Blog

COVID-19 and the gender-related economic consequences for Africa

The world is struggling to cope with the economic and health consequences of the COVID-19 pandemic. However, its impact on women, and in particular the economic impact on women in sectors where they are predominantly employed, is often lost in the noise of the crisis. Such sectors include the informal sector, cross-border trade, subsectors of hospitality, healthcare (particularly nursing), and clothing and textiles. Moreover, the social and economic impact of this pandemic will be felt for many years yet. It has the potential to be particularly pronounced in Africa given the inability to adequately socially distance in crowded urban settlements, limited access to safe water, undernourishment, strained and underfunded healthcare systems, and underlying health conditions such as tuberculosis (TB) and HIV/AIDS (ISS, 2020).

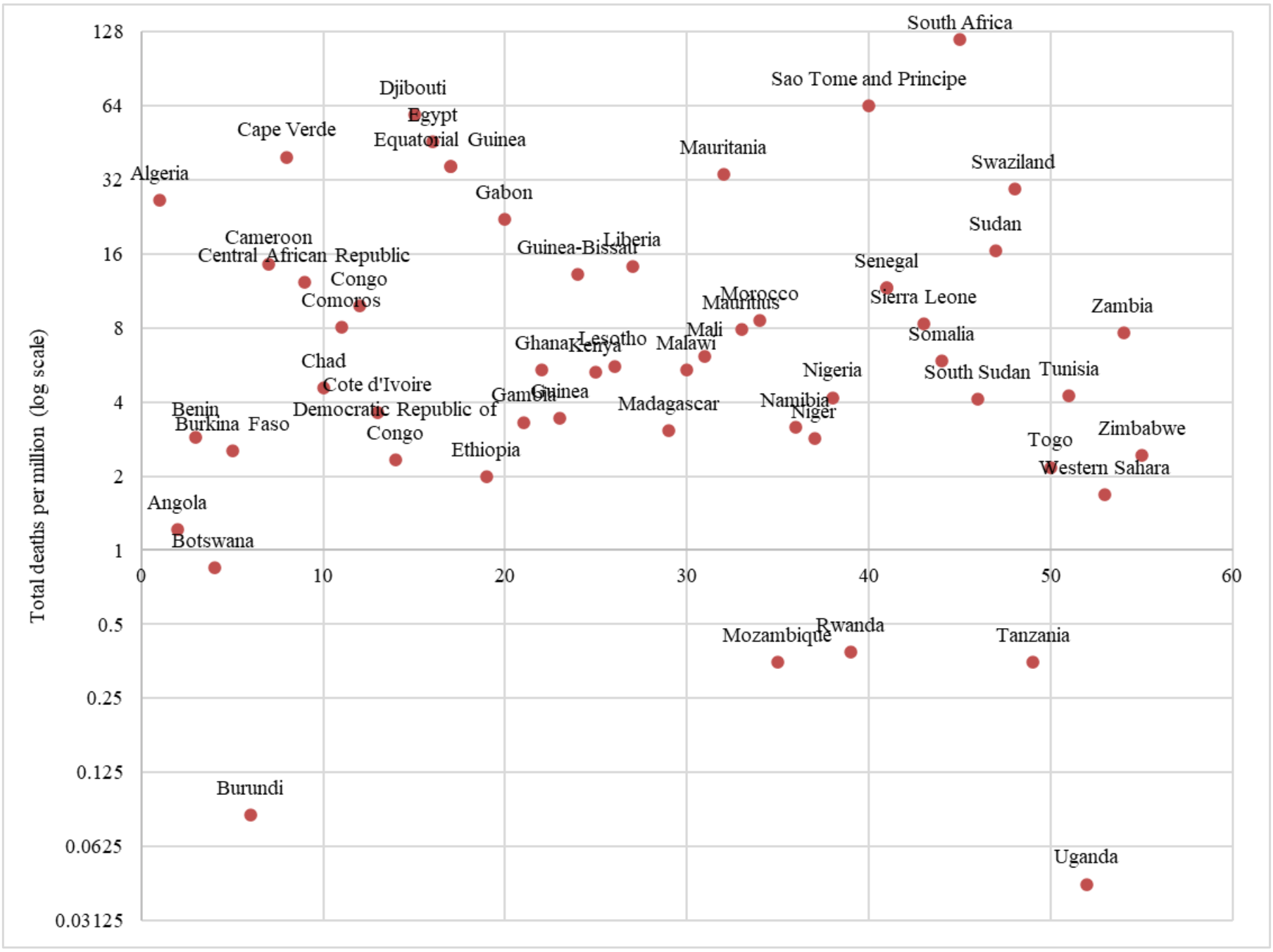

Figure 1 shows that the majority of African countries have reported considerably less than 32 COVID-19 related deaths per million (although some caution is warranted given possibilities of underreporting and sparse data). South Africa is the worst affected African country, with currently 120 deaths per million (and arguably better reporting). Although the mortality rate has to date been relatively low on the continent, the economic impact of COVID-19 is expected to be considerably more prominent.

