visit to the Managing Director of Nigerian Export Import Bank (NEXIM), Mr. Roberts Orya recently, Chairman of the taskforce, Mr. David Adejuwon, said the body had taken proactive steps to identify what constitutes technical and physical barriers to movement of goods in the sub region.

He confirmed that there are about 35 check points during the day and about 50 checkpoints at night from Lagos to Seme border, hindering trade between both countries. This, he said, was against protocol that ECOWAS member countries signed to reduce it to three checkpoints.

According to him, all these have been impacting negatively on the country’s image and its competitiveness in the effort to attract foreign direct investment (FDI) into the country.

He pointed out that once the taskforce was able to remove those barriers in the border posts, it will go a long way to facilitate trade between Nigeria and other African States. He called for support and collaboration from NEXIM Bank to facilitate trade between Nigeria and other West African States.

Adejuwon on behalf of the taskforce sought for the support of NEXIM Bank in the provision of surveillance vehicles, trade facilitation workshop, sensitisation and public awareness as well as disseminating and publicising information on the operation of the Committee.

Orya had pointed out that Nigeria has the biggest market in Africa and there was need to reduce the multiple checkpoints, which have militated against free movement of goods in the sub-region.

He added that Nigeria, being a strategic nation in both economic and political institution owned by ECOWAS, needed to explore the sub region market, saying that NEXIM Bank has started deepening payment system by supporting Nigerian exporters. Despite his promises at the time, nothing much has been done to show seriousness on the part of government.

NANTS Tasks ECOWAS

However, despite Nigeria’s efforts, some African countries especially those in West Africa are not taking adequate steps to ensure hindrances in achieving regional integration are removed.

Recently, the National Association of Nigerian Traders (NANTS) charged Economic Community of West African States (ECOWAS) leaders to address the poor implementation of the ECOWAS Treaty and Protocols, especially the protocol on free movement by member states as a major hindrance in achieving regional integration objectives.

Also, the association, in a message and agenda to the speaker of the ECOWAS parliament, pointed out that there is poor adherence to the provisions of the protocol on Rights of Residence and Establishment.

It added that the problem is further complicated by the lack of access to the ECOWAS Court of Justice by community citizens on violations of their socio-economic rights under the Protocols and the ECOWAS Treaty itself.

“NANTS has been canvassing for the compliance of member states with these laws, but has also noted that the role of the ECOWAS Parliament in cases like this is unfortunately limited to merely advisory as it lacks law making powers necessary for the review of sub-optimal provisions in a Protocol,” the association said.

NANTS added that, “It is therefore our expectation that your administration as the Speaker of the Parliament would strengthen the extant weak powers of the ECOWAS Parliament, empower the ECOWAS Commission to be more efficient where necessary, enhance the laws of the Community by possibly infusing strict sanction mechanisms thereunto and effectively capacitate even the National Parliaments and other relevant institutions as fundamental organs in the enforcement of laws and or dispensation of justice and integration in West Africa.”

It urged the Speaker to take immediate action and review the laws establishing the ECOWAS Court of Justice, with a view to broadening its mandate and jurisdiction in line with other regional Courts such as the European Court.

NANTS said it expected that the ECOWAS Parliament would be instrumental to driving the achievement of the ECOWAS Vision 2020 objectives, particularly of transforming ECOWAS from ‘an ECOWAS of States to an ECOWAS of people.’

“In this regard, we envisage that the Community Development Programme (CDP) would be institutionalised as a veritable instrument for realising the objectives of the Vision 2020, which is endorsed by the Authority of Heads of States and Governments of ECOWAS. This is essential given that the CDP seeks to anchor regional policies, programmes and plans shaped by the citizens themselves rather than erstwhile practice of approval of wholly-Consultant-drawn-policies and programmes,” NANTS said.

“Basically, the CDP seeks to rather institute a ‘bottom-up’ approach to policy making in the region as opposed to a ‘top-bottom’ approach. As representative of the community citizens, NANTS believes that the ECOWAS Parliament should play a more visible role in the entire transformation process.

“We would therefore cherish an opportunity to not just brief you in details on the CDP process but also explore options for the immediate involvement of the Parliament in the CDP process. Indeed, we wish to emphasise that NANTS believes that the ECOWAS Parliament is indispensable and crucial for the actualisation of the ECOWAS vision 2020,” NANTS stressed.

Trade Performance in Africa

Meanwhile, the Organisation for Economic Cooperation and Development (OECD), in a recent report on trade performance in Africa, noted that one critical reason for Africa’s relatively poor trade performance is the weak diversification of African trade both in terms of trade structure and destination.

Most African economies, OECD said, depend on very few primary agricultural and mining commodities for their exports and mainly import manufactured goods from advanced countries.

“As the traditional markets in advanced countries are expected to grow less than markets in emerging Asian and Middle East countries as well as markets within Africa, enhancing trade relations with these more dynamic markets is key. Several inefficiencies also constrain trade within Africa. These inefficiencies include poor transport infrastructure such as maintenance and connectivity, political instability and lack of security within and among several regions, and intra-African trade barriers.

“Despite progress, intra-African trade is still low, representing on average around 10 per cent of total exports. Many factors contribute to the low trade performance, including the economic structure of African countries, which constrains the supply of diversified products; poor institutional policies; weak infrastructure; weak financial and capital markets; and failure to put trade protocols in place, “OECD said.

OECD in the report pointed out that Africa’s trade performance is extremely low compared with other trading blocs outside the continent.

It said: “For example, trade within the Association of South East Asian Nations (ASEAN) accounts for about 60 per cent of their total exports. The same is true for the countries belonging to the North American Free Trade Agreement (NAFTA) area, whose intra-regional trade accounted for 56 per cent of total exports. It is no wonder that the economies of ASEAN and NAFTA are doing remarkably well.

“Barriers to external and internal trade in Africa are numerous, despite Africa’s determination to dismantle trade restrictions in order to create a common market within the framework of regional and sub-regional agreements. These barriers are mostly the consequences of the above-mentioned factors. In addition, 15 of the countries in Africa are landlocked,” it said.

These countries, the report stressed, continue to face serious challenges in having direct access to the sea adding that lack of territorial access to the sea, remoteness and isolation from world markets, and high transit costs continue to impose serious constraints on the overall socio-economic progress of landlocked developing countries.

The situation, it said, has pushed many landlocked developing countries to higher poverty levels.

“Currently, the African Union Commission is focusing on its Minimum Integration Programme (MIP), consistent with previous AU Conferences of African Ministers in Charge of Integration (COMAI). This focus underscores the need for rationalising resources and harmonising the activities and programmes of Regional Economic Communities (RECs). The MIP is in line with a broader undertaking, namely the realisation of the African Economic Community (AEC), as envisaged in the Abuja Treaty and the Constitutive Act of the African Union, “the report said.

UNECA, AFDB’ Efforts

It added that, “Furthermore, the African Union Commission, together with the United Nations Economic Commission for Africa (UNECA), the African Development Bank (AfDB) and the RECs, has also made notable progress in establishing three-pan-African financial institutions: the African Central Bank, the African Monetary Fund and the African Investment Bank.

“The AfDB is also supporting the institutional setup for improving macroeconomic and financial convergence on the continent. It has also focused on the preparation of a continental Programme on Infrastructure Development in Africa (PIDA), as well as on the development of an EPA template to be used as a guide in the negotiations for EPAs. This last aspect will be particularly conducive to greater coherence between the different EPAs being negotiated and other regional agreements, which are already in place.”

Ebola Changes the Equation

Efforts to get African countries working together to enhance economic integration may have suffered a huge blow following the recent outbreak of the Ebola Virus Disease. Following embargo on movements to curb the spread of the epidemic economies around West Africa are already suffering. For instance, it is estimated that Nigeria may lose $3.5 billion to the Ebola epidemic by December this year, if nothing is done to contain the spread of the deadly disease.

In a recent report released, the Chief Executive Officer, Financial Derivatives Company Limited, Mr. Bismarck Rewane said the fear of the disease had affected economic activities significantly.

According to him, the sectors of the economy mostly affected by the fear of the disease are aviation, tourism and hospitality, trade, medical and agriculture.