Figure 1: COVID-19 mortality rate for African countries (as at 28 July 2020)

Source: Our World in Data, 2020

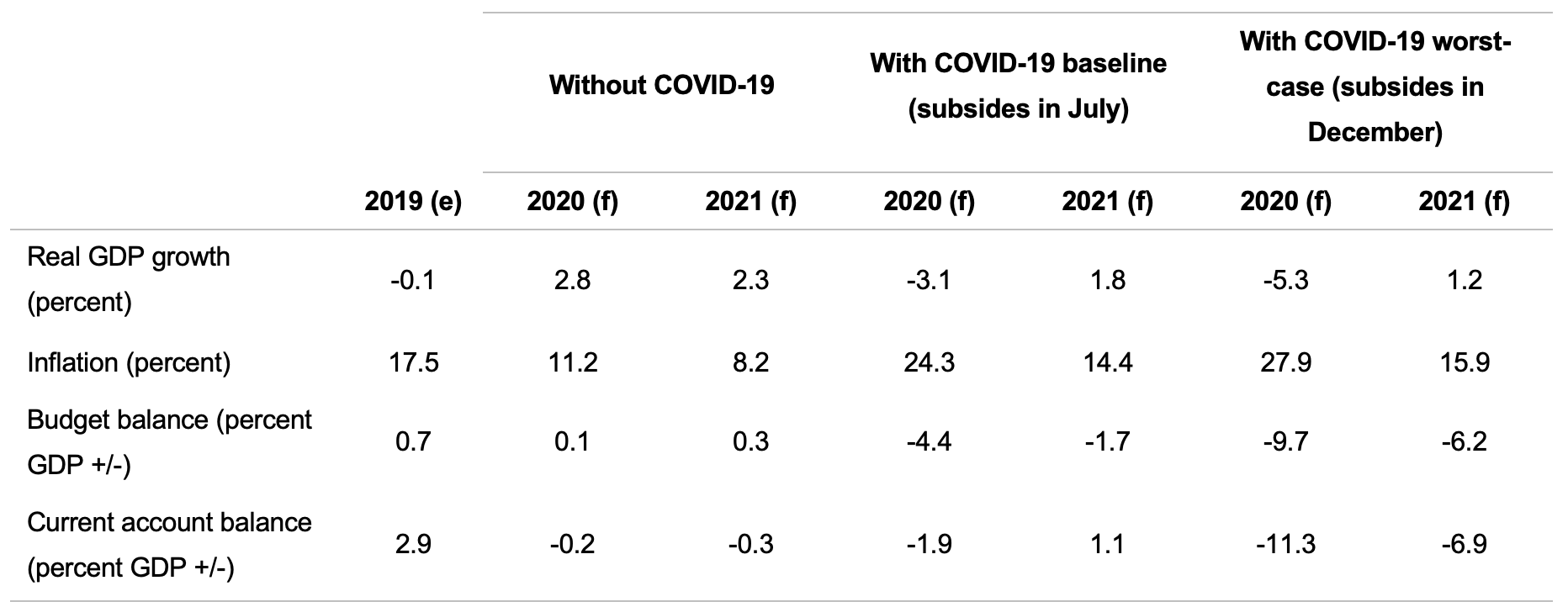

The African Development Bank has estimated the impact of COVID-19 given various macroeconomic indicators for the continent (See Table 1). Without COVID-19, the continent was estimated to grow at a robust rate of 2.8% real GDP in 2020 and 2.3% in 2021. Under the baseline and optimistic scenario of the pandemic subsiding by July, this real growth rate is estimated to be -3.1% for 2020 and 1.8% in 2021. Under the worst-case (and until a vaccine is found it remains optimistic) scenario, real GDP growth is projected to decline a considerable -5.3% in 2020 and increase by a modest 1.2% in 2021. The other macroeconomic indicators show strong declines, with the current account balance being of considerable concern.