He added, “Analysing these sectors’ contribution to the Gross Domestic Product shows that Nigeria may lose about $2 billion in the first quarter of the outbreak. The chance of the outbreak going into a second quarter is very slim; which could extend the loss to $3.5 billion.”

The Boko Haram insurgency had been the headline news in Nigeria until July 25 when it was confirmed that Ebola was imported into the country.

Since then, fear, panic, disbelief and frustration have set in as economic, particularly in Lagos, have gradually slowed down. Global rating agency, Moody’s, has announced that the outbreak of Ebola in Nigeria can lead to serious disruptions in some sectors of the economy with negative financial consequences.

The World Health Organisation has also reported that the Ebola crisis is vastly underestimated as the reported cases and deaths do not reflect the scale of the crisis.

About 1,069 persons have died in the affected countries, out of which three are Nigerians and 198 other persons are currently under quarantine in the country.

Impact on West Africa

Teneo Intelligence estimates that economic growth in Liberia, Sierra Leone and Guinea may reduce by two percentage points.

In other words, Sierra Leone’s growth rate in 2014 may not exceed 12 per cent instead of the initial forecast of 14 per cent. Liberia, Sierra Leone and Guinea have a combined Gross Domestic Products (GDP) of approximately $13 billion, equivalent to 2.5 per cent of Nigeria’s GDP.

Rewane further stressed that a small part of the Nigerian economy was already benefiting from the Ebola scare. These include shop owners selling sanitizers.

He, however, said a larger part was experiencing losses.

He said, “Air transport was 0.09 per cent of Nigeria’s GDP in the first quarter and the second most used this means of transportation after road. Since the outbreak of Ebola in West Africa, several airlines including Arik Air, Asky, British Airways and Emirates have suspended flight operations to and from any of the Ebola affected countries.

“Saudi Arabia also suspended giving out visas to Muslim pilgrims from West African countries. Serious screening for Ebola has also begun at several international airports before passengers are allowed to board an airplane. We expect revenues in the aviation sector to plunge downwards, which would affect both the airlines and the support industry (handling companies, oil marketers, catering, duty free shops, etc.)”

He further said, “Hospitality and tourism preliminary information shows that many hotel and airline bookings in Lagos have been cancelled by in- bound travellers due to Ebola scare. This is not surprising since India and Greece have openly advised their citizens to avoid non-essential travel to Nigeria and other Ebola-affected countries. It is estimated that restaurant visits in Lagos have already declined by 50 per cent.”

“Trade in the first quarter contributed 17.35 per cent to Nigeria’s GDP. Trade and investment flows are critical to the external sector of this vibrant country and the West African region. The region enjoys almost a custom union with common external tariff and movement of visitors without visas. Since movement of people is restricted in and out of the affected regions, fewer goods will be equally transported. Air transportation is very critical to trade.

“Hence, a reduction in the number of international flights literally means a reduction in international trade flows. Domestic trade is also likely to be negatively affected significantly if the disease spreads,” he stated.

Related News

Africa needs to diversify its economy

Investor enthusiasm for Africa is gaining traction. As the home to two economic powerhouses, the continent offers growth and the opportunity of lucrative return on investment.

In the past, Africa’s economic growth was primarily driven through extractive enterprises. But in the past decade success from manufacturing, agriculture and natural resources has shown that with the right partnerships in place, Africa is poised to outgrow its reputation as a market driven only by consumption and commodities.

To take this next step and to reach Africa’s consumers we need a common market and economies of scale. It is evident that there is a need for further regional integration and intra-African trade for the diversification of the continent’s economy. This in turn will spur on wealth creation across all existing sectors, in all countries.

This point was reinforced by former public enterprises minister Malusi Gigaba (the current home affairs minister) in his keynote address at this year’s American Chamber of Commerce South Africa annual general meeting, held in Johannesburg in March. Gigaba expanded on the importance of regional integration for Africa – especially in an environment where developed markets are experiencing an extended downturn.

A highlight in his speech was that Africa’s growth prospects remained positive and that there was significant optimism about the development of the continent. He pointed out that Africa needed to incorporate partnerships with other leading emerging markets around the globe in order to strengthen inter-regional ties in trade, investment and business, and also achieve success through increased economies of scale.

Early last month the US government hosted its US-Africa Summit in Washington, DC. The event was widely hailed as a success. The summit was geared towards strengthening ties between Africa and the world’s most powerful nation. In attendance were 40 out 47 African heads of state (including President Jacob Zuma and Nigerian President Goodluck Jonathan) as well as senior representatives from major US companies.

Along with US President Barack Obama’s support of the renewal of the African Growth and Opportunities Act (Agoa) $33 billion (R352bn) worth of deals was made through the “Doing Business in Africa” programme.

Agoa was signed into law by former US president Bill Clinton in 2000 and expires in 2015 (it was originally set to expire in 2008 but was extended). The trade agreement allows duty-free export access of thousands of products from eligible sub-Saharan African countries into the US. A renewal of another 15 years is anticipated.

This conference has been regarded as an important platform to strengthen trade and investment ties between the US and Africa, to enhance co-operation on peace, safety and security, and to discuss ways to foster progress towards inclusive and sustainable development in Africa.

One of the biggest priorities on the African agenda remains achieving peace and stability on the continent, and South Africa has proved that there is an abundance of economic benefits that come with a strengthened democracy that is complemented by strong institutional and regulatory frameworks.

The 2013/14 Global Competitiveness Report of the World Economic Forum (WEF) found that countries that were highly innovative and had strong institutions topped international competitiveness rankings. The report also showed that of the Brics (Brazil, Russia, India, China and South Africa) nations, South Africa was second in its competitiveness after China.

Another finding in the report was that in sub-Saharan Africa, Mauritius was the region’s most competitive economy, with South Africa in second place. Among low-income economies, the report showed that Kenya had made the biggest improvement – moving up 10 places to 96th position.

Imagine if these economies collaborated for partnered growth and development.

The WEF report shows us that there is a need for more insightful efforts to improve Africa’s competitiveness. A good starting point is through the diversification and opening up of its markets.

The fact is the numbers don’t lie. They point to an optimistic future ahead. A key enabler will be regional integration, and in particular the role of trade agreements as the key building blocks of that integration. There are a number of trade agreements or trade arrangements in Africa – the Common Market for Eastern and Southern Africa (Comesa), the Southern African Development Community (SADC), the Southern Africa Customs Union, the Economic Community of West African States, the East African Community (EAC) – but most remain on paper and in so doing are unable to unleash the true potential of Africa’s vast human capital and resources.

African leaders should now embrace the opportunity and renewed political will to build on these trade agreements and demonstrate their benefits by implementing them in practice.

The challenges faced by businesses operating in Africa are well documented: limited energy security, irregular banking frameworks, protecting intellectual property, and achieving a balance between aid and trade. However, these challenges are not unique to emerging markets and they are not without solutions.

Similar to other emerging markets, such as south-east Asia and Latin America, Africa can present boundless prospects for its investors. Business needs to approach Africa differently because the continent is a study in diversity. Yes, there is common opportunity like growing consumerism, rapidly developing technology, globalisation and access to information. But different countries present different opportunities and the most sustainable way to tap into these is through strengthened free trade agreements and regional integration.

South Africa, for example, where democracy is 20 years old – boasts one of the world’s most sophisticated financial systems and has the capability to use its data and institutions to grow its economy.

On the other hand Kenya, the largest economy in east Africa, is classified as a low-income market but it continues to strengthen its democracy, open its market to international investors, encourages entrepreneurship and is exploring new ways to improve its socio-economic prospects.

A recent media report (Financial Mail, February 7) indicates that Kenya exports goods valued at approximately 3 billion Kenyan shillings (R355 million) to South Africa and South Africa exports goods worth about 70 billion Kenyan shillings to Kenya.

Based on this, preferential trade agreements could come by way of a proposed tripartite agreement between Comesa, the EAC and the SADC, to establish a free trade area by 2015.

In anticipation of the promise of these agreements, and due to improved relations between the countries, a number of South African entities have established business interests in Kenya. These include Tiger Brands, Old Mutual, FirstRand and Distell.