Table 1: Estimated macroeconomic impact of COVID-19

Source: African Economic Outlook, 2020

Beyond the macroeconomic outlook, COVID-19 presents many gender-based challenges. Besides a marked increase in gender-based violence and a decrease in access to sexual and reproductive health, COVID-19 is expected to affect women significantly more than men (WEF, 2020), especially through widening existing financial inequality between men and women. The pandemic will also potentially worsen maternal healthcare (prenatal and postnatal) as well as have a significant impact on maternal and infant mortality – both Sustainable Development Goals pillars. As an example, the UN Population Fund projected that the 2014-16 Ebola epidemic in Liberia, Guinea and Sierra Leone led to 120 000 preventable maternal deaths – a figure 10 times more than those killed by the disease itself (11 310 fatalities). Furthermore, we must also be cognizant of the additional knock-on effects leading to declines in vaccination programs against TB, yellow fever, and measles as well as declines in attendance to prenatal and postnatal appointments. This has the potential to lead to additional deaths and developmental delays far outstripping the direct health consequences of COVID-19. Therefore, access to and availability of prenatal and postnatal care, as well as access to modern contraception must remain a priority.

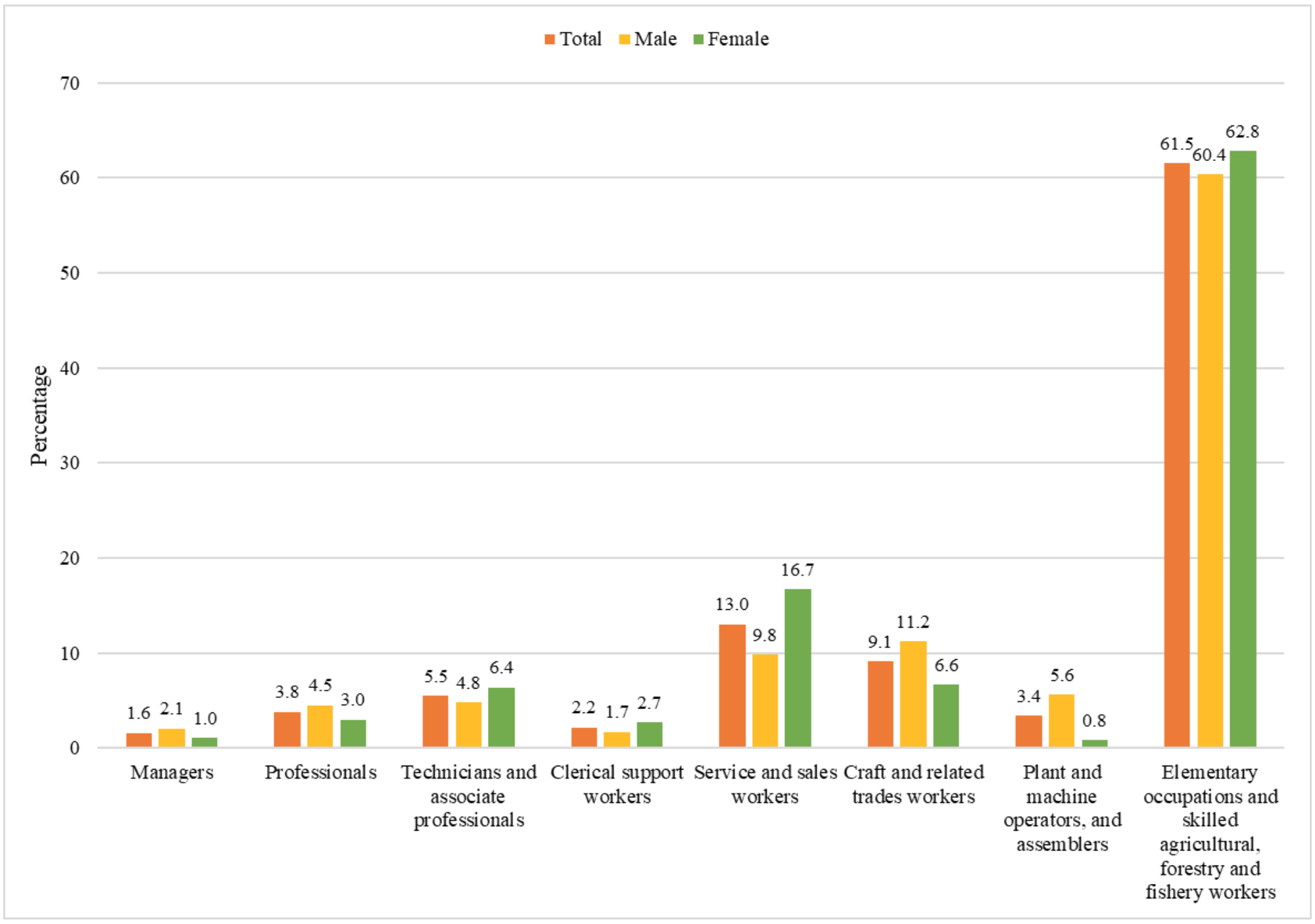

Figure 2: Employment distribution by occupation (2020)

Source: ILO modelled estimates, 2020

COVID-19 is also expected to exacerbate the financial inequality between men and women, as globally women are most likely to hold precarious or vulnerable jobs. These are often the first to be lost due to economic shocks. Figure 2 highlights the distribution of employment by occupation by gender for Sub-Saharan Africa. It is derived from ILO modelled estimates for 2020. It is clear that a vast majority of males and females are employed in elementary occupations and skilled agricultural, forestry and fishery work. Moreover, slightly more females as a percentage of total females are employed within these occupations. Also, males outnumber females in managerial and professional occupations, which should be more resilient to COVID-19 shocks. Females make up the bulk of service and sales workers; positions which are expected to be severely affected by COVID-19 due to suppressed economic activity and consumer demand. Other important occupations for females include craft and related trades as well as technicians and associate professionals. Another concern is, of course, the medical frontline, where women are estimated to make up over 70% of the world’s global health and social sector workforce. These professionals face the dual challenge of contact in high-risk environments and a lack of personal protective equipment (PPE).