Africa has many of these one-off case studies, but global investor consensus is that Africa has the potential and opportunities that can redefine it as a market that grows organically in all its sectors, instead of primarily depending on consumption to drive development.

The 2013 African Economic Outlook shows that sustainable development in Africa rests on diversification and investment in human capital. The report also shows that African countries must provide the right conditions to allow untapped resources such as minerals and natural wealth to optimise job creation opportunities.

The perceived “deterrents” to investing in Africa can be managed only when confronted by all stakeholders on the continent. It requires the understanding of each country’s specific dynamics, its policies and frameworks, and what each country can do to implement and help achieve intra-regional trade.

Markets will be accessible, jobs created, infrastructure development accelerated and the continent’s economy will be beneficial to more people and companies – not just for multinationals like Ford but for companies of all sizes that wish to contribute towards development and diversification.

Jeff Nemeth is president and chief executive of Ford Motor Company of Southern Africa and president of the American Chamber of Commerce in South Africa.

Related News

Global growth at risk from slow reform progress

The health of the global economy is at risk, despite years of bold monetary policy, as countries struggle to implement structural reforms necessary to help economies grow, according to the Global Competitiveness Report 2014-2015 released today by the World Economic Forum.

In its annual assessment of the factors driving countries’ productivity and prosperity, the report identifies uneven implementation of structural reforms across different regions and levels of development as the biggest challenge to sustaining global growth. It also highlights talent and innovation as two areas where leaders in the public and private sectors need to collaborate more effectively in order to achieve sustainable and inclusive economic development.

According to the report’s Global Competitiveness Index (GCI), the United States improves its competitiveness position for the second consecutive year, climbing two places to third on the back of gains to its institutional framework and innovation scores. Elsewhere in the top five, Switzerland tops the ranking for the sixth consecutive year, Singapore remains second and Finland (4th) and Germany (5th) both drop one place. They are followed by Japan (6th), which climbs three places and Hong Kong SAR (7th), which remains stable. Europe’s open, service-based economies follow, with the Netherlands (8th) also stable and the United Kingdom (9th) going up one place. Sweden (10th) rounds up the top-10 of the most competitive economies in the world.

The leading economies in the index all possess a track record in developing, accessing and utilising available talent, as well as in making investments that boost innovation. These smart and targeted investments have been possible thanks to a coordinated approach based on strong collaboration between the public and private sectors.

In Europe, several countries that were severely hit by the economic crisis, such as Spain (35th), Portugal (36th) and Greece (81st), have made significant strides to improve the functioning of their markets and the allocation of productive resources. At the same time, some countries that continue to face major competitiveness challenges, such as France (23rd) and Italy (49th), appear not to have fully engaged in this process. While the divide between a highly competitive North and a lagging South and East persists, a new outlook on the European competitiveness divide between countries implementing reforms and those that are not can now also be observed.

Some of the world’s largest emerging market economies continue to face difficulties in improving competitiveness. Saudi Arabia (24th), Turkey (45th), South Africa (56th), Brazil (57th), Mexico (61st), India (71st) and Nigeria (127th) all fall in the rankings. China (28th), on the contrary, goes up one position and remains the highest ranked BRICS economy.

In Asia, the competitiveness landscape remains starkly contrasted. The competitiveness dynamics in South-East Asia are remarkable. Behind Singapore (2nd), the region’s five largest countries (ASEAN-5) – Malaysia (20th), Thailand (31st), Indonesia (34th), the Philippines (52th) and Vietnam (68th) – all progress in the rankings. Indeed, the Philippines is the most improved country overall since 2010. By comparison, South Asian nations lag behind, with only India featuring in the top half of the rankings.

To boost its economic resilience and keep the economic momentum of past years, Latin America finds its major economies still in need of implementing reforms and engaging in productive investments to improve infrastructure, skills and innovation. Chile (33rd) continues to lead the regional rankings ahead of Panama (48th) and Costa Rica (51st).

Affected by geopolitical instability, the Middle East and North Africa depicts a mixed picture. The United Arab Emirates (12th) takes the lead and moves up seven places, ahead of Qatar (16th). Their strong performances contrast starkly with countries in North Africa, where the highest placed country is Morocco (72nd). Ensuring structural reforms, improving the business environment, and strengthening the innovative capacity so as to enable the private sector to grow and create jobs are of key importance to the region.