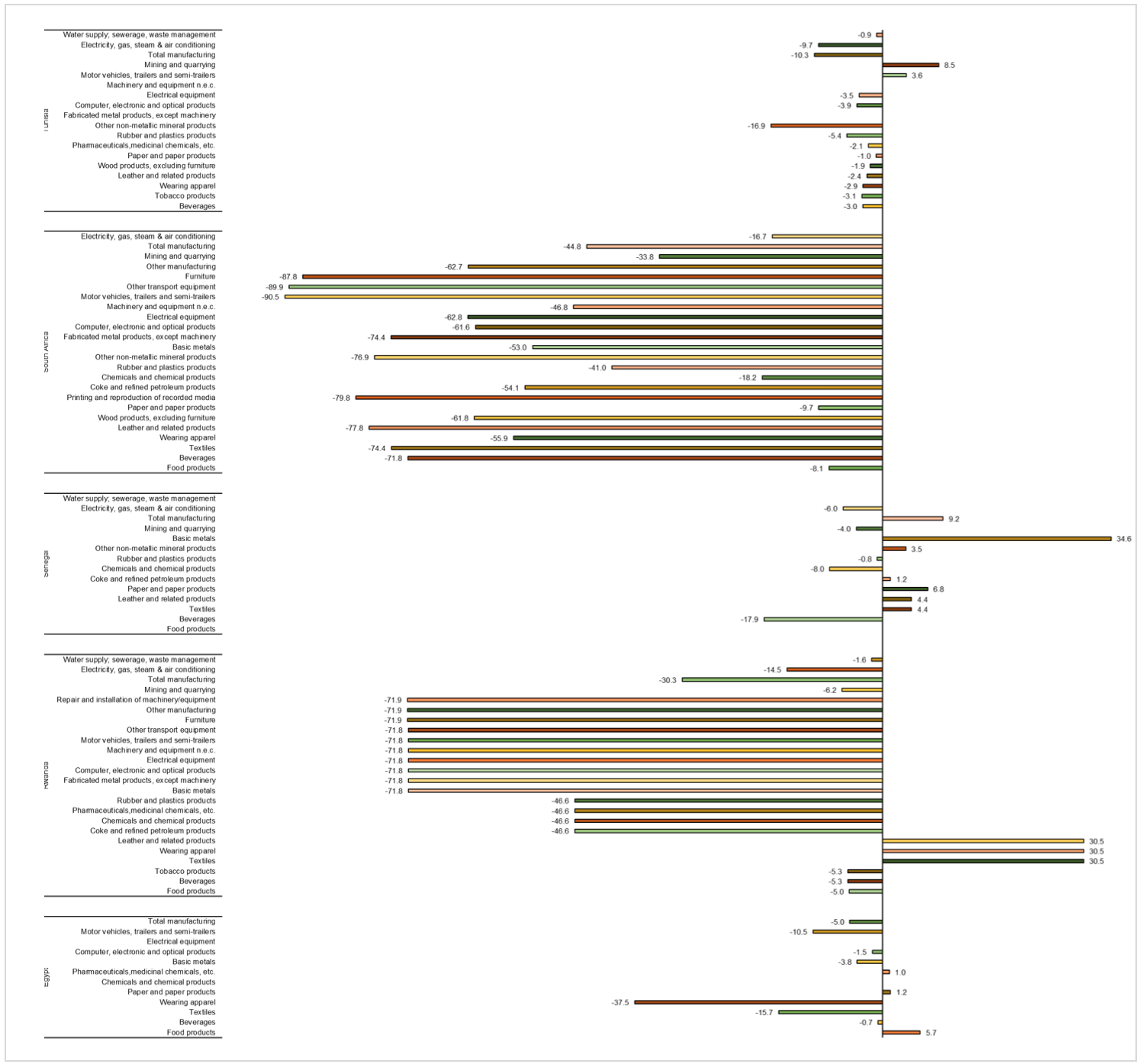

Figure 3: Percentage growth for industries in selected African countries (March-April 2020)

Source: UNIDO, 2020

Figure 3 shows the change in the seasonally adjusted Index of Industrial Production (IIP) for selected African countries between April and March 2020. Here the impact of COVID-19 on industries on the continent is clear – the vast majority of industries within these countries saw a substantial decrease in the IIP. Total manufacturing for Tunisia, South Africa, Senegal, Rwanda, and Egypt saw declines of 10.3%, 44.8%,4%, 30.3% and 5% respectively over the period. This is nothing short of catastrophic. Industries employing significant proportions of women (leather and related products, wearing apparel, textiles, pharmaceuticals, computer, electronic and optical products) saw greater than average declines in total manufacturing IIP for the selected countries. South Africa was particularly hard hit with huge declines of 77.8%, 55.9% and 74.4% in leather and related products, wearing apparel and textiles, respectively. Rwanda is the lone exception which saw growth in the IIP for textiles, wearing apparel and leather and related products.

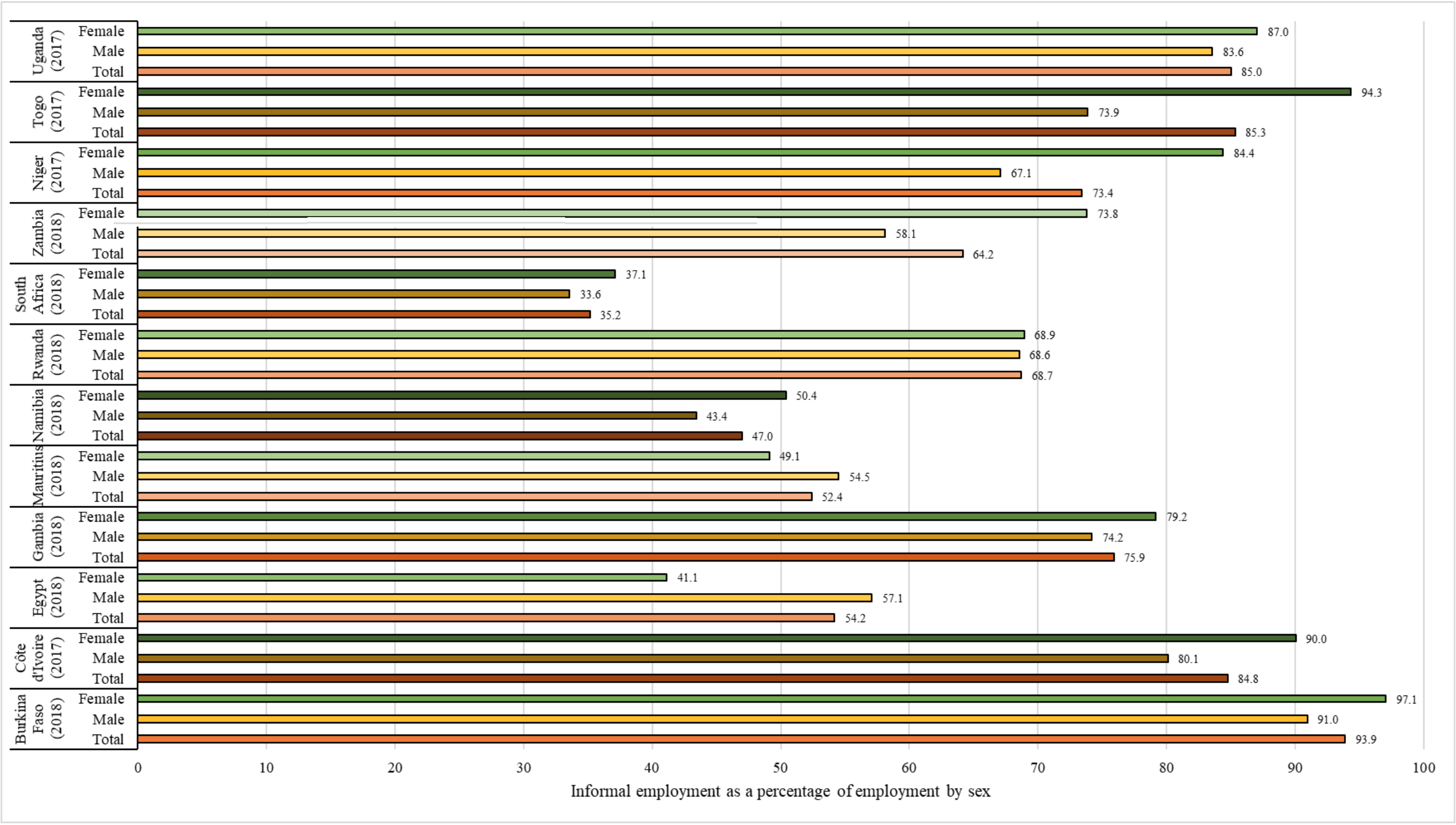

Figure 4: Informal sector employment by gender

Source: ILO, 2020

The informal sector will also be considerably hard hit by COVID-19. Women are actively involved in this sector throughout the continent, but data on this sector is notoriously scarce and unreliable for Africa. However, we present the latest available data from the ILO for selected African countries in Figure 4. This shows the percentage of people employed in the informal sector (Total), percentage of females employed in the informal sector (Female), and percentage of males employed in the informal sector (Male).

What is immediately clear from Figure 4 is that the informal sector in Africa plays a major role in employment creation. Only in South Africa (35.2%) and Namibia (47%) does the informal sector account for less than 50% of total employment. Furthermore, the informal sector appears to be a major conduit for female employment (and empowerment) with most of the countries shown exhibiting far greater female participation (as a percentage of total female employment) in the informal sector. Only in Rwanda is male and female participation relatively equal, whilst only in Egypt and Mauritius do we see a greater percentage of male employment in the informal sector.

Not only does the informal sector play a major role in empowerment in Africa, but it also provides women with the opportunity to earn an income and gain a greater level of financial independence and support for their families. However, the COVID-19 pandemic has a great negative potential to erase the gains made in this sector as people are confined to their homes, and the fear of spreading the virus weighs heavily on citizens and governments minds. There certainly will be restricted movement of individuals and lower demand for the goods and services of the informal sector as the movement of people is severely limited. This will have a substantially negative impact on the livelihoods of millions of women and families in the region, particularly given the absence of labour (employment and social) protection ordinarily afforded in the formal sector as well as a lack of social security from government and tax assistance as such informal enterprises are not formally registered.

Finally, COVID-19 presents an opportunity for governments to reflect and consider how best to extend equal economic participation to women. There are considerable challenges to overcome, and as pointed out above, women are considerably more vulnerable to the negative consequences of the pandemic in terms of financial inequality and industries of highest participation share. However, levels of women’s entrepreneurship, leadership, and the percentage of women trading in the informal economy contributing to the overall economy are positives to foster on the road to a stronger and faster recovery. Post-COVID-19 presents governments and policymakers the opportunity to level the playing field through targeted investment, encouraging equal representation in leadership and the expansion of social protections to harness the vast potential (UN, 2020) of the neglected half of the continent.

About the Author(s)

Leave a comment

The Trade Law Centre (tralac) encourages relevant, topic-related discussion and intelligent debate. By posting comments on our website, you’ll be contributing to ongoing conversations about important trade-related issues for African countries. Before submitting your comment, please take note of our comments policy.

Read more...