Sub-Saharan Africa continues to register impressive growth rates close to 5%. Maintaining the momentum will require the region to move towards more productive activities and address the persistent competitiveness challenges. Only three sub-Saharan economies, including Mauritius (39th), South Africa (56th) and Rwanda (62nd) score in the top half of the rankings. Overall, the biggest challenges facing the region is in addressing human and physical infrastructure issues that continue to hamper capacity and affect its ability to enter higher value added markets.

“The strained global geopolitical situation, the rise of income inequality, and the potential tightening of the financial conditions could put the still tentative recovery at risk and call for structural reforms to ensure more sustainable and inclusive growth,” said Klaus Schwab, Founder and Executive Chairman of the World Economic Forum.

Xavier Sala-i-Martin, Professor of Economics at Columbia University in the US, added: “Recently we have seen an end to the decoupling between emerging economies and developed countries that characterized the years following the global downturn. Now we see a new kind of decoupling, between high and low growth economies within both emerging and developed worlds. Here, the distinguishing feature for economies that are able to grow rapidly is their ability to attain competitiveness through structural reform.”

Background

The Global Competitiveness Report’s competitiveness ranking is based on the Global Competitiveness Index (GCI), which was introduced by the World Economic Forum in 2004. Defining competitiveness as the set of institutions, policies and factors that determine the level of productivity of a country, GCI scores are calculated by drawing together country-level data covering 12 categories – the pillars of competitiveness – that collectively make up a comprehensive picture of a country’s competitiveness. The 12 pillars are: institutions, infrastructure, macroeconomic environment, health and primary education, higher education and training, goods market efficiency, labour market efficiency, financial market development, technological readiness, market size, business sophistication, and innovation.

Read The Global Competitiveness Report 2014-2015 here.

Related News

Impact of trade policy on poverty examined in new UNCTAD book

A novel collaborative approach between academics and policymakers examines the impact of trade policy on poor people in eight developing and transition countries in a new book published by the UNCTAD Virtual Institute (Vi).

“Trade Policies, Household Welfare and Poverty Alleviation: Case Studies from the Virtual Institute Academic Network” is the outcome of a three-year capacity-building project for researchers in developing and transition countries.

The findings of the project will be presented by the authors and their policymaker partners to government representatives in Geneva 8–10 September, during the Virtual Institute’s Seminar on Trade and Poverty, with the book launched on the afternoon of 8 September.

The book takes the form of eight case studies from the Philippines, the Former Yugoslav Republic of Macedonia, Argentina, China, Costa Rica, Peru, Nigeria and Viet Nam.

The studies address the relationship between globalization and poverty in the context of two broad themes. One set of studies examines the welfare consequences of the recent increases in global food prices. The other set of studies examines the welfare effects of trade policy and exchange rate changes.

The researchers used a methodology based on household-level surveys to assess short-term effects of global price changes or trade policies on household consumption, production and labour income, and subsequently, on household welfare and poverty. The country studies are based on actual situations faced by developing countries, such as recent increases of global food prices, a change in import tariffs or exchange rate appreciation. An overview of the analysis and conclusions of individual studies are available in Table 1.

“The research yielded several insights about the relationship between changes in commodity prices or trade policies, and poverty,” the book’s editor Nina Pavcnik, a professor of economics at Dartmouth College, said.

“For example, while the rural poor tend to be harmed by increases in the price of rice in the Philippines, they benefit from an increased price of maize in the former Yugoslav Republic of Macedonia. This difference stems from the fact that the rural poor in the Philippines tend to be net consumers of rice, while the rural poor in the former Yugoslav Republic of Macedonia are net producers of the commodity that experienced a large price increase. Such assessments can provide a useful tool to help policymakers enhance the potential positive impact of trade on poverty.”

The trade and poverty project from which the book emerged began with a 12-week online course developed specifically for researchers and university lecturers from developing and transition countries. The objective of the course was to provide participants with the empirical tools needed to assess the impact of trade and trade-related policies on poverty and income distribution so that they may assist policymakers in the design of pro-poor trade policies